The above is the title of an article in The New York times which caught my attention.

I believe that we are moving from Just in Time to Just in case and it is going to get ugly out there on corporate profitability. I also think that companies will not be able to pass on this increased cost as consumers are already going on a purchasing strike.

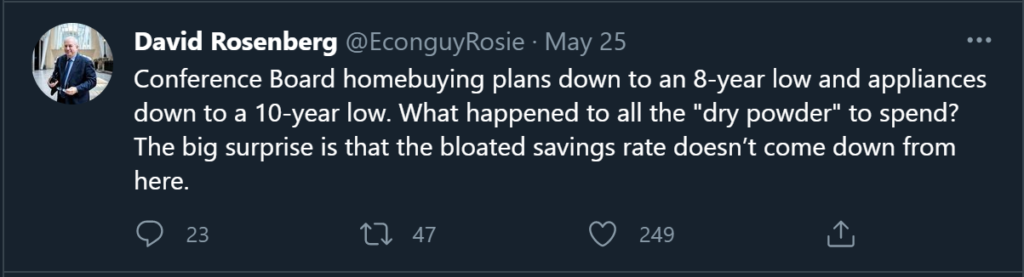

consider this tweet quote from David Rosenberg

Now back to the article

“In the story of how the modern world was constructed, Toyota stands out as the mastermind of a monumental advance in industrial efficiency. The Japanese automaker pioneered so-called Just In Time manufacturing, in which parts are delivered to factories right as they are required, minimizing the need to stockpile them.

Over the last half-century, this approach has captivated global business in industries far beyond autos. From fashion to food processing to pharmaceuticals, companies have embraced Just In Time to stay nimble, allowing them to adapt to changing market demands, while cutting costs.

But the tumultuous events of the past year have challenged the merits of paring inventories, while reinvigorating concerns that some industries have gone too far, leaving them vulnerable to disruption. As the pandemic has hampered factory operations and sown chaos in global shipping, many economies around the world have been bedeviled by shortages of a vast range of goods — from electronics to lumber to clothing.

In a time of extraordinary upheaval in the global economy, Just In Time is running late.”

read the full article below by creating an account

For the past few years, I have been critical of the Ponzi Sector. To me, these are businesses that sell a dollar for 80 cents and hope to make it up in volume. Just because Amazon (AMZN – USA) ran at a loss early on, doesn’t mean that all businesses will inflect at scale. In fact, many of the Ponzi Sector companies seem to have declining economics at scale—largely the result of intense competition with other Ponzi companies who also have negligible costs of capital.

I recently wrote about how interest rates are on the rise. If capital will have a cost to it, I suspect that the funding shuts off to the Ponzi Sector—buying unprofitable revenue growth becomes less attractive if you have other options. Besides, when you can no longer use presumed negative interest rates in your DCF, these businesses have no value. I believe the top is now finally in for the Ponzi Sector and a multi-year sector rotation is starting. However, interest rates are only a small piece of the puzzle.

Conventional wisdom says that the internet bubble blew up due to increasing interest rates. This may partly be true, but bubbles are irrational—rates shouldn’t matter—it is the psychology that matters. I believe two primary forces were at play that finally broke the internet bubble; equity supply and taxes. Look at a deal calendar from the second half of 1999. The number of speculative IPOs went exponential. Most IPOs unlock and allow restricted shareholders to sell roughly 180 days from the IPO. Is it any surprise that things got wobbly in March of 2020 and then collapsed in the months after that? Line up the un-lock window with the IPOs. It was a crescendo of supply—even excluding stock option exercises and secondary offerings. The supply simply overwhelmed the number of crazed retail investors buying worthless internet schemes. Back in 2000, I used to joke that in a scenario where a company wanted to raise equity capital, but insiders wanted to sell, they’d both dump shares on the market—but the insiders would get out first. What do you think that did to share prices as both parties fought for the few available bids?

However, the proximate cause of the internet bubble’s collapse was when people got their tax bills in March and had to sell stocks to pay their taxes in April. What’s the scariest thing in finance? It’s when you owe a fixed tax bill from the prior year, yet your portfolio starts declining. You start selling fast to stop the mismatch. Trust me, I’ve been there. Tax time is pushed back a bit this year, but it is coming.

Admittedly, All 3 Are Full Of Shit…

I bring this all up, because the SPAC market is in the process of detonating and it will take the Ponzi Sector with it. Let’s look back at the internet bubble. A VC firm would IPO 4 million shares at $20, the stock would open at $50 and end the day at $100. Everyone chased it to get in. Then the brokers would upgrade it and the CEO would go on TV. With a 4 million share float, it was easy to manipulate the shares higher. Often, the newly IPO’d company would level out well north of $100 a few weeks later. It was a virtuous cycle and everyone played the game. What was left unsaid was that there were another 46 million shares held by management and VCs and these shares would hit the market 180 days later. At first, the market absorbed the new supply so no one showed concern—then the market choked. I wrote about this when talking about the QS unlock. This process is about to repeat, but now with the odd nuances of SPACs.

A typical SPAC deal involves a few hundred million dollars raised for the SPAC trust—this is the only real float. Then a few hundred million more is raised for the PIPE—these guys are buying at $10 because they plan to flip for a gain as soon as the registration statement becomes effective—which is often a few weeks after the deal closes. When a company merges with a SPAC, billions in newly printed shares are given to the former owners—those shares start to unlock a few months later in various tranches. Finally, the promoters behind the SPAC get to sell. When you look at a pre-merger deal trading at a big premium to the $10 trust value, you’re looking at an iceberg. There might be ten or twenty restricted shares for every free trading share—all of these guys desperately want out. It’s a game theory exercise—how do you find enough bag-holders without destroying the price? Hence, part of why the current price is determined by an artificially restricted float and the unlocks come in tranches. As restricted shares come unlocked, the promoters lose control of the float and the house of cards collapses.

Part of the hilarity of SPACs is that the promoters claim to be aligned with shareholders because they exit last in terms of unlock tranches. What’s left unsaid is that their shares have almost a zero-cost basis—hence when they sell out at well under $10, it’s still all profit. Meanwhile the acquired company insiders often have an even lower cost basis because they founded the company at a negligible cost, there were bidding wars by various SPACs which drove the valuations to nosebleed levels and the acquisition targets are often mostly fake anyway.

