This is a must watch video. It talks about the far reaching impact of battery technology, Electric Vehicles and autonomous vehicles, and how close are we to an unbelievable disruption!

In the end, it converges to a very positive impact for people, for industry at the large and for economies in western world and environment in general.

…..’Cause

I’ve had the time of my life..and I owe it all to you..

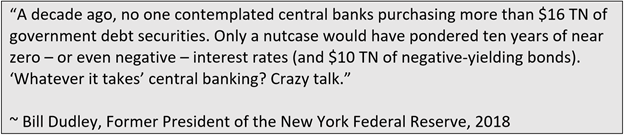

The original song from Dirty Dancing is one of my all time favourites and somehow reminds me of the Global Markets performance this year.Every conceivable asset class (except cash) posted positive returns ,thanks to the LIQUIDITY provided by global central banks.The Fed is my view moved to implement the “ high pressure economy” regime outlined in former chair Janet Yellen’s 2014 speech at the Boston Fed Reserve bank https://www.federalreserve.gov/newsevents/speech/yellen20161014a.htm.

Indirecly

this document suggest the US central Bank has returned to the Greenspan

approach to bubbles- they will deal with the consequences once it pops.

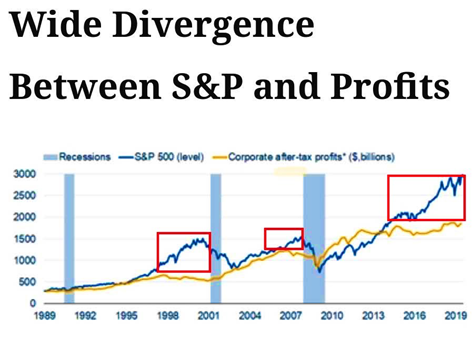

The chart below explains the LIQUIDITY story.

Gone are the good old days when Earnings used to be tailwind for market valuations.

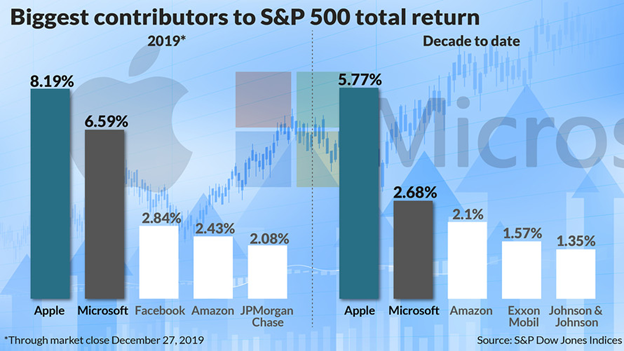

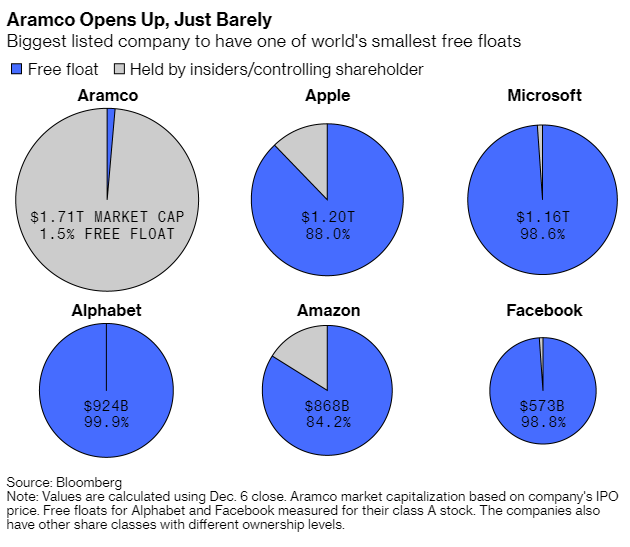

The polarising performance of US markets.

The

two stocks, Apple and Microsoft, each having a market cap of USD 1 trillion

have contributed the most to 2019’s total stock-market returns and also hold

that position for the entire decade.

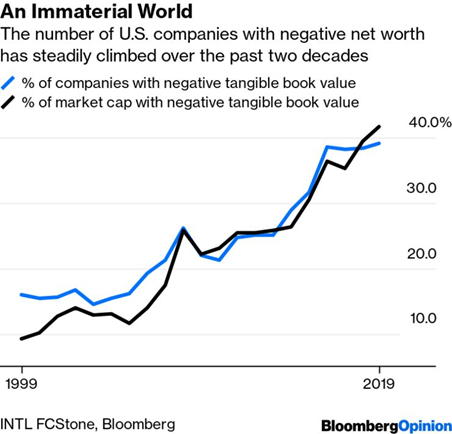

The number of Zombie companies continue to rise along with their market caps.

The above charts were examples of distortion created by excess pumping of money.

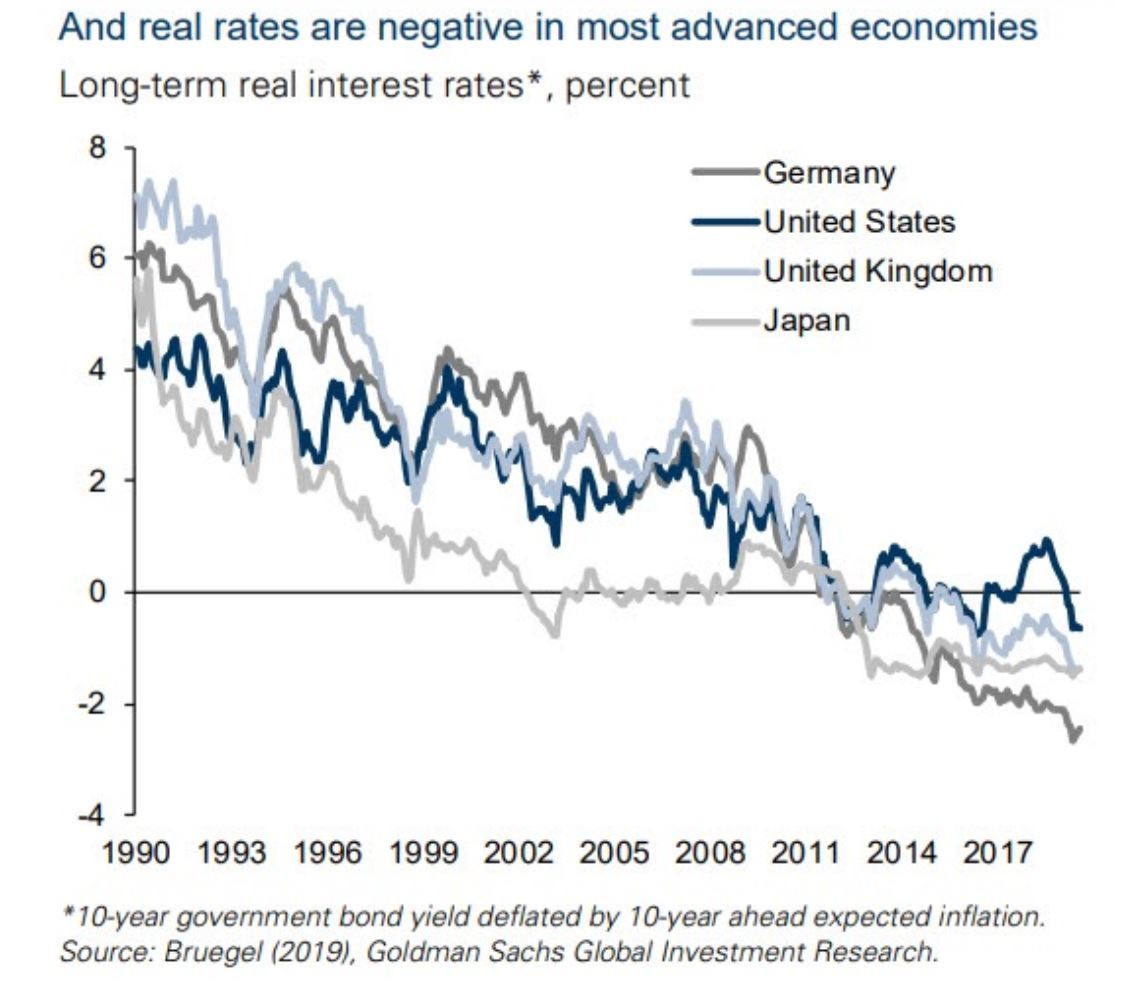

Jerome Powell raised the bar for raising rates significantly whereas the bar for lowering rates has gone down. More evidence that Central Bankers will tolerate higher inflation and low or negative real rates.

BOFA has a crystal ball and they see the endgame approaching .

The global economy has entered a period called ‘slowbalization,’ which is the result of geopolitical shifts and secular trends that have slowed down globalization or, in some cases, completely reversed it. A global manufacturing recession was sparked by changes in consumer preferences that have roiled manufacturing hubs and complex supply chains in developed and emerging markets. Almost every major central bank across the world is easing at the moment in hopes of generating a mini-cycle trough to rebound growth in 2020.

(Ben Hunt via

The Eplison Theory)

Neel Kashkari has just become the voting member of FOMC for the year 2020 and he wants to redistribute wealth in the society.

The farce is complete.

