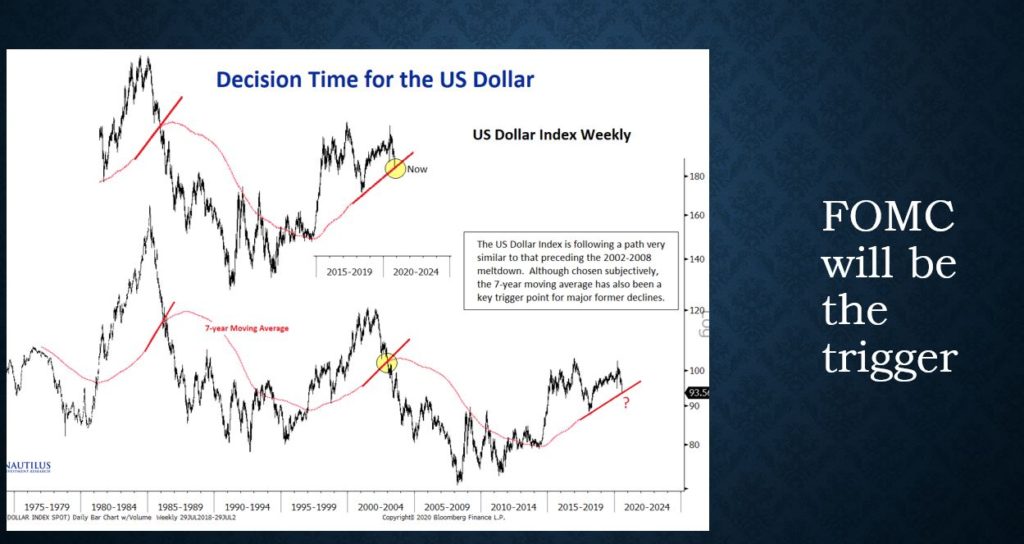

Making sense out of Chaos

In this week’s final installment of Louis-Vincent Gave’s three-part series on possible explanations for the recent rebound in global equity markets, Louis considers the possibility that investors are flocking into equities out of fear that the U.S. dollar could be worth a lot less in the years ahead. As you will read, two of the main beneficiaries of this tidal shift have been gold, which recently hit an all-time high, and gold miners, who have outperformed all other asset classes year-to-date.

THE CONSEQUENCES OF ‘WORTHLESS CASH’ BY LOUIS-VINCENT GAVE

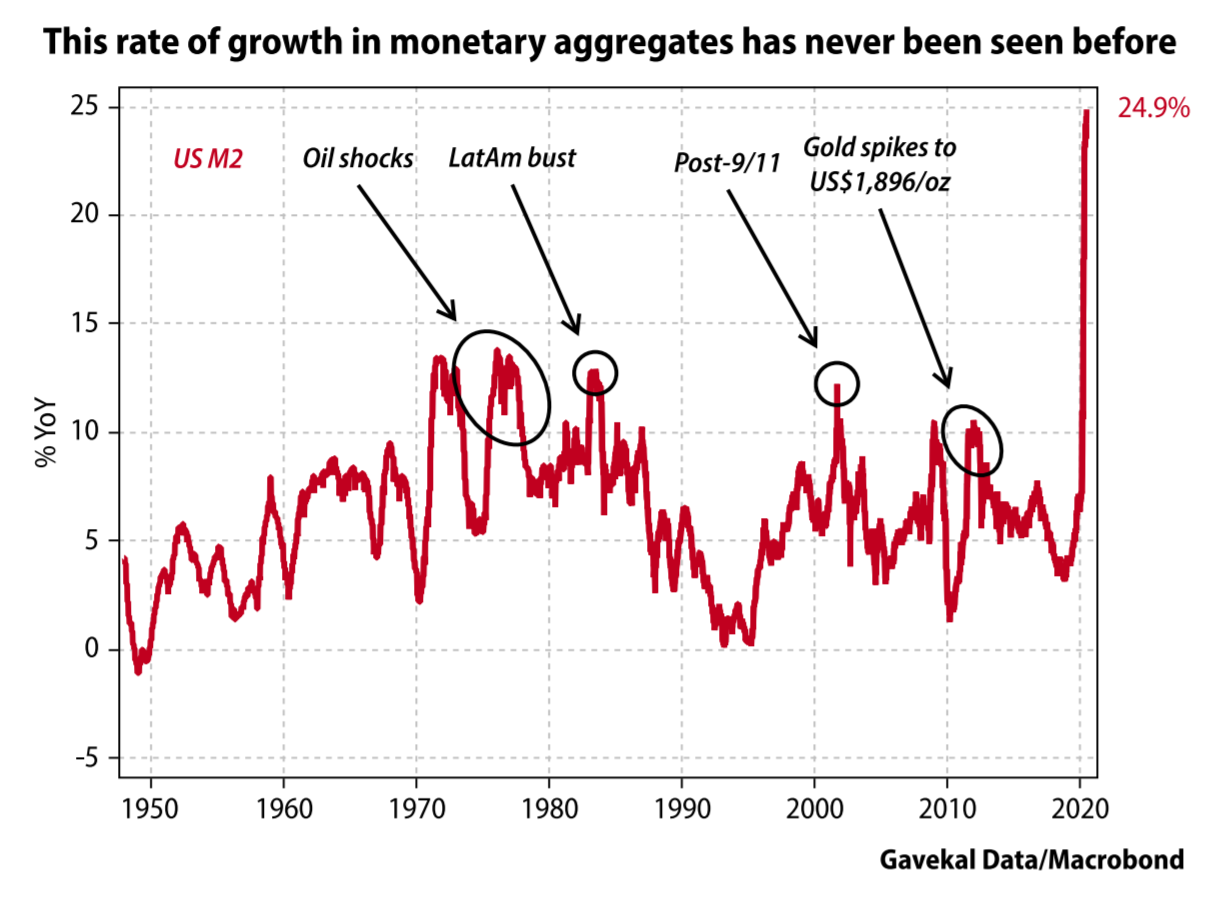

In the second quarter of this year, global equity markets registered their best quarterly performance in two decades. What was behind this record-breaking rebound? A number of explanations appeared possible. In the first paper of this series, I considered the possibility that markets were pricing in a return to the macro environment that prevailed in the post-2008, pre-Covid-19 world. In the second paper, I pondered the possibility that investors had simply lost their senses. In this, the third paper, I will consider the possibility that the present growth in monetary aggregates is leading investors to conclude that they have no alternative; money is being debased at such a pace that sitting on cash in a bank account is, over the long term, sheer madness.

Over the last few months US monetary growth has broken new highs week-after-week. Today US M2 growth stands at 24.9% year-on-year, more than six times the structural growth rate of nominal GDP. So the idea that cash is in danger of becoming worthless is no delusion; this rate of money printing has never been seen before in the history of the US, or of any other G7 economy.

An uncomfortable diagnosis

Finance 101 teaches that the price of an equity is determined by a company’s future cash flows, discounted by an interest rate, to which is added a risk premium. Theoretically then, to be successful an investor should only have to formulate a view on these three variables. But is it really that simple? Consider the following:

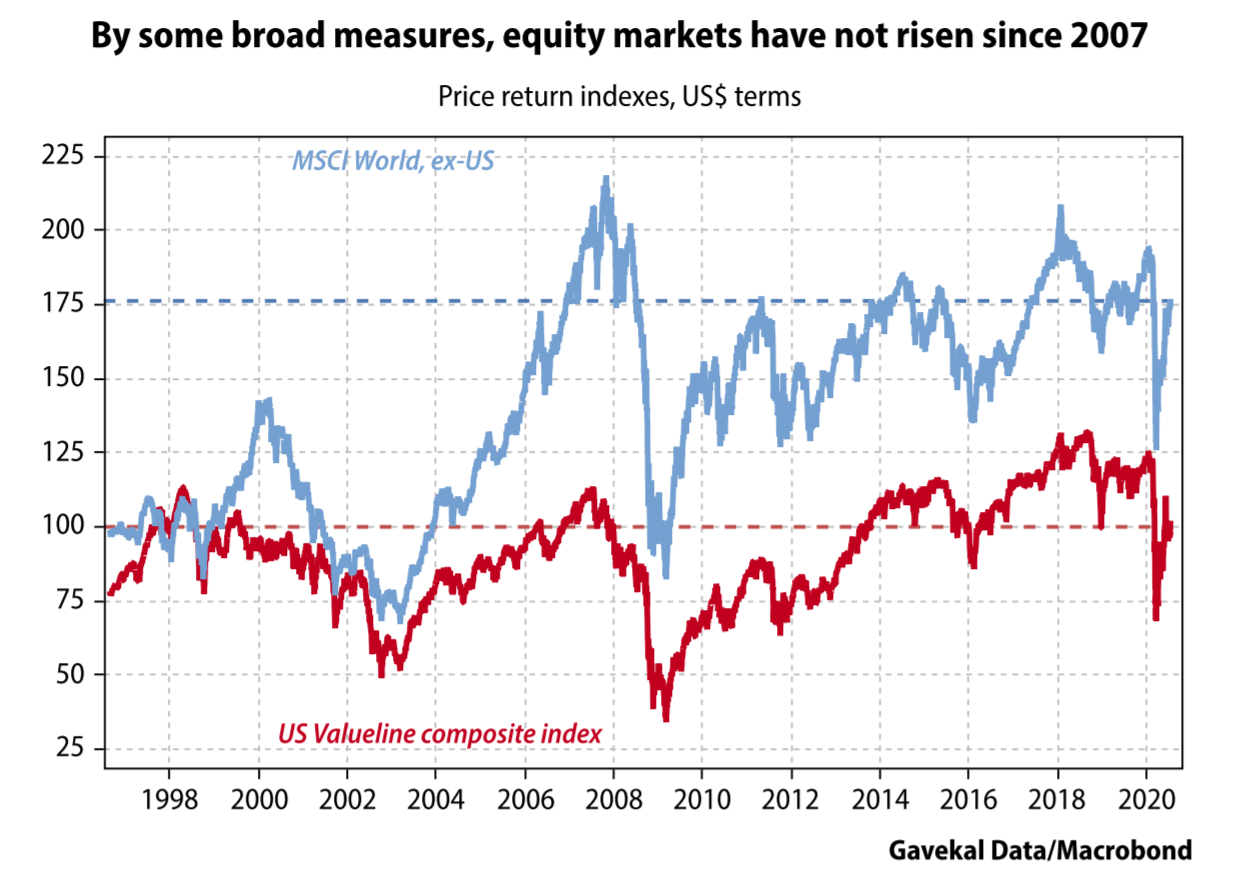

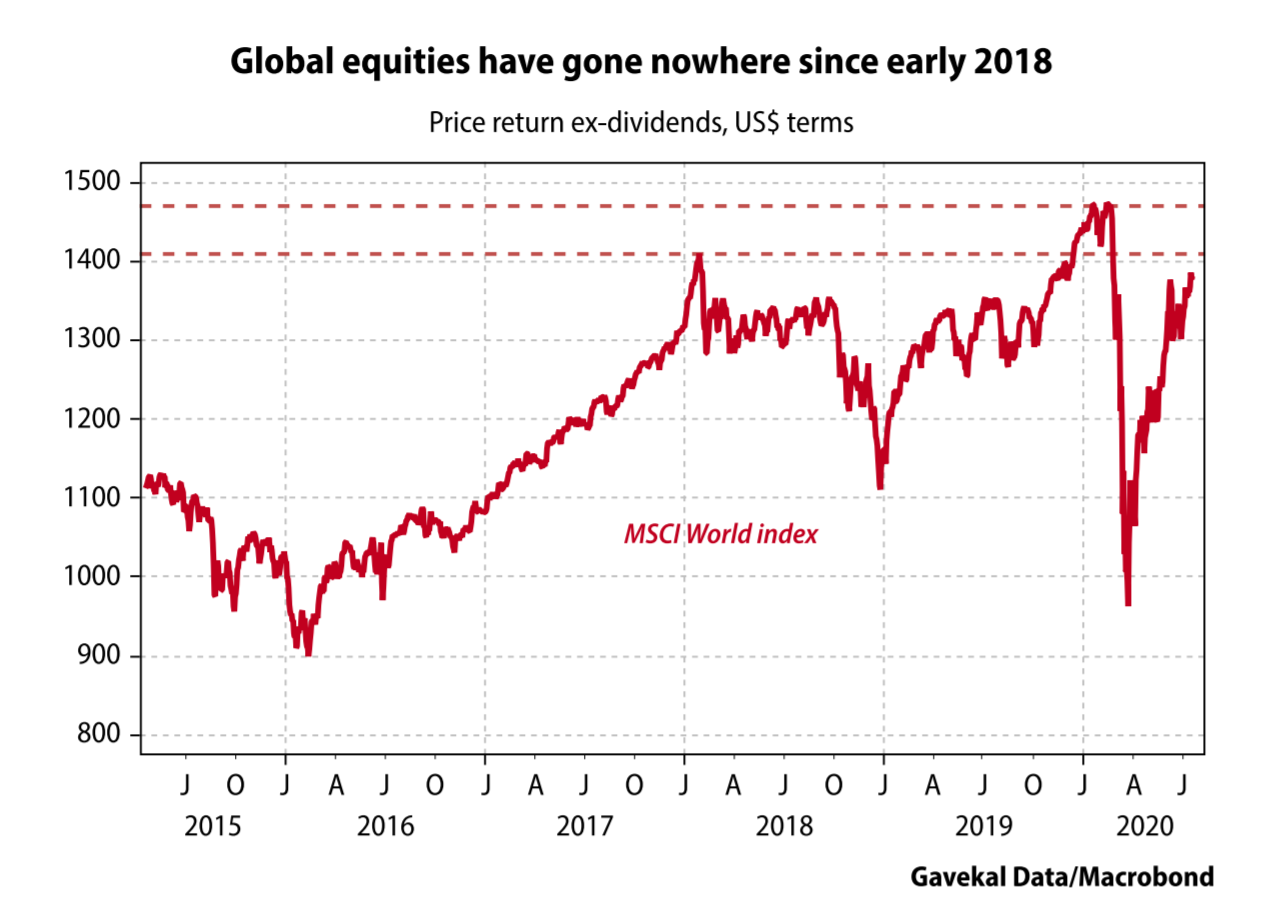

Or maybe the simpler explanation is that for all the talk about the rampaging equity bull market, global equities aren’t in much of a bull market at all. In the first two papers of this series, I pointed out that the MSCI World ex-US index has flatlined since both 2007 and 2014. Perhaps even more surprising, the Valueline composite index, which is arguably the best proxy for the performance of the median US stock, stands at the same level today as in 1998 (see the chart below).

Admittedly, the Valueline is a price index, and so does not include the contribution of dividends to total returns. Nevertheless, the failure of key broad equity market benchmarks to make anything like new highs despite all the talk of a rampaging equity bull market is remarkable. So where should investors actually look to find this remarkable bull?

Finding the rampaging bull

Defining a bear market is easy enough: if the price of an asset falls by a given amount—for equity indexes, usually -20%—then it is generally accepted that the asset is in a bear market. But if it is to be useful, the definition of a bull market needs to be more complicated. The financial media usually talk about a 20% rise as a “bull market,” but that hardly seems satisfactory. Under that definition, oil, which has more than doubled from its mid-April lows, would be in a bull market. However, very few energy investors have been popping the champagne corks lately.

So, it may be more useful to propose an alternative definition: an asset class is in a bull market when its underlying price continues to make new cycle highs.

This handy definition is particularly useful today, given that markets bottomed in mid-March 2020, and have since rallied hard almost everywhere around the world. Yet within this broad rebound, some assets have gone on to make new highs for the year, while others have not. With this in mind, it is easier to argue that the assets that have made new highs are in a bull market, while those that have yet to recover their start-of-the-year levels still have a lot to prove.

Using this—admittedly self-serving—definition narrows the current bull market down greatly, and so this investigation is within manageable limits. Sticking to the “must have made new year-to-date highs” benchmark, it becomes clear that:

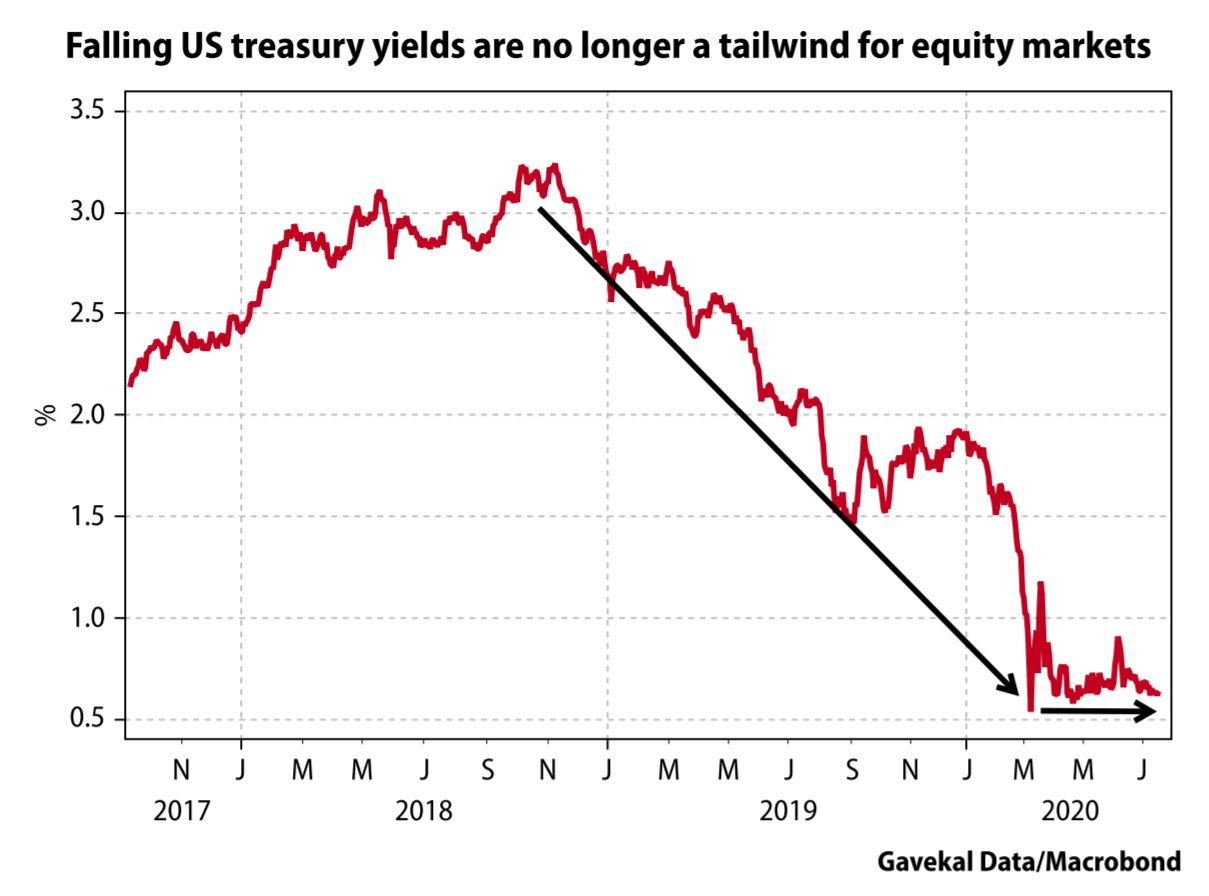

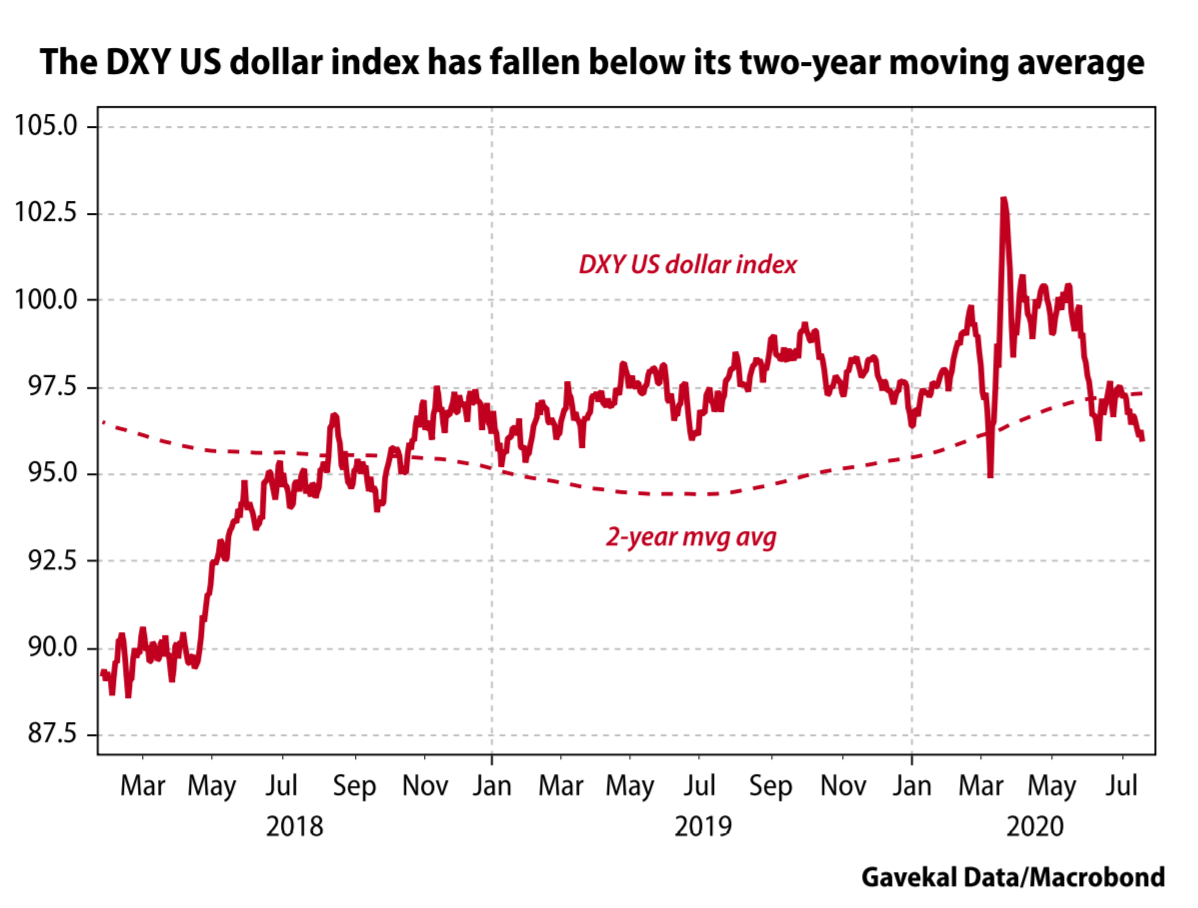

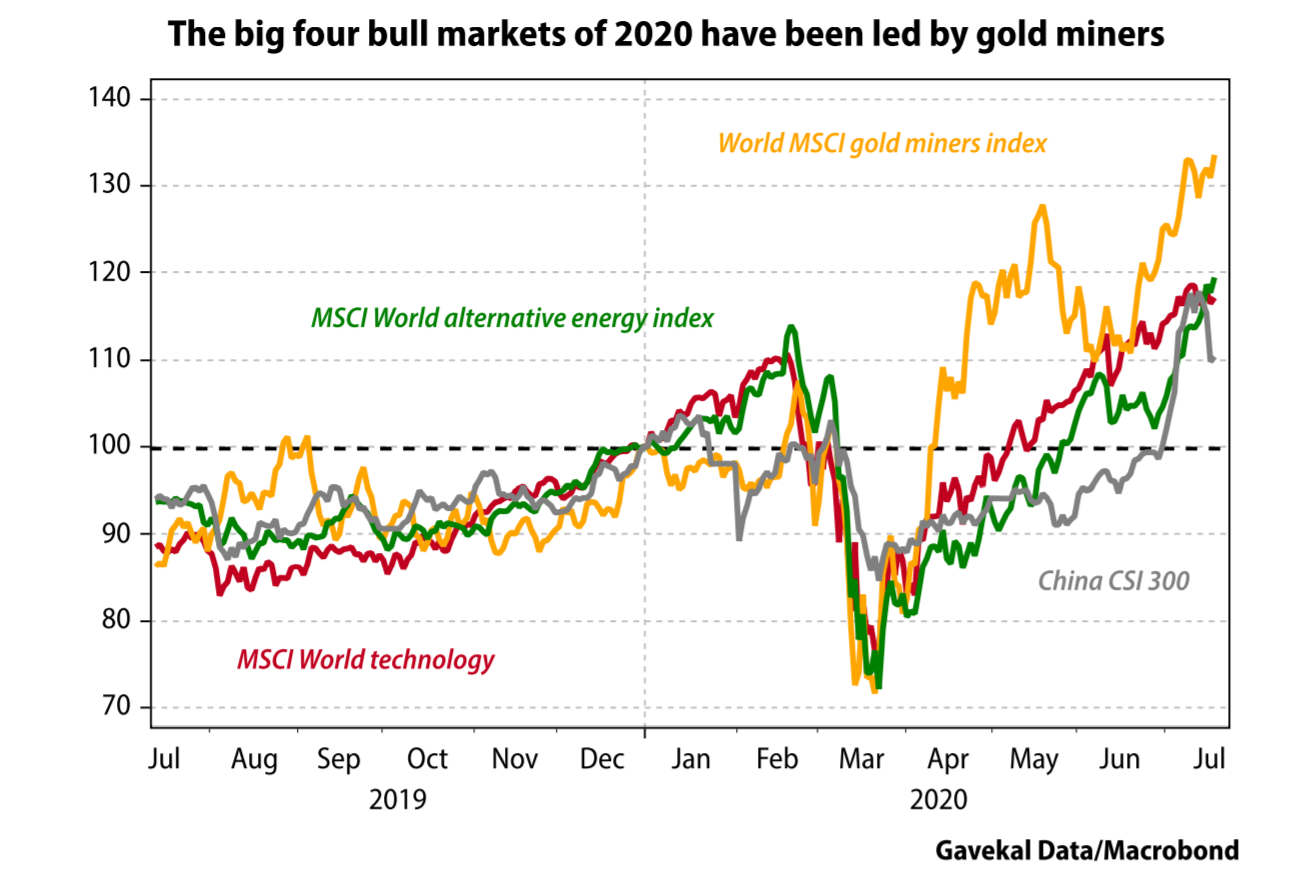

Nonetheless, behind this backdrop of flat interest rates, mild US dollar weakness and flatlining—albeit volatile—global equity markets, the rampaging bull has found a home in four different asset classes: (i) Big Tech, (ii) green investments, (iii) precious metals, and (iv) Chinese equities. And of these, precious metal miners have outperformed all other asset classes year-to-date. Let’s look at these four bull markets one-by-one.

The Big Tech bull market

Many liters of ink have been spilled over the Big Tech bull market. The subject is unavoidable, if only because Facebook, Amazon, Apple, Microsoft and Google now account for more than a fifth of the S&P 500. As a result, the decision either to overweight or to underweight Big Tech has made or broken many portfolio managers’ performance in recent years. And it’s likely to continue to do so for a good few years to come.

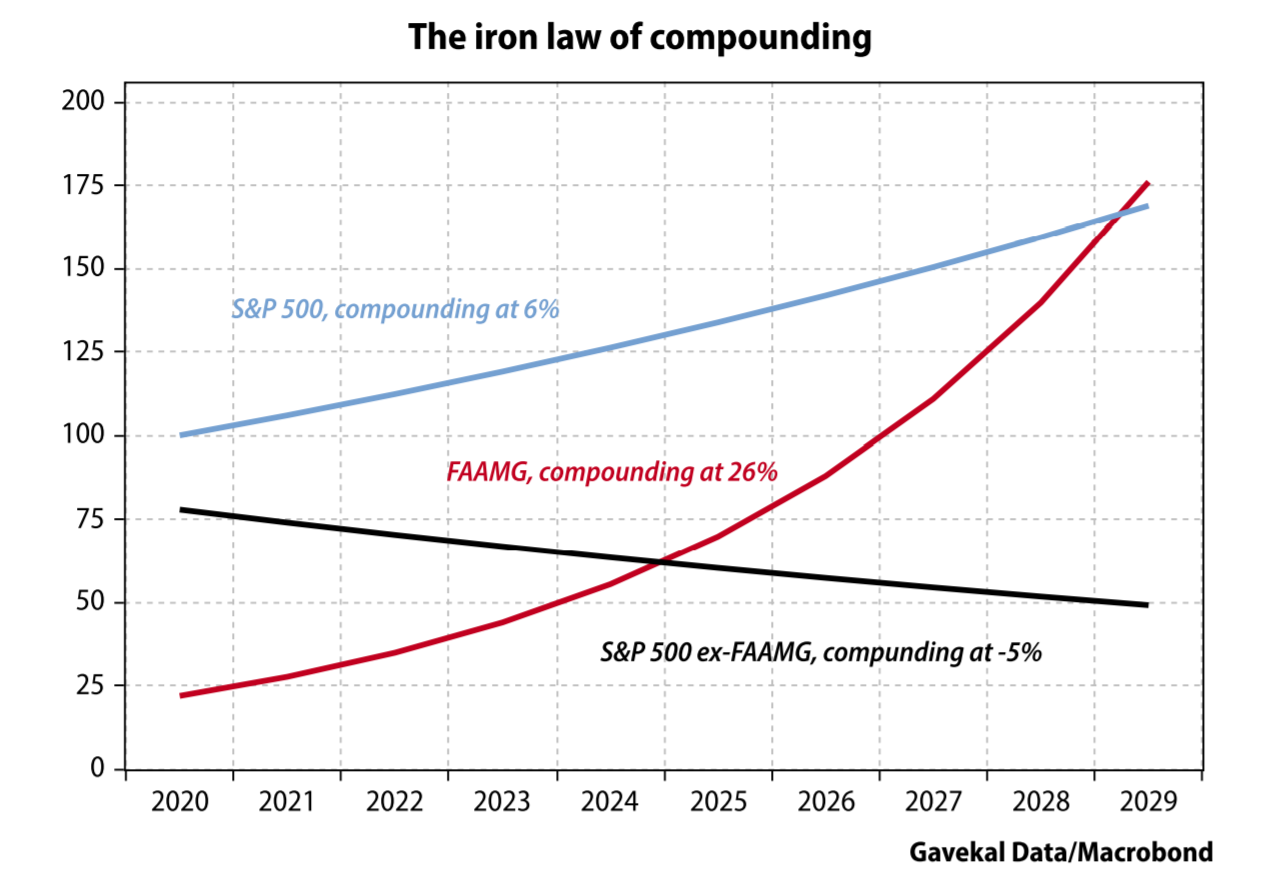

In Have Equities Become A Bubble?, I reviewed the most cogent argument against overweighting Big Tech—that the law of large numbers presents a serious hurdle to future gains. To illustrate this challenge, let me propose the following exercise. Let’s accept that:

If we accept these two points, then, as the chart below illustrates, for the maths to “square up,” we would have to imagine the following:

As readers will have realized, there is an obvious flaw in the chart above: if the FAAMG do continue compounding at 26% over the coming decade, then as they begin to make up an ever greater share of the S&P 500, the S&P 500 as a whole would begin to compound at a faster rate. And this begs the question whether the S&P 500 can compound at a rate much higher 6%.