When there were only a few high-profile SPACs, this supply could be absorbed—very much like 1999 with internet IPOs. This made people unconcerned about the supply deluge. Now we’re starting to enter the teeth of the unlock window from 2020 vintage SPACs. There are literally tens of billions a week in stock flooding the market—except there’s no natural shareholder base for these things. There are only so many retail punters who wake up and want to buy a fake “green” company with no revenue and no path to revenue—much less profits. When everyone is making money in ESG themed frauds, it draws fresh capital into the bubble and helps inflate things. When the losses start stacking up, capital leaves—yet there are still hundreds of billions of dollars in SPAC shares waiting to be unlocked and dumped. Remember how their cost basis is effectively zero? The insiders and promoters literally do not care what price they sell at. It is the internet bubble all over again.

You may wonder how the SPAC bubble will infest the rest of the Ponzi Sector. It comes down to collateral and shareholder bases. On the collateral side, much of the Ponzi Sector bubble is built on leverage. That could be margin debt or YOLO call options, but it’s all leverage. As asset values decline, brokers will force punters to de-lever. This will lead to waves of selling, leading to more forced selling. As for YOLO call options? They’re not exactly firm bedrock when it comes to a bubble. The SPACs and the Ponzi Sector are all tied together, because they all have the same shareholder base. As these owners take losses, they’ll be forced to sell “best in class” Ponzis like Tesla (TSLAQ – USA).

Back in 1999, there were various firms that enabled the internet bubble. They had handshake agreements that they’d be given IPO allocations, on the understanding that they wouldn’t sell—in fact, they frequently bought more in the open market, often at many times the IPO price. This allowed VC firms to tighten up already tight floats and manipulate shares higher. As these firms outperformed, they had inflows, allowing them to continue buying the same companies and pushing shares higher—leading to more inflows. It was a virtuous cycle and many firms worked together as wolf-packs in the same names. When redemptions came, these firms were forced to sell and the process unwound—except it was unusually speedy to the downside as the share prices were artificially propped up.

I have my sights on a certain ETF for this cycle. Go through ARK Innovation ETF’s (ARKK – USA) position list, go through all the quasi-affiliated firms that have copied this position list. All these firms have surprising concentrations in the same names. When it comes tumbling down, you don’t want to own any of these positions—especially the ones where ARKK owns more than 10% of the shares. You won’t want to own positions that are owned by people who own ARKK type positions as they’ll be forced sellers too. You want to be as far away from the Ponzi Sector ecosystem as possible.

I don’t know when it’s going to blow, but if I’m right that the top is in, the deluge isn’t too far off. Bubbles are highly unstable—if they’re not inflating, they’re usually bursting—there isn’t really a middle option. I think the past few weeks are more than a simple pullback—the losses from the SPAC bubble are going to dent the Ponzi Sector psychology. With this in mind, I took my long book way down over the past few weeks (including my GameStop (GME – USA) straddle for a nice score). That said, I don’t have shorts because this is still “Project Zimbabwe.” If I’m wrong, so be it. I’ll do just fine on my Event-Driven book. Besides, 2021 has already been a pretty spectacular year for me.

Turning to Grayscale Bitcoin Trust (GBTC – USA), it now trades at a surprising discount to NAV—partly due to the shareholder base’s cross-ownership of other Ponzis. I had told myself that I’d hold GBTC through the sort of shake-outs that Bitcoin is famous for. However, this week when I went through my position sheets, I asked myself if I really needed this much exposure to a Ponzi Scheme, after repeatedly reminding myself that the Ponzi Sector is detonating. As a result, I booked a bit more than half of my GBTC exposure—taking all of my cost basis out and then some. I’m not going to say that my dismount in the mid-$40s was graceful—I wish I had sold it with a $5 handle, but I’m up 4-fold in 8 months and it still feels like quite the victory. For now, I intend to keep the rest of the position, though I’m moving my stop up once again. Will Bitcoin get caught in the downdraft? Who knows; I don’t need a position limit while I find out.

But Kuppy, what about “Project Zimbabwe?” Won’t the Ponzi Sector go up with everything else? My good friend, Kevin Muir, over at The MacroTourist (if you aren’t subscribed, you are missing out), likes to say that we’re “experiencing a period of rolling bubbles.” History says that once a bubble pops it rarely re-inflates. I believe that the Ponzi Sector bubble is now past the apex. With losses stacking up, the bubble psychology will break and people will start looking at things rationally again. How does this square with my “Project Zimbabwe” paradigm? It squares perfectly. We will have a rotation and some other asset class will bubble up next. I suspect it is one where increased cost of capital and massive government interference shuts off supply growth. Could inflation beneficiaries be next? I want exposure where the puck is going, not where it’s overstayed its welcome for far too long. On this pullback, that is where my focus will be.

Why an inflationist? Rising energy prices despite lockdown is a prelude, of sorts, to rising inflation since transformation of energy underpins all economic activity.

Shortage of energy and also semiconductors, for example, sets us up for higher prices.

Negative real rates due to central bank actions has prompted investors to shift from cash and bonds to equities and commodities.

Where are bond yields headed? It will depend chiefly on central bank policies. Will they fully embrace yield curve control to keep the cost of government borrowing in check and in the process destroy the value of their currency? Or will they let the bond yields go towards more natural levels? The Fed is likely to go with the first option.

US treasuries have come to be regarded as “anti-fragile”: they are understood to perform well when the rest of the components of an investor’s portfolio do badly. However, the current macro setup does not support this view, and these bonds can come crashing down when the market wakes up to this truth.

Of late, equities and bonds have tanked simultaneously, undermining the 60/40 rule. In the backdrop of falling equity prices due to Covid-19, bonds have contributed to increasing rather than containing the volatility of one’s portfolio. The reason bonds cannot do their job of reducing volatility any longer is in large part due to their negative real returns.

The failure of bonds to deliver in this respect has necessitated diversifying into other asset classes to reduce portfolio volatility.

We must deploy capital in places where the currencies are not being debased. With the debasement of Western currencies because of unprecedented fiscal and monetary stimulus, the internationalization of Renminbi, de-dollarization of international trade, there is case to be made for owning Asian currency bonds, where the size of monetary and fiscal stimulus in response to coronavirus has at best been modest. These may be the new anti-fragile assets.

The growth components of an investor’s portfolio are shifting from “growth from volume” (i.e. technology) to “growth from prices” (i.e. energy, material industries etc.). It makes sense in light of the upcoming inflation.

