Last Tuesday night, around 10:30pm the Google search term, “How to apply for Canadian citizenship,” spiked.

Other popular searches that night included “how to move to Canada” or simply, “move to Canada.”

This was in response to two men in their 70s childishly bickering at each other for an hour and a half, televised live across the world.

For people in the United States, Canada always seems to be the first place that comes to mind whenever they think about leaving.

It seems every time there’s a controversial election, for example, a bunch of celebrities always threatens to move to Canada. (In 2016, the list included Snoop Dogg, Barbara Streisand, actor Bryan Cranston, and comedian Chelsea Handler… though none of them actually moved.)

It’s an obvious first choice given the similarities between the two countries.

But if you’re serious about making a move– or at least identifying a place you -might- consider moving to– before the chaos escalate, taxes go through the roof, or the public schools convince your child to identify as a seedless watermelon. . . then take a look at the menu.

The world is a big place, and there are dozens of countries around the world to choose that offer the widest variety of climate, culture, lifestyle, nature, business/investment opportunities you could imagine.

If you do like the cooler climate, with four distinct seasons, maybe look into Estonia or Georgia– both offer certain remote workers residency for a year. You could try it out, and see if you are serious about leaving your home country behind.

If you want to be in a similar time zone as North America, you could go south to Panama or Barbados, both of which have straightforward residency processes or temporary work permit options.

If Europe is more intriguing, Spain, Portugal, and Germany all have temporary visa options that allow you to live and work there as long as you have sufficient income or savings.

And if you REALLY want to just hop across the border, don’t forget about Mexico.

Hollywood has done tremendous work to brutalize Mexico’s reputation as a haven for violence. But that’s only true in certain parts of the country.

It would be as if foreigners judge the US based on antifa violence in Seattle and Portland, or the murder rate in downtown Baltimore. Most of the country is pretty quiet by comparison.

For instance, in areas like Mexico’s Yucatan state, crime is actually on par with the State of Wyoming.

Some of the countries I mentioned, including Mexico, Panama, and Portugal, allow permanent residency which can lead to full citizenship and a second passport.

If you happen to NOT be a US citizen, moving abroad generally means that you can completely divorce yourself from your home country’s tax system.

And if you’re a US citizen, moving to another country means that you can take advantage of the Foreign Earned Income Exclusion.

For tax year 2020, the Foreign Earned Income Exclusion means expats can earn up to $107,600 in wages without paying a dime of US federal income tax.

If you’re married, your spouse can qualify too. Plus there are generous housing allowances as well. So you can earn roughly $250,000 or more per couple and put almost all of it in your pocket.

Depending on which state you currently live in, you’d have to earn a pre-tax salary of roughly $400,000 in order to put the equivalent $250,000 in your pocket each year.

Not to mention, there are plenty of countries overseas where the cost of living is MUCH cheaper, where the schools, medical care, housing costs, etc. are incredibly low.

So there can clearly be a lot of financial benefit to living outside of your home country.

It’s a big world out there. There are so many options.

I’m not suggesting that you pick up and move. I am, however, suggesting that you at least think about it.

Consider what’s important to you: what are the most important characteristics of a potential new home?

Tax benefits? Nature? Safety and security? Medical care?

Whatever your priorities are, there are probably several options that tick the boxes.

And, as part of a good Plan B, it makes sense to at least have some of those options identified, regardless of whether or not you choose pull the trigger.

Back in July, one of the most respected credit strategists on Wall Street caused stunned gasps across the financial world, when he admitted that he is “a gold bug.” Deutsche Bank’s Jim Reid may have been forever cast out of the ranks of polite, non tinfoil hat/conspiracy theory society when he said that in his opinion, “fiat money will be a passing fad in the long-term history of money”, a shocking admission (if one that many of his peers secretly harbor) for most financial professionals who are expected to tow the Keynesian line and always believe in the primacy of fiat and its reserve currency, the US Dollar.

Of course, for those who have been following Reid’s writings over the past few years (we feature his Daily Morning Reid note in our AM wrap), that admission was hardly a surprise: for much of the past decade, he has been closest to saying what most rational, clear-thinking people on Wall Street – and elsewhere – think and believe, yet are afraid of speaking it for fears of direct and indirect retaliation from an established monetary and financial system which has zero tolerance for anyone casting doubts over its viability (the fact that he works at Deutsche Bank is an added bonus).

For those unfamiliar with his work, some of his more notable recent writings can be found below:

Reid’s natural curiosity and eagerness to ask the right question even if it provokes established financial dogma is why we read his latest must-read long-term asset return study titled appropriately “the Age of Disorder” with great interest, and why we republish the executive summary in its entirety because for better or worse, he gets it right (we will have several follow up posts to follow).

* * *

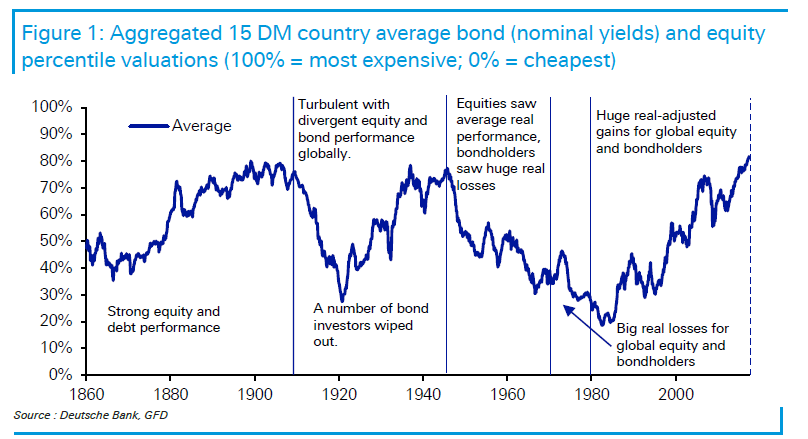

Economic cycles come and go, but sitting above them are the wider structural super-cycles that shape everything from economies to asset prices, politics, and our general way of life. In this note we have identified five such cycles over the last 160 years, and we think the world is on the cusp of a new era – one that will be characterised initially by disorder.