The first pillar on which the Big Tech bull market rests is that inflation and economic growth around the world will remain modest for as far as the eye can see. And in a world with low inflation, low growth and low interest rates, investors might as well pay up for aggressive growth stocks. In a low return world, the 15% annual profit growth delivered by Big Tech stands out so blatantly it warrants a 26% share price appreciation.

This brings me back to the challenge of big numbers and the iron law of compounding (Albert Einstein reputedly said that there is no more powerful force in the universe than compounding). This iron law faces an obvious logical challenge.

Trying to square this particular circle, investors can come to only one of two possible logical conclusions. The first is that FAAMG stocks will not be able to keep compounding at 26% a year. At some point in the future, we will look back at Microsoft on 11.5 times sales, Tesla on 10.5 times sales, and Facebook on 9.5 times sales and remember the words of Scott McNealy, the CEO of Sun Microsystems, who said of the early-2000 valuation of his company:

“At 10 times revenues, to give you a 10-year payback, I have to pay you 100% of revenues for 10 straight years in dividends… That assumes I have zero cost of goods sold, which is very hard for a computer company. That assumes zero expenses, which is really hard with 39,000 employees. That assumes I pay no taxes, which is very hard. And that assumes you pay no taxes on your dividends, which is kind of illegal. And that assumes with zero R&D for the next 10 years, I can maintain the current revenue run rate… Do you realize how ridiculous those basic assumptions are? You don’t need any transparency. You don’t need any footnotes. What were you thinking?