Gold is a Mercurial player: it can do badly but also shine on an occasion and save the day when all other assets are faring badly. Given that real rates are going to fall because inflation is anticipated to rise faster than nominal yields, gold can be expected to perform well, very well, in fact, but only for a short span of time, after which it will consolidate (like always). Even though equities and other commodities (copper, energy) are doing well, should they tank in the future, we can turn to gold to work up its magic.

Coming to energy, oil has a potential to rise higher still for one simple reason: demand from reopening will arrive sooner than the turnaround in production.

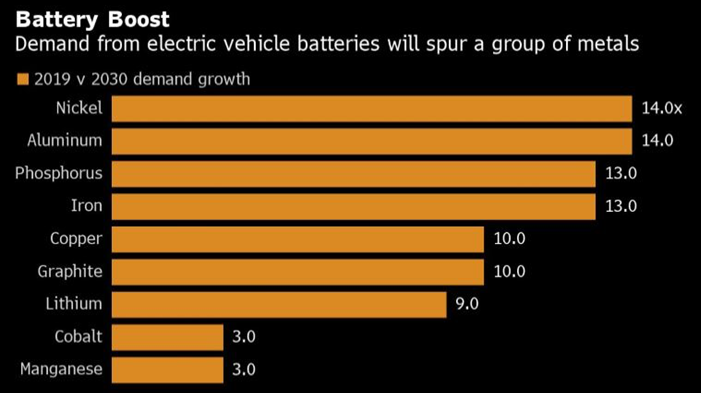

Copper prices have soared already, but supply continues to remain constrained. In future, greater demand from electric car production etc. could spell a further rise in its price.

China has taken over Hong Kong to help in internationalization of the Renminbi. And even though Hong Kong has remained mired in political tensions, it will continue to be a major financial center. Singapore has tons of finance business too, but it cannot replace Hong Kong any time soon.

Because China has taken over Hong Kong, it is not in China’s interest if Hong Kong capital markets perform poorly. Indeed, they are thriving at present. China is now the guarantor of Hong Kong’s financial stability.

Money printing is a dangerous way to fight the ongoing downturn: it can lead to exploding prices of commodities (for example, food). Add this to the pervasive confinement policies put in place to fight the virus, and you will have angered people a lot. There could be riots, too.

I believe that rising commodity demand will not be met by increase in supply for a long period and we are headed for “Higher for longer” commodity prices.

They are not increasing Capex but giving back the cash

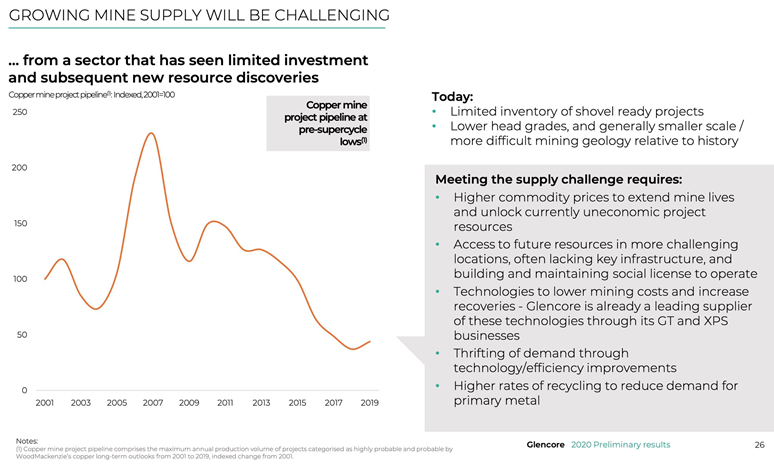

This one from Glencore presentation yesterday on state of copper mining

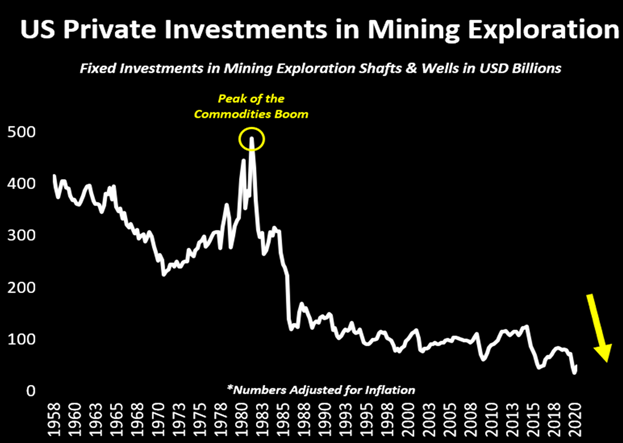

However, investments in mining exploration are at a 62-year low!

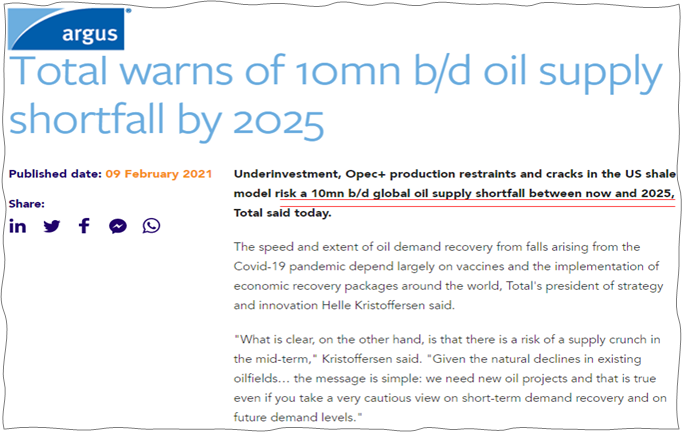

Industry leaders and insiders are raising the alarm on crude oil prices.

Look at the size of demand

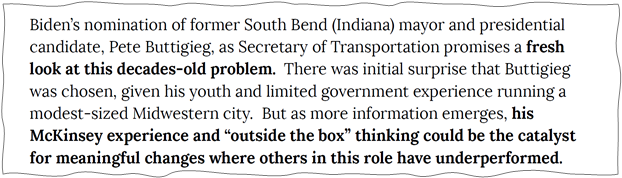

and the demand which will come because of US infrastructure bill which most investors are not taking it seriously.