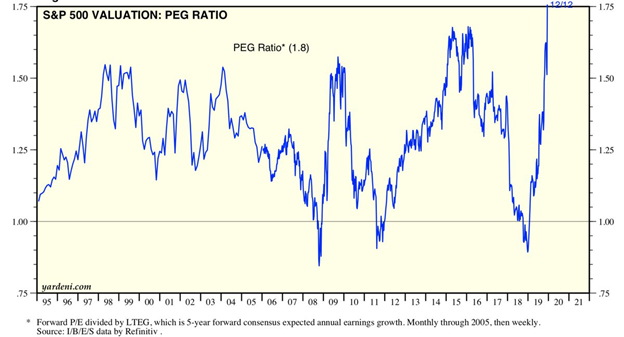

When markets run on nothing but multiple expansion the PEG ratio (price earnings growth) may just skyrocket higher. In this case: Through the historic roof. Don’t let anyone tell you this market is cheap. It’s not, it’s the most expensive in our lifetimes on a PEG basis.

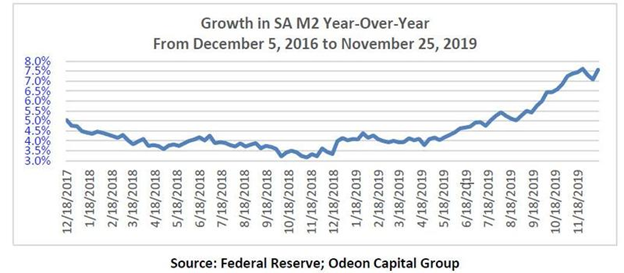

US M2 growth y-o-y which was growing at 3.2% in November 2018, is now growing at 7.6% y-o-y. The economy is not growing rapidly enough to absorb this growth and the competition from the money and bond markets, domestically and overseas, is not compelling.

Money supply is expanding at above average rates and share growth is not. Consequently, share values are expanding — not likely to stop soon.

Winter is coming

Market Outlook

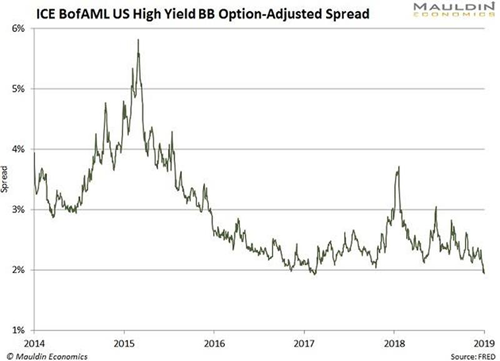

Sure, a lot of things could pop the bubble, if you think it’s a bubble. Inflation fears could do it, lots more of Treasury supply, etc. And the flows just keep on coming. High-yield spreads have dropped to historic lows and I give more credence to signals from credit spreads than equity markets.

But the inflection point in my view was the collapse of WeWork which changed the sentiment away from loss making enterprises in the hopes of dominating market share, to more efficient operations focused on at least attempting to generate profits. Second, the hike by the RiskBank this month to Zero is a sign that negative rates have lost their allure. I couldn’t help but put this photo of Germans standing in line at Cologne outside Degussa showroom to buy precious metals since their hard-earned money lying in bank deposits is now earning negative interest rates.

Finally, the Dollar index (DXY), which was in a rising trend for some time and was supported by a strong US GDP growth is in the process of rolling over and making lower highs and lower lows. Trump and Fed would be happy at this achievement but who knows what a falling dollar bring with it.

Overall, these developments

would appear to support some whiff of reflation and higher inflationary expectations,

1). Shift away from buying

cash- burning market share to buying profits.

2).

Weaker dollar raises the prices of imports and create domestic pricing power.

What are the possibilities regarding

a potential “normalization of repo liquidity post-run? In the year 1999-2000 Fed

had similarly flooded the system with massive liquidity to tide over Y2K

related issues and when it went to withdraw that liquidity there was sharp

negative reaction by stock market. I guess we will see the same towards the end

of first quarter 2020. Emerging markets will be bid till the time Dollar index

is soft. In terms of bonds, the prospect of less certain funding and higher

deficits might also stifle some enthusiasm. Commodities could outperform stocks

as a class.

What if the Fed finds that it can’t step back from repo

operations due to fear of financial dislocations? In this case, stocks could

see a more aggressive “melt-up” helped by tsunami of Fed liquidity, but the

dollar will fall more, and GOLD will benefit.

U.S. recession risk is limited to a 20% chance in 2020

Federal Reserve to remain on hold, not raising or cutting rates in 2020

The U.S. will lead in relative strength

China weakens further

Limited inflation because of limited wage growth

Lower, but positive stock market gains in 2020… with a better first half than second half of the year

Growth above consensus at 2.5%

Year-end close of 3400 for the S&P-500 in 2020 but only if we get a divided U.S. Government after the 2020 elections, and yet…

A full 100% of Goldman Sachs’ sophisticated private equity clients expect a recession in 2020

Central Banks across the globe are holding real (inflation subtracted) rates in negative territory, showing persistent global economic weakness

CHARLES SCHWAB:

Key risks for 2020 are manufacturing weakness and business investment fatigue hurting consumer spending and job growth… unemployment claims are already starting to build even as employment levels rise

Federal reserve to remain on hold

USDollar remains strong but moves mostly sideways

Inflation may slightly rise, helping TIPS (Treasuries that are inflation protected)

Buy extended-duration Treasury-bonds over shorter-duration

Buy investment-grade over high-yield corporate bonds

United States continues to lead in relative strength

Market volatility to be higher than usual

Buy quality, low-volatility large-cap stocks

Small-cap stocks continue their weakness

EVERCORE (Ed Hyman, voted #1 Economist for the past 39 straight years via Institutional Investor’s Annual Survey):

The big stock market drop in December of 2018, followed by the Federal Reserve response, prolonged the market cycle

Lower growth in 2020, unless corporate earnings pick up

Gold is an important part of any portfolio because of the massive amount of money-printing by all world governments

No recession in 2020

Low inflation continues

Interest rates low for longer

Way down the road, the government deficit and high corporate debt will eventually create stagflation

FIDELITY:

The Federal Reserve is unlikely to raise interest rates in 2020, all Central Banks will want their economies to run hotter than normal

For 2020, hold a mix of investment-grade and high-yield corporate bonds even though there will be a deterioration in high-yields as the late-cycle advances

Expect increased volatility over the next two years

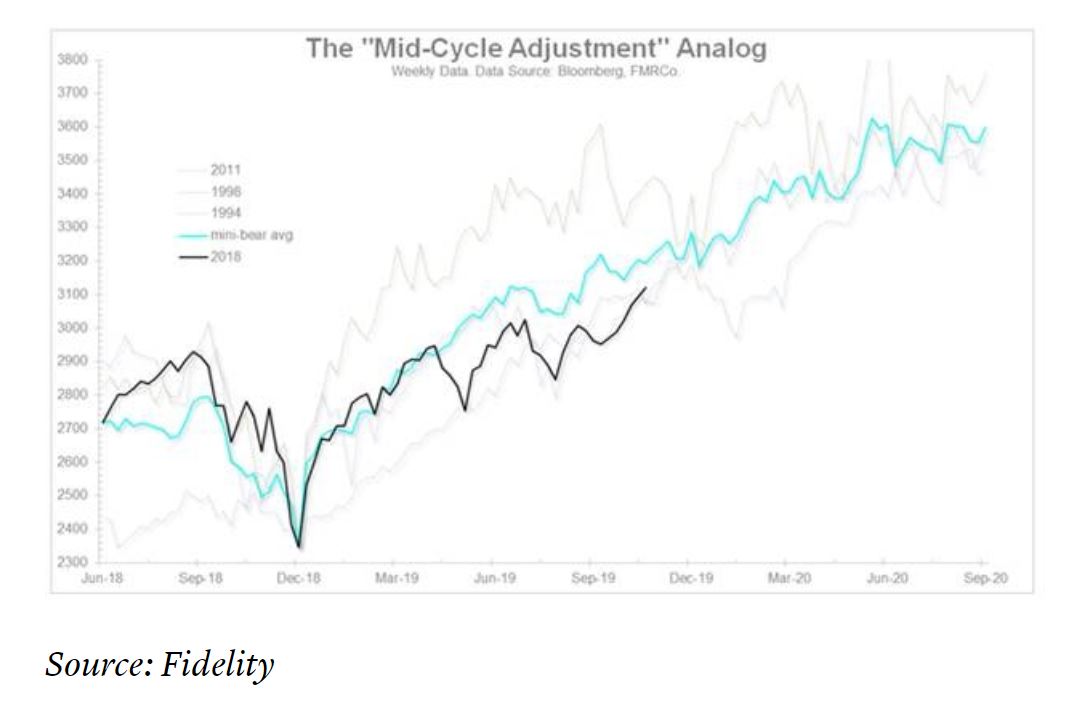

Jurrien Timmer, Head of Global Macro at Fidelity (and one of my favorite analysts), suggests that stocks may continue to run up until the end of summer in 2020 (dark black line below continuing up to the upper-right corner of chart), with a possible recession starting in early 2021:

BANK of AMERICA:

8% corporate earnings growth (because it will be easy to move up from the flat earnings growth of 2019) and this leads to an 8% stock market gain for 2020

Manufacturing weakness may have already bottomed

The financials sector will be the strongest

Several under-valued and beaten down sectors will rotate to the top (IE, energy)

There will be increased volatility and greater draw-downs

Hedge funds will get killed chasing momentum stocks

Pension funds are now holding mostly illiquid (un-sellable) investments and if forced to sell during a major downturn, they will be forced to sell their (liquid) S&P-500 stock positions, further driving down the market

BLACKSTONE:

The stock market is risky and perhaps topping and the Federal Reserve is in a too weak position to offer support