Not all disorder is ‘bad’. Indeed, if the themes of the world economy swing like a pendulum, then it may be that some have swung too far from a ‘sensible centre’ and are due to revert. This can have a cleansing effect. What is worrying, though, is that several themes appear poised to revert at a similar time. This is the point – that simultaneous changes to structural themes will create a level of disorder that will define a new era.

Before we review the key themes of the upcoming “Age of Disorder”, we must note that while some historical super-cycles have begun and ended abruptly, others were slower to evolve and end. The most recent era – the second era of globalisation, during 1980-2020 – is much more like the latter. It started slowly and has been gradually fraying at the edges over the last half-decade. The end of this era has been hastened by Covid-19 and – when, in years to come, we look at the rearview mirror – we may see 2020 as the start of a new era.

By our measure, there have been five distinct eras in modern times, with a sixth likely starting this year:

The first era of globalisation (1860-1914)

The Great Wars and the Depression (1914-1945)

Bretton Woods and the return to a gold-based monetary system (1945-1971)

The start of fiat money and the high-inflation era of the 1970s (1971-1980)

The second era of globalisation (1980-2020?)

The Age of Disorder (2020?-????)

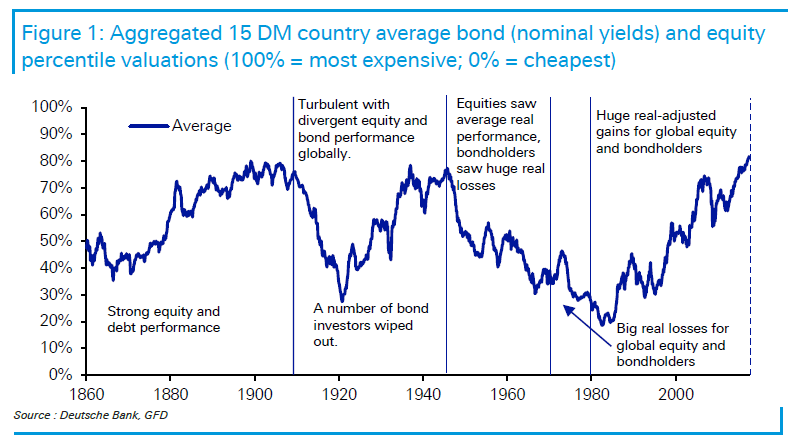

The era of globalisation to we are likely waving goodbye saw the best combined asset price growth of any era in history, with equity and bond returns very strong across the board. The Age of Disorder threatens the current high global valuations, especially in real terms. We believe this coming new era will be marked by at least eight themes, which we will briefly summarise in this executive summary and then expand upon in the full note.

Deteriorating US/China relations and the reversal of unfettered globalisation.

A make-or-break decade for Europe, with muddle-through less likely following the economic shock of Covid-19.

Even higher debt and MMT/helicopter money becoming mainstream.

Inflation or deflation? As a minimum, it is unlikely it will calibrate as easily as we saw over the last few decades.

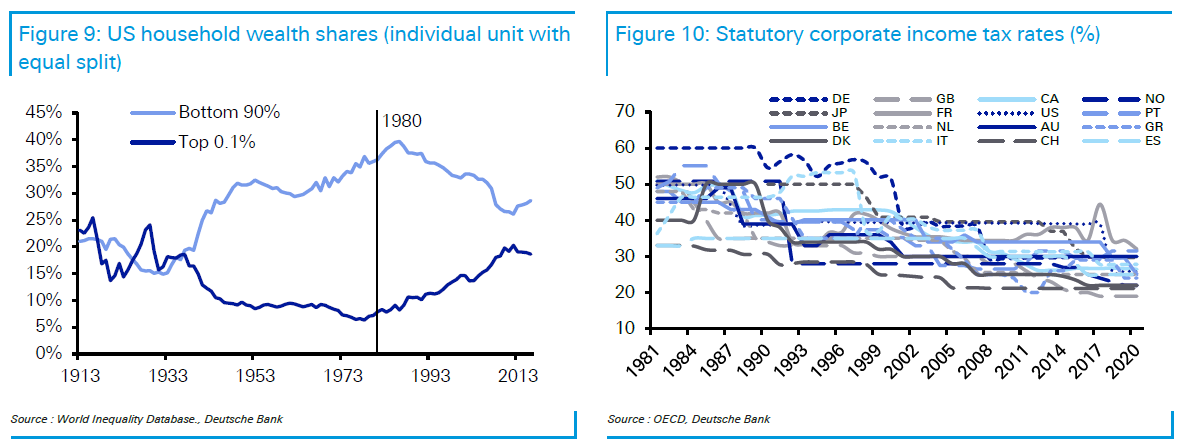

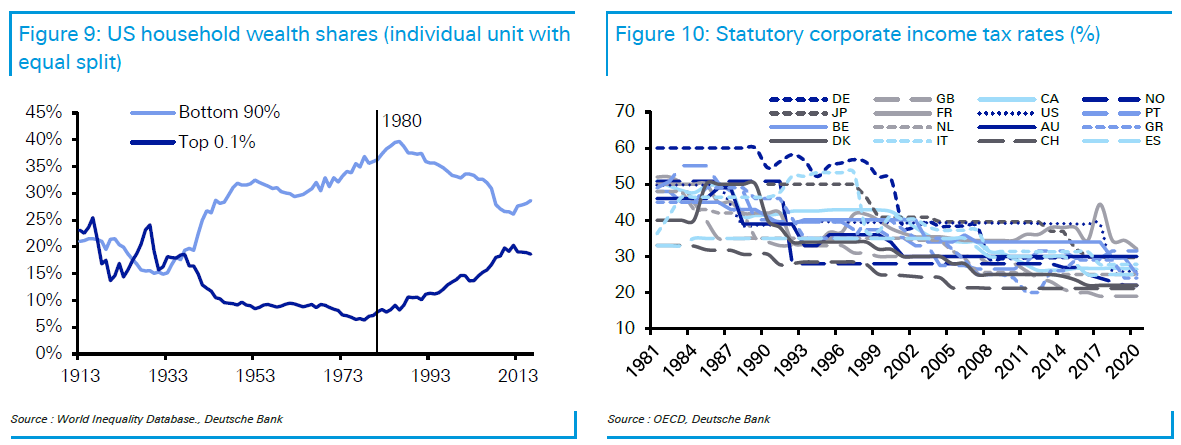

Inequality worsening before a backlash and reversal takes place.

