The following is a synopsis of what the larger professional institutions and their research departments are expecting for 2020; via

GOLDMAN SACHS:

- U.S. recession risk is limited to a 20% chance in 2020

- Federal Reserve to remain on hold, not raising or cutting rates in 2020

- The U.S. will lead in relative strength

- China weakens further

- Limited inflation because of limited wage growth

- Lower, but positive stock market gains in 2020… with a better first half than second half of the year

- Growth above consensus at 2.5%

- Year-end close of 3400 for the S&P-500 in 2020 but only if we get a divided U.S. Government after the 2020 elections, and yet…

- A full 100% of Goldman Sachs’ sophisticated private equity clients expect a recession in 2020

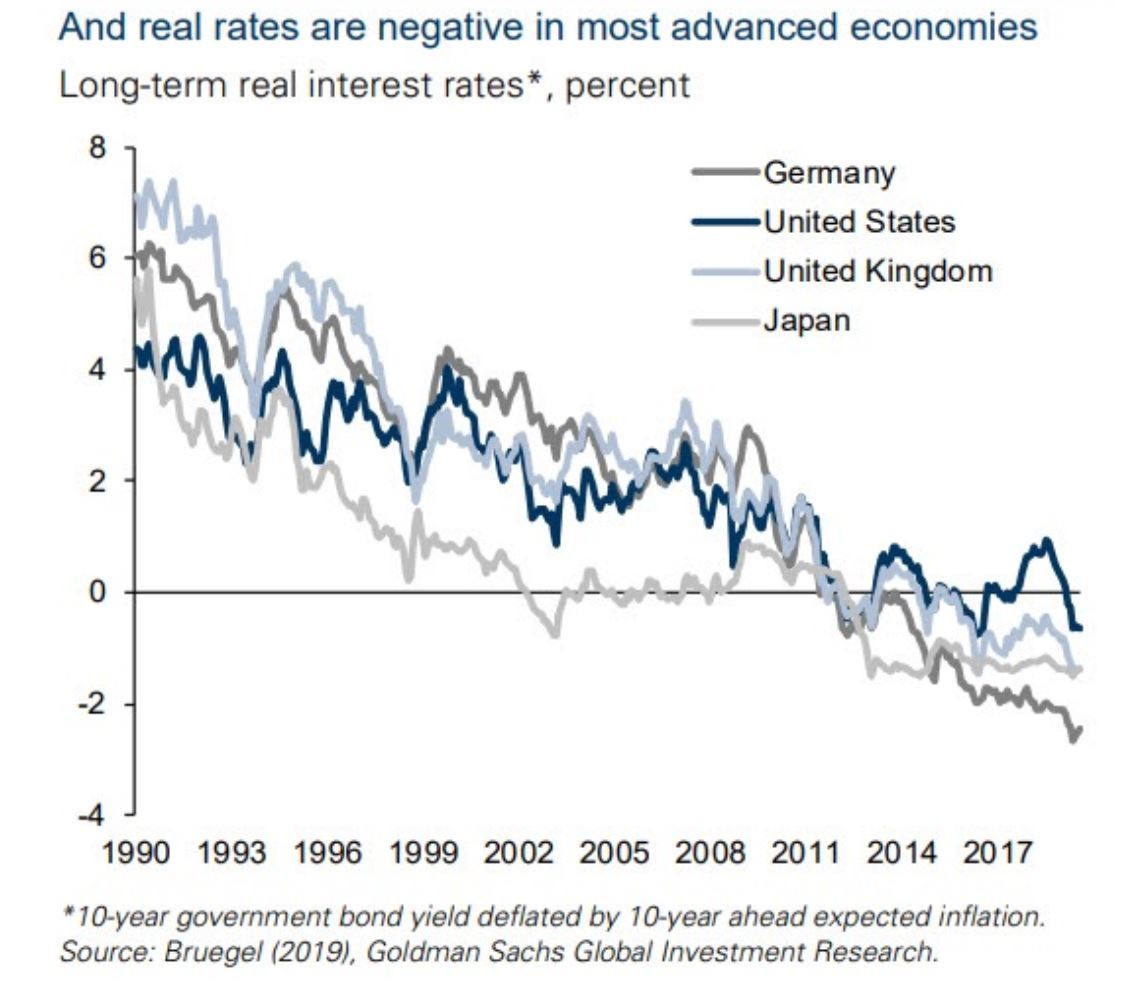

- Central Banks across the globe are holding real (inflation subtracted) rates in negative territory, showing persistent global economic weakness