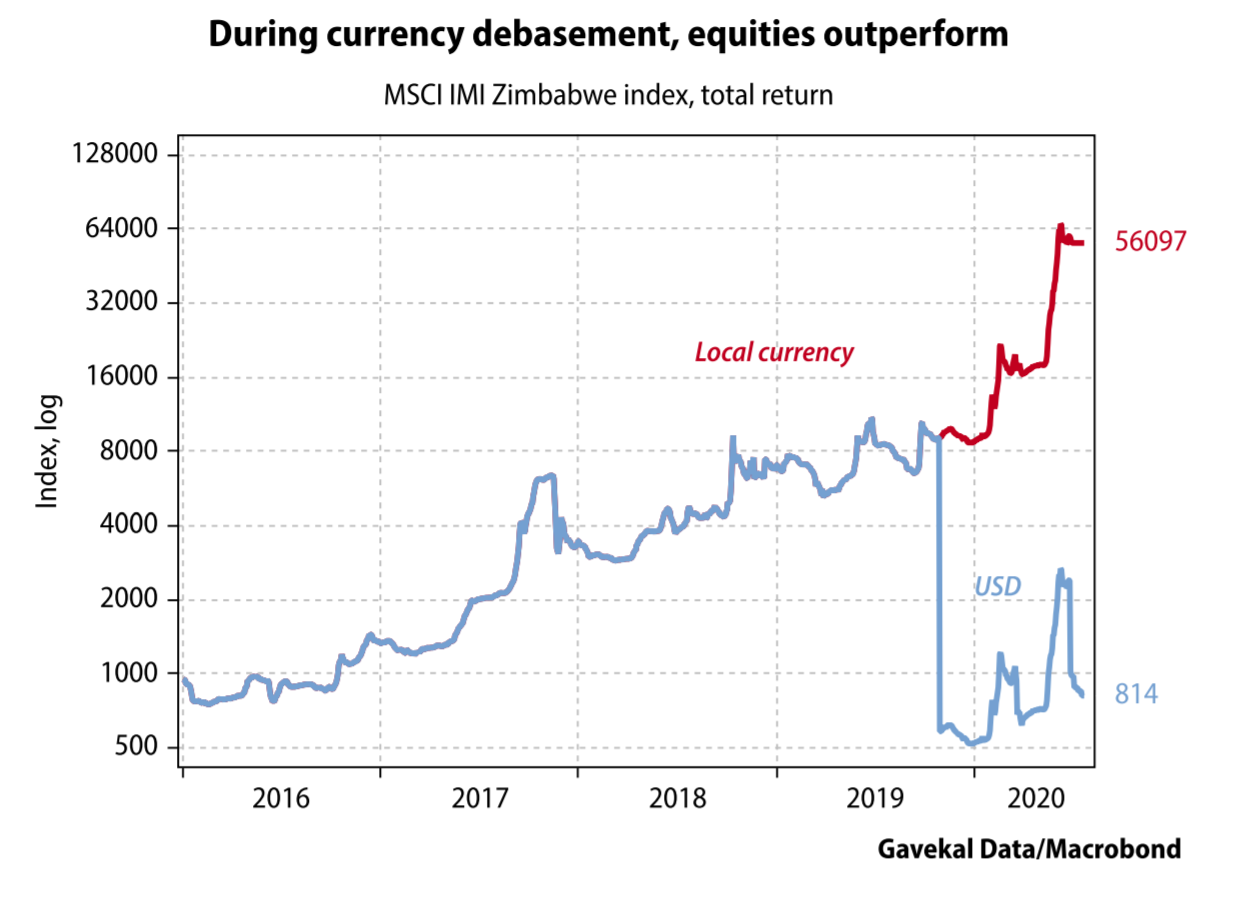

The second possible conclusion to square the circle of FAAMG stocks compounding at such a high rate that the broader market also compounds at an ever higher rate, against a backdrop of weak US and global GDP growth, is that the currency in which all of this is denominated becomes ever more worthless. And in an environment of rapid currency debasement, equities usually outperform bonds and cash, even in the absence of credible GDP growth. One particular example springs to mind.

This brings me to the second bull market that is unfolding: the one we might call “the rise of the green machine”.

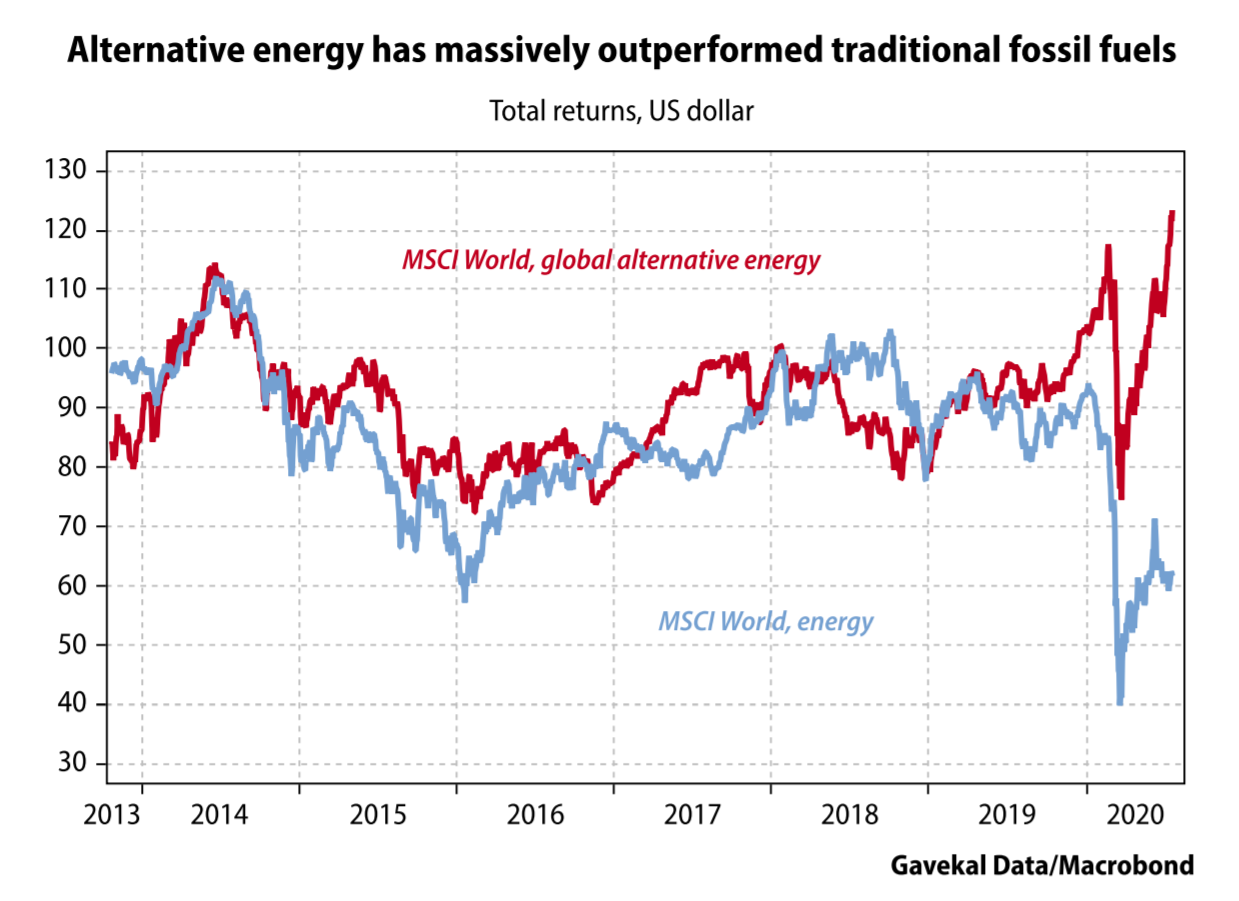

The rise of the green machine

In the chart below, the red line tracks the performance of alternative energy stocks around the world. The blue line tracks the performance of more traditional energy providers—mostly oil producers, some natural gas, and a tiny little bit of coal. For most of the past six years, these two energy provider segments delivered roughly the same performance.

This makes sense given that, by and large, alternative energy companies and traditional energy companies sell—at bottom—the same product: energy. The one key difference is the way this energy is produced.

Suddenly, however, the difference in the method of production has become important enough to justify a massive divergence in performance between the share prices of the two groups of energy producers.

This divergence leaves investors facing a question: why should the value of alternative energy producers be climbing to new highs, even as traditional energy producers continue to be the biggest three-legged donkey in the paddock? There are three possible explanations.

Richard Cantillon, an Irishman who spent much of his life in France, only wrote one book: Essai Sur La Nature Du Commerce En Général. It was only published after his death in the early 18th century and today is seldom studied in economics classes, even though it was a ground-breaking text in the history of political economy, and one which had a huge influence on the likes of Knut Wicksell, the economists of the Austrian school, and the great Irving Fisher.

Cantillon’s starting point was, originally for the times, the value of money. While everyone uses money to measure all the other values in the system, few economists before Cantillon had spent any time trying to understand why money has value in the first place, or just as importantly, why that value changes over time. The reason Cantillon was drawn to the subject may have been because he lived in such extraordinary times.

One of Cantillon’s contemporaries was John Law, who through his Mississippi Company ignited an epic boom and devastating bust in France, which until then had been by far the wealthiest country in Europe. It is fair to say that despite the long list of Englishmen who through history have inflicted such damage on France—Edward the Black Prince, Horatio Nelson, the Duke of Wellington, Brian Moore—none have caused as much damage as the Scotsman Law. However, at least one positive thing came out of the bust: Cantillon’s insights. And these were derived from practical experience; Cantillon was a phenomenally successful speculator, who made out like a bandit in both the South Sea and Mississippi bubbles, first on the way up, then on the way down.

