I know the following article first published in CNN sounds crazy and may be it is crazy but aren’t crazy things happening around us.

why I liked the article is because it has all ingredients of a great economics 101 about demand and supply. No body is contesting falling demand for crude but what about a steeper drop in Supply aided by collapse in Capex necessary to maintain the supply.Add a spice of climate activist and Large funds which are shunning oil equities, the oil guys are a lonely lot

CNN BUSINESS WRITES ….In a little-noticed report, JPMorgan Chase warned in early March that the oil market could be on the cusp of a “supercycle” that sends Brent crude skyrocketing as high as $190 a barrel in 2025.Weeks later, the coronavirus pandemic set off an epic collapse in oil prices as demand imploded. And yet the bank is doubling down on its bullish view.Brent hit a two-decade low of $15.98 a barrel in April. US crude crashed below zero for the first time ever, bottoming at negative $40 a barrel. The United States, Russia and Saudi Arabia — the three largest producers — have dramatically slashed production in response. The massive supply cuts helped breathe life back into oil prices.

Oil is up $80 in seven weeks. The remarkable recovery could be too good to be trueThough demand remains depressed, JPMorgan still thinks a bullish oil supercycle is on the horizon. A huge amount of supply has been taken offline and the industry could have major trouble attracting future capital. “The reality is the chances of oil going toward $100 at this point are higher than three months ago,” said Christyan Malek, JPMorgan’s head of Europe, Middle East and Africa oil and gas research.

Looming deficit suggests prices will ‘go through the roof’

For years, the world has had more oil than it needs. That glut caused storage tanks to fill up to the point that crude turned negative in April. So oil producers slashed supply. But now the pendulum in the boom-to-bust oil industry could swing too far in the opposite direction. Oversupplied oil markets will flip into a “fundamental supply deficit” beginning in 2022, according to a JPMorgan report published June 12. The most likely scenario, JPMorgan said, is that Brent rises to $60 a barrel to incentivize higher output. The report didn’t spell out a price target for its bull case scenario — yet Malek told CNN Business that JPMorgan’s $190 bullish call from March still stands. In fact, he thinks it’s even more likely now. Malek, who has been bearish since 2013, pointed to the very large supply-demand deficit that’s expected to emerge in 2022 and could hit 6.8 million barrels per day by 2025 — unless OPEC and others pump much more. “The deficit speaks for itself. That implies oil prices will go through the roof,” he said. “Do we think it’s sustainable? No. But could it get to those levels? Yes.”

BP sounds the alarm

Of course, it’s hard to imagine triple-digit crude today. Some analysts believe even the rebound in US oil from negative $40 to positive $40 in just seven weeks is overdone. Coronavirus cases are spiking in some areas in the United States and Latin America. Demand for gasoline is improving but isn’t nearly back to pre-pandemic levels. And it could take years for the airline industry to fully recover — if it ever does.

BP warns of $17.5 billion hit as pandemic accelerates move away from oilBP (BP) warned this week that the health crisis could have an “enduring impact on the global economy,” causing less demand for energy over a “sustained period.” The UK oil giant slashed its forecast for Brent crude prices over the next three decades by 27% to $55 a barrel. BP also said it plans to write down the value of its assets — including untapped oil and gas reserves — by up to $17.5 billion. Somewhat counterintuitively, JPMorgan’s Malek said the BP writedown and gloomy forecast are “one of the most bullish” developments he’s seen. That’s because oil companies must spend heavily just to maintain production, let alone increase it. If they do nothing, output will naturally decline.And BP’s weaker outlook suggests even fewer long-term oil projects will make the cut. That in turn will keep supply low — even as demand rises. “It validates our point,” Malek said.

Oil spending could collapse to 15-year lows

Between 2015 and 2020, more than 50 new oil projects were sanctioned globally, according to JPMorgan. But the bank estimates just five so-called “greenfield” projects will come on the line in the next five years. And some Big Oil companies including BP, Shell (RDSB), Total (TOT) and ConocoPhillips (COP) have delayed making final investment decisions. Global upstream investments are expected to plunge to a 15-year low of $383 billion in 2020, according to a recent Rystad Energy report. Those spending cuts, Rystad said, will make it “more challenging to maintain existing production” and will potentially impact the “stability” of supply in the long run.