CHARLES SCHWAB:

- Key risks for 2020 are manufacturing weakness and business investment fatigue hurting consumer spending and job growth… unemployment claims are already starting to build even as employment levels rise

- Federal reserve to remain on hold

- USDollar remains strong but moves mostly sideways

- Inflation may slightly rise, helping TIPS (Treasuries that are inflation protected)

- Buy extended-duration Treasury-bonds over shorter-duration

- Buy investment-grade over high-yield corporate bonds

- United States continues to lead in relative strength

- Market volatility to be higher than usual

- Buy quality, low-volatility large-cap stocks

- Small-cap stocks continue their weakness

EVERCORE (Ed Hyman, voted #1 Economist for the past 39 straight years via Institutional Investor’s Annual Survey):

- The big stock market drop in December of 2018, followed by the Federal Reserve response, prolonged the market cycle

- Lower growth in 2020, unless corporate earnings pick up

- Gold is an important part of any portfolio because of the massive amount of money-printing by all world governments

- No recession in 2020

- Low inflation continues

- Interest rates low for longer

- Way down the road, the government deficit and high corporate debt will eventually create stagflation

FIDELITY:

- The Federal Reserve is unlikely to raise interest rates in 2020, all Central Banks will want their economies to run hotter than normal

- For 2020, hold a mix of investment-grade and high-yield corporate bonds even though there will be a deterioration in high-yields as the late-cycle advances

