via Zerohedge

By Nicholas Colas of DataTrek Research

Highly skilled equity managers know how to find great stocks, but they are not so good at knowing which positions to sell. That observation comes from a recently published paper which is the subject of this post. The problem here is one of attention. Great PMs spend a lot of time looking for the next big idea and much less on evaluating their current positions. When they sell, that information gap leaves them open to unproductive mental shortcuts. Good news: the paper’s findings point to 4 hacks around this problem.

* * *

The decision to buy or sell a stock should be based on the same question: how will it perform in the future? Therefore, you’d think that highly skilled portfolio managers would be good at both. They should (generally) pick winners and sell them when they’re about to stop working.

A recently published NBER paper shows that’s not what happens, however. The paper’s title, “Selling Fast and Buying Slow: Heuristics and Trading Performance of Institutional Investors”, is a nod to Daniel Kahneman’s book “Thinking, Fast and Slow”. We love a good behavioral finance story, so the paper’s findings and our thoughts on them are the subject of this week’s Story Time Thursday.

The study, done by researchers at the University of Chicago, MIT, and UK data firm Inalytics, (link to the full paper below) looked at buy and sell decisions across 783 actively managed portfolios from 2000 to 2016. All portfolios were unlevered and actively managed by institutional, long-only managers who make concentrated bets (average of 80 positions at any one time). They outperformed by an average of 2.6 points/year over their benchmarks during this period, so we’re talking about a skillful group of individuals.