Yet shale drillers can’t bank on the once-unlimited stream of Wall Street funding. Investors are demanding frackers live within their means after years of burning through piles of cash. “Shale is growing up. It’s still there, but it’s maturing,” said Malek. Capital is being further restrained by heightened concerns about climate change and the rise of socially responsible investing. A growing number of investors simply don’t want to touch oil stocks. The combination of the price crash, capital flight and climate change could limit the oil industry’s ability to attract the necessary money — just when it’s needed the most. The past few months have shown how difficult it is to forecast the future. While $190 crude might sound far-fetched, so did negative-$40 oil.

Rohit Srivastava of indiacharts has written a brilliant article on cause and effect relationship.

For those who still believe in fundamentals should read the article below.

Rohit writes…In my most recent ‘Forex Analytics’ webinar I spoke about two possible regime changes that are taking place right now. The 1st major change is likely to be a move away from the deflationary regime towards an inflationary regime. I titled this ‘The reflation trade 2.0’ because the 1st attempt to make the shift was made in 2017 when the dollar index topped out to decline for the entire calendar year.

That was followed by a 2 year advance in the dollar that made a protracted attempt at the beginning of 2020 to take out the top made in 2017, but failed to do so and has left us behind with the possible double top in the dollar index.

While most people might wait long enough before they shift their positioning based on the above setup, Elliott wave analysis allows you to have the confidence to do so at a point when the risk reward is exponential, meaning that you are close enough to the turning point that may become the important stop loss for your view to go wrong. The ability to assess the probability of an opinion is not possible with any other fractal science. Knowing it early gives you a clear risk reward to deal with.

If you start looking for data to confirm then you might end up looking at backward looking information for example the chart below of WPI inflation that was published after the most recent data and shows a drop in wholesale prices growth to the lowest level in years. But this decline did not start in 2020 after the COVID-19 pandemic. Deflationary forces have been pushing down inflation since 2012 you look at longer dated chart.

This second chart shows the history of inflationary cycles in India. There are many spikes to 15% and higher that later cooled off. But we went below 5% after 2 decades in the late 1990s. The most recent episode saw inflation peak in 2010 and since then deflationary forces are at hold. The chart below is into the year end of 2019, so it misses the recent drop seen above. Now back at near zero inflation has a chance to start another move higher especially aided by fiscal and monetary stimulus.

in my mind the 1st signal of this regime change came with oil prices dropping to single digits achieving many long-term forecasts for sub $ 20 that had been made over the years. Subsequently not only has the Fed stepped into buying oil bonds, but central banks around the world have resumed asset purchases that are being accompanied by some form of fiscal intervention as well. That oil prices have gone back from single digits to $ 40 recently may have gone unnoticed as the media went silent/numb on the rebound, after going hyper when we dropped to negative in the futures market. This quarterly chart shows the massive candle that we are forming on the rebound.

Starting last year itself the RBI stepped up bond buying by conducting LTROs in a direct attempt at bringing down long-term interest rates to ensure transmission. The initial size of the program was small but expanded many fold after the Covid crisis. This is unlikely to stop.

The direct result of these operations can be seen in declining bond yields, that are now below the trendline from the 2002 lows, setting us up for interest rates that may end up being the lowest that we have seen in Indian history. This is now a trend and not a knee-jerk reaction as the central bank may continue to push yields lower, and over time expect borrowing rates not just for the corporate sector but consumer related purchases as well to come down significantly. Over the next year or two I would not be surprised if borrowing rates come down to lower single digits something we have probably not seen in decades.

For investors this has a very significant bearing on their investment behavior. On the one hand saving accounts become even more unattractive and deposits lag behind the inflation rate. As inflation slowly makes a comeback equity valuations that appeared expensive all of a sudden start looking cheap. Valuation models after all a function of interest rates [or the risk free rate] and once you bring down rates everything changes. Some might argue that the end result would be a bubble, but bubbles are processes and they first need to be built before they can pop. The opportunity is in between

The years 2010 to 2018 involved the recognition of India’s economic winter in the form of excessive debt in the corporate sector and its resulting impact on non-performing assets in the banking system. Most of these problems are now in the open and being addressed by the central bank. Many corporate groups and banks and financial institutions have already reached near failure over the last 7-9 years. In its most recent address the RBI has stated that it will not allow any more of the banks/financials in India to fail.