- Expect increased volatility over the next two years

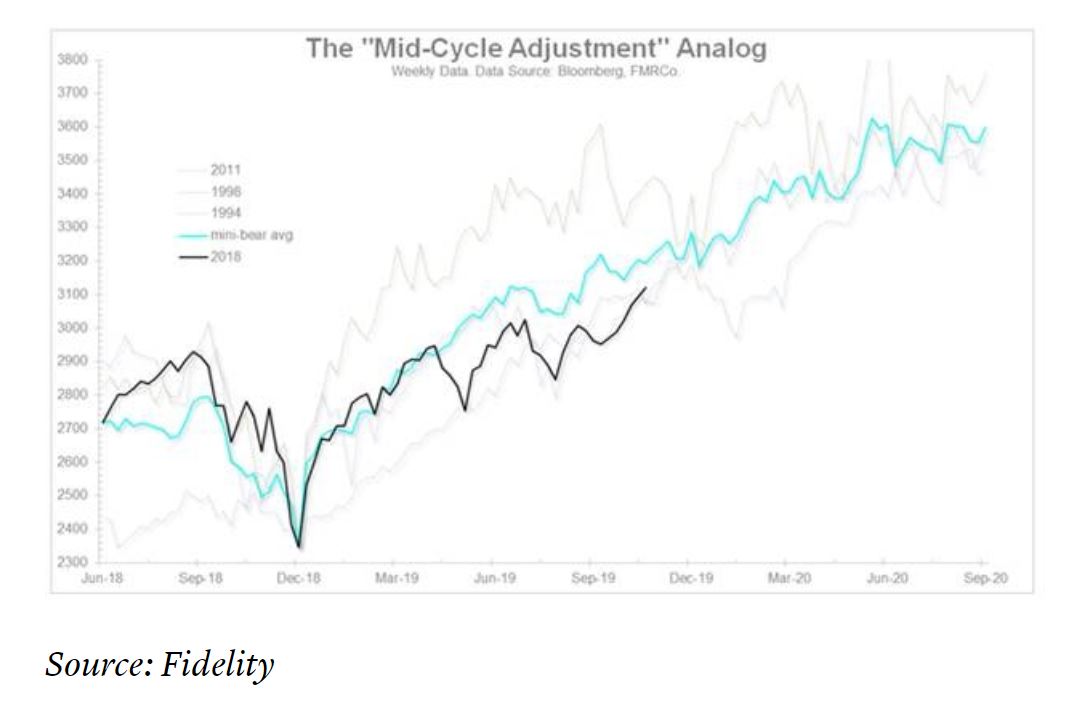

Jurrien Timmer, Head of Global Macro at Fidelity (and one of my favorite analysts), suggests that stocks may continue to run up until the end of summer in 2020 (dark black line below continuing up to the upper-right corner of chart), with a possible recession starting in early 2021:

BANK of AMERICA:

- 8% corporate earnings growth (because it will be easy to move up from the flat earnings growth of 2019) and this leads to an 8% stock market gain for 2020

- Manufacturing weakness may have already bottomed

- The financials sector will be the strongest

- Several under-valued and beaten down sectors will rotate to the top (IE, energy)

- There will be increased volatility and greater draw-downs

- Hedge funds will get killed chasing momentum stocks

- Pension funds are now holding mostly illiquid (un-sellable) investments and if forced to sell during a major downturn, they will be forced to sell their (liquid) S&P-500 stock positions, further driving down the market

BLACKSTONE:

- The stock market is risky and perhaps topping and the Federal Reserve is in a too weak position to offer support

- Weaker earnings growth than ‘The Street’ expects

- Volatility should increase in 2020

- Yields will move slightly higher in response to rising wages and this will cause a slight uptick in inflation

- Mid-cap stocks may offer superior gains over large caps

BLACKROCK:

- Decent growth for the global economy

- Suggest a current mix of cyclicals (especially technology) with defensives (such as healthcare & staples)… and high quality stocks

- Positive on U.S. stocks

- Negative on European stocks

- Positive on Japanese stocks

- Very positive on Emerging Market stocks, except…

- China weakens further

- Positive on gold, especially as a portfolio hedge

- Best bonds = high-yield corporates and TIPS (Treasuries that are inflation protected)

GUGGENHEIM PARTNERS:

- Economic indicators will continue to weaken

- Odds of a recession in the U.S. during 2020 have increased to 50% (which is high)

- Pickup in job layoffs to increase in 2020

- Both Treasuries and gold should perform well in 2020

- There is danger in high-yield corporate bonds because of improper risk ratings

- Possible 40%-50% pullback for stocks if recession occurs… 20% pullback if no concurrent recession

Yes, it keeps going…

NEUBERGER BERMAN:

- Possible recession in 2020, but more likely in 2021 with stocks falling 6-9 months before recession starts (stocks starting to fall in 2020)

- More Fed rate cuts likely during late 2020 and into 2021

- There will be increased and more prolonged market volatility

- Investment-grade corporate bonds to beat high-yield corporate bonds

- Expect a 20% correction sometime in 2020 regardless of recession occurrence

YARDENI RESEARCH:

- Main worry is that the S&P-500 could rapidly “melt up” toward 3500… and then crater into a prolonged recession

- If bull market continues, then expect better earnings growth at 5.2% in 2020 and 4.7% in 2021

- Continued subdued inflation in 2020

- Trade War Phase 1 (fluff) likely completed sooner rather than later in order to calm financial markets

- Trade War Phase 2 (real deal) likely to be postponed to after the elections with China wanting to ‘wait-and-see’ if President Trump wins a second term

FUNDSTRAT:

- Stock market up in 2020 because corporate earnings will grow by 10%

- >10% gain in the S&P-500… to 3450

- There will be mild inflation that increases in the second half of the year

- Best sectors are technology, industrials, financials and energy

- U.S. will lead in relative strength

INVESCO:

- No recession in 2020

- Weak, low growth economy

- Rates on hold

- No full resolution to Trade War

- Growth stocks continue to beat value stocks

- U.S. stocks continue to lead in relative strength

- Strong USDollar

- Favor high-yield over investment-grade corporate bonds

- Favor corporate bonds of all types over Treasuries

- Positive on Real Estate Investment Trusts (REITs)