Cantillon’s key insight was that when “new’” money is created, those who are closest to the source of its creation are the first to see the prices of whatever they are selling rise. By contrast, those furthest from the source of the money will be the last to see the prices of their particular wares increase. To cut a long story short, if we define inflation as an increase in the money supply, then its main impact is a change in relative prices—and not, as most people believe, a change in absolute prices.

Those who are close to the central bank get rich; those who are not get poor. As a result, investment piles into the “favored” sectors, while the rest of the economy is starved of money. Eventually, these changes lead to a misallocation of capital with the appearance of multiple false “natural rates,” while there is only one market rate. It is in this mechanism that we find the origin of the market crashes which, as night follows day, always come after major misallocations of capital.

As an example, Cantillon cited the 16th and 17th centuries’ massive increase in Latin America’s production of silver, most of which was “captured” by the King of Spain. As a result, the prices of the goods bought by the Spanish court skyrocketed immediately, while food prices took a long time to follow. And when the production of silver eventually collapsed, all the “court-linked sectors” went bankrupt.

Fast forward to today, and is it possible to imagine a sector closer to power than alternative energy? Which of today’s professional politicians does not want to be seen to be writing checks for the clean energies of the future, produced right here at home? And at the same time, is it possible to think of an industry further from the center of power today than big oil?

When former vice president Joe Biden announces a plan to spend US$2trn once he’s elected on a “green new deal,” is the motivation behind his largesse the promise of future financial returns? Or is it the desire to signal virtue? (With other people’s money, naturally; the US is already running multitrillion US dollar budget deficits, with a debt-to-GDP ratio now higher than at its World War II peak. But who’s counting?)

I would argue the latter. This implies that the performance of the alternative energy bull market is an especially strong signal of a Cantillon effect unfolding right in front of our eyes. And on the other side of a Cantillon-effect bull market always lies currency depreciation.

This brings me to the third of today’s bull markets: precious metals.

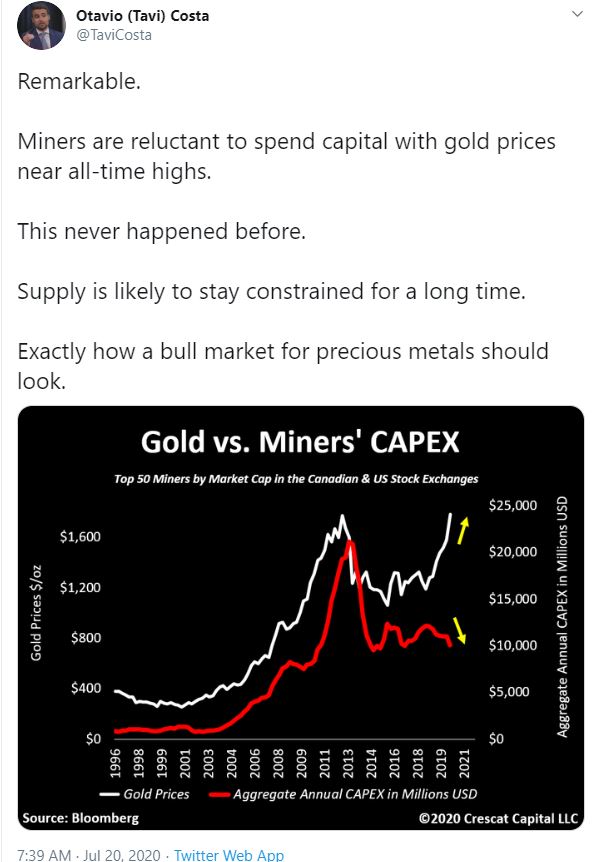

The bull market in precious metals

Year-to-date, gold and silver miners have outperformed all other major asset classes. This outperformance has come against a backdrop of steadily rising gold prices, and sharp rallies in silver prices. Gold has now made new all-time record highs in every currency except the US dollar. And when it comes to the US dollar, if you look at quarterly averages for the price of gold, then the average price in 2Q20 of US$1,780/oz was a shade above the average price of US$1,772 at the peak of the previous bull market in 3Q12.

If anything would confirm that the current bull market is driven primarily by currency debasement, it would be the outperformance of gold and silver against all other assets. As it turns out, the metals themselves are not outperforming tech. But gold and silver miners are. The question is whether this outperformance carries an important message about today’s world.

Historically, once gold bull markets get going, they tend to be long, drawn-out affairs, interrupted only by sharp tightening from the US Federal Reserve, as in 1981, or by a sustained rise in the US dollar, as in 2012. Today, neither appears to be on the cards. So, what will stop the bull market in gold?

One answer might have been a major bust in the emerging markets. Most of the physical demand for gold today comes from India, China, South East Asia and the Middle East. The Indian sub-continent weighs especially heavily in the supply and demand equation. When things go well in India, the marginal rupee tends to find its way into gold. And when things go badly, it has generally flowed out of gold. This pattern makes the current bull market all the more remarkable: gold prices have been rising even though the Indian economy has ground to a standstill.

However, even as India has hit the skids, the world’s second gold market, China, has been thriving. Or at least its stock market has been ripping higher.

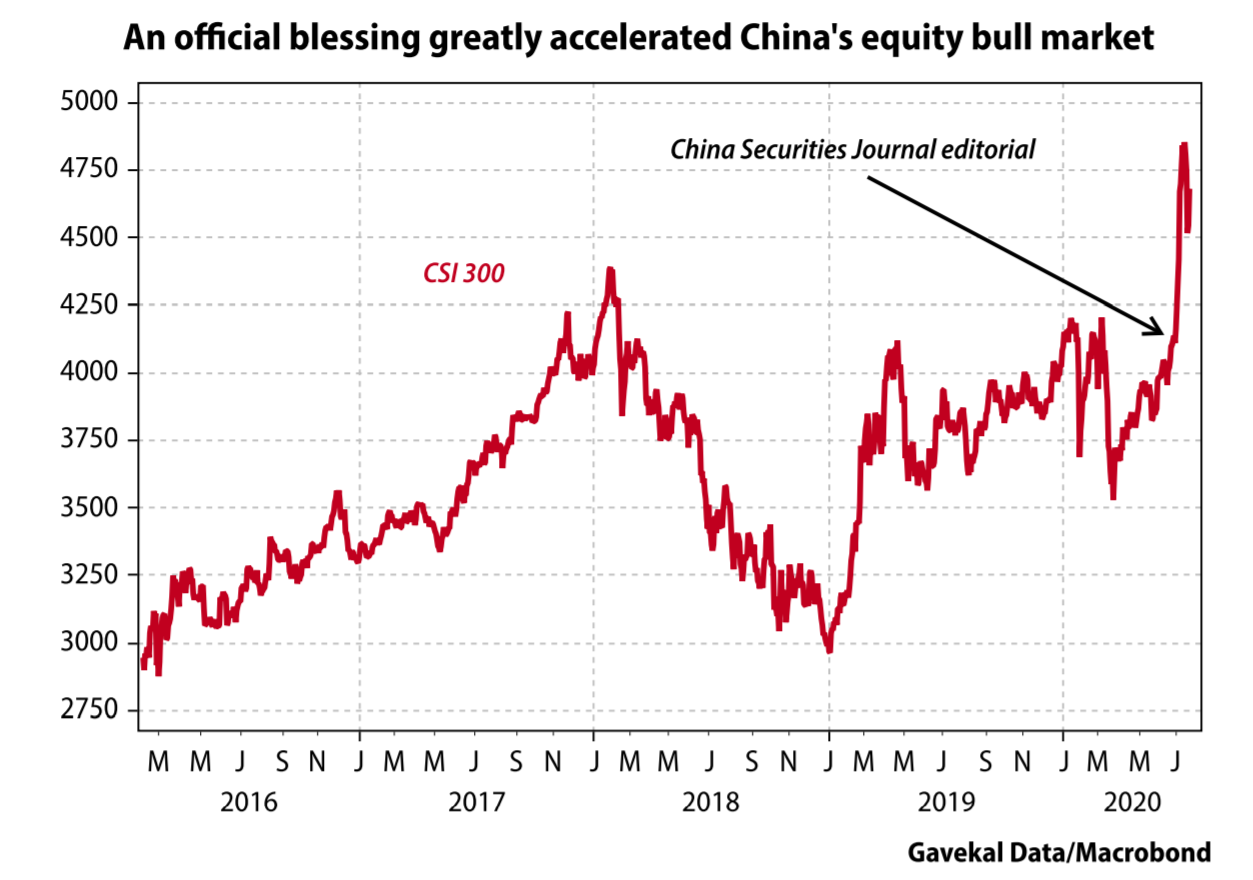

The China bull market

With Covid-19 originating in China, the US-China relationship deteriorating further, China imposing a highly unpopular security law on Hong Kong, global trade collapsing, the UK banning Huawei, China and India coming to blows in the Himalayas, and the Chinese government doing far less fiscal and monetary stimulus than any other major government, who would have thought that the CSI 300 would be outperforming all other major markets year-to-date, except for the Nasdaq? Yet, that is exactly what is happening. And just as success has many fathers, there are probably several germinal forces behind the rising Chinese equity market.

