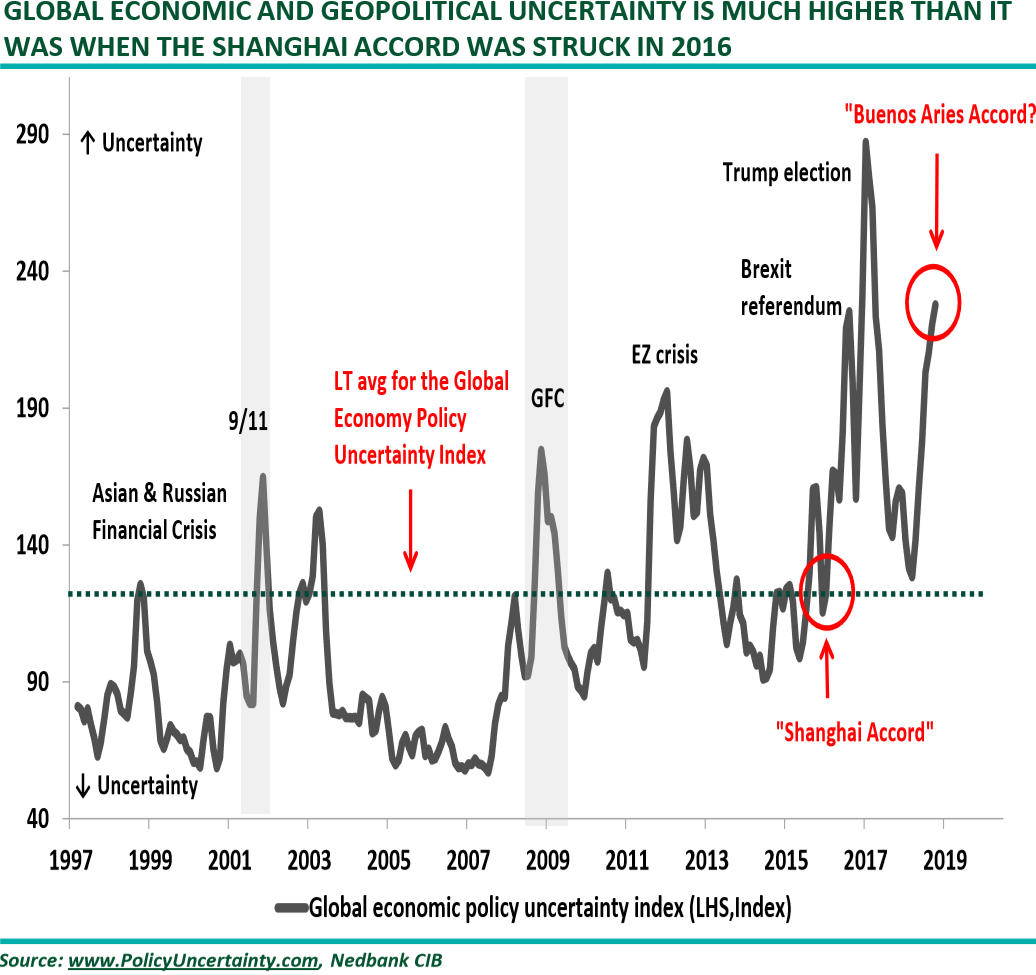

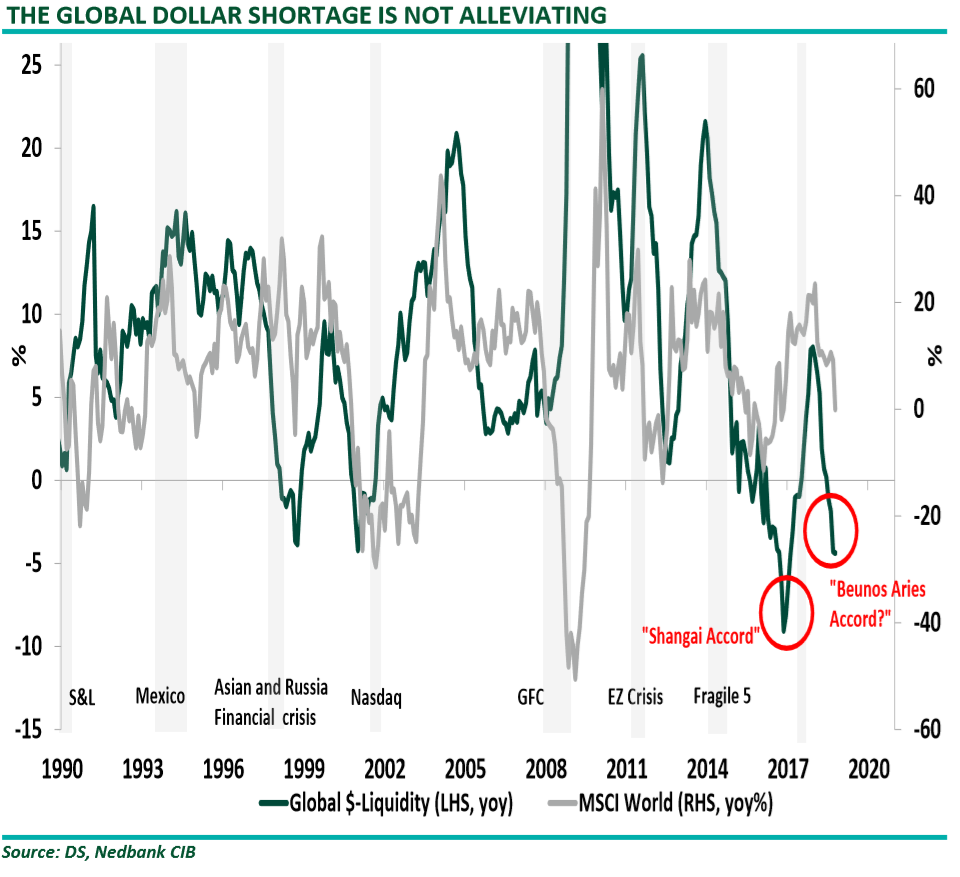

There we go again, a binary outcome awaits as we head into G-20 meeting. Mehul Daya and Neels Heyneke of Nebank explains is their Macro Strategy note “At the G20 meeting in Shanghai in February 2016, policy makers pledged to boost economic growth and restore stability to financial markets. This was in the midst of global economic growth faltering and as financial markets were grappling with heightened volatility amid fears of deflation. Stock markets were under pressure, the US bond was rallying and EMs experienced large outflows. The strong US dollar tightened global financial conditions considerably.As a result of the globally coordinated effort by policy makers, i.e., the “Shanghai Accord”, a risk-on phase ensued. This led to a weaker US dollar (easing financial conditions), triggering an outperformance in many risk assets, in particular, EMs.

G-20 might have lost its relevance as leaders cant even agree on joint communique ,but we need another shanghai accord to ease high levels of economic policy/geopolitical uncertainty as can be seen in the chart . There is another issue of contracting dollar liquidity as FED continues to unwind its balancesheet

Nedbank concludes “We are sceptical about whether a “Buenos Aires Accord” could be re-engineered again, for the following reasons:

1. Rise in geopolitical tensions

2. Global US dollar shortage

3. Expectations of tighter monetary policy by global Central Banks

4. Contraction in China’s credit cycle

Their Investment recommendation: “We have been underweight risk assets in 2018 and advise investors to remain conservative in their asset allocation towards risk assets going into 2019, unless there is consensus among global policy makers to boost liquidity“.

My two cents. A G-20 accord even remotely like shanghai will give new lease of life to markets and possibly a new high in US markets irrespective of FED stance and rate hike in its December policy.

Afterall availability of LIQUIDITY is more important than the cost of liquidity.

An interesting writeup – thought would share…

https://www.bloomberg.com/amp/opinion/articles/2018-11-29/fed-s-powell-proves-bonds-are-smarter-than-stocks

I read this article and frankly bonds are a much better indicator because of the size of market . Equity is more emotional. I am of the view that bonds would have well till Powell is doing his job and will go rogue when he goes soft. so watch out for steepness in the curve with bond market revolting because of higher US deficit