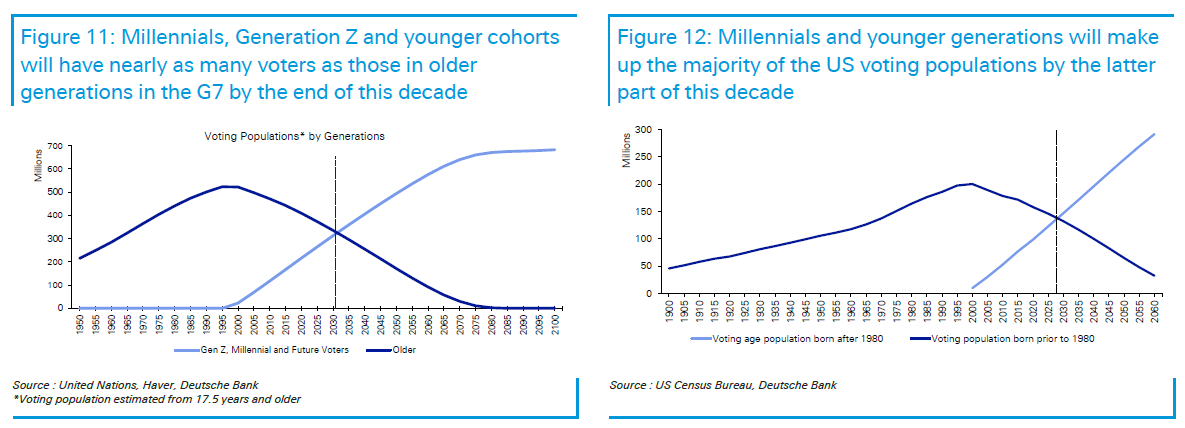

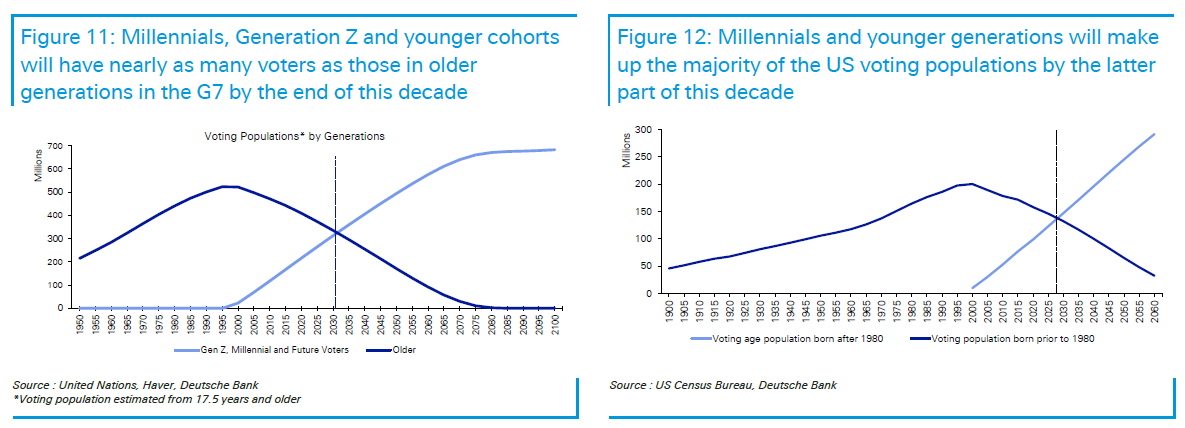

The intergenerational divide also widening before Millennials and younger voters soon start having the numbers to win elections and, in turn, reverse decades of policy.

Linked to the above, the climate debate will build, with more voters sympathetic and thus creating disorder to the current world order.

We’re in the midst of a technology revolution with astonishing equity valuations reflecting expectations for a serious disruption to the status quo. Revolution or Bubble? Also, if WFH becomes more permanent, it will cause major changes to societies and economies. Big cities were huge winners in the previous era, and this could now reverse.

Although some of these themes have been around for some time, it is only recently that they have begun to feed off each other to hasten the demise of the second era of globalisation. Their increased interaction has thus created the conditions to start their own new era of much change.