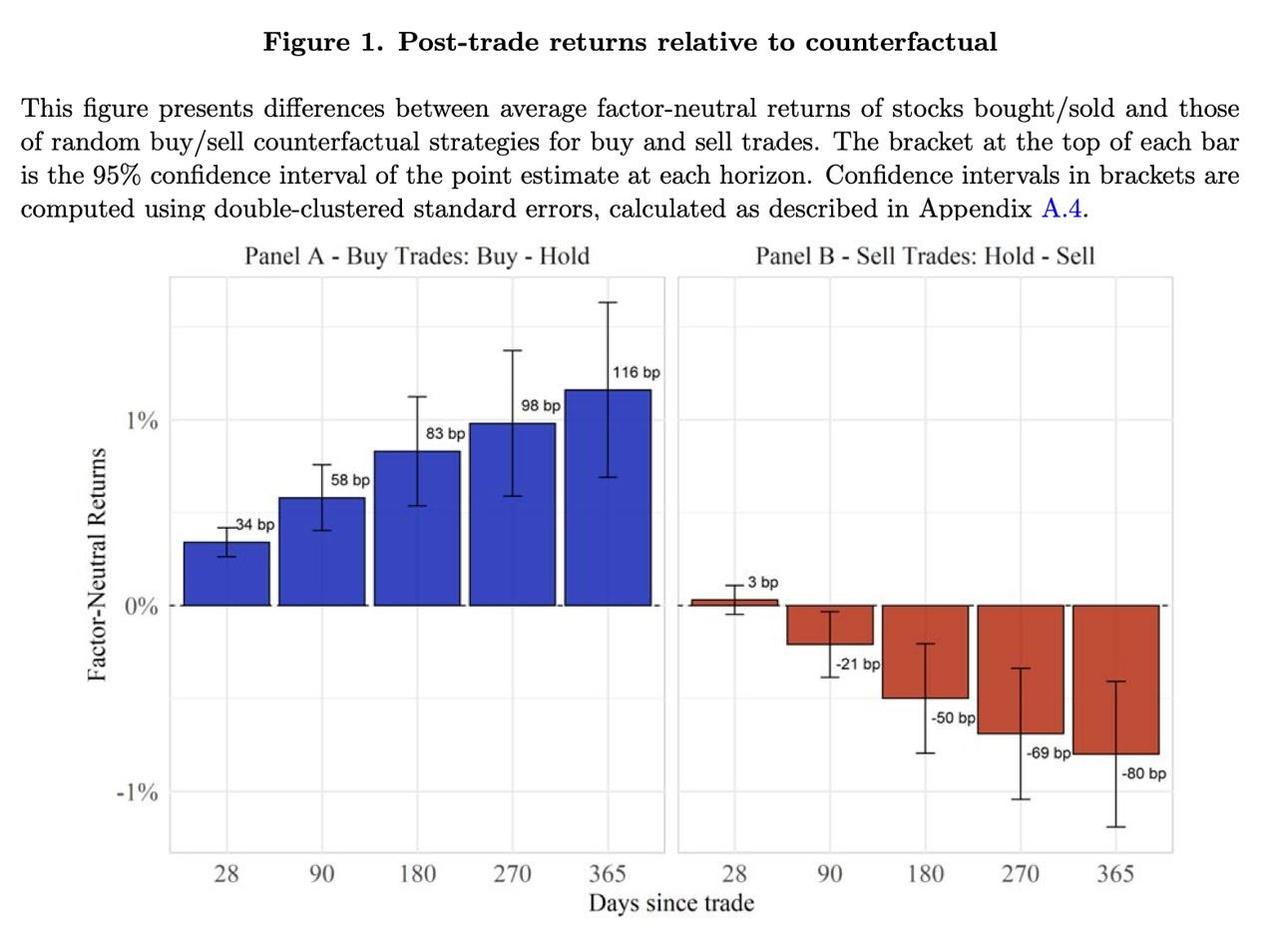

This graph summarizes the researchers’ key finding: these PMs were great at buying the right stocks, but not so great at knowing which names to sell out of their portfolios. The left side bar graph shows that these managers on average picked winners versus their benchmark. Great, but … The graph on the right shows they would have been better off either 1) selling a small part of every name in their portfolio or 2) randomly picking a name to ax, rather than selling the name they chose to cut loose.

{kind=link}

The paper’s authors believe that “the stark discrepancy in performance between buys and sells is consistent with an asymmetric allocation of limited cognitive resources towards buying and away from selling”. In layman’s language, there’s only 24 hours in a day and PMs spend most of that time looking for the next hot investment idea. That leaves less time for keeping up on the names they already own. When pressed to sell out a position, therefore, they lean on counterproductive heuristics (mental shortcuts).

As odd as all this sounds, the realities of running a money management business do (sort of) demand it:

- Describing new and interesting investment ideas is a huge part of the marketing process for investment managers. Many fund-raising meetings start with the allocator asking “OK, tell me a stock story I haven’t heard before”. Of course a PM is going to allocate more time to finding a new name rather than having to discuss something they’ve owned for a while and will therefore seem stale.

- Wall Street doesn’t care about counterfactuals. If a PM has a winning record, they will generally be able to find new clients. “You’re a great money manager, but you sell the wrong names so I’m not giving you any money to manage” has never been said by anyone, ever.

Even with that cynical (but absolutely correct) second point, the paper does still offer 4 actionable observations that we believe are applicable to anyone looking to improve portfolio performance:

- When a good investment process leads you to an idea, do all the work up-front and size it appropriately (i.e., no “cheerleading positions” – make it count). Selling low-conviction ideas (as measured by portfolio weighting) was responsible for most of the underperformance the researchers found in the data. These were names the PM had put on the sheet in a small way, but had not felt confident enough to size up. When they found something they thought was better, they ditched the small holding to fund their next purchase.

- It can often be a good idea to wait for the next earnings report before selling. Researchers found that sales made on earnings announcement dates “substantially” outperformed the random-sale counterfactual (randomly selling a name or just cutting back the entire portfolio evenly). Oddly, purchases made on earnings announcement days saw no net outperformance versus other buys.

- Don’t just focus on whether a name has been a big winner/loser for you when deciding to sell. Past performance is not a predictor of future returns, but the PMs studied still sold outliers (big winners or big losers) at rates “more than 50 percent higher” than other positions. As with the prior point, this bias did not exist when PMs made Buy decisions.

- Value investors beware; the paper found that “funds that score higher on value appear to underperform most in selling”. Momentum strategy portfolios, by contrast, had no selling underperformance over the 1 year after their sales.

The bottom line to all this: where the head goes, the portfolio follows. Finding new ideas to own requires a disciplined approach, but so does making sales. The paper’s key finding is that even highly skilled managers mentally overweight “buying” and underweight “selling”, leaving them open to a range of unproductive heuristics when deciding to unload a position. The good news – for them and for all investors – is that correcting this imbalance comes down to just paying a bit more attention to what’s already in the portfolio.