Weaker earnings growth than ‘The Street’ expects

Volatility should increase in 2020

Yields will move slightly higher in response to rising wages and this will cause a slight uptick in inflation

Mid-cap stocks may offer superior gains over large caps

BLACKROCK:

Decent growth for the global economy

Suggest a current mix of cyclicals (especially technology) with defensives (such as healthcare & staples)… and high quality stocks

Positive on U.S. stocks

Negative on European stocks

Positive on Japanese stocks

Very positive on Emerging Market stocks, except…

China weakens further

Positive on gold, especially as a portfolio hedge

Best bonds = high-yield corporates and TIPS (Treasuries that are inflation protected)

GUGGENHEIM PARTNERS:

Economic indicators will continue to weaken

Odds of a recession in the U.S. during 2020 have increased to 50% (which is high)

Pickup in job layoffs to increase in 2020

Both Treasuries and gold should perform well in 2020

There is danger in high-yield corporate bonds because of improper risk ratings

Possible 40%-50% pullback for stocks if recession occurs… 20% pullback if no concurrent recession

Yes, it keeps going…

NEUBERGER BERMAN:

Possible recession in 2020, but more likely in 2021 with stocks falling 6-9 months before recession starts (stocks starting to fall in 2020)

More Fed rate cuts likely during late 2020 and into 2021

There will be increased and more prolonged market volatility

Investment-grade corporate bonds to beat high-yield corporate bonds

Expect a 20% correction sometime in 2020 regardless of recession occurrence

YARDENI RESEARCH:

Main worry is that the S&P-500 could rapidly “melt up” toward 3500… and then crater into a prolonged recession

If bull market continues, then expect better earnings growth at 5.2% in 2020 and 4.7% in 2021

Continued subdued inflation in 2020

Trade War Phase 1 (fluff) likely completed sooner rather than later in order to calm financial markets

Trade War Phase 2 (real deal) likely to be postponed to after the elections with China wanting to ‘wait-and-see’ if President Trump wins a second term

FUNDSTRAT:

Stock market up in 2020 because corporate earnings will grow by 10%

>10% gain in the S&P-500… to 3450

There will be mild inflation that increases in the second half of the year

Best sectors are technology, industrials, financials and energy

U.S. will lead in relative strength

INVESCO:

No recession in 2020

Weak, low growth economy

Rates on hold

No full resolution to Trade War

Growth stocks continue to beat value stocks

U.S. stocks continue to lead in relative strength

Strong USDollar

Favor high-yield over investment-grade corporate bonds

Favor corporate bonds of all types over Treasuries

Positive on Real Estate Investment Trusts (REITs)

Expect low but positive returns for gold

Bearish on commodities in general

Volatility rises in second half of 2020

WISDOM TREE (via their senior strategist Jeremy Siegel of Warton School of Finance):

Interest rates will stay low and float between 2.5% and 1.5%

Holding U.S. Treasury-bonds will hedge against stock market losses

Expect an S&P-500 gain of 8% (that includes a 2% dividend)

Dividend-paying stocks should excel in relative strength

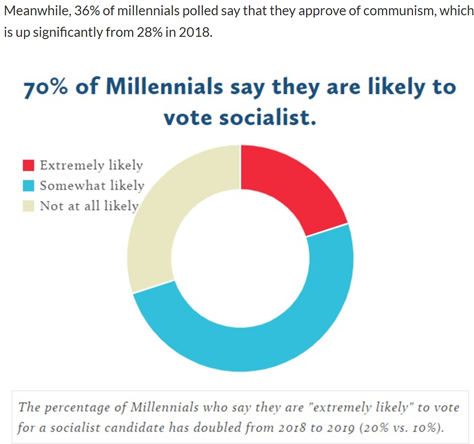

The two biggest threats to the stock market are a continued Trade War and the possible election of either Bernie Sanders or Elizabeth Warren

Recession probability is at 40% during the next two years (and this is fairly high)

(David) ROSENBERG RESEARCH and ASSOCIATES:

A recession is imminent, most likely in 2020, and the problem is that…

The high government deficit means a potential weak government stimulus and…

Low interest rates means a potential ‘too weak’ Central Bank stimulus

The stock market is simply running out of steam

Residential housing has contracted for 6 quarters

Commercial building is now contracting

U.S. exports down for past 6 months

Business capital spending already in recession

Employment data is starting to weaken

Consumer data is weakening

GDP breadth is weakening with 30% of GDP already in contraction

Leading Economic Indicators have recently moved into contraction

Most of globe is ahead of the U.S. in the weakening of economic data

LAZARD:

Slow growth, but no recession in 2020

Extremely accommodative monetary policy

Equities = 5% gain in 2020

Bonds = 5% gain in 2020

BTIG:

More clarity on trade and Brexit would be bullish for stocks

Cyclical stocks beat defensive stocks

Leadership will be found in financials and energy

Neutral on technology, however tech still likely moves up

Bond yields have bottomed, however Fed unlikely to raise rates

FIRST TRUST:

Bullish with the S&P-500 heading to 3650 in 2020

No recession within next 12 months

Interest rates begin to head back up because of increasing inflation

Greatest risk to the market is a far left Democrat winning the White House

FRANKLIN TEMPLETON:

Modestly cautious going into 2020

Risk is still skewed to the downside

Moderate risk of recession in 2020

Mild inflation may cause out-performance by Emerging Markets, in both stocks and bonds

JP MORGAN:

Target of S&P-500 @ 3400

Choose cyclicals (tech) over defensive (utilities)

Choose late-stage sectors such as energy and industrials

Muted inflation despite expected wage growth

LEUTHOLD GROUP:

No recession in 2020

Emerging Market stocks will be the big global winner

In the United States, cyclicals will beat defensives

Mid-cap stocks to be stronger than large-caps

Late-stage assets such as industrials and energy may excel

UBS:

Strong U.S. economy in 2020

No rate hikes

Increased volatility creating deeper pullbacks

MERRILL LYNCH:

Bullish on stocks with a 20% expected gain in 2020

Mom-&-Pop retail investors to drive market higher

Bond risk is increasing, so keep portfolio total bond level @ 20%

U.S. stocks continue to lead in relative strength

Best stocks will be found in the high-quality-large-cap area

RUSSELL INVESTMENTS:

Central Bank easing coupled with the cooling China-U.S. trade war have set the scene for a modest global economic rebound in 2020

Recession in 2021

Low inflation… no Fed rate changes

Sluggish growth in Australia… they will likely implement income tax cuts

Modest growth in the Euro-zone, including U.K.

Minimal growth in China and Emerging Markets

Bullish on U.S. stocks, but they are already expensive

Both high-yield and investment-grade corporate bonds are expensive

Treasury bonds offer the most attractive relative value

DOUBLELINE:

The Federal Reserve is already secretly doing QE-4, as if we are already in a recession

Debt is higher and yet GDP is worse

Manufacturing is now worsening

If no recession in 2020, then President Trump wins another 4 years

LPL RESEARCH:

Economic data, such as earnings, will exceed the current lowered expectations (low hurdle)

Possible recession in late 2020

Solid U.S. equity performance benefiting cyclical sectors (such as tech) and large-cap stocks in general

Weakness in Europe, Japan and China

Stick with high-quality bonds

Low inflation continues

Strong USDollar

QUOTE OF THE MONTH… Larry Kudlow, head of Trump’s National Economic Council (via Forbes Business Magazine): “Tax cuts impose restraints on the size of government. Tax cuts will starve the beast. Specifically, tax cuts provide a policy incentive to starve Social Security, Medicare, education and the environment.”

There is a strong incentive for the bigger institutions to give high “end of year” targets… they want people to enthusiastically give them more money to manage. So, shown above is the 2020 year end S&P-500 forecast (courtesy of MarketWatch). Regarding the 14 analysts shown, I normally pay the most attention to market commentary coming from Brian Belski, Savita Subramanian and Francois Trahan. The truth is that not a single person on this list knows where the stock market will end in 2020. Someone’s prediction might get lucky, merely by chance.

MarketCycle’s PREDICTIONS: We are in the late-stage of the bull market that started in early 2009.

STOCKS: There is the possibility of a bullish melt-up that could even persist into Fall. We could see the S&P-500 @ 3330 by late spring. This boiling pot has to be watched.

RECESSION: There is almost no possibility of a U.S. recession in the next six months. If there is no U.S. recession or late-in-year bear market drop in 2020, then President Trump likely wins a second 4 year term.

RISK: With each passing day, there is an increasing chance of a temporary yet strong & scary stock market pullback of perhaps close to 20%.

BONDS: The Fed is unlikely to raise interest rates in the near or intermediate term and this may benefit interest and dividend paying assets.

USDollar: Likely to remain strong with price drifting sideways.

INFLATION: Non-stop money-printing and government spending coupled with low unemployment could translate to inflation slightly rising from extremely low current levels. In 15 years, inflation could be quite high.

GOLD & COMMODITIES: Typical late-stage assets; likely to benefit from any increase in inflation. Gold is a good portfolio hedge when used in the late-stage of the market cycle.

TRADE WAR: As I predicted months ago, the end of Phase-1 Trade War didn’t move the needle much, at least not in the right direction. The major import by China has always been farm products and they just moved backwards from the #2 importer to the #5 importer of food from the United States. The key feature of the Phase-1 agreement is that China will buy food imports from the United States. The problem is that they just agreed to buy much less than they were already buying. Farmers are really getting hurt. President Trump now seems to be on the attack against Europe, especially after the recent NATO trip where world leaders directly insulted him. He just added 100% tariffs on many European items and this is during a period when much of Europe is already in recession.