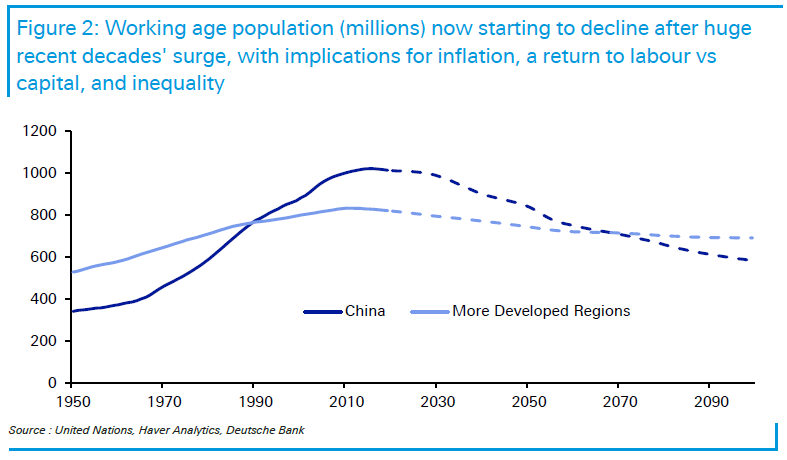

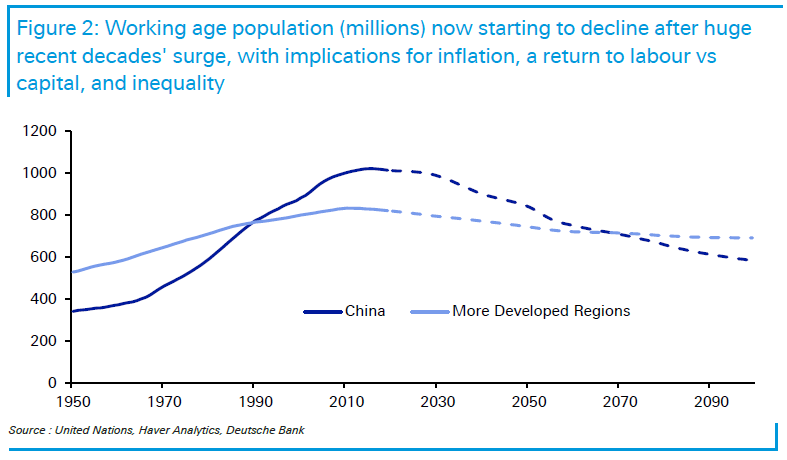

The key to understanding this new age of disorder, then, is to see how its themes emerged during the most recent era of globalisation. This was the era that began around 1980, when the world accelerated the move to abolish regulations and capital controls, which subsequently boosted free trade (and global capital flows) and begat a more liberal world order. Global demographics massively supported this phenomenon and ensured a huge increase in workers, many of them from China and other low-income countries. By the mid-1980s, the second era of globalisation was in full flow.

This era was win-win for most of the globe, and everything fell into place over the next three to four decades. Inflation fell largely due to a huge surge in workers (now behind us), and there was also downward pressure on wage inflation due to global labor market integration. In addition, there was help from direct central bank policy, including increased independence around the world. Lower inflation meant lower bond yields (real and nominal) and lower interest rates, and this all allowed for ever-higher equity valuations and profits. As a result, equities generally performed very well relative to what was slowing developed-market growth.

The cracks in this era began to emerge after the GFC, which revealed that ever-higher leverage had papered over the problems that globalisation had created in many Western countries. Firmly in the spotlight were issues including low real wage growth, the outsourcing of many low-paid jobs, and increased inequality. In response, authorities used heavy intervention (especially monetary) to prop up the existing system (rather than reform it), but populism and resentment built. The Brexit and Trump victories were manifestations of this anger in the UK and US, but populism increased across the globe. It was then that most people realised the era of full-feted globalisation was certainly fraying and the problematic issues it had incubated were about to take centre stage.