We all know about the debt problem or the problem of overcapacity in some sectors and are doubtful about the solutions. However economic winter cycles always end with 1 of the 2 outcomes. Either a default by all over stretched sectors or and the debt leads to a series of banking and corporate failures and a contraction in the economy on the back of these events before growth can be revived, or, those in power decide along the way to attempt to inflate their problem of Debt/GDP by expanding the denominator in nominal terms. In short the nominal GDP can be increased by slowly increasing prices at an acceptable rate, to bring down the debt to GDP ratio.

It is very important to understand which one is being undertaken by the government or central bank in power to be able to comprehend the end result and its impact on investment assets. Too many people relate a deflationary cycle with the 1929 US stock market crash that involved the Dow Jones Industrials index falling by 90%. What they forget is that one of the reasons for this deep decline was the then President’s decision to allow businesses and banks to fail if they had made mistakes. This was among the primary reasons why the collapse exaggerated itself on the downside.

This is also the reason why central banks are more proactive this time round to avoid a similar scenario. However the other alternate path is to inflate. The is an option. In other words the outcome at the end of a deflation is not just something that has to happen one way, but a function of what the policy path is to reset the debt. By default or inflation. So we are not in a position to decide this. We have to pay attention to the policy makers and then take the lead. This then will show up in the many indicators discussed here from the dollar to inflation to interest rates. The path to inflation is the path it appears, at least at the moment, that most of the world has taken to. Provide as much liquidity in the financial system as required to ensure that there is no financial collapse because of systemic issues. To allow failed businesses to either restructure or be downsized and refinanced into a new entity. US started down that road in 2008, India now faced with its own crisis is going down the same path now. Lower rates and avoid financial failure. Then wait for the lower rates to reignite consumption as the cost of borrowing new money goes down making it viable even at higher prices of goods [read inflation of prices] accompanied by wage increases [another form of inflation in wages].

While the US has been trying to inflate its economy since 2009, it is new for India because we are only going through this process now. After more than a two year crash in mid-and small cap stocks and the broad market, and a sell off in large caps in the post pandemic period, India joins the rest of the world in an attempt to reflate the economy without a debt collapse. In many parts of the world where monetary policy is no more having an effect on the economy direct government spending is now be undertaken. India is currently at the stage of using more of monetary policy before it can adopt more fiscal profligacy. So a lot of the inflation India may face maybe imported. This part is important to understand. Monetary policy only supports expansion of debt and consumption but that does not always result in rising prices. Fiscal spending is more direct and its impact on demand and prices could be very different. India however is still behind the curve in the long wave cycle than other parts of the world. We are doing what they have already a decade ago.

All the above put together is having changes in many major trends that have been in force over the last decade. Here are a couple of charts showing historical cycles of some patterns. The 1st between value and growth investing. It displays a prolonged period of growth outperforming value a trend that might be overdue for change.

The 2nd chart shows another trend where developed markets were outperforming emerging markets. Part of the reason may have been the pressure that came from a rising dollar. The US recovery since 2009 was accompanied by a rising dollar that lead to many crisis in bond markets of Brazil and Russia, and a hyperinflation in Venezuela, and trouble in Turkey. The list may be longer, but an easing of pressure on the dollar could change this trend once again in favor of emerging market equities.

The advent of floating-rate currencies has been one of the greatest financial engineering feats of our time. It has allowed the world to manage interstate balances and debts in a way like never before. In the past the government would have had to devalue its currency openly creating a currency panic. However this single change decades ago change the game completely. Today multiple central banks devalue their currencies simultaneously or in sequence one after the other with no net effect on either. This does not mean that there have not been any casualties along the way, but at large we have been able to create a much larger credit environment. The chart below shows the exponential growth of total credit both government and corporate over time. The risk to emerging market debt that is at large now denominated in dollars comes from rising dollar. Between 2008-2020 EM debt expanded by over 10$ trillion [estimates]. A falling dollar environment where a large part of the dollars are supplied by the US Fed reduces the pressure on these financial markets.

