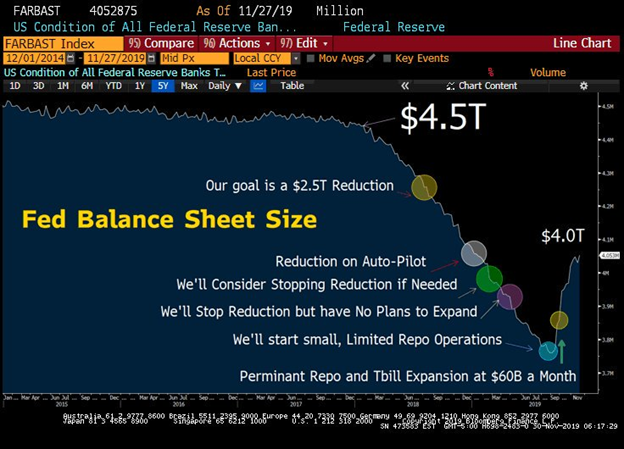

What kept the markets rally going in November? The chart below has all the answers. Fed’s balance sheet at $4.05 trillion, highest level since Jan 9, up $293 billion over the last 3 months.

But as per Jerome Powell “This is not QE.”

I think we will see even faster growth with year-end funding pressure, surpassing in a few months the all-time high of $4.5T in Jan 2015.

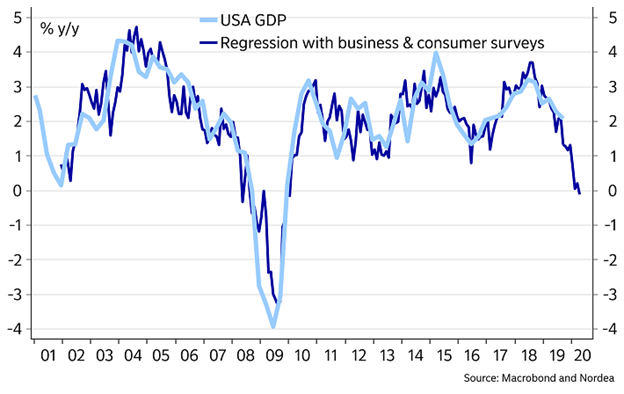

The FOMO (Fear of Missing Out) continues as I had outlined in my previous month outlook. The economic data continues to worsen except for Chinese PMI (in case you believe the Chinese data). US GDP growth for Q4 and Q1 2020 is tracking 0%, yes that is Zero as per Nordea. This is what a trillion-dollar fiscal deficit buys for you now a days. Yikes!

Markets are now completely detached from reality because we are in PE expansionary phase supported by monetary policy.

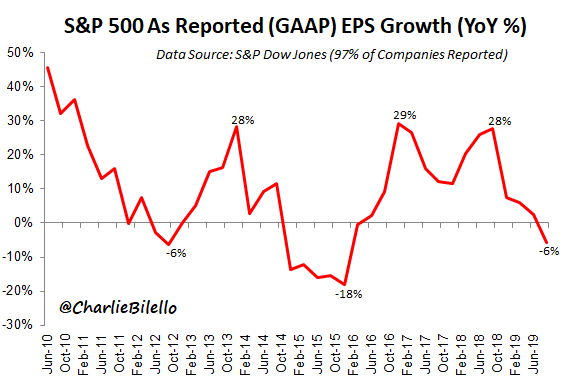

97% of companies reported S&P 500 GAAP earnings were down 6% over the past year – largest decline since Q4 2015 https://twitter.com/charliebilello

One more chart to satisfy you that we are living in a utopian world

How many of you missed the most important news headlines over last few days? No, it is not about trade war or North Korea, but an almost silent generational change in monetary and fiscal policy.

This one freshly baked out of ECB oven.

And now for the new role for Ex BOE governor.

FED wants to allow inflation to run “ HOT” , ECB wants a role in funding “ GREEN BONDS” out of its balance sheet and Mark Carney is there at UN to help shape world policy on funding climate change because we are told it is an “ existential threat”.

The new MMT (Modern Monetary Theory) is taking shape under the guise of preventing “CLIMATE CHANGE”.

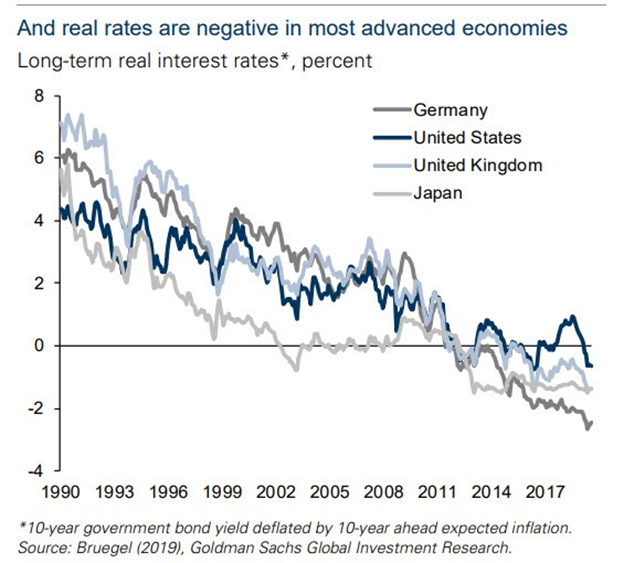

Thankfully for those who are playing this game, they have support in the form of negative real rates across the developed world which will soon be replicated in developing world. This will force more and more savers to consume or seek out risk assets rather than save and pension funds to take on more risk to maintain the desired level of promised returns.

Market outlook

Well I could sense the change in monetary policy but chose to play by going long commodities and volatility over Equity (I sometimes hate that I am ahead of the curve) and since we are all conditioned by environment and career risk in short term, portfolio managers did what they are supposed to do in November to keep their bonus and job intact by buying what matters most “ EQUITIES” in the face of rising inflation and wage pressure. Never mind, the winds are changing, and precious metal and other commodities equities have now started outperforming the Global Equities. This trend change is still in nascent stage and I expect it to pick up steam as we enter into the first quarter of next year.