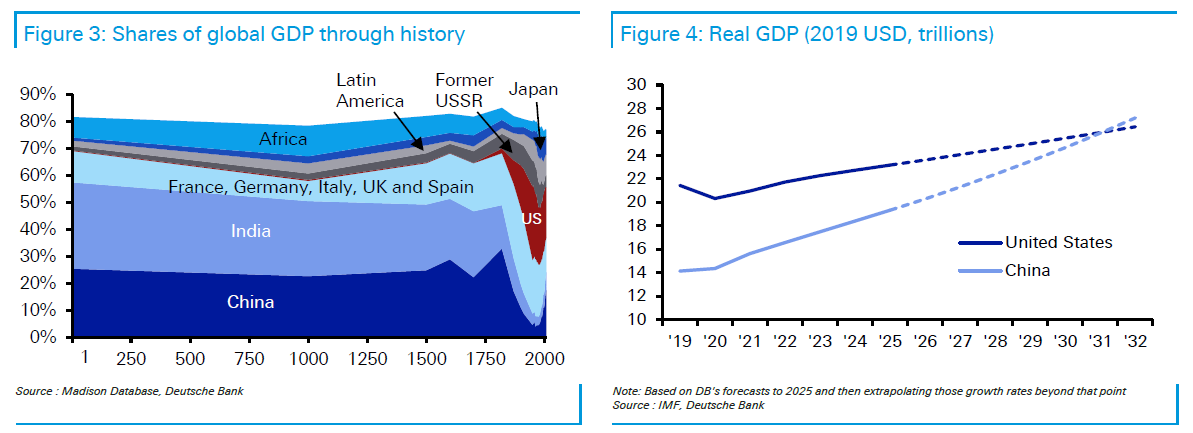

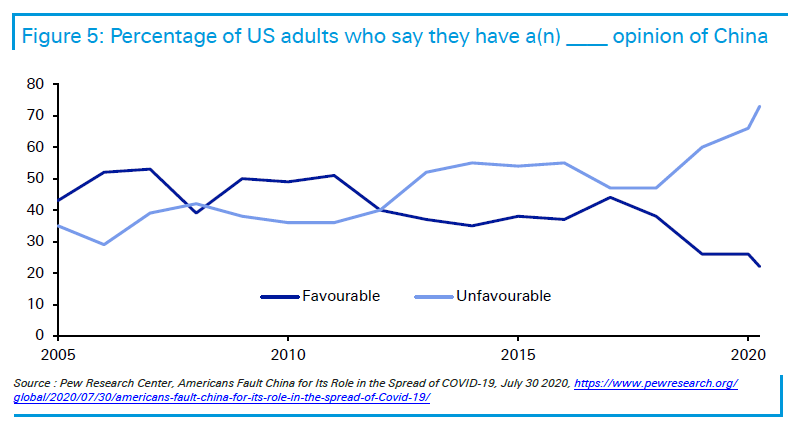

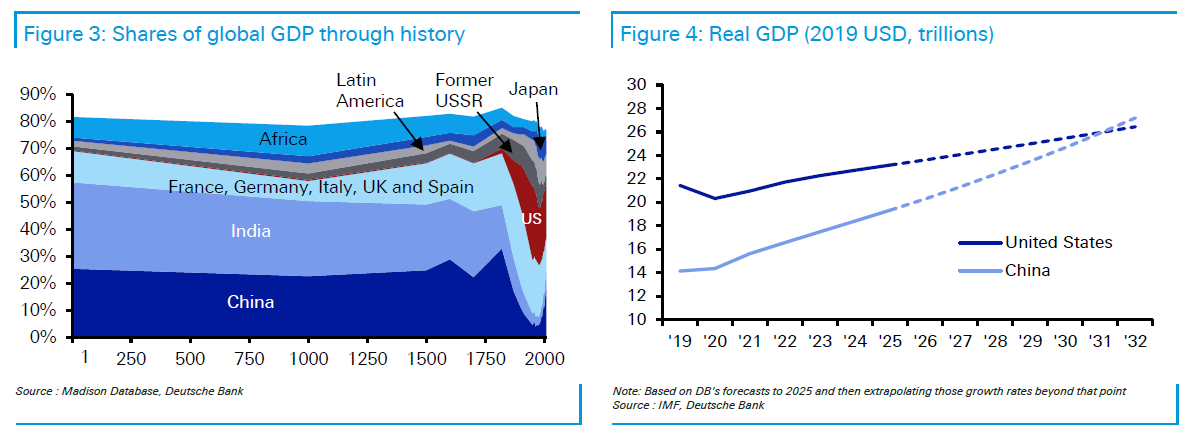

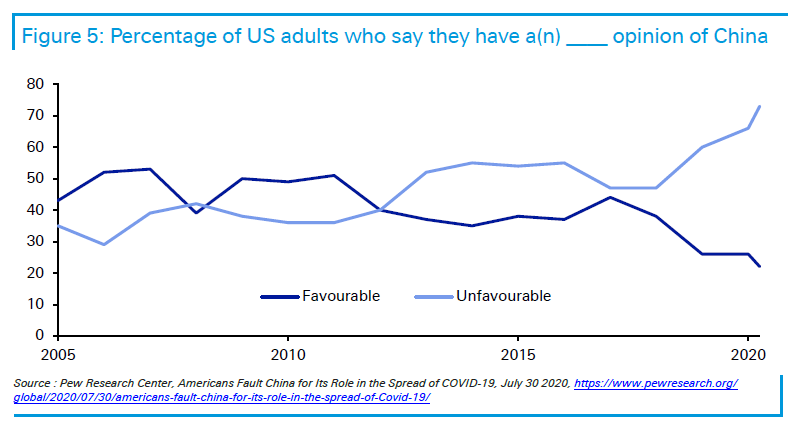

As the Age of Disorder begins, we believe one of the biggest issues will be the political tension between the US and China. Indeed, this should characterise the era of disorder because China has been at the heart of the most recent era – that of globalisation. The future of this relationship can only be forecast by understanding the past. We delve into this in more detail later, but to summarise: China is looking to restore the position it held for much of history as a global economic powerhouse. To illustrate, from two thousand years ago until the early nineteenth century, the country represented around 20-30% of the global economy. It then suffered under colonial powers, particularly in the century before Mao established the modern Chinese state in 1949. By the early 1960s, China’s share of the global economy hit an all-time low of 4%. It is now back to 16%.

While China’s fortunes rapidly grew during the era of globalisation, so too did tensions with the West. Partly, this came from the incorrect assumption in the West that as China developed it would increasingly become more Western in its outlook and values, and fully integrate into the liberal world order, which contains much American architecture. With hindsight, this was naïve as China has a long, proud and powerful history with its own values.

A clash of cultures and interests therefore beckons, especially as China grows closer to being the largest economy in the world. From the West’s point of view, China would not be in its current position if the West had not accepted China into its economic orbit during the latest era of globalisation. Now, the Covid-19 pandemic will likely speed the symbolic point at which China overtakes the US economy as the largest in the world. China has seen a post-Covid V-shaped recovery already, while it has become obvious that recovery in many Western countries will be a lengthier process. Assuming its current trajectory continues, China could become the world’s largest economy around the end of this decade or soon thereafter. Regardless, the crossover point with the US seems only a matter of time.

As the economic gap between the US and China narrows, many worry about the so-called Thucydides Trap. This refers to the fact that on 16 occasions over the last 500 years, a rising power has challenged the ruling one, and on 12 occasions it ended with war. While a military conflict today seems highly unlikely, an economic battle is likely to ensue, with the benign global trading conditions of the globalisation era likely to be resigned to the history books. The result of the US election in November is unlikely to change the direction of travel. Over the course of this decade, relations will likely deteriorate into a bipolar standoff as both the US and China seek to prevent encirclement by the other. Companies that have embraced globalisation will be stuck in the middle if relations sour as we fear.

The second theme of the Age of Disorder is that the 2020s could be a make-or-break decade for Europe. The strains on the continent were evident prior to Covid-19, but the virus has probably reduced the chance of the 2020s being a muddle-through decade like the 2010s. The economic divergence between countries will likely be even more pronounced and, as such, it feels like the probability of both integration and disintegration has increased over the last six months. On the one hand, the Recovery Fund is a genuine and welcome step in the right direction, but it needed to be. On the other hand, given the economic issues ahead, further measures will probably become necessary in the years ahead to prevent maximum disorder.

Even if further economic stimulus can be negotiated as needed, it is likely to be done against a backdrop of consistent volatility and brinkmanship, particularly if domestic politics across the continent gravitate away from those consistent with further EU integration. With the Covid economic shock, that must be a greater possibility now. So the chances of muddling through for Europe have decreased, while the potential for both further integration or disintegration has increased post-Covid. Even if integration wins out, it may still take an acute threat of disintegration to concentrate political minds.