- Expect low but positive returns for gold

- Bearish on commodities in general

- Volatility rises in second half of 2020

WISDOM TREE (via their senior strategist Jeremy Siegel of Warton School of Finance):

- Interest rates will stay low and float between 2.5% and 1.5%

- Holding U.S. Treasury-bonds will hedge against stock market losses

- Expect an S&P-500 gain of 8% (that includes a 2% dividend)

- Dividend-paying stocks should excel in relative strength

- The two biggest threats to the stock market are a continued Trade War and the possible election of either Bernie Sanders or Elizabeth Warren

- Recession probability is at 40% during the next two years (and this is fairly high)

(David) ROSENBERG RESEARCH and ASSOCIATES:

- A recession is imminent, most likely in 2020, and the problem is that…

- The high government deficit means a potential weak government stimulus and…

- Low interest rates means a potential ‘too weak’ Central Bank stimulus

- The stock market is simply running out of steam

- Residential housing has contracted for 6 quarters

- Commercial building is now contracting

- U.S. exports down for past 6 months

- Business capital spending already in recession

- Employment data is starting to weaken

- Consumer data is weakening

- GDP breadth is weakening with 30% of GDP already in contraction

- Leading Economic Indicators have recently moved into contraction

- Most of globe is ahead of the U.S. in the weakening of economic data

LAZARD:

- Slow growth, but no recession in 2020

- Extremely accommodative monetary policy

- Equities = 5% gain in 2020

- Bonds = 5% gain in 2020

BTIG:

- More clarity on trade and Brexit would be bullish for stocks

- Cyclical stocks beat defensive stocks

- Leadership will be found in financials and energy

- Neutral on technology, however tech still likely moves up

- Bond yields have bottomed, however Fed unlikely to raise rates

FIRST TRUST:

- Bullish with the S&P-500 heading to 3650 in 2020

- No recession within next 12 months

- Interest rates begin to head back up because of increasing inflation

- Greatest risk to the market is a far left Democrat winning the White House

FRANKLIN TEMPLETON:

- Modestly cautious going into 2020

- Risk is still skewed to the downside

- Moderate risk of recession in 2020

- Mild inflation may cause out-performance by Emerging Markets, in both stocks and bonds

JP MORGAN:

- Target of S&P-500 @ 3400

- Choose cyclicals (tech) over defensive (utilities)

- Choose late-stage sectors such as energy and industrials

- Muted inflation despite expected wage growth

LEUTHOLD GROUP:

- No recession in 2020

- Emerging Market stocks will be the big global winner

- In the United States, cyclicals will beat defensives

- Mid-cap stocks to be stronger than large-caps

- Late-stage assets such as industrials and energy may excel

UBS:

- Strong U.S. economy in 2020

- No rate hikes

- Increased volatility creating deeper pullbacks

MERRILL LYNCH:

- Bullish on stocks with a 20% expected gain in 2020

- Mom-&-Pop retail investors to drive market higher

- Bond risk is increasing, so keep portfolio total bond level @ 20%

- U.S. stocks continue to lead in relative strength

- Best stocks will be found in the high-quality-large-cap area

RUSSELL INVESTMENTS:

- Central Bank easing coupled with the cooling China-U.S. trade war have set the scene for a modest global economic rebound in 2020

- Recession in 2021

- Low inflation… no Fed rate changes

- Sluggish growth in Australia… they will likely implement income tax cuts

- Modest growth in the Euro-zone, including U.K.