If the above trends create an even bigger bubble, we will have to deal with it tomorrow. But we are not at the end but a possible new beginning of a global bubble to be created by cheap money and easy credit in Emerging markets. Ems may attempt to Mimic the extravagance of the west. The regime shift from a strong dollar to a weak dollar maybe one of the biggest culprits of this trend. One of the secondary effects of all of the above might be another regime shift that markets have not thought about. Liquidity may flow from DMs to EMs financing another round of expansion at lower rates of interest as long as inflation does not become a problem.

Last but not least we may witness a move from a low Volatility regime to a high volatility regime. After years of the US weeks remaining below 17 on average, we may now have to get used to above 17. A similar period of high volatility can actually be seen between 1997 and 2003. In other words the tech bubble of the late 1990s actually took place in a high volatility regime and it did not change till the next bull market took hold. Few discuss this today given that low volatility has become the norm with many strategies built around it. If higher volatility becomes the norm then expect the coming bubble to the rapid and fast both on the way up and on the way down.

At the end of such a long discussion people always want a timeline for these events. In my experience time is not a science but a guesstimate of possible future outcomes. The 7 year cycle for the dollar from 2017 may end in 2024 and can provide a rough timeline for these outcomes. What you can expect though is that this game goes on till inflation runs hot enough for one markets to pay attention. At that point interest rates will have to adjust to that reality and might break the bond market bubble. Interest rates particularly in EMs would be important. Interest rates in DMs are already flirting with negative rates. EMs are starting a move from high yield to low yield at the end of a deflationary crash in oil and commodity prices. Low interest rates and liquidity are the fuel for EMs as of now as long as the dollar is falling. If any of these factors change course so will I.

All this is still part of how the Economic Winter ends. So being bullish or bearish has nothing to do with the Economic winter. The winter is about debt. But the impact on markets can change from time to time based on policy action toward that debt and we need to pay attention. Given this explanation there is nothing irrational about what the markets are doing right now. Still, for those of you who still think it is irrational, while markets can be irrational longer than anyone can be solvent, timing is everything, irrespective.

My Good friend Kevin Muir from Macro Tourist has been banging on about Modern Monetary Theory (MMT) for ages. I’ll admit, some of his pieces have been difficult to read as I’m firmly planted in the Austrian school—I believe gold is money and everything else is fiat. I believe governments create inefficiency and corruption while politicizing common sense ideas. I am against MMT in all of its insidious forms as it only legitimatizes all that I disagree with. With that out of the way, I’ve matured enough to know that what I think doesn’t matter. My job isn’t to stake the moral high ground; it is to make money for my hedge fund clients by noticing trends before others do. While I disagree strongly with MMT, Kevin has been right to repeatedly educate himself and his readers on MMT because it’s coming (whether or not you want it).

With Kevin’s permission, I have re-posted his most recent MMT note in full. I think this will be one of the most important macro pieces I’ll post on this site. There’s been a fundamental change in how governments tax and spend, yet most do not yet realize it. MMT is going mainstream. Are you ready…???

Yesterday, MMT-advocate, Stephanie Kelton released her much-awaited book, The Deficit Myth.

You might think MMT to be a crock. It might make every bone in your body shudder. You might feel sick to your stomach as you read the theory. These are just a few of the responses I have heard from traditionally trained hard-money types who learn about MMT.

I suspect most of you know that I am open-minded to many aspects of MMT, but expect it will be taken too far – just like monetarism has been taken too far.

When I see the extreme monetary policy of Europe and other countries with negative rates, all I can ask is how can anyone claim with a straight face that monetarism is working for us? So yeah, I would rather try something new than continue down the current road of easier and easier monetary policy.

Yet, what you or I think about a particular economic policy doesn’t mean squat. I am not here to debate what should be done, but what will be done.

So let’s put aside the economic merits of the different schools of thought, and focus on discounting their probable implementation.

The Deficit Myth

I haven’t yet fully read Prof Kelton’s book, but glancing at the introduction, she does an admirable job sketching out her viewpoint in easy-to-understand layman’s terms. I have taken the liberty of pulling the important bits:

There is nothing new in Kelton’s introduction. MMT’ers have understood these concepts for more than a decade.