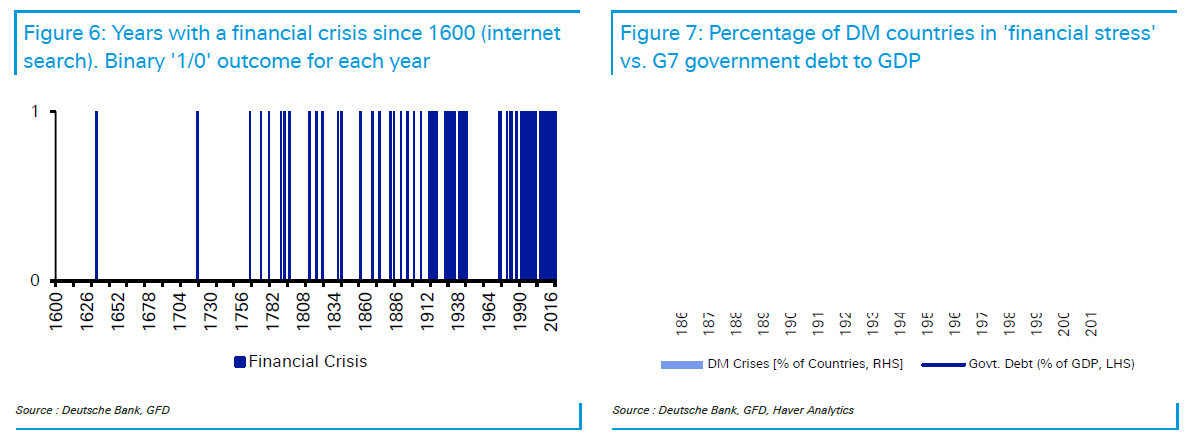

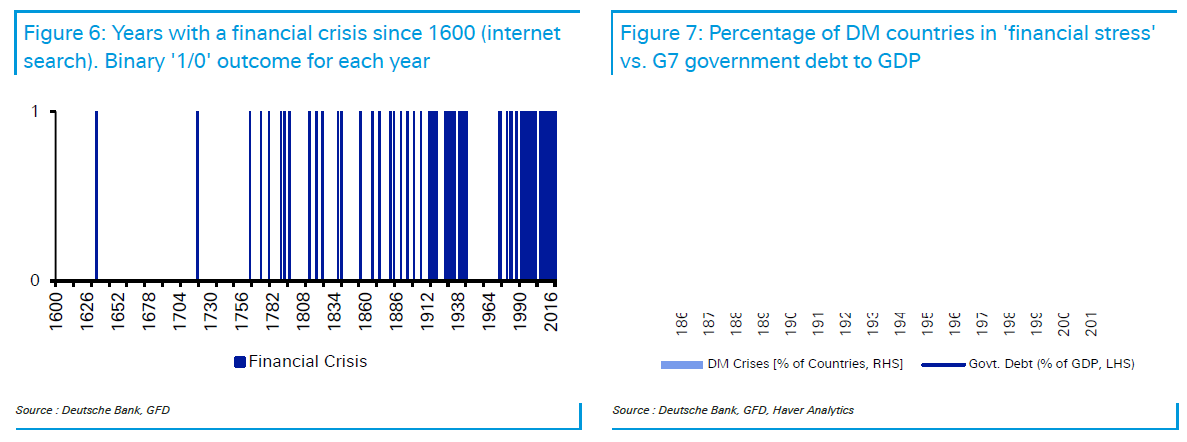

A key problem Europe faces is that many of its countries have too much debt, and this leads straight to our third theme in the Age of Disorder. Far from being just a problem in the European periphery, debt is a global issue – and it is only because central banks have distorted free markets that global borrowing can be financed at a viable interest rate. Given central banks have committed to underwriting the post-Covid recovery, they will have an even more outsized role over the years ahead. Our work in a previous long-term study “The Next Financial Crisis” suggests that periods of higher debt lead to a higher intensity of financial shocks and crises. This trend will be amplified by the Covid-19 crisis and means we will likely see more crises, more disorder and even more money printing in the years ahead. Yes, lower interest rates mean we can run with more debt, but a high-leverage society is always likely to be more shock-prone.

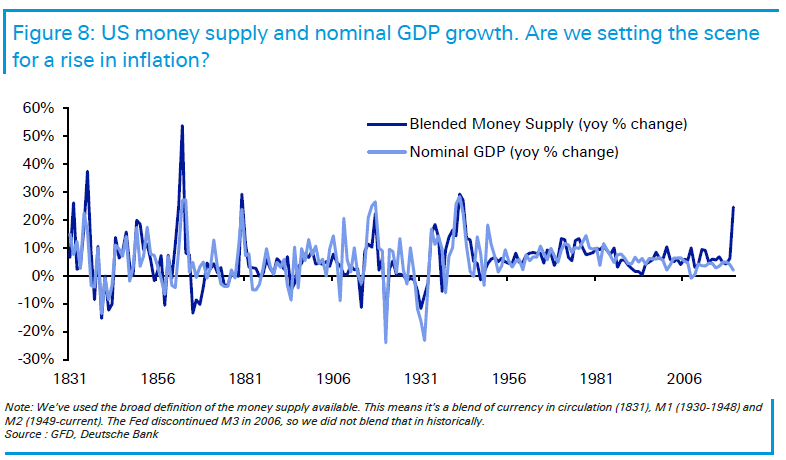

The extent to which we can reduce the huge global debt burden depends heavily upon the fourth theme in the Age of Disorder – inflation. On this topic, DB is still split on whether the debt and Covid-19 crises will be inflationary or disinflationary. Although this team is in the inflationary camp, we acknowledge that the outcome is path-dependent. If we move to a MMT/helicopter-money type world, where both fiscal and monetary policy are expansionary, it is pretty easy to see a jump in inflation. For us, Covid-19 has forced global policy makers to cross the Rubicon with regards to expansionary fiscal policy, and it is unlikely that they’ll go back to the austerity of the early-2010s – and with ultra-loose monetary policy almost guaranteed, this will put us in a completely different world order to that seen previously and create a very different macro environment. However, if we’re wrong and governments prioritise the repair of their balance sheets, then – even if central banks keep printing – we are likely to be stuck with low inflation for a longer period. With so much debt, such a scenario will also almost certainly ensure its own elements of disorder ahead.

Regardless of which outcome materialises, it feels that the ability of policymakers to perfectly calibrate inflation towards target in a post-Covid world will be incredibly difficult given the size of the opposing forces. So we expect a higher probability of more extreme outcomes going forward.

As the outcomes become more extreme, they will heavily influence how progress is made on inequality – our fifth key theme. It may initially worsen, but the need to pay for the Covid shock, and perhaps the reduction of globalisation, may encourage governments to increase taxation on those with deeper pockets. This is likely to be biased towards the highest-paid individuals, but also companies as they have benefited from a race to the bottom in corporate tax in the globalisation era. Technology firms are already attracting greater attention on this front, especially as they have largely benefited from the pandemic.