RELATIVE STRENGTH: The U.S. continues to lead in strength relative to other countries, although Emerging Markets may get a boost as 2020 progresses.

Stock “buybacks” are starting to rapidly decrease and the Mom-&-Pop retail investor is stepping up to the plate. Normally, Mom-&-Pop arriving on the scene is a late-stage phenomenon that occurs in conjunction with the final bullish melt-up of stocks in an advancing market cycle.

What would make me think that the market cycle may be prolonged this time around? A strong and beneficial stock market correction coupled with a concurrent & rapid positive change in our risk indicators. Our risk indicators showed minimal risk from April 2, 2009 until just before the big 20% stock market drop in December of 2018… almost 10 years. Now, instead of clearing out after that big correction as they normally would have, they have only shown even higher risk levels, so we are positioned to benefit from any market direction. If the market goes up, MarketCycle’s clients should reap about 75% of the gain but if the market drops substantially, we are likely to also make profits. This is a good position in which to be.

LONG TERM: After we reap our eventual and overdue recession, we then continue our journey into the ROARING 20’s decade which will merely be the second half of the current Secular Stock Bull Market that technically began in October of 2011. As I’ve stated several times, I bought the domain name of DOW80000 with the year 2029 in mind. And I am amazed by the magnitude of forces that are due to come to a head or to completion in 2029. Hummm… could 2029 mimic 1929? Could the years after 2029 mimic the difficult years that followed 1929?? Will the cycle repeat all over again?

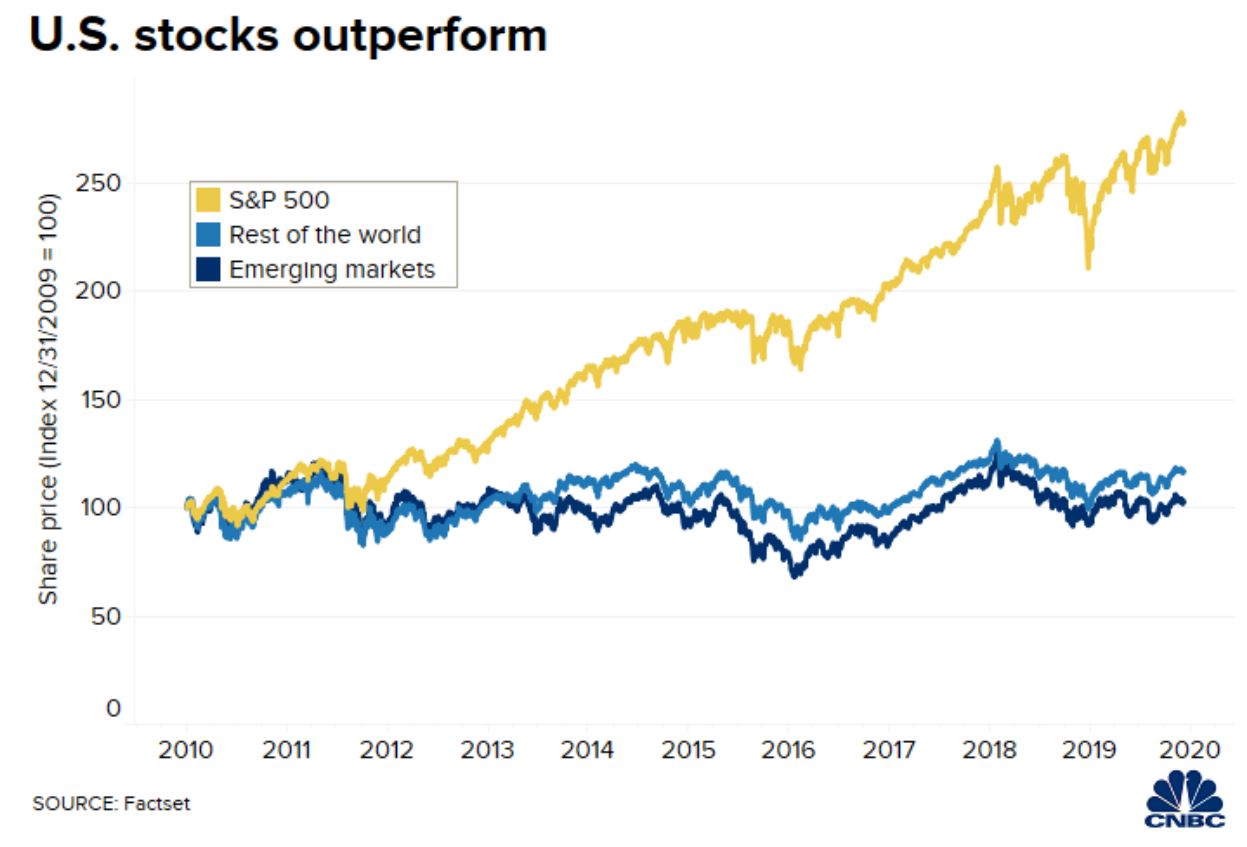

Although we recently took a small position in global stocks, MarketCycle has been correctly holding almost entirely U.S. stocks since the start of this bull market in 2009. From the below chart, you can see (via the gold line) how important this type of decision is and why ‘relative strength analysis’ is so critical to investing. Always hold strength and avoid weakness. (Chart courtesy of Factset & CNBC)

At the dawn of what is going to be a hyper-interesting year in the markets and in society, let’s see what the lovable and goofy Amigos have to say. As usual, we’ll use gold and silver daily charts and a copper daily along with a longer-term view with a weekly chart for the Economic Ph.D. metal.

The charts are the metals futures (click ’em for a larger, clear view), live when I clipped them a little while ago. The caveat with the metals as with macro markets in general is that it is still Santa silly season and so the signals are suspect to whatever degree you put weight on that.

Gold (counter-cyclical Amigo with a heavier anti-economy, liquidity haven utility) is reestablishing the daily chart uptrend by ticking a new high in an attempt to take out short-term resistance. The SMA 200 has been pointing up the whole time and has not hit my favored pullback point where it meets support. Oh well, that’s fine. Prepared is always a good thing to be. It is starting to get a little overbought but would be more so if it makes a new high, as is the technical objective of this breakout.

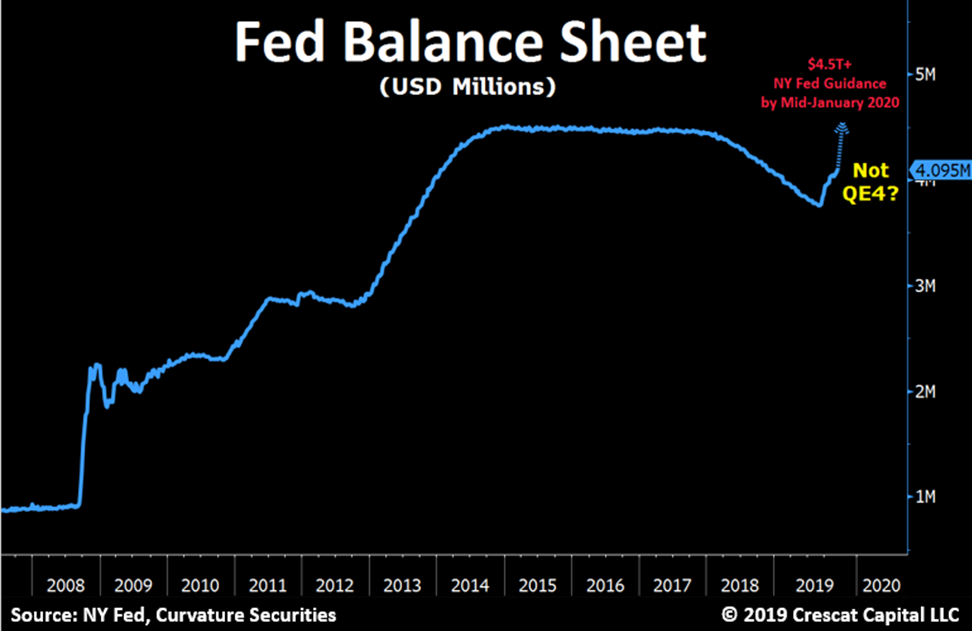

The highly probable and downright inevitable unwind of today’s trifecta of financial asset bubbles: stocks, corporate credit, and Treasury bonds may soon morph into brutal bear market. The end game is unstoppable in our view and approaching fast. The Fed is between a rock and a hard place. It has been printing money like it’s the depth of the Global Financial Crisis while stocks and corporate credit are flying high reflecting a dangerous combination. The panic stimulus at this point in the business cycle is completely understandable, but it is only hastening the unwind of the imbalances the central bank has created and been impossibly trying to maintain. The idea that money printing is an insurance policy that does not come with a cost is simply wrong.

Repo Crisis

The Fed is in fight-or-flight mode because there are very real credit bottlenecks in the plumbing of the banking system that have created a US Treasury funding emergency. The central bank has been forced to add $364 billion of Treasury securities to its balance sheet over last four months and has committed to another $471 billion though mid-January. The money printing was necessary to fight a repo market funding shortage that warns of a systemic financial crisis in the making. Usually when the repo alarm bell flashes, it’s too late. Because of the Fed’s swift action, mayhem was averted but likely only in the very short-term. Major imbalances remain. One huge problem is that investors at large do not even know what a repo crisis means, so they have been interpreting the cash injections as a reason to go all in on risky assets. The bullish investor sentiment and positioning among investors last week reached the highest levels we have ever seen. Such ebullience in the past has been associated with major stock market tops. Today, we have structural imbalances and catalysts to make that a highly likely scenario, potentially even as we head into year end.

