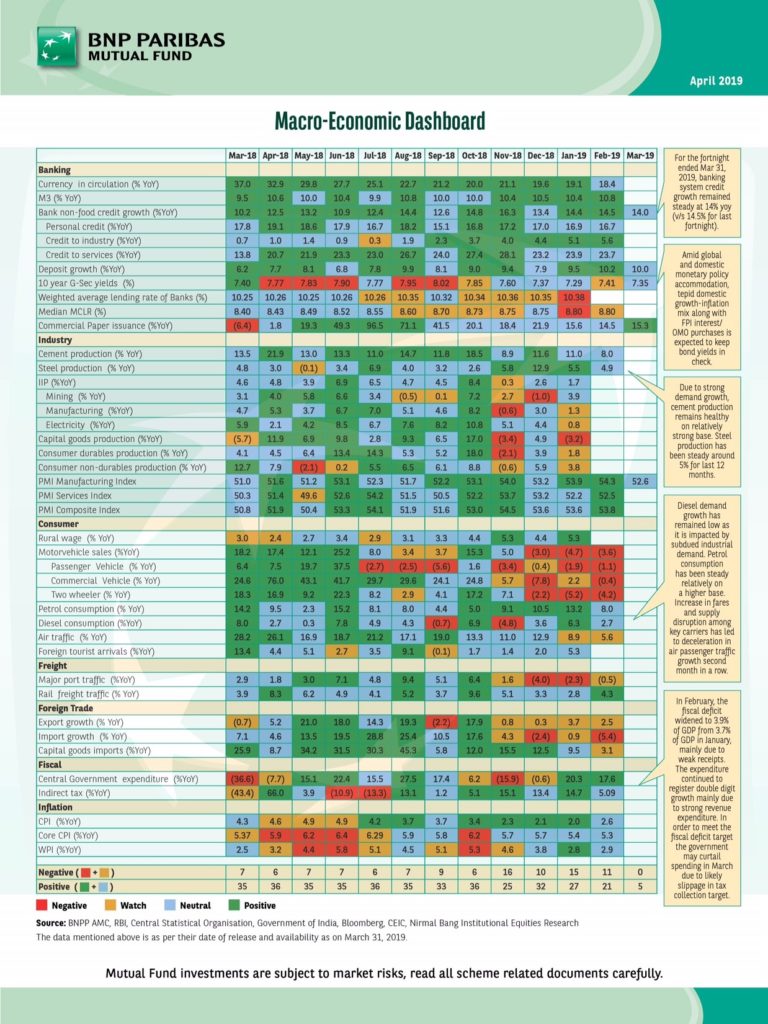

Key highlights of the fortnight:

· For the fortnight ended Mar 31, 2019, banking system credit growth remained steady at 14% yoy (v/s 14.5% for last fortnight).

· Amid global and domestic monetary policy accommodation, tepid domestic growth-inflation mix along with FPI interest/OMO purchases is expected to keep bond yields in check.

· Due to strong demand growth, cement production remains healthy on relatively strong base. Steel production has been steady around 5% for last 12 months.

· Diesel demand growth has remained low as it is impacted by subdued industrial demand. Petrol consumption has been steady relatively on a higher base. Increase in fares and supply disruption among key carriers has led to deceleration in air passenger traffic growth second month in a row. . . In February, the fiscal deficit widened to 3.9% of GDP from 3.7% of GDP in January, mainly due to weak receipts. The expenditure continued to register double digit growth mainly due to strong revenue expenditure. In order to meet the fiscal deficit target the government may curtail spending in March due to likely slippage in tax collection targets