I am quite impressed by the credentials of Infrastructure czar

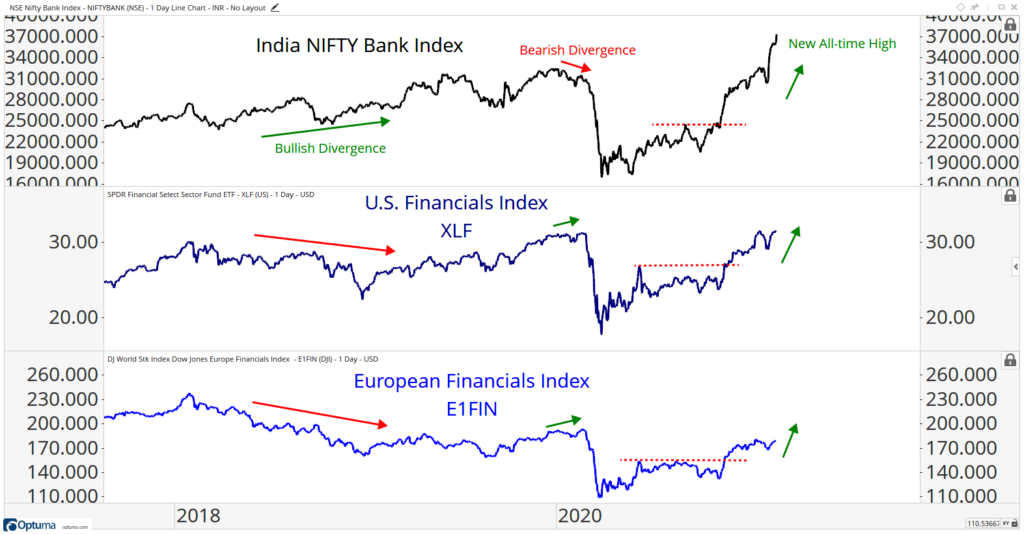

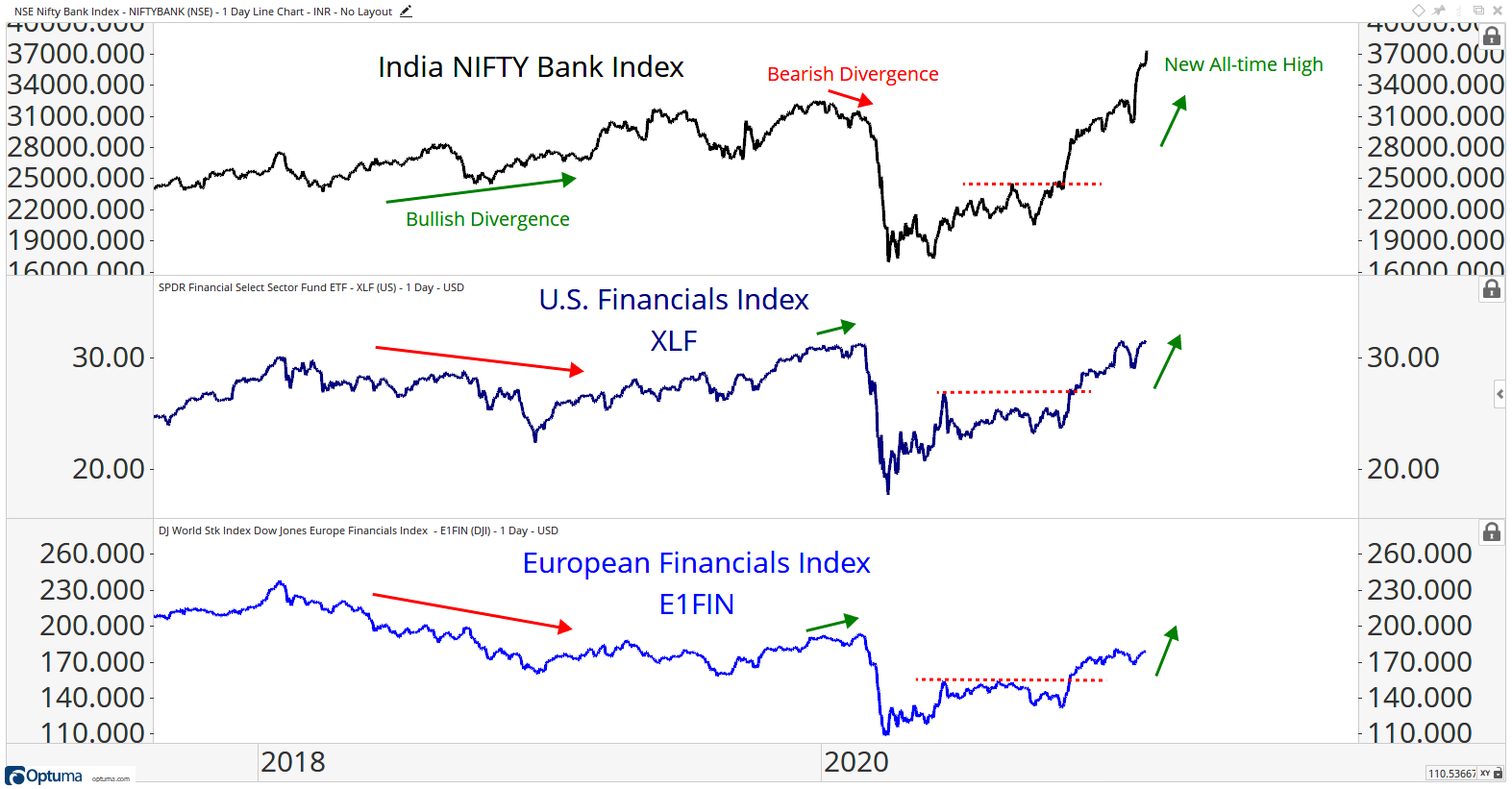

If you’re ignoring the Indian Stock Market, I think you’re doing yourself a huge disservice.

Even if you never plan on trading stocks in India at any point in your life, it doesn’t matter. There’s amazing information coming from there.

For example, take a look at that relative strength in Indian Bank stocks before US Stocks, and Stocks in general, rallied throughout 2019. That was an epic rally, if you recall.

The Indian Banks had already been telling us that it was coming!

Then Fast forward to Q1 2020 when US Financials made new highs along with European Banks. But Indian Bank stocks were already warning otherwise, for months before stocks finally crashed.