The Fed miscalculated the level of reserves it should have kept in the system so that banks can smoothly supply credit to the securities and FX markets and fulfill their regulatory capital requirements at the same time. So, it was a complete surprise on September 17, when US Treasury repo funding market froze up and the overnight rate jumped as high as 10% that day. Since then, the Fed has been trying to prevent a disorderly deleveraging of the entire financial system. Short-term interbank lending is the core of the entire financial system. When repo rates spike, it means there is not even enough cash in the system for banks to support the Treasury market, let alone the rest of the securities and FX markets to allow their normal functioning. For instance, when the repo rate jumped in September 2008, it froze the global financial system and bankrupted Lehman Brothers, so it’s a big problem.

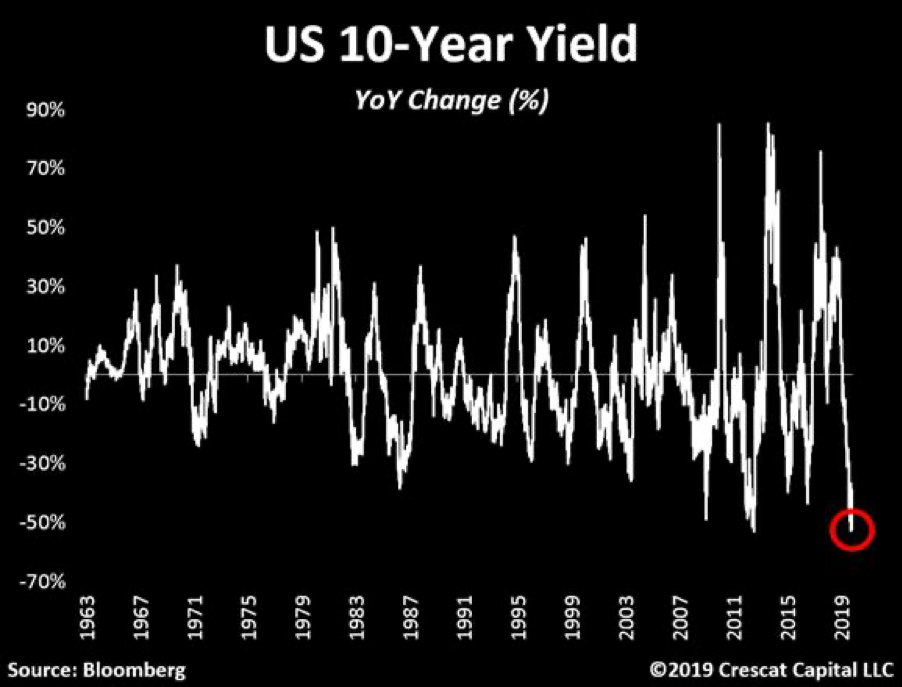

The repo rate is also the short-term financing cost for financial institutions such as hedge funds to buy Treasury securities on margin including buying long duration Treasuries to speculate on a declining interest rates and/or deflation. It is one side of the popular risk parity trade among large hedge funds and institutional investors. In 2019, investors crowded into long duration Treasuries as the yield curve inverted in anticipation of a recession. The 10-year yield had its biggest year-over-year decline ever. After such a move, this trade simply became too crowded. In our view, it has already played out. Today, we believe there is a strong case for rising global yields on the long end of the curve as we explain below.

One thing the average investor is likely not paying attention to is the selloff on the long end of the Treasury curve which indicates that the repo funding problem may not been contained yet. Rising long-dated yields preceded the September shock and have only continued during the emergency Fed injections. Large hedge funds and institutions have crowded into leveraged long bond positions which rely on repo funding. If credit tightness continues these positions could be forced unwind creating more market instability necessitating the official beginning of the QE4. It’s key to note that it’s not just US Treasuries but the entire global sovereign long end that has been selling off.

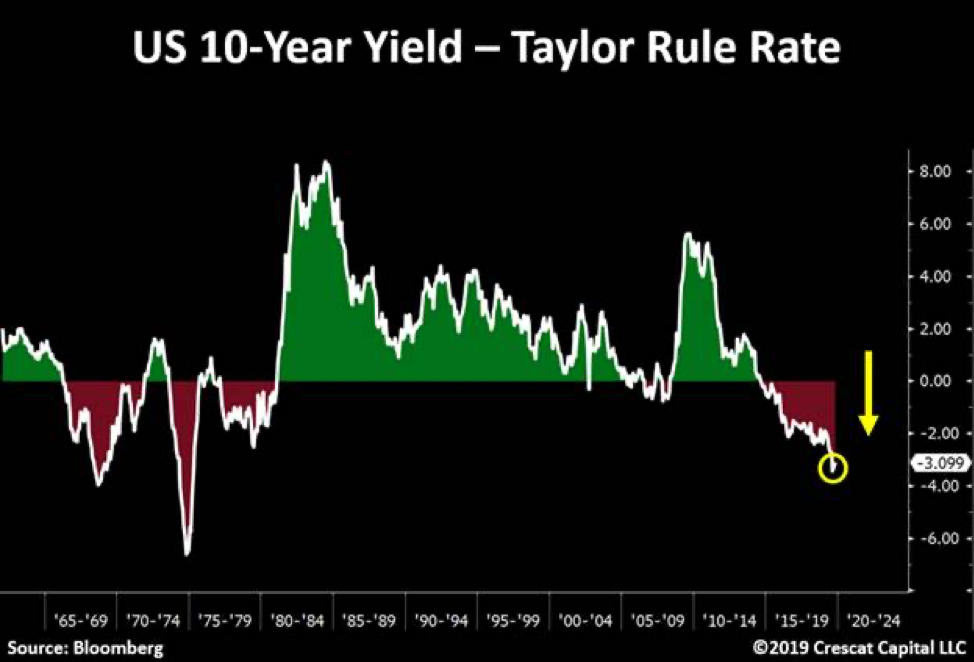

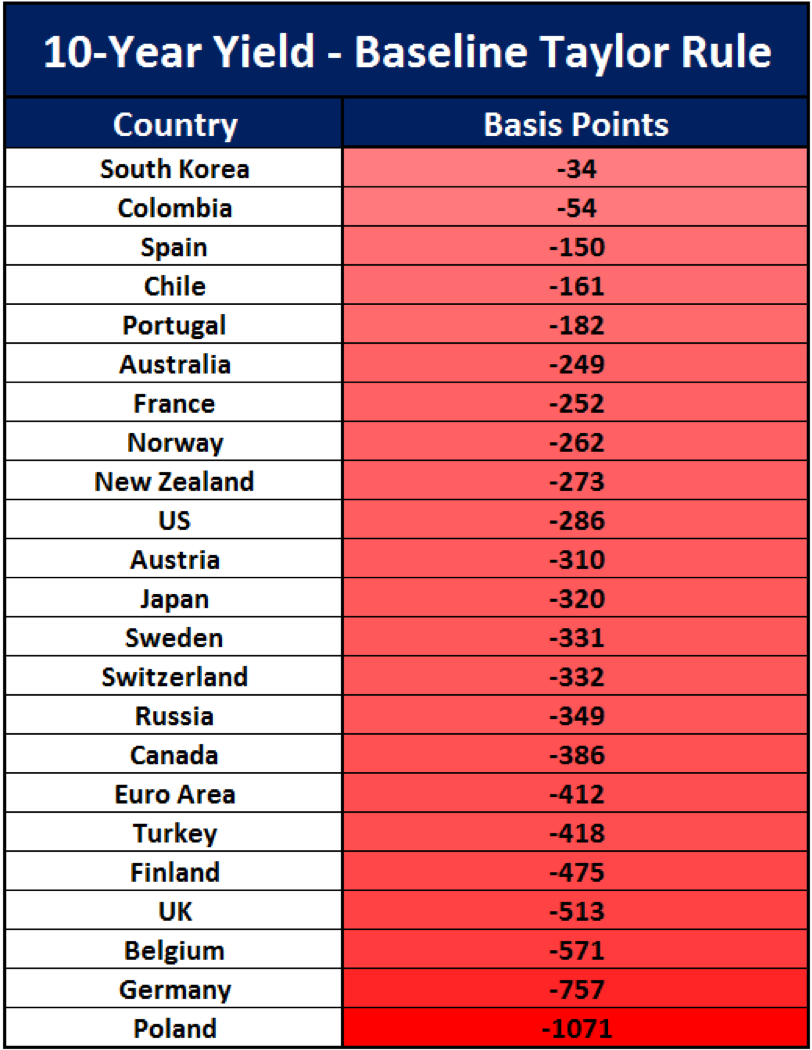

Running Hot

The Fed’s monetary policy is running hot and long-term interest rates aren’t aligned accordingly. John Taylor, a Stanford University economist once considered to lead the Federal Reserve, developed a formula to calculate where the Fed funds rate should hypothetically be according to inflation rates, strength of the labor market, and potential output of the economy. Using that as our baseline for interest rates, the Fed isn’t just running an aggressive inflationary policy on the short end of the curve, long-term rates are also notably out of balance. For instance, the 10-yr yield vs. the Baseline Taylor Rule rate is now at its most extreme in 44 years. Inflation became a problem during all times this spread went negative. What makes this issue even more unique is the fact that on top of running an extreme loose rate policy, the Fed is printing money in a massive way. It’s hard to say monetary policy won’t come at a major cost this time.