- Minimal growth in China and Emerging Markets

- Bullish on U.S. stocks, but they are already expensive

- Both high-yield and investment-grade corporate bonds are expensive

- Treasury bonds offer the most attractive relative value

DOUBLELINE:

- The Federal Reserve is already secretly doing QE-4, as if we are already in a recession

- Debt is higher and yet GDP is worse

- Manufacturing is now worsening

- If no recession in 2020, then President Trump wins another 4 years

LPL RESEARCH:

- Economic data, such as earnings, will exceed the current lowered expectations (low hurdle)

- Possible recession in late 2020

- Solid U.S. equity performance benefiting cyclical sectors (such as tech) and large-cap stocks in general

- Weakness in Europe, Japan and China

- Stick with high-quality bonds

- Low inflation continues

- Strong USDollar

QUOTE OF THE MONTH… Larry Kudlow, head of Trump’s National Economic Council (via Forbes Business Magazine): “Tax cuts impose restraints on the size of government. Tax cuts will starve the beast. Specifically, tax cuts provide a policy incentive to starve Social Security, Medicare, education and the environment.”

There is a strong incentive for the bigger institutions to give high “end of year” targets… they want people to enthusiastically give them more money to manage. So, shown above is the 2020 year end S&P-500 forecast (courtesy of MarketWatch). Regarding the 14 analysts shown, I normally pay the most attention to market commentary coming from Brian Belski, Savita Subramanian and Francois Trahan. The truth is that not a single person on this list knows where the stock market will end in 2020. Someone’s prediction might get lucky, merely by chance.

MarketCycle’s PREDICTIONS: We are in the late-stage of the bull market that started in early 2009.

- STOCKS: There is the possibility of a bullish melt-up that could even persist into Fall. We could see the S&P-500 @ 3330 by late spring. This boiling pot has to be watched.

- RECESSION: There is almost no possibility of a U.S. recession in the next six months. If there is no U.S. recession or late-in-year bear market drop in 2020, then President Trump likely wins a second 4 year term.

- RISK: With each passing day, there is an increasing chance of a temporary yet strong & scary stock market pullback of perhaps close to 20%.

- BONDS: The Fed is unlikely to raise interest rates in the near or intermediate term and this may benefit interest and dividend paying assets.

- USDollar: Likely to remain strong with price drifting sideways.

- INFLATION: Non-stop money-printing and government spending coupled with low unemployment could translate to inflation slightly rising from extremely low current levels. In 15 years, inflation could be quite high.

- GOLD & COMMODITIES: Typical late-stage assets; likely to benefit from any increase in inflation. Gold is a good portfolio hedge when used in the late-stage of the market cycle.

- TRADE WAR: As I predicted months ago, the end of Phase-1 Trade War didn’t move the needle much, at least not in the right direction. The major import by China has always been farm products and they just moved backwards from the #2 importer to the #5 importer of food from the United States. The key feature of the Phase-1 agreement is that China will buy food imports from the United States. The problem is that they just agreed to buy much less than they were already buying. Farmers are really getting hurt. President Trump now seems to be on the attack against Europe, especially after the recent NATO trip where world leaders directly insulted him. He just added 100% tariffs on many European items and this is during a period when much of Europe is already in recession.

- RELATIVE STRENGTH: The U.S. continues to lead in strength relative to other countries, although Emerging Markets may get a boost as 2020 progresses.

- Stock “buybacks” are starting to rapidly decrease and the Mom-&-Pop retail investor is stepping up to the plate. Normally, Mom-&-Pop arriving on the scene is a late-stage phenomenon that occurs in conjunction with the final bullish melt-up of stocks in an advancing market cycle.

- What would make me think that the market cycle may be prolonged this time around? A strong and beneficial stock market correction coupled with a concurrent & rapid positive change in our risk indicators. Our risk indicators showed minimal risk from April 2, 2009 until just before the big 20% stock market drop in December of 2018… almost 10 years. Now, instead of clearing out after that big correction as they normally would have, they have only shown even higher risk levels, so we are positioned to benefit from any market direction. If the market goes up, MarketCycle’s clients should reap about 75% of the gain but if the market drops substantially, we are likely to also make profits. This is a good position in which to be.

- LONG TERM: After we reap our eventual and overdue recession, we then continue our journey into the ROARING 20’s decade which will merely be the second half of the current Secular Stock Bull Market that technically began in October of 2011. As I’ve stated several times, I bought the domain name of DOW80000 with the year 2029 in mind. And I am amazed by the magnitude of forces that are due to come to a head or to completion in 2029. Hummm… could 2029 mimic 1929? Could the years after 2029 mimic the difficult years that followed 1929?? Will the cycle repeat all over again?