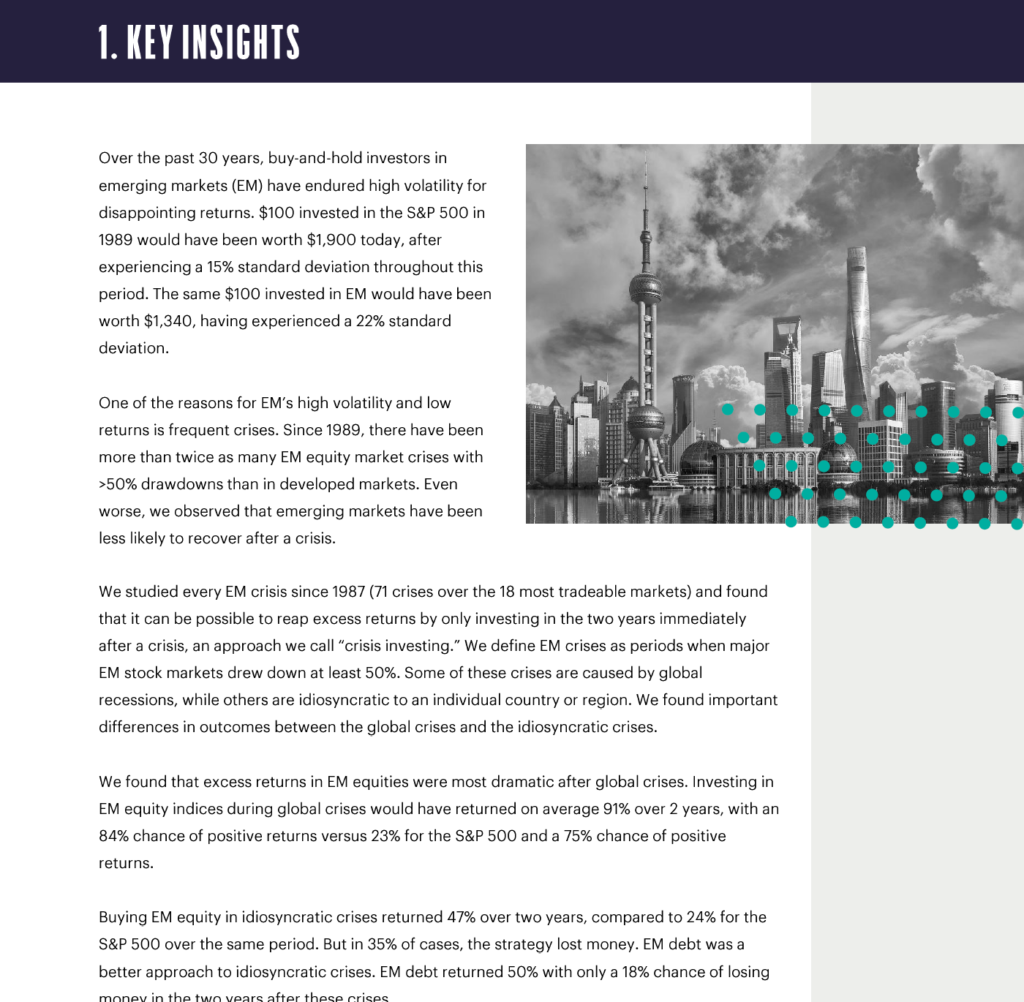

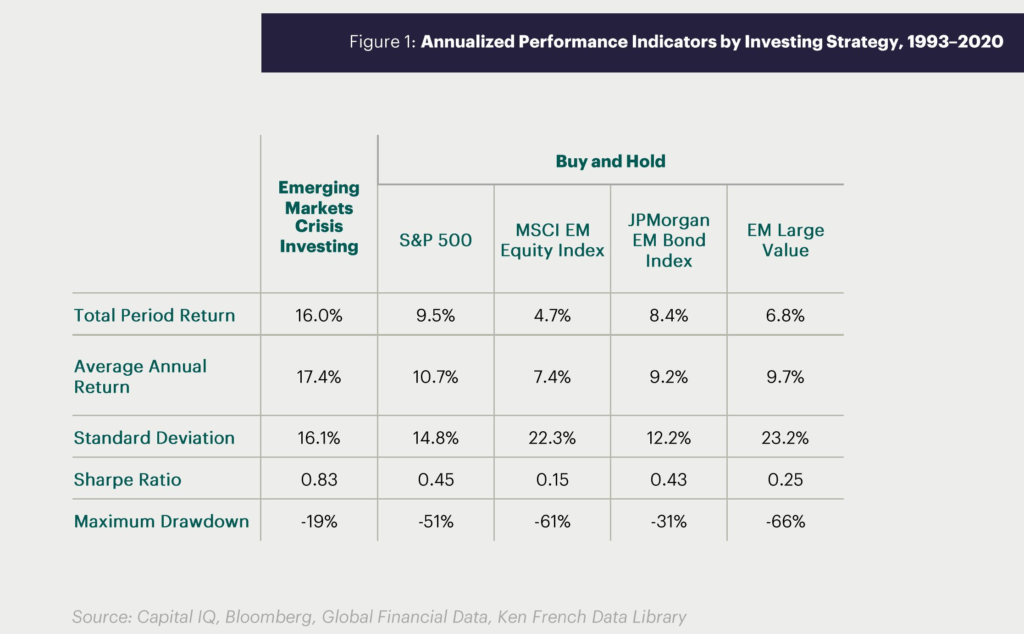

This is a brilliant paper on “when is the best time to invest in Emerging markets” and the author concludes that EM gives best returns after a global crisis.

I read a piece by Goehring & Rozencwajg you may also access the commentary here on supply demand mismatches commodities in general and specifically on some of my favorite topics like OIL, AGRI, URANIUM, COPPER, GOLD

Main Points

On Alternate Energy

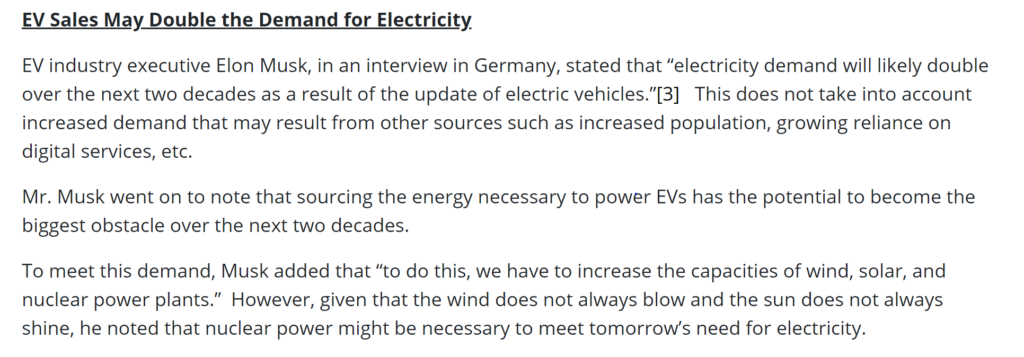

Vaclav Smil, Distinguished Professor Emeritus in the Faculty of Environment at the University of Manitoba, is the best energy scholar we have ever read, in our opinion. In his Energy Transitions, he notes that historically a new energy source takes between 40–60 years to gain significant market share. The current proposals assume wind and solar will make comparable gains in only 20 years. Ambitious plans often carry ambitious budgets, and the green energy transition is no exception. Using extremely aggressive cost saving assumptions, a widespread move to renewable power is expected to cost $70 tr over 20 years, nearly $50 tr more than if we stayed on the current trajectory. Unfortunately, our research tells us this additional spending will not even come close to generating the expected reduction in global carbon.