The discussion of inequality within and between countries will not be limited to wealth and income. In fact, an issue that is quickly emerging as a political force is the intergenerational gap. This is our sixth theme in the Age of Disorder. This segment of inequality has been allowed to build and build in the globalisation era. The general assumption is that the divide between the young and old will worsen as the population ages, and the self-interest of the older generation will ensure that the status quo continues. However, this misses the key point: the age at which the intergenerational divide begins is not constant. It is likely that this age will increase over time as those left behind are unable to catch up and thus the average age of discontentment with the status quo continues to increase over time.

The Millennial generation (born in the early 1980s), along with Generation Z and younger voting cohorts, are firmly established as generational ‘have nots’. Yet in G7 countries, the combined size of these groups is fast catching up to that of the generations born prior to the Millennials. The two groups on either side of the divide will be close to neck-and-neck by the end of this decade in aggregate and slightly earlier in the US.

NEVER MISS THE NEWS THAT MATTERS MOST

ZEROHEDGE DIRECTLY TO YOUR INBOX

Receive a daily recap featuring a curated list of must-read stories.

Assuming life does not become more economically favourable for Millennials as they age (many find house prices increasingly out of reach), this could be a potential turning point for society and start to change election results and thus change policy. This is particularly the case when we recognise that the votes for Brexit and Trump in 2016 left many younger people feeling angry and alienated by political decisions that a sizable majority of them were against.

Such a shift in the balance of power could include a harsher inheritance tax regime, less income protection for pensioners, more property taxes, along with greater income and corporates taxes already mentioned, and all-round more redistributive policies. The “new” generation might also be more tolerant of inflation insofar as it will erode the debt burden they are inheriting and put the pain on bond holders, which tend to have an ownership bias towards the pensioner generation and the more wealthy. The older generation may also have to be content with lower (or even negative) asset price growth if the younger generation does not have a sudden income boost.

Whether or not individuals see the above as ‘good’ or ‘bad’ is not necessarily the point. Rather, it seems clear that this will be a big break from the status quo and lead to far more disorder than in the prior era of globalisation.

Amidst the clash between the young and old, an increasingly fraught issue will be climate change – something that increased during and because of the recent globalisation era. This is our seventh key theme and is one where heavily polarised opinions exist – not just about the extent of the problem, but around the various options available to respond. Although the pandemic has displaced climate change from the front pages for now, as the size of the pro-climate younger generation grows, so too will the pressure on leaders to act.

We are likely to see huge pressures for a greener response to the post-pandemic economic rebuild. To move the world to a consumption-driven model of measuring and judging carbon emissions, we believe a carbon border adjustment tax is needed and this will likely be implemented this decade. Given more Millennials will be elected into positions of power over the coming decade, this tax will probably not suffer from the same watering-down as other environmental legislation. As such, a strong carbon border tax will reinforce the disruption to the status quo and create disorder for both companies and countries in terms of the relationships between them that in the era of globalisation were relatively calm.

Most of the trends identified here would likely have occurred without Covid-19, but many are now likely to be accelerated by its arrival. However, the pandemic brings disorder of its own, which leads us to our final point. As we go to print, we’ve now marked six months of working from home with no immediate end in sight for many. It’s reached a stage where much of this trend will have an element of permanence. This has major implications for cities, residential and commercial property, transport, workers and many ancillary sectors and general activities we’ve taken for granted over the last several decades. Big/mega cities have been major winners in the globalisation era. Will this trend reverse post-Covid? If so, this will have a major disorderly impact on society as we currently know it.

On a related theme, this is all occurring alongside record tech valuations in equity markets, with some astonishing valuations. It feels this could go one of two ways, both of which would bring large disruption. Either these valuations are proved to be justified and we’re close to major technological advancements impacting all facets of life, or we run the risk of a repeat of 2000 where a bubble burst even if much of the technology survived and progressively became integrated into our lives in a more normal evolutionary manner. The latter would have major financial market consequences for a period of time, but would be less revolutionary. The answer is perhaps a combination of both: rapid technological change that is both positive and disruptive but with stark winners and losers in both the tech sector and the wider global economy.

So, the Age of Disorder is likely upon us. In the years ahead, simply extrapolating past trends could be the biggest mistake you make.

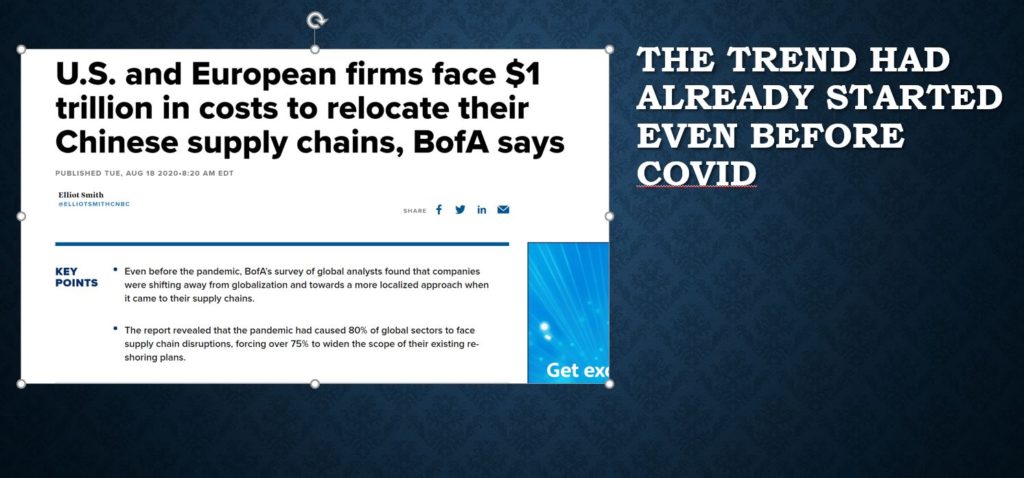

Before the world had even heard of the coronavirus, the intricate transnational trade networks that feed the modern factory already appeared vulnerable. A wide range of forces are responsible: From trade disputes to national security concerns to climate change and the rise of automation and robots. “It’s not just one factor but many,” says Candace Browning, head of BofA Global Research. “And what’s remarkable is that they’re all happening at the same time.” The result? A fundamental—and accelerating—shift toward de-globalization, as more and more companies are bringing supply chains, manufacturing and jobs closer to home, according to a report from BofA Global Research, titled Tectonic Shifts in Global Supply Chains.