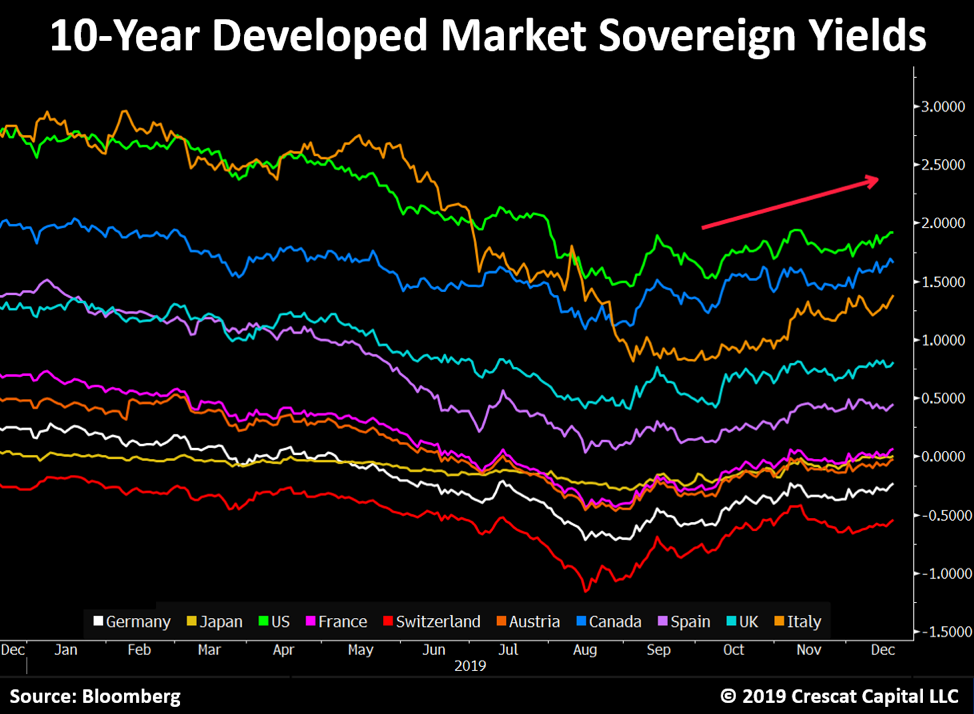

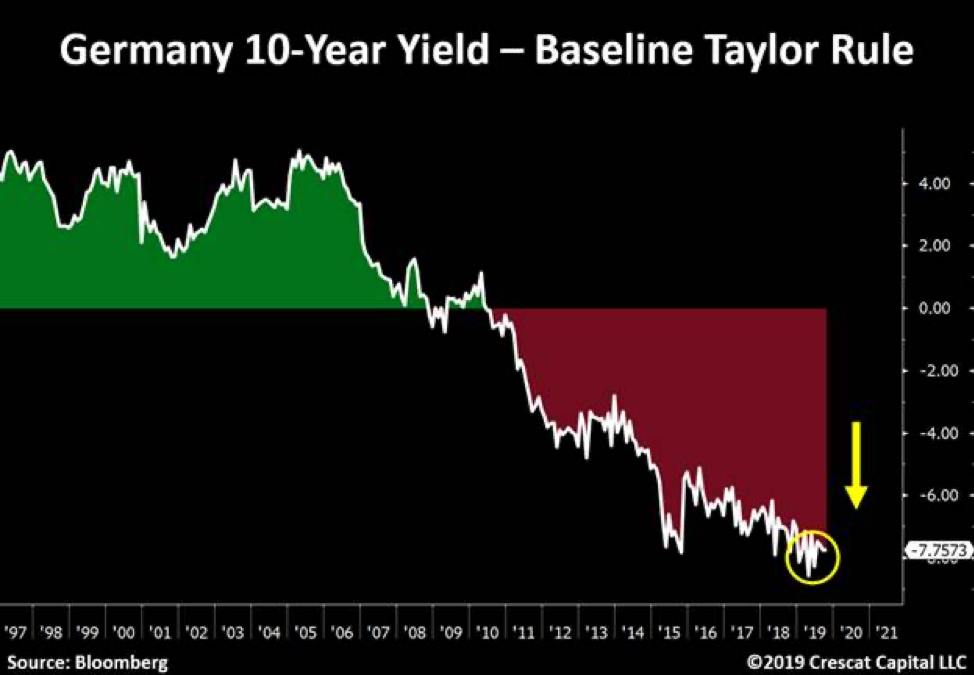

This is not only a domestic phenomenon. We see this issue worldwide. Germany’s case, for instance, is twice as extreme. According to the Taylor rule formula, short term interest rate should be close to 8%. In contrast, ECB rates are close to -0.5% while bunds’ 10-year yields are at -0.22%. The spread of between German long-term rates and its baseline Taylor rule rate is now at its highest level in history.

Below are similar disparities across the globe to consider. Most of them are in Europe, but almost the entire world should start seeing more pressure on long-term interest rates to rise while global central banks continue to run aggressive monetary policies to foster a global economic expansion now nearing exhaustion while funding record indebted governments.

The Labor Market and Consumer Confidence – Falling into Place

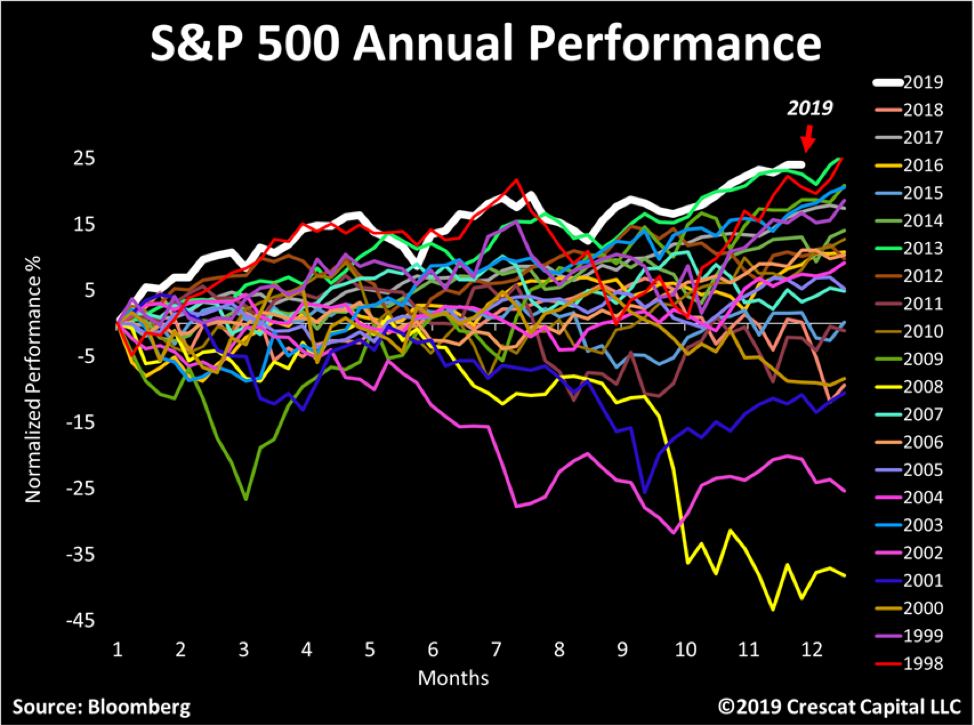

Stocks are on pace for their best performance in 22 years all the while many key fundamentals such as corporate earnings and industrial production have been deteriorating all year. Continued gains for the broad stock market in 2020 are highly improbable in our view as even more of the key fundamentals in the jobs and consumer market are only just starting to roll over from exuberant extremes.

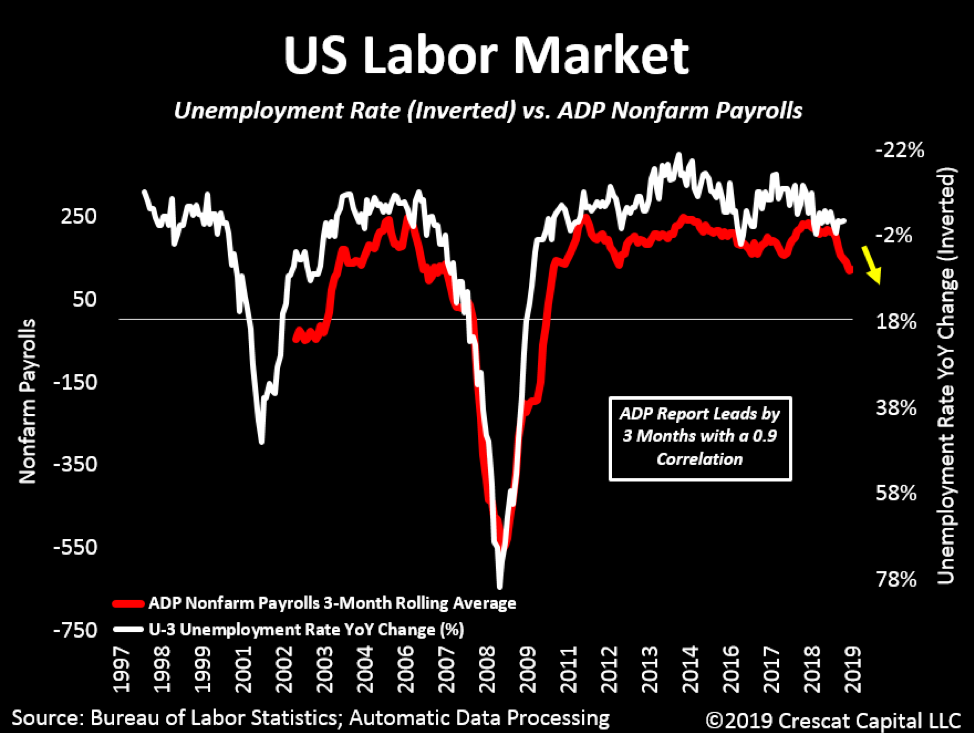

Among the many imbalances and catalysts we cited in last month’s recent research letter, the over-extended labor market is showing significant signs of cooling. The lagging and contrarian unemployment rate from the Bureau of Labor Statistics remains near cycle lows, just like it always does at the peak of a business cycle, right before a market downturn and recession. Meanwhile, three leading employment indicators are showing signs of significant cracks:

(1) Declining BLS Job Openings;

(2) Spiking DOL Initial Jobless Claims; and

(3) A recent plunge in the ADP Employment Report

The ADP report calls into question the more optimistic BLS job numbers with the largest negative divergence since 2010. The year-over-year change for ADP payrolls is decelerating in a pattern last seen directly ahead of the Global Financial Crisis. What’s crucial is that the 3-month rolling average of ADP payrolls leads the rate of change in unemployment rate by 3 months with a correlation of almost 0.9!