But we always must remind ourselves, as traders and investors, what’s important is to discount how the public perceives those ideas. Remember the whole Keynesian beauty contest concept (probably not the most politically correct analogy, but let’s remember that Keynes lived in a different era. In fact, I suspect if Keynes were alive today, he would be more politically correct than some of his most vocal opponents –Niall Ferguson apologizes for remarks).

Keynes rightfully understood that investors discount what the crowd will perceive as the most likely outcome as opposed to the best choice.

Which brings me to my main point. And I know some of you might think this is nuts. But I don’t care.

I have been watching for signs that the concept of “governments are not financially restrained” taking hold within the non-financial community.

I have even postulated that the corona virus crisis might prove to be the tipping point for this theory gaining traction. With all the extreme fiscal measures being put in place (without undue immediate negative effects), the public might realize that the government’s large fiscal response works miracles at staving off short-term economic pain. They might suddenly understand there is nothing holding society back from doing that again for other priorities.

Well, I think I got my signal. Earlier in the week, I noticed a popular rapper tweeting out the following:

Yup. The whole theory behind MMT is being endorsed by rap musicians now!

When disputing the need for a balanced fiscal budget, MMT’ers have often resorted to the argument, “if there is always money for war, then why isn’t there always money for other social programs?”

I don’t want to dispute the validity of their argument. However, the narrative that “we need to balance budgets” has been torn down by the corona crisis better than the war argument ever did.

Over the last month, a growing portion of society has concluded that there was never any financial constraint to spending money.

I know the hard-money and traditionally-trained-economic thinkers will scream bloody murder at that thought. I get it. It doesn’t seem to make any sense. How can there be a free lunch? There is no such thing.

I will repeat again – I don’t want to discuss the merits of MMT. We will save that for another post.

What’s important – and it’s probably the most important thing that has ever happened in my investing career – is that the narrative surrounding deficit spending has changed.

Deficits are no longer “bad”. The budget hawks have all been silenced.

This will have ramifications that will last generations.

If this MMT school of thought continues to gain traction, then many of the investment playbooks from the last few decades need to be thrown out the window. It will be as a dramatic shift as the 1981-Paul-Volcker-stamping-out-of-inflation. It will be an end of an era.

Over the course of the coming months I will discuss the long-term investment consequences. But I wanted to highlight that MMT is about to go mainstream. And as it becomes more popular, it will turn investing as we know it on its head.

Decades from now we will look back at the corona crisis and say it changed more than just our attitudes about viruses, it marked the beginning of a change in the way we think about money.

While not exactly a chart but Russell Napier has changed his view and wrote an article titled ” The dawning of age of inflation” . He expects the inflation to cross 4% in developed world by 2021.

A key reason the US middle & working classes have seen stagnant relative real income growth over the past 45 years, in a single chart.