What does this mean for the U.S. and global economies? How might companies best adapt to the changing environment, and could this present new opportunities for investors? Co-authors Browning and Ethan Harris, head of Global Economics for BofA Global Research, share their thoughts on this evolving trend and the seismic changes it represents.

What ignited your sense of urgency around the changes that may be underway in the global economy?

Candace Browning: We’re always looking beyond daily events at bigger economic trends affecting the United States and the world. We’d heard that companies were thinking more locally but wanted to gauge whether it was myth or reality. So, we surveyed our international team of equity analysts—who together cover some 3,000 global companies—and were struck by what we found. Across 12 industries ranging from semiconductors to capital goods, companies in more than 80% of those industries are rethinking, or plan to rethink, at least some of their supply chains. We weren’t surprised that companies are shifting from China towards lower labor costs in Southeast Asia and India. What really did surprise us was the number of companies, particularly in North America and Asia, that intend to “reshore” supply chains to their own country or region. Firms in almost all industries plan to make the transition work using robots and automation. Our forecast that industrial robots will double to 5 million units by 2025 may be conservative—and the cost of automation and robots keeps going down.

“What really did surprise us was the number of companies, particularly in North America and Asia, that intend to ‘reshore’ supply chains to their own country or region.”

– Candace Browning, Head of BofA Global Research

What exactly are supply chains, and why is this shift so significant?

Ethan Harris: For 60 years after World War II we witnessed a steady rise in international trade and revolutionary changes in how products are made and sold. Today, through complex networks of suppliers, a single smart phone or appliance contains parts sourced from many countries. In the last decade, though, international trade has leveled off, and our new findings suggest that what had seemed a relentless march toward globalization may now be reversing. Of course, that doesn’t mean that international trade will end. But when you consider that the companies in the 12 global industries we cover represent $22 trillion in combined market value, even incremental shifts toward “de-globalization” could have major implications for economies, jobs and consumers.

Why now? What’s driving this trend?

Browning: Higher wages in the developing world and advances in automation are reducing some of the cost benefits that have long made overseas suppliers so attractive. Another factor is ongoing trade tensions, even taking into account the new Phase-1 trade deal between the United States and China. National security is a growing concern as countries seek to protect their technologies. From an environmental, social and governance perspective, sourcing parts locally may leave a smaller carbon footprint and help companies ensure that suppliers treat employees well. It’s too early to know which of these forces will play the most important roles in de-globalization, but we’ll be watching developments closely.

Who might the beneficiaries be, and where are the challenges?

Harris: U.S. companies seem most ready to embrace automation and its cost savings. Technology companies and their suppliers could benefit as demand for robots rises. Generally, larger companies tend to have multiple suppliers and their scale may give them greater flexibility to adjust supply chains. China faces perhaps the greatest challenges. The underlying story is positive, with a rising middle class earning more money. But that means China needs to speed up its effort to depend less on exports and more on domestic consumers and services. The coronavirus, which has forced a number of Chinese factories to slow down or stop production altogether, contributes to these pressures.

Browning: Small U.S. businesses may also benefit as part of industrial “clusters” that develop when large manufacturers move into an area. Manufacturers spend 5.5% of domestic net sales on research and development, compared with 3.6% for non-manufacturers, so that, too, creates opportunities for companies that support them.1In some cases, reshoring will mean moving supply chains to nearby developing countries. So Mexico is likely to benefit from reshoring of U.S. companies, for example.

What does all this mean for workers and consumers now?

Browning: Some 400,000 U.S. factory jobs are currently unfilled, and companies are going out of their way to lure job seekers with higher wages, signing bonuses and other benefits. Moving supply chains closer to home will increase the demand for skilled workers such as welders, engineers and machine programmers—and manufacturing jobs already pay 15% more in total compensation than nonmanufacturing jobs.2 So, wages are likely to grow. But jobs, too. Ten years ago, conventional wisdom held that workers were all going to be replaced by robots. Yet while automated factories do require fewer employees, every new manufacturing job generates an estimated six additional jobs indirectly.

The benefits may be less pronounced among service companies, and unskilled workers will face steeper challenges. So companies and policymakers alike will have to emphasize retraining and other programs to help give workers the skills they need for the new manufacturing landscape.

Harris: For consumers, a lot depends on what the major forces behind de-globalization turn out to be. If it’s mostly about trade barriers, consumers will pay higher prices, which is obviously not good for them. But if it’s because companies find greater efficiency through automation and lower shipping costs, that’s good news for everyone. That story is still unfolding.

What risks does de-globalization present? Harris: Protectionism or national security could prompt government anti-trade policies that make this process happen much too quickly. In the technology sector, for example, different countries have developed very different capabilities. Forcing everyone to suddenly shift to local supply chains would be incredibly expensive and quite disruptive. One of the toughest challenges for governments will be finding ways to address national security concerns while minimizing those disruptions.

“We’re calling this a ‘tectonic’ shift because we expect things to move slowly but persistently over the next five or 10 years. It won’t happen overnight, but some of the forces seem unstoppable.” –

Ethan Harris, Head of Global Economics, BofA Global Research

How quickly do you expect these changes to take place—and what should investors watch for? Harris: We’re calling this a “tectonic” shift because we expect things to move slowly but persistently over the next five or 10 years. It won’t happen overnight, but some of the forces seem unstoppable. National security and protectionist concerns aren’t going away. Automation’s not going away. Labor costs in China aren’t going to suddenly drop.

Browning: While de-globalization is likely to play out over a number of years, a look at market values and fund investments tells us that investors may not be fully prepared for a sustained recovery in manufacturing that could begin by mid-2020. We see opportunities ahead for industries ranging from automation to industrials to the banks that will help finance changes in supply chains. For these reasons, we believe investors should start thinking now about the implications for their portfolios, and how they can prepare for the global shift.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}