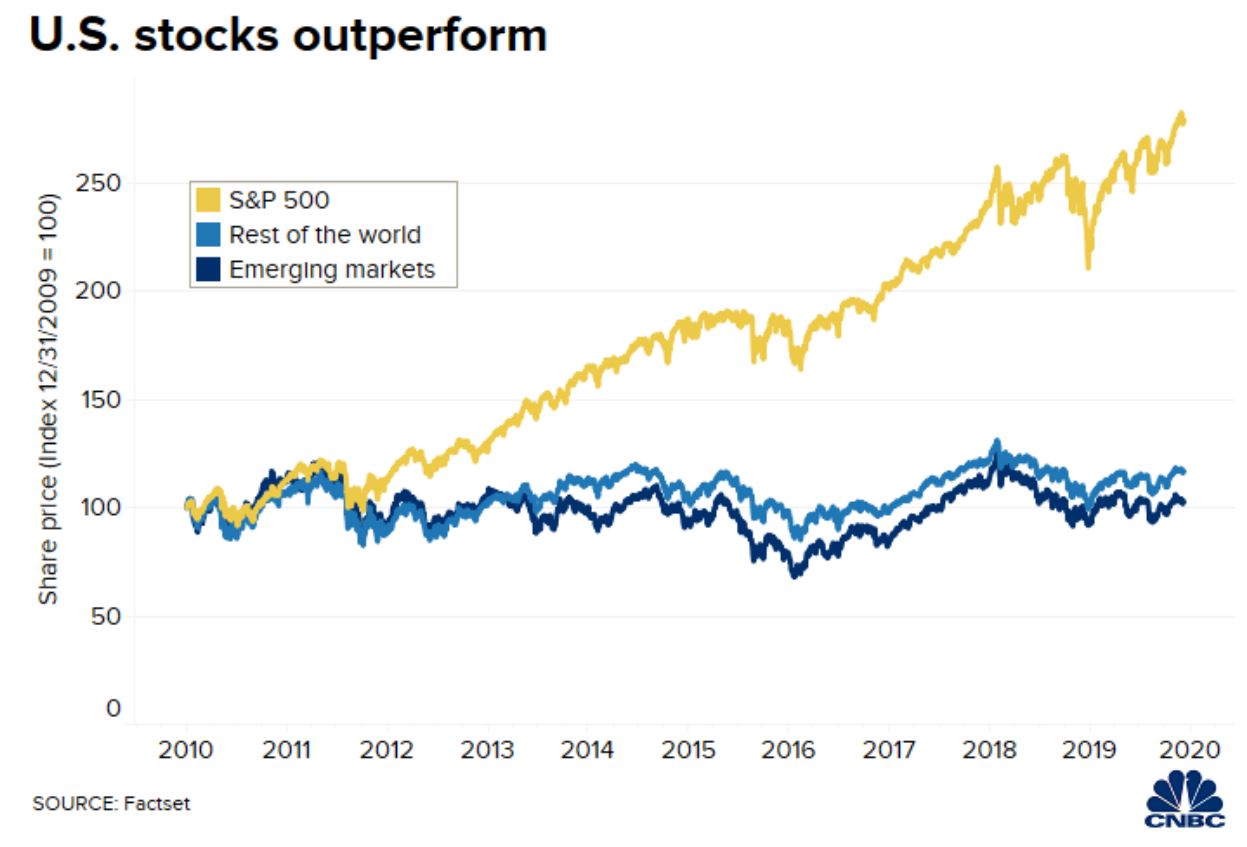

Although we recently took a small position in global stocks, MarketCycle has been correctly holding almost entirely U.S. stocks since the start of this bull market in 2009. From the below chart, you can see (via the gold line) how important this type of decision is and why ‘relative strength analysis’ is so critical to investing. Always hold strength and avoid weakness. (Chart courtesy of Factset & CNBC)

******************************