Electric vehicles will likely not deliver the necessary carbon reduction either. In Norway, electric vehicle sales have gone from zero to nearly 60% penetration between 2010 and 2019. Despite such a dramatic shift away from oil, Norway’s carbon intensity has declined by 10% compared with 11% in the US where EVs remain less than 2% of all vehicle sales.

Wind and solar are extremely inefficient generators of electricity due to their low energy density and their intermittency. In the coming weeks, we will release a podcast that goes into much greater detail about these shortcomings. In summary, a solar panel likely only dispatches between 12 and 20% of its rated capacity due to the intermittency of sunshine. A wind turbine is somewhat better, but still less than 25%. As a result, excess capacity must be built to generate the necessary electricity. Moreover, the power must be “buffered” by a storage system to smooth out the inherent variability coming from both short-term dislocations (clouds and periods of calm), as well as different patterns between day and night.

On Oil

Regarding demand, we believe 2021 will see a huge rebound. Although the financial press has made little comment, oil consumption in China, India, and now Brazil has made new highs. If our models of emerging market oil demand are correct, 2021 will see global oil demand surpass its pre-COVID highs as the successful roll-out of vaccines gets underway. As we progress through the year, we expect a structural gap between supply and demand will emerge, eventually approaching nearly three million barrels per day, even once all OPEC+ curtailed oil is brought back onto the market. Given that oil prices should recover strongly in 2021 and that oil-related investments remain undervalued, we recommend maximum exposure in this space.

On Copper

China today is pushing to become a leader in generating electricity from renewable sources, an extremely copper intensive exercise. This alone could add several hundred thousand tonnes of incremental copper consumption annually. Also, China, has announced huge investments in their data center and cloud computing industries, both extremely copper and power intensive

On Precious Metals

We continue to believe this gold bull market will be driven by Western investors, as opposed to the 1999–2011 gold bull market, which was driven almost entirely by investors from India and China. The recent slacking of Western demand, as measured by the physical ETFs we follow, gives us more evidence that a potential lengthy period of sideways price action in both gold and silver prices is now taking place.