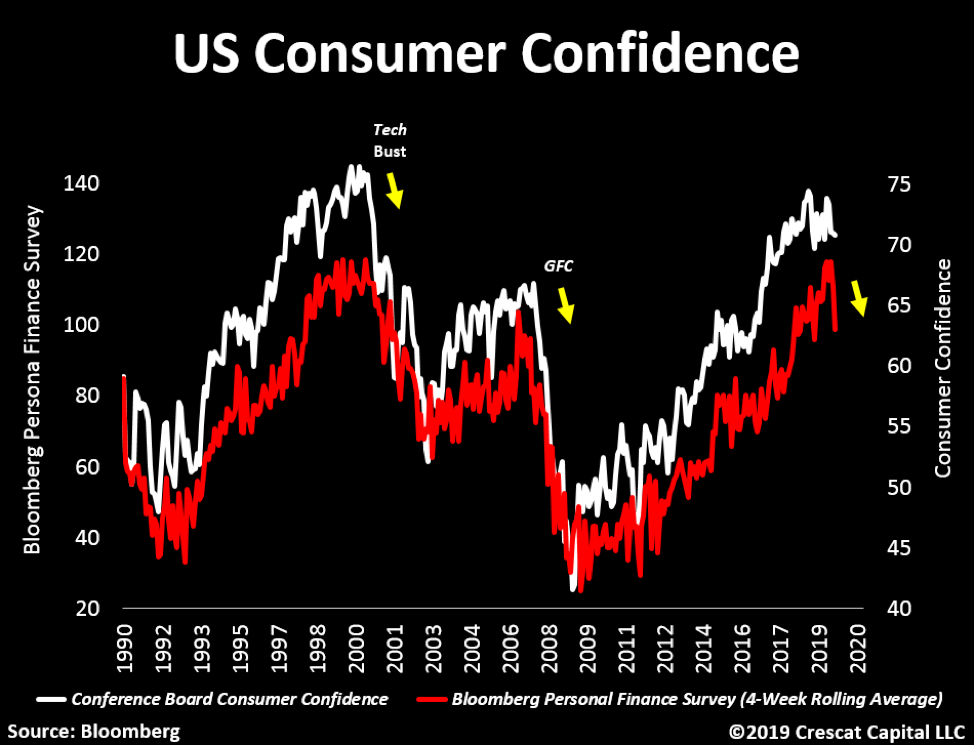

We have likely reached peak consumer complacency, another key piece of the macro puzzle. After retesting tech bubble levels, the Bloomberg Personal Finance Survey index is now falling and significantly diverging from the Conference Board’s Consumer Confidence. With the jobs market topping out, we believe consumer confidence will be the next shoe to drop.

Cost of Capital Poised to Rise

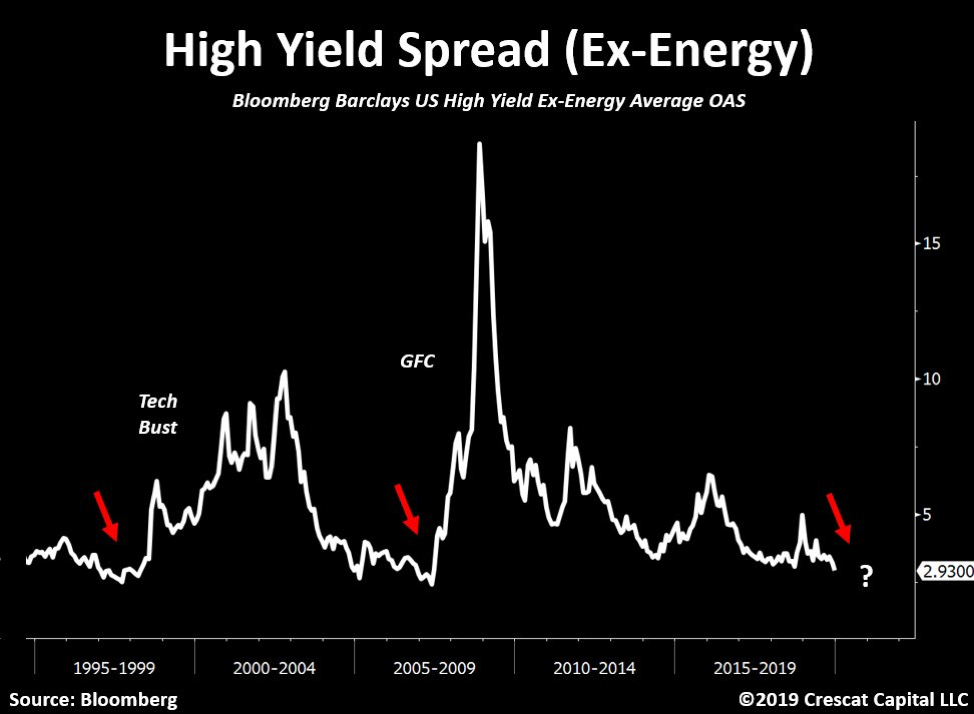

The bull case for stocks rests on one major liquidity force, the cost of capital. That’s driven by the availability of credit and the strength of company fundamentals. When looking at equities broadly, aggregate earnings per share for Russell 3000 index just started to fall on a year over year basis. Furthermore, corporate balance sheets never looked so weak. Leverage ratios are at record highs, and in contrast, companies with a junk credit status are now borrowing money at their lowest levels since the peak of the housing bubble. For instance, the Bloomberg Barclay High Yield (Ex-Energy) Index today is at its lowest premium to 10-year Treasuries since June of 2007.

When default risk returns and interest rates spike higher, many of these low-credit-quality businesses will not survive. Since WeWork had to scrap its plans to go public and other recent new issues broke below their IPO price, investors have been turning their focus away from top-line growth towards companies that have underlying free cash flow profitability, or at least a clear path to get there soon. We believe this shift in mindset is already forcing companies to either raise prices of goods and services or cut costs to improve margins, and we expect this trend to continue. These changes should have a significant impact on consumer prices, labor markets, and the business cycle.

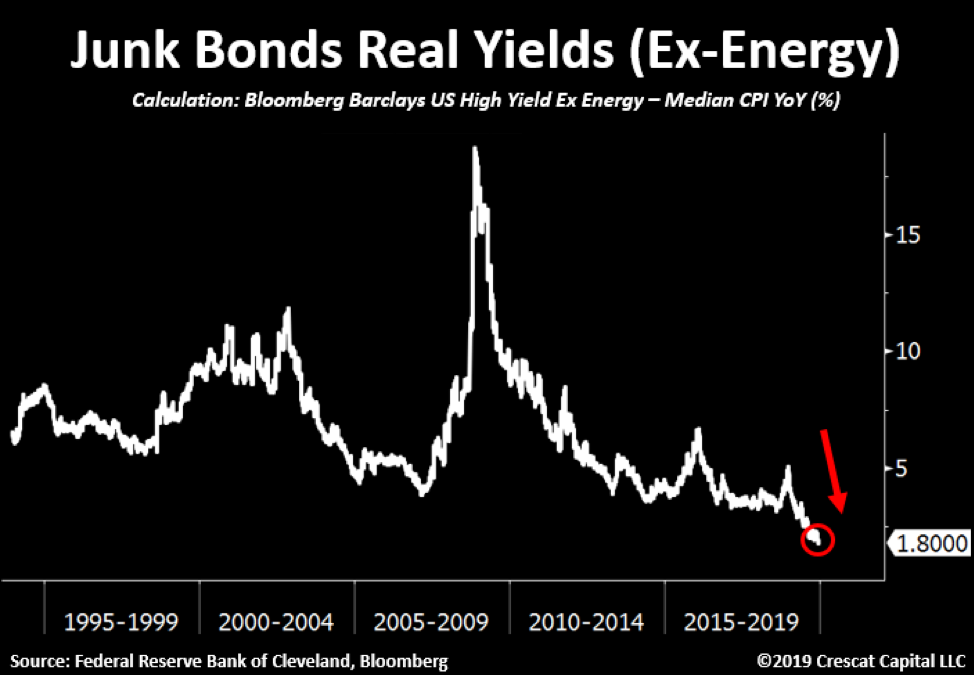

In this backdrop, we question if the demand for low-rated bonds will remain strong relative to higher quality assets. Junk bonds only yield 180 basis points higher than median CPI! It’s the lowest level in the history of the data.

