George Vanderheiden is one of the best investors I’ve ever known. He chose to retire in early 2000, massively underweight technology and massively overweight home builders, tobacco and other value oriented stocks. He had written “Tulip bulbs for sale” on the whiteboard outside his office and left a package of them underneath in late 1999.

2020, especially the end of it, has me thinking of George and what I have learned from listening to him over the years.

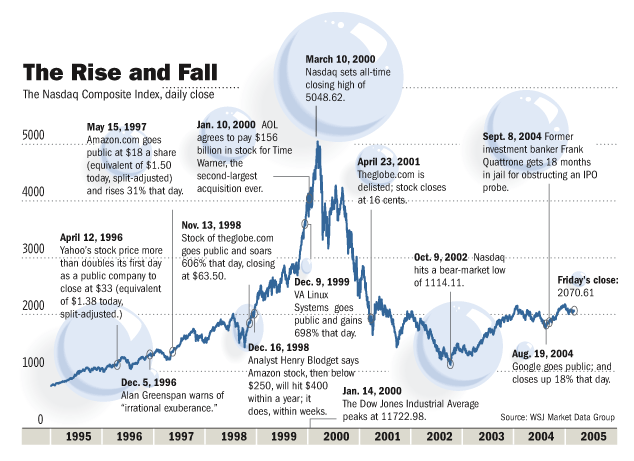

Manias often end at the end of a calendar year. To quote George via a New York Times article dated January 13, 2000: “What I’ve found over a lot of years is that a lot of these manias seem to end at the end of the year” with the article further noting that George “thought a value revival might be just around the corner, noting that the end of other investing crazes — the run-up in the Japanese stock market during the 1980’s, the biotechnology craze of 1991 and the rise of the Nifty 50 in 1972 — all fizzled around the start of a new year.” Obviously prescient and does make one think about the current environment, which is clearly a mania of sorts even if it is “narrower” mania than 1999/2000.

It is important to start the year thinking about where one could lose the most money, rather than where one can make the most money. George spoke to the analysts and fund managers from time to time after he retired. During one of those talks, hosted by Will Danoff, George observed that while most fund managers began the year thinking about which stocks they should own to make the most money, he began the year with the knowledge that roughly 50% of his positions were mistakes, tried to carefully think about which of those mistakes would cost him the most money and eliminate those positions. Minimizing mistakes is essential given that almost all investors — even the best ones — are wrong circa 50% of the time. I really love the humility inherent to this mentality, which is aligned with my increasing belief that “I don’t know” are the three most important words in investing, not “margin of safety.” One can always be wrong, no matter how much work has been done or big the “margin of safety” appears to be.

Being too early is the same as being wrong. Analysts and fund managers often say that “they were early,” rather than wrong. George’s point was that being too early is a mistake rather than a defense. Time in the market is more important than timing the market, but timing does matter for individual stocks as the “price you pay determines the return you get.”

Being a fund manager makes it easier to change your mind relative to being an analyst. George once said that being an analyst, forced to publicly defend and justify your decisions, made it much harder to change your mind relative to fund managers “who could buy or sell in the dark of the night without anyone knowing.” Very true and important given that I believe investing success comes down to finding the right balance between conviction and flexibility; i.e. changing your mind at the right time, especially when you have been wrong.

As a fund manager, you cannot take so much risk that you get taken out of the game or take yourself out of the game at the wrong time. George was obviously 100% right about the technology bubble and value resurgence that followed. He was positioned perfectly for the next 3–5 years, but he wasn’t there to reap the benefits. While George chose to retire, I am also reasonably confident that the relentless questioning from management, consultants, the press and the constant outflows from his funds in 1999 contributed to his decision. This dovetails with both the idea of “client alpha” and George’s own “sometimes being too early is the same as being wrong.” Difficult to even say the latter because George was SO right for the right reasons and didn’t just own value stocks, he owned the stocks that were the best performing value stocks over the next few years. But the larger point for me is that there is a level of risk that is unhealthy for all constituents, even the fund manager. There is nothing better when you are winning and nothing worse when you are losing.

“Client alpha” really matters. “Client alpha” is the idea that having the right clients who are aligned with what you are trying to achieve as a fund manager is critically important. Otherwise capital is often taken away at exactly the wrong time. Buffett was able to stay in the game in 1999 because he had a permanent capital vehicle and a carefully cultivated public image. This is one reason that being a good communicator is important to being an investor if one is managing external capital — one cannot have “client alpha” if the clients don’t understand what the fund manager is trying to accomplish. George was a great communicator, but no one has ever been better than Buffett.

George is one of the greats. I am grateful for all that I learned from him over the years. And to this Morningstar headline from October 5, 2000, “Gasp, could George Vanderheiden been right,” I will simply yes, George was right.

WRITTEN BYGavin Baker