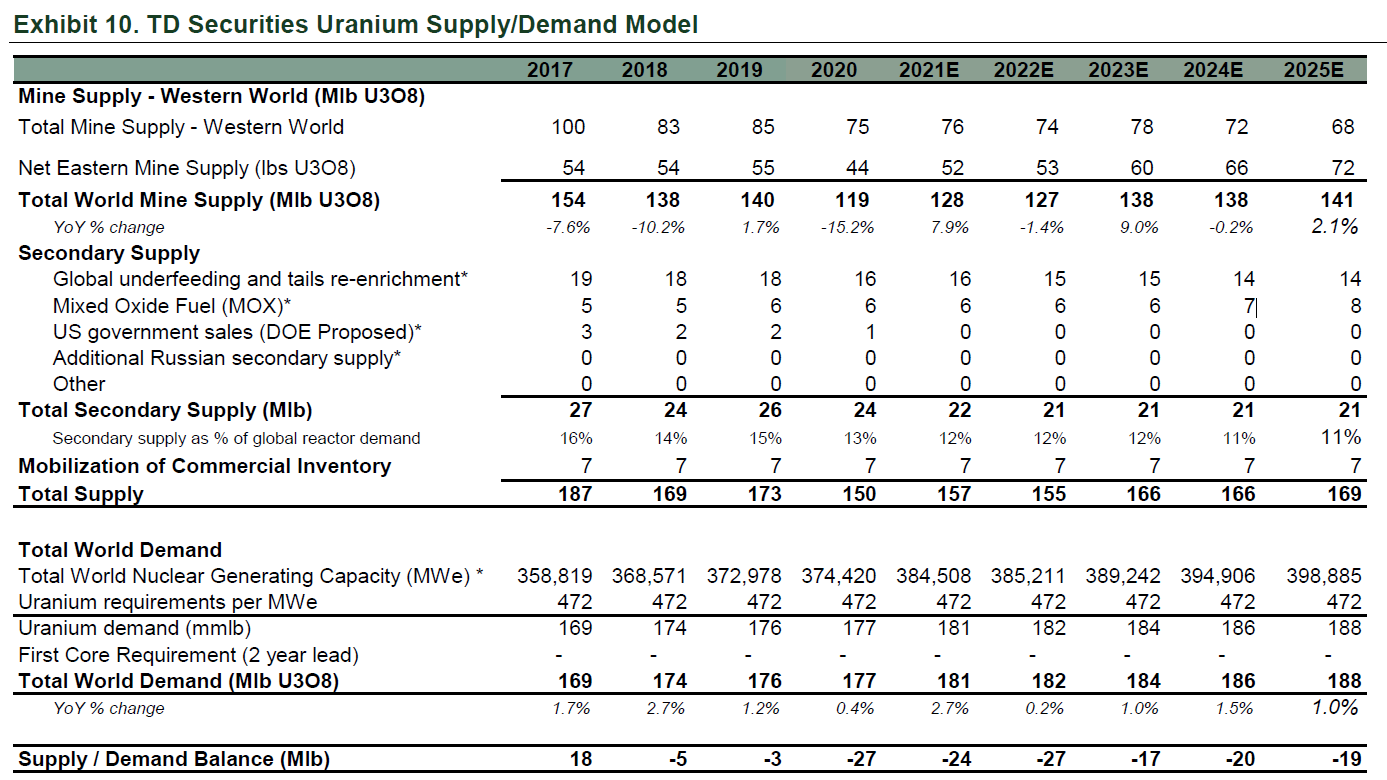

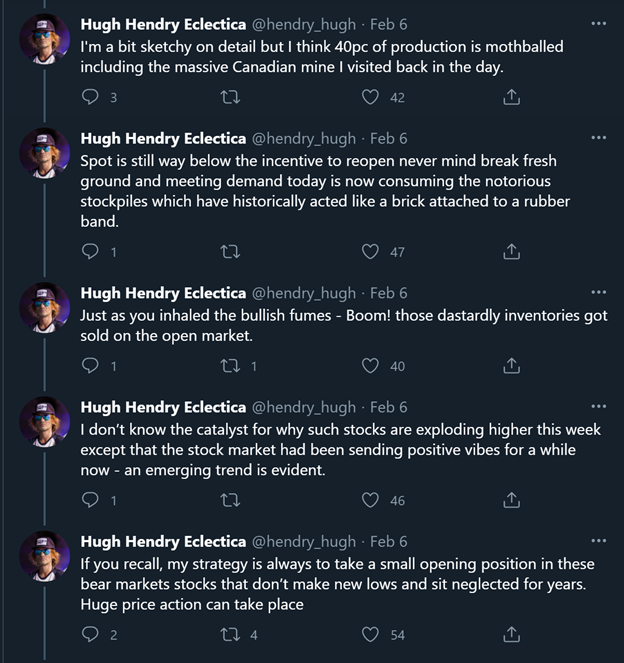

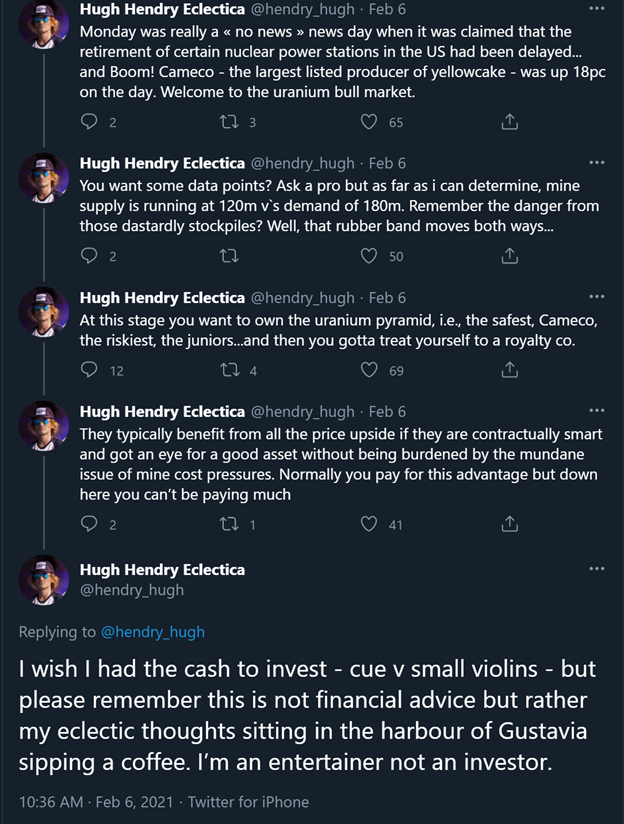

On Uranium

Despite the bullish outlook (and the Q4 rally), 2020 in many ways, was a frustrating year for uranium investors. Spot prices were strong between January and May, rallying from $24 to $34 per pound before retracing half the advance to end the year at $30.20 per pound on much lower volumes. Term prices rallied from $32 to $36 per pound between December and January and have been stable since on extremely depressed contracted volumes. Concerns over COVID related demand forced many term fuel buyers to the sidelines. US utilities are only 2% uncovered in 2021, but this level jumps to 35% by 2025, suggesting fuel buyers are vulnerable to any rise in price. With the recent speculation of delayed US reactor retirements, we believe we may see fuel buyers finally reenter the term contract market sometime in 2021.

Turning to supply and demand, trends exhibited in 2020 continue to be very bullish. Since nuclear reactors represent baseload capacity—much more so than natural gas plants—and rely on multi-year fueling programs, global demand was less impacted by COVID-19 than other areas in global energy markets. We estimate that global demand was only off 1%—or 1.2-mm pounds. Mine supply on the other hand was greatly impacted by curtailed production at Kazatomprom and the suspension of operations at Cameco’s flagship Cigar Lake due to COVID cases among employees. In total, global mine supply was down 20 mm pounds or 14%. After restarting in September, production at Cigar Lake was yet again suspended in December and remains shut as of today, implying continued tightness into the first months of 2021. Global uranium inventories likely drew in excess of 30 mm pounds in 2020 and we anticipate further draws this year as well.

The coming global agriculture crisis

Over the last four years, global agriculture has sat on a knife’s edge. Extremely strong grain demand, sourced from the developing world, has been met with extremely favorable global growing conditions resulting in bumper crops. Because of favorable weather, global grain markets have been able to accommodate strong demand with little in the way of upside price pressure. However, we believe this is now changing.

”Grain inventories have now been drawn down to levels that could easily slip into dangerous zones if weather in the 2021 northern hemispheric growing season becomes even slightly problematic, which we believe it may. The first signs of drought conditions have already emerged in Brazil, the wheat growing region of the Former Soviet Union, and in the US Midwest. Northeast China’s wheat growing region is currently suffering extremely cold weather causing severe damage to their winter wheat crop.

The next war will be fought over “chips” and “Rare earth Metals”