To add to the bearish thesis, the 3-month implied volatility for put options on JNK, a high yield corporate bond ETF, is now at its lowest level ever. Prior cyclical lows in volatility preceded significant selloffs in this ETF as well as overall stocks. We view this as an opportunistic entry point to short junk bonds ahead of a business cycle downturn that is fast approaching.

Precious Metals

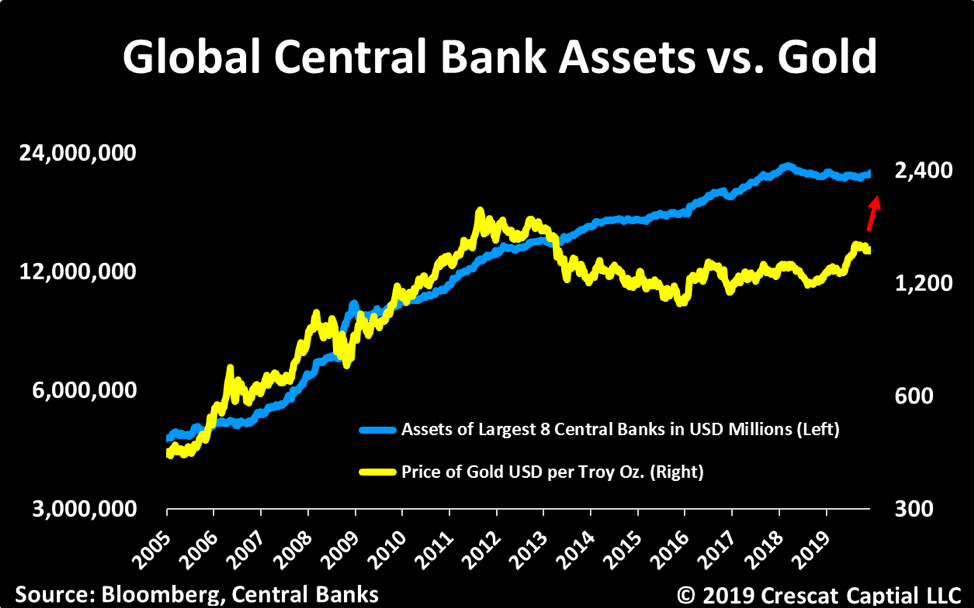

Precious metals are poised to benefit from what we consider to be the best macro set up we’ve seen in our careers. The stars are all aligning. We believe strongly that this time monetary policy will come at a cost. Look in the chart below at how the new wave of global money printing just initiated by the Fed in response to the Treasury market funding crisis is highly likely to pull depressed gold prices up with it.

The imbalance between historically depressed commodity prices relative to record overvalued US stocks remains at the core of our macro views. On the long side, we believe strongly commodities offer tremendous upside potential on many fronts. Precious metals remain our favorite. We view gold the ultimate haven asset to likely outperform in an environment of either a downturn in the business cycle, rising global currency wars, implosion of fiat currencies backed by record indebted government, or even a full-blown inflationary set up. These scenarios are all possible. Our base case is that governments and central banks will keep their pedals to the metal to attempt to fend off credit implosion or to mop up after one has already occurred until inflation becomes a persistent problem.

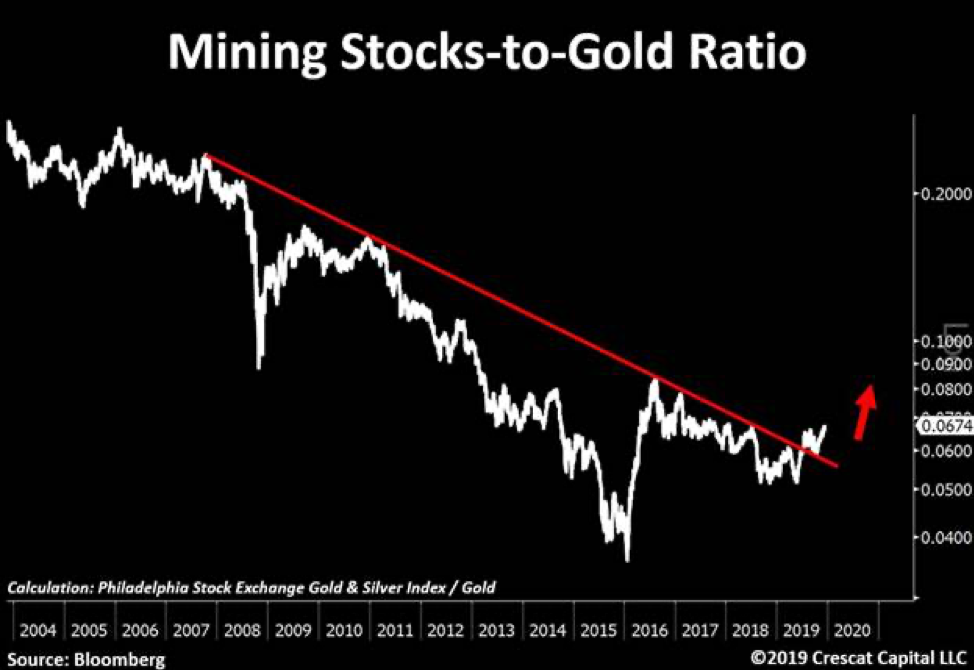

The gold and silver mining industry is precisely where we see one of the greatest ways to express this investment thesis. These stocks have been in a severe bear market from 2011 to 2015 and have been formed a strong base over the last four years. They are offer and incredibly attractive deep-value opportunity and appear to be just starting to break out this year. We have done a deep dive in this sector and met with over 40 different management teams this year. Combining that work with our proprietary equity models, we are finding some of the greatest free-cash-flow growth and value opportunities in the market today unrivaled by any other industry. We have also found undervalued high-quality exploration assets that will make excellent buyout candidates.

We recently point out this 12-year breakout in mining stocks relative to gold now looks as solid as a rock. In our view, this is just the beginning of a major bull market for this entire industry. We encourage investors to consider our new Crescat Precious Metals SMA strategy which is performing extremely well this year.

Zero Discounting for Inflation Risk Today

With historic Federal debt relative to GDP and large deficits into the future as far as the eye can see, if the global financial markets cannot absorb the increase in Treasury debt, the Fed will be forced to monetize it even more. The problem is that the Fed’s panic money printing at this point in the economic cycle may hasten the unwinding of the imbalances it is so desperate to maintain because it has perversely fed the last-gasp melt up of speculation in already record over-valued and extended equity and corporate credit markets. It is reminiscent of when the Fed injected emergency cash into the repo market at the peak of the tech bubble at the end of 1999 to fend off a potential Y2K computer glitch that led to that market and business cycle top. After 40 years of declining inflation expectations in the US, there is a major disconnect today between portfolio positioning, valuation, and economic reality. Too much of the investment world is long the “risk parity” trade to one degree or another, long stocks paired with leveraged long bonds, a strategy that has back-tested great over the last 40 years, but one that would be a disaster in a secular rising inflation environment.

With historic Federal debt relative to GDP and large deficits into the future as far as the eye can see, rising long-term inflation, and the hidden tax thereon, is the default, bi-partisan plan for the US government’s future funding regardless of who is in the White House and Congress after the 2020 elections. The market could start discounting this sooner rather than later. The Fed’s excessive money printing may only reinforce the unraveling of financial asset imbalances today as it leads to rising inflation expectations and thereby a sell-off in today’s highly over-valued long duration assets including Treasury bonds and US equities, particularly insanely overvalued growth stocks. We believe we are in the vicinity of a major US stock market and business cycle peak.

Crescat is positioned to take advantage of this opportunity and you can read more about it below

MSCI All-Country World index IS breaking out above 2018 highs this month, which many find as reason to rejoice- But yet, ,the same thing happened also in 2007 exceeding 2000 peaks? ( Mark Newton)

This 12-year breakout in mining stocks relative to gold now as solid as a rock. Couldn’t be more bullish for such a historically depressed industry. Exactly how the early stages of a precious metals bull market should look like. ( Tavi Costa)

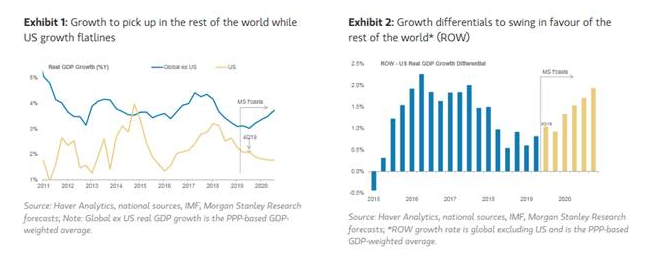

Morgan Stanley expects for 2020 will be driven by an improvement in the world excluding the US, while US growth flatlines around trend. Growth differentials will therefore swing back in favour for the rest of the world.

There is basically not a single financial price that currently has any true information value any longer… But really hard to lean against equity momentum. Link to our editorial -> https://ndea.mk/Zombie

The US central bank has been in control of short-term rates, not long-term. The Quantitative Easing of 2008-2009 was all about reducing the supply of long-term debt in hopes of lowering long-term rates, which they hoped would revitalize the real estate market. Here, the Fed is dealing with its own perceived power. The mere fact that the Fed had to step into the repo market and continues to provide liquidity is an effort to prevent short-term rates from rising. It also reflects the reality that the Fed has lost control of interest rates. They will ultimately be unsuccessful in maintaining control over short-term rates on a sustained basis. We are entering a whole new dimension. This is not Quantitative Easing as so many immediately called it. They just lack the understanding of how the economy truly works both globally and domestically.

The Federal Reserve made no change to its