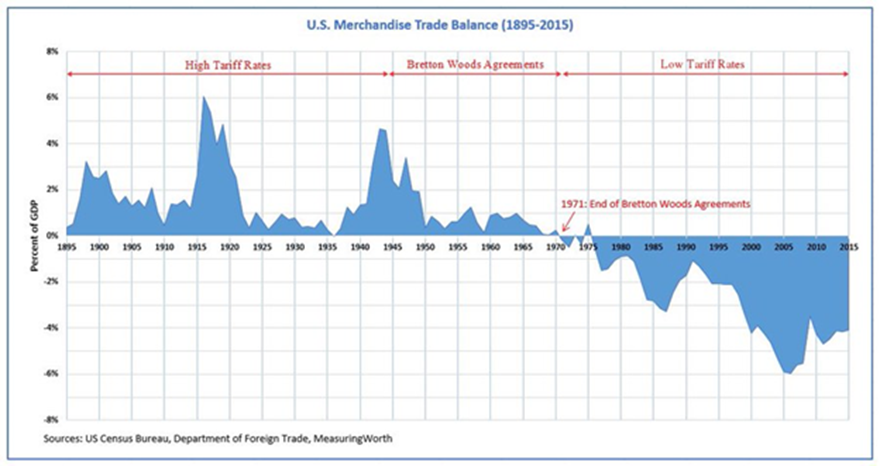

Trade and Tariff barriers are coming back

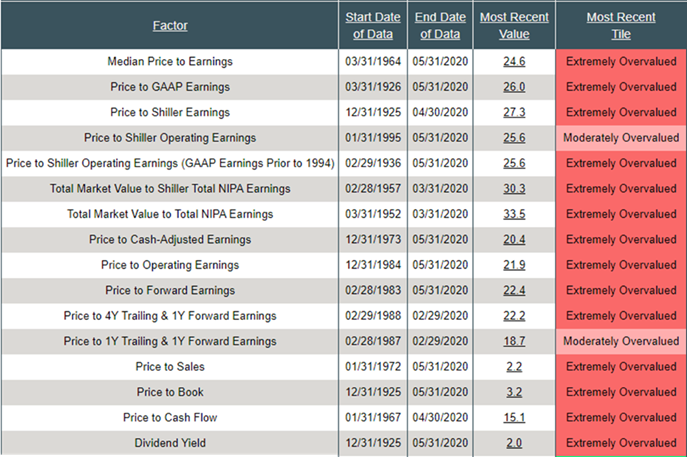

Let’s talk about valuations. Forward price-to-earnings (P/E) sits at 22.4. Median P/E (my favorite indicator, which looks at actual trailing 12-month earnings) sits at 24.6. For comparison purposes, the 52-year average, call it “Fair Value,” is 17.3. That suggests the S&P 500 Index’s fair value is 2,134.06. More than 30% below today’s level of 3,202. And it’s not just price relative to earnings. It’s price-to-sales, price-to-operating earnings, price-to-book. Price-to-everything is expensive. Here’s a look (red is bad):

Pre Covid-19, India’s last decade of growth was Debt financed household spending. This created winners in the market for companies who were part of this value chain from financiers who were funding tis growth to the companies who were recipient of this spending by the household.

As a result few companies have delivered outsized returns at the expense of everybody else due to it being a consumer debt financed growth.

As Debt levels peak the previous trends will reverse moving money elsewhere and create new winners

Covid will accelerate three trends

Onshoring of supply chains aided by subsidies, incentives and cheap cost of funds. Overruling of the WTO consensus worldwide will resurrect industries that were on the verge of extinction due to imports.

As countries like Japan, Europe and US look to diversify supply chains , the suppliers to the industries shifting to india will win huge.

The current QE in coordination with government spending is aimed at the real economy and as velocity of money picks up it will lead to inflationary outcomes. The governments will however exercise Yield control on bonds, making Resource , Argo commodities , gold and silver miners extremely bullish bets .

As a result of impending inflation, fixed income investments in duration of higher than 3 years is ill advised.

In a low growth world countries like Vietnam , Bangladesh among others will capture some part of the supply chains moving out of china. They will thus be poised for a outsized rally in their markets due to their growth prospects being similar to India 10 years ago.

The investments in global equities , precious metals miners and emerging trends like 3D printing or betting on nascent recovery in Europe is possible for Indian investors who can invest through LRS ( Liberalized Remittance Scheme) of RBI.

The WSJ ( known as mouthpiece for Fed) wrote last week that “Fed officials are thinking hard about” yield curve control, or pegging various duration at certain levels. It’s not clear from the article whether that’s conjecture, speculation or some kind of leak. However there is a detail in the report that suggests this is beyond conjecture: If the Fed concludes it is likely to hold rates near zero for at least three years, it could amplify this commitment by capping yields on every Treasury security that matures before June 2023.Another debate the article touches on is forward guidance and whether to tie it to the calendar or to economic outcomes. Yield caps would be a natural complement to the calendar-based guidance but could be trickier to communicate if paired with outcome-based guidance.

Peter Garny of saxo banks writes

Yield-curve control has mixed results when it comes to equities. Japan’s YCC policy since September 2016 has not been a success judging from real GDP growth and for Japanese equities which have underperformed global equities. The period 1942-1951 when the Fed had a YCC policy in place suggests a more positive picture for equities against inflation hinting that YCC can work as a crisis tool.

However, the key risk related to YCC is inflation risk as our study of inflation and equity returns suggest inflation growth of 4% or higher leads to bad real rate returns for equities.