The most obvious hand is that of the government. The market had been grinding slowly higher, like other markets, until an editorial on the front page of the China Securities Journal highlighted that a bull market would be most welcome at the current juncture. The army of Chinese retail investors did not need to be told twice, and the domestic Chinese equity market promptly gapped higher.

But why, following the 2015 debacle, would the Chinese government decide to take another swig from this particular chalice? Possible explanations include:

This last explanation brings me back to the thesis developed in the book that Charles and I wrote a little over a year ago: that China is now actively attempting to dedollarize pan-emerging-markets trade. This matters enormously, because should China succeed, emerging markets across Asia, Africa, Central Asia and Eastern Europe will find themselves needing far fewer US dollars. A world in which the US dollar’s share of global trade starts to shrink rapidly— still highly hypothetical—is a world which would rapidly find itself with far too many US dollars floating abroad.

A world with an overflow of US dollars would be a very different world from the one we inhabit. It would be a world in which:

Now, come to think of it, isn’t this precisely what we are seeing today?

link to the article – https://blog.evergreengavekal.com/the-consequences-of-worthless-cash/

Diana Choyleva of enodo economics is a long term china watcher and she has just written a report on

It will be harder for china to increase its share of global manufacturing and exports because of

-Rise in Productivity adjusted labor costs

-change of rules of engagement between US and China.

-Coronavirus causing countries to rethink their reliance on China.

A move towards localization away from globalization based on national security risks. This will lead to lower efficiency and higher costs.

From the Global Financial Crisis to 2016 the value added by China was one quarter now it is over one sixth.

The “Made in China 2025” plan it set out had a goal of increasing the domestic content of core components and materials from 40% in 2020 to 70% in 2025.

However, even as China’s was climbing up the value chain, the size of china’s economy was already proving to be a headwind. Even though china’s average standard of living was only one fifth of America’s Purchasing power parity.

Little countries can go on capturing shares in world markets until their income per head catches up. Big countries cannot, unless they make those markets commensurately bigger. China’s development has not made markets commensurately larger. Global consumption grew by just 2.7% a year in real terms in 2001-2018, down from 3.2% in 1971-2000. Instead, China’s economic policies contributed to a global savings glut that precipitated the GFC in2008 and shares the blame for the weak global recovery since then.

China’s pool of cheap labor allowed it to catch up regarding low value-added assembly of industrial processes. Within a decade it had saturated global output and capacity in low value-added industries.Since 2008, China’s share of global manufacturing value has risen at a slower pace, but china cannot make up for most of the world manufactures.With rise of 5G, the clash of Chinese and American ideologies is nowhere more fundamental than technology.

The Yuan-dollar peg has been a disaster for the global economy. For past 25 years yuan has been pegged or managed against the dollar, while being massively different in economic and political structure.

The peg was the foundation of imbalances that led to GFC, its rectification has led to this current decoupling.The peg allowed china to industrialize fast while protecting it from vagaries of international capital flows. China failed to understand the pegs usefulness was over as China became big. Initially Americas debt financed consumption of Chinese surplus products helped the peg chug along. But after the GFC, the adjustment of America consuming less and china consuming more and producing less did not happen.For both countries the fastest and most beneficial route to achieve this rebalancing would have been a big nominal exchange rate adjustment and the freeing-up of capital flows in and out of China. This did not happen though.The rebalancing did happen via increase of China’s relative labor cost eroding its competitive advantage with respect to USA. Wages in China rose four-fold with respect to to wages in USA which rose by only 34%. The effective revaluation of bilateral relative unit labor costs and the tariffs Trump has imposed on Chinese goods are now almost sufficient for US manufacturing to rise as a share of GDP, either through substituting imports for domestic products or gaining export share or both.

Wage and lower productivity growth have lifted china’s labor costs. While demographics have also reduced pool of cheap labor. The demographic trends cannot be reversed by China for the coming decades and China is not receptive to immigration. So, the demographic trend is going to exacerbate further.

Easy productivity gains from shifting workers from agriculture to low value but high productivity manufacturing has been exhausted.Although efforts have been made towards creating a skilled workforce it has not fructified and workers remain unequipped for automation and knowledge intensive manufacturing.The other major issue is that college graduates prefer to work for SOE’s than private sector enterprises where bulk of the jobs are.

Post 2011, China export led growth model had reached its end date. China however poured more money into investment with an increase of debt to GDP and structural growth decline.China’s development was premised on a closed capital account to accumulate large domestic savings and use them to subsidize its industrial rise with underpriced credit. This led to Chinas consumer spending as a % of GDP to fall to 34.4% in 2007.As migrant labor force declined, the share of wages in GDP increased. As medical care and social security provision improved, households savings rate started to decline. Chinese today have two thirds of their wealth in low interest-bearing deposits leading to booms in investment cycle at the cost of reduced returns on household wealth.Wealth management products and other shadow banking products provided few more percentage points than their savings accounts, which led to urban consumers to save less. Rural economy initiatives and E ecommerce was used to unlock pent up spending and lower household savings rate.Household Credit share of GDP rose in 2011 from low levels to dangerously high levels in 2016, after which Beijing started reining in shadow banking sector to reduce systemic financial risk. The once booming P2P lending industry crashed inflicting huge losses leading to a lot of protests.

In a potentially important reform unveiled in August 2019, the central bank replaced its benchmark lending rates with a market-based alternative. The PBOC has phased out its benchmark lending rate, but not its cornerstone deposit rate. Policymakers worry that competition among banks would raise deposit rates and damage government efforts to lower borrowing costs in order to help cushion the economic slowdown.

Property is one of the principal assets that Chinese hold and Xi’s attempt to arrest house price inflation while making sure house prices don’t crash meant household owners had to scale down future wealth expectations. His policies have a cumulative effect of sapping urban household wealth. tax and other measures to stimulate consumption are targeting rural Chinese and those on lower incomes, not urban high earners. But with towns and cities accounting for 80% of consumer spending, rural households, struggling to upgrade their skills, will find it hard to carry the economy on their shoulders.

Thus, the author sees three paths forward for Chinese policymakers –

Full liberalisation of financial markets and interest rates would allow transition of cheap capital access to private firms as opposed to overcapacity creating SOE’s.

Continuation of investment led growth would mean ever more larger debt problems. losses as estimated by ENODO estimated for banks were around 19% of GDP. Chinese government leverage is at 50% of GDP which means these and further losses can be cushioned and will reach 75% of GDP. According to ENODO China has five years to wean itself off of its reliance on debt to power its development.

Since GFC China’s Current Account deteriorated while its capital account improved due to capital intervention. Similarly, the government can carry out a sharp devaluation in a short time. China has $3.1 Trillion stockpile of Foreign Exchange reserves and can withstand one or two years of Capital Outflow, while maintaining exchange rate. If China’s current account swings into the red, Beijing’s ability to keep its command-and-control show on the road will get that much harder

For foreign companies, the business climate is turning increasingly chilly as a result of Xi’s determination to strengthen the grip of the Communist Party in every sphere of Chinese life. The Party has been formally represented within foreign companies for years. A survey conducted by the Central

Organisation Department in 2016 found that 70% of them had a Party cell or a Party-controlled union. Under Xi, however, these bodies are becoming increasingly assertive. China is preparing a corporate version of the “social credit” system it is already using to punish people for anti-social behaviour. According to the EU chamber, companies are being rated by different agencies for their compliance with regulations; those found to have violated rules are blacklisted. Beijing plans to combine those ratings into a single database that could be up and running in 2020.

“The overall outlook has shifted from cautious optimism to cautious pessimism.” US firms, regularly criticised by Trump for manufacturing in China instead of back home, will be conscious of the need to stay on the right side of public opinion when they make their investment decisions.

Over the Years China has focussed on cutting electricity and logistics costs for its producers, however its current use of water resources is clearly unsustainable.

There was overcapacity in power generation and as the market liberalised prices fell along with government stepping in many times to slash prices. The National Development and Reform Commission, China’s state planning body, cut administered electricity prices by 10% in 2018, another 10% in 2019 and has pledged a further cut in 2020. Beijing’s focus has also been to wean itself off of coal and shifting to costly but less polluting sources of energy. Reducing overcapacity also means that 1.3 Million workers will have to find jobs as a result.