And who is the biggest buyer of chips in thworld

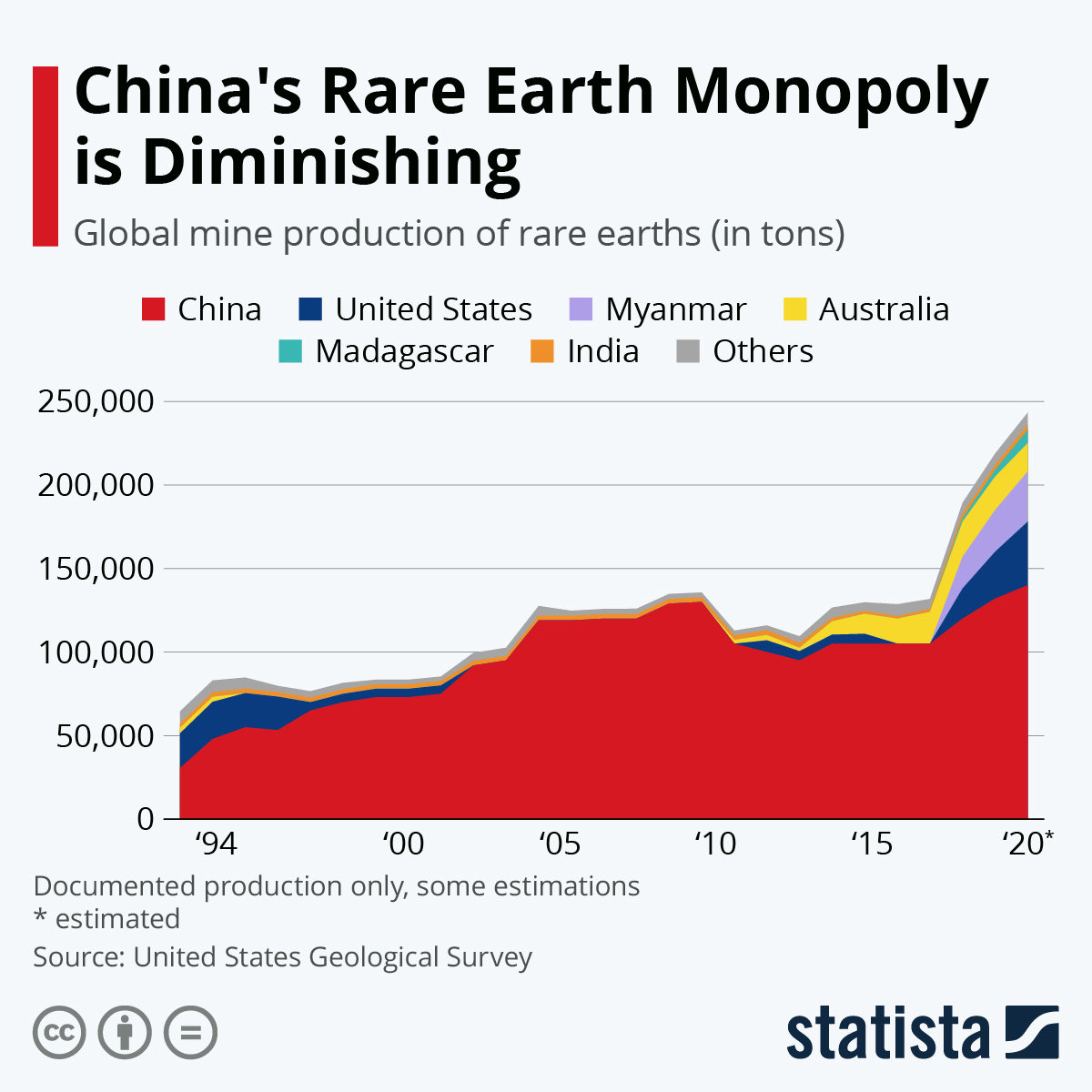

Next is Rare earth metals…

and Myanmar coup just in time. Honestly, most people cant place Myanmar on the map but today Myanmar is one of the most important countries in the world from geopolitical point of view… why?

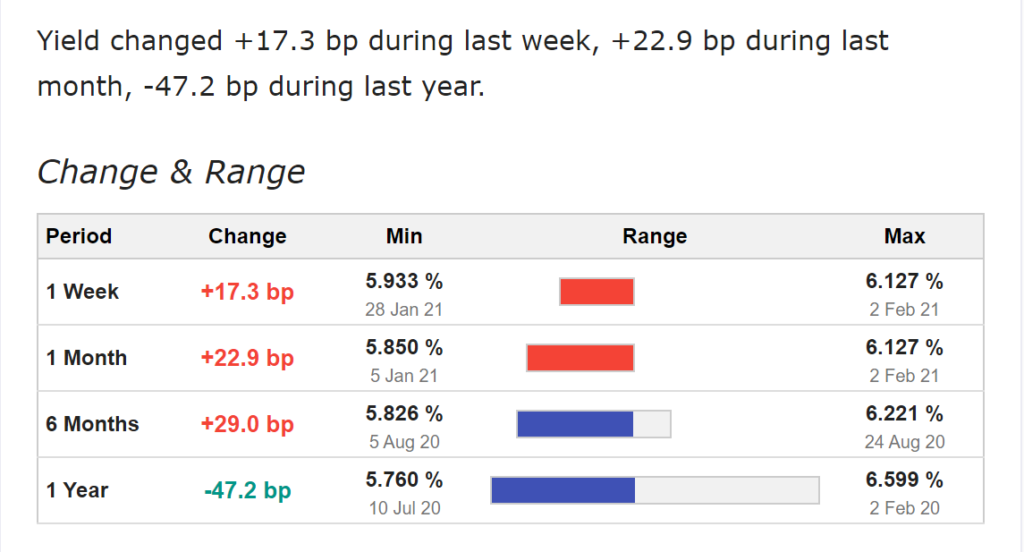

India is the first country among major economies where Bond market vigilantes are rising from ashes

Indian govt announced the budget this Monday and the following headlines from Bloomberg is the only one you need to read to visualize the size of budget and extent of market borrowings

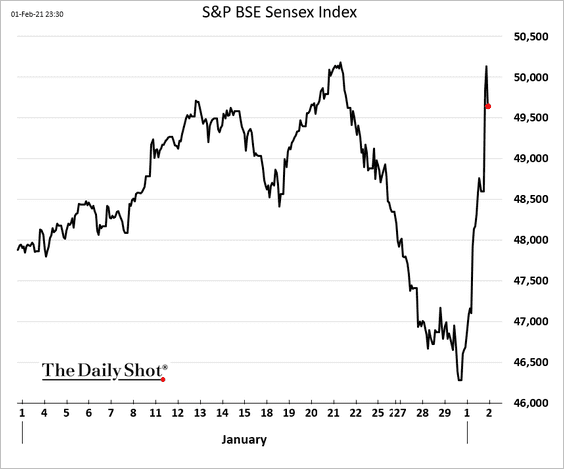

as a result the following reaction from SENSEX was a foregone conclusion

but not so fast

Indian bonds sold off hard with bond market not at all liking the extent of spending and revolting by raising the borrowing cost for govt.

I have often commented in past that till the time bond market oblige… equity markets get a free pass.

Another 30-40 BP increase in Indian 10 year bond yield will start to weigh heavily on equity valuations.

Bond market has spoken, either monetize the deficit and put a lid on bond yields which should be massively bullish for real and financial assets in the short run at the cost of longer run inflation

or

watch rising yields jeopardize government borrowing plans by raising the yields and in turn slowing down the economic momentum even before govt get a chance to kickstart their spending program.

{kind=link}