Which sectors will benefit from YCC?

The cap on long-term interest rates will also cap banks’ profitability through an upper bound on net interest margin. However, to the extend that YCC creates growth this will grow loan books and thus market values of banks. Our view is that financials should be avoided in this environment but that growth companies with a large part of their value coming from the future should be overweight as YCC creates a low discount factor for future cash flows.

Highly leveraged companies and capital intensive industries such as auto, airliners, steel, real estate, shipping, construction etc. should also outperform in this environment as YCC will set financing rates artificially low.

In nutshell you need to be with asset owners who will benefit from lower nominal value of debt and higher nominal value of assets

Inflation beyond a threshold in the danger to equities….

YCC combined with aggressive US government deficits could suddenly create inflation which history suggests has a tendency to be a wild beast when it escapes its normal ring-fencing. Higher inflationary pressures will not immediately become negative for equities because excess capacity coupled with inventories buildup provide a cushion for near term .

A mild positive inflation shock has historically been associated with positive real returns in equities.

It’s actually a large deflationary shock that has been associated with negative real returns.

Peter analysis concludes that

“Equities have historically delivered negative real return when inflation has sustained its growth rate above 4%. This is the real danger for equities.”

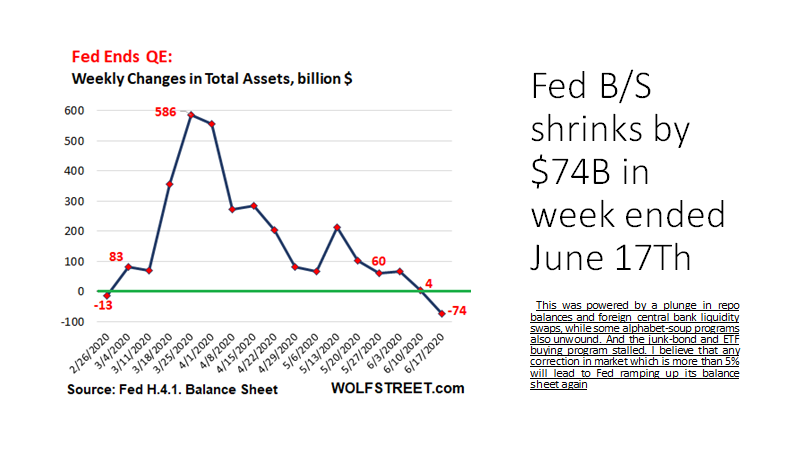

Repo Volumes are rising in a similar fashion to the beginning of the crisis in February. Liquidity is leaving the system. Last two days, repos (O/N and term) rose above $100Bn. S&P500 topped on February 19 while repo volumes were about half of what we are seeing today. By the time we hit $100Bn in repos (March 3), the index had dropped 10%.

We had about two weeks (March 3-March 22) of repos printing about $128Bn on average per day. S&P 500 bottomed on March 23 as the Fed started stepping in with its various programs. Repos went down below $50Bn on average a day. More importantly liquidity started flooding the system. Reverse repos skyrocketed from $5bn on average per day to $143Bn a day by mid-April! Equities rallied in due course.

April/May, things went back to normal: repo volumes between $0Bn and $50Bn a day and reverse repos averaging about $2-3Bn a day->Goldilocks: liquidity was just about fine. Equities were doing well. Then in the first week of June, repos jumped above $50Bn, and last Friday and today they went above $100Bn. Reverse repos are firmly at $0Bn: they have literally been $0Bn for the last 4 days.

Again, just like in February, liquidity is starting to get drained from the system. By that level of repo volumes in March, equities were already 10% lower from peak. S&P500 is just a couple % below that previous peak, but Nasdaq is above!

I am not sure why the market is here. It could be that, in a perfect Pavlovian way, investors are giving the benefit of the doubt to the Fed that it will announce an increase of its asset purchasing program at this week’s FOMC meeting. If it doesn’t, US equities are a sell.

And don’t be fooled by no YCC or any forward guidance. The Fed needs to step in the UST market big way. YCC on 2-3 year will do nothing. Fed needs to do YCC on at least up to 10yr. As to really address the liquidity leaving the system, Fed needs to at least double its weekly UST purchases.