As a share of GDP logistics costs have already declined sharply in the past few years. The price of express parcels, the main delivery method for e-commerce firms, has fallen steadily. In May 2018 it halved the vehicle purchase tax for trailers carrying goods for a period of three years. It also halved the land-holding tax on bulk commodity storage facilities leased by logistics companies.

Overall water resources in China are not significantly more constrained than in the UK. But the problem is that 80% of the water is in the south, but 85% of China’s coal reserves are in water-scarce provinces in the north and 64% of arable land is also in the north. Agriculture accounts for 62% of China’s water consumption, power and industry for 22% and households for 14%. Twelve northern provinces suffer from water scarcity, eight of them acute, and they represent 38% of China’s agriculture, 50% of its power generation, 46% of its industry and 41% of its population. China has 20% of the world’s population but only 7% of its water. The water crisis puts the ambitions of Xi’s “Made in China 2025” strategy in an important light. A failure to set far higher water prices now, while understandable in terms of social stability, will exacerbate the water scarcity problem in the longer term.

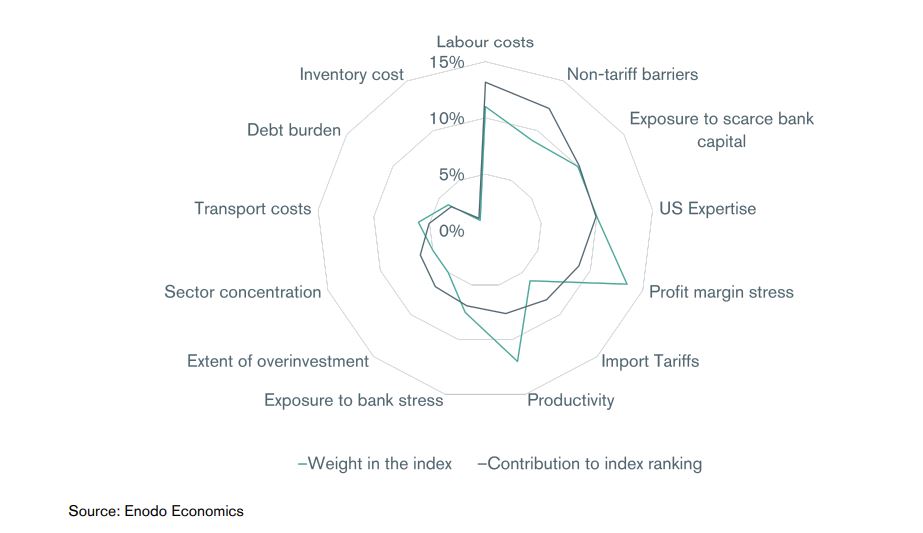

ENODO Reshoring Index

China’s industrial sectors ranked by likelihood of a shift in production back to the US with 0 being most vulnerable to reshoring.

According to the Enodo Reshoring Index, the sectors most likely to move back to the US are automobiles, electrical machinery and equipment, wood processing and chemicals, rubber and plastics, along with the rail, ship and aircraft sector and pharmaceuticals

Enodo Reshoring Index category weights and the contribution of each category to the index ranking for

the top ten sectors most likely to reshore.

Link to the Full Report –

In an interview with Edward Griffith in 1984, former KGB operative Yuri Bezmenov outlined the playbook of the Soviet Union and the staged manner in which a communist apparatus takes over a country.

The ideal recruit for the KGB were rich filmmakers, academicians and cynically egocentric people. These people held the most potential what is required to destabilize a country are narcissistic, greedy and morally devoid people. He cites that KGB recruited Professors and civil right defenders to subvert and destabilize the country. He repeats again when these useful idiots serve their purpose they are to be killed or exiled. His disaffection with the KGB began after he understood what was to happen to the Pro Soviet Indian Journalists, but when he tried to get the message across, they did not believe him.

The ultimate objective of KGB was Ideological subversion which was supposed to be carried out by changing perception of reality, and not be bothered by what is true or false. But rather be driven by self-interest.

He lists down four phases as to how it happens –

Phase 1 – Demoralization

This is a process which can take about 15-30 years to perform . During this stage, the moral fibre and integrity of the country is put into question, thereby creating doubt in the minds of the people. To do so, manipulation of the media and academia is required to influence young people. As the younger generation embraces new values, such as Marxism and Leninism in newer and trendy Garbs , the older generation slowly loses control simply through attrition.

Phase 2– Destabilization

The intent is to create a massive government permeating society and becoming intrusive in the lives of its citizens. This can take from two to five years to perform, again with the active support of academia pushing youth in this direction. Here, entitlements and benefits are promised to the populace to encourage their support. Basically, they are bribing the people to accept their programs.

Phase 3 – Crisis

This is a major step lasting up to six weeks and involves a revolutionary change of power. This is where an alarming event upsets and divides the country thereby creating panic among the citizens.

Phase 4 – Normalization

The final stage is where the populace finally acquiesces and begins to assimilate communism. This can take up to two decades to complete.

The List of Rules he cites for Revolution are –

1. Corrupt the young, get them interested in sex, take them away from religion. Make them superficial and snobbish in their understanding of the world.

2. Divide the people into hostile groups by constantly harping on controversial issues of less importance to create and compound a divide.

3. Destroy people’s faith in their national leaders by holding the latter up for contempt and ridicule.

4. Always preach democracy, but seize power as fast and as ruthlessly as possible.

5. Encourage government extravagances, destroy its credit system, which will produce years of inflation with rising prices and general discontent.

6. Incite unnecessary strikes in vital industries, encourage civil disorders and foster a lenient and soft attitude on the part of the government towards such disorders.

7. Breakdown the old moral virtues of honesty, sobriety, self-restraint, faith.

The Main point he makes it all starts by the act of trying to legislate equality rather than understanding the fundamental that not all are born equal. Once this process starts there has to be a third party who has to legislate this equality and that usually is the government. Once you create an atmosphere of information where people who are deemed unequal have to be made equal by law is where you lay the foundation of discontent. These negative feedback loops are taken advantage of by politicians and this ultimately leads to critical mass of discontent. Once a society is this fragile it takes one catalyst to spark the flame which starts engulfing the system.

Link to the Interview – https://www.youtube.com/watch?v=KLdDmeyMJls

Well this video was shot in 1984 but you can correlate to whats happening in western society today. The prophetic words about the moral decay of the society is so evident in US where riots have broken out on street, the educated majority has gone silent and hooligans getting free handouts have taken over.

This will not end well. Oh no not at all. The free money is the opium of the people and Leninist Marxist ideology will be having the last laugh.

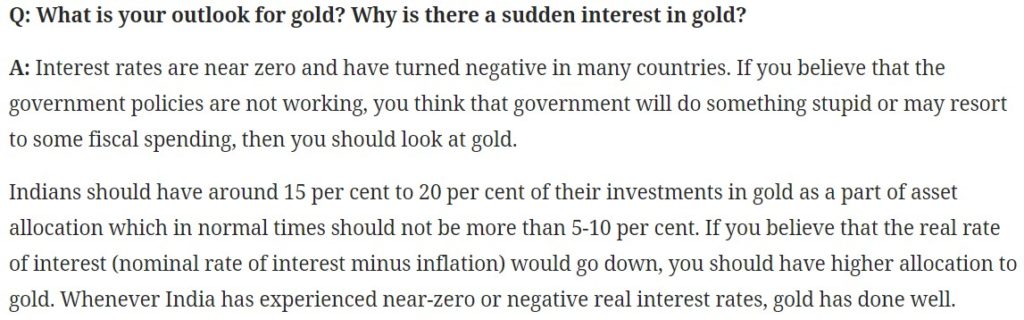

Link – https://www.valueresearchonline.com/stories/32058/the-macros-expert/

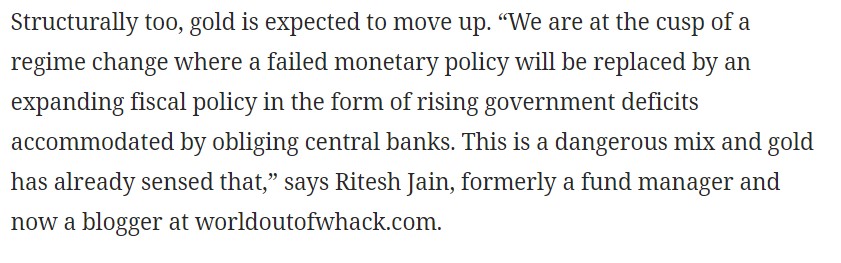

Link – https://blog.ventura1.com/2020/03/in-conversation-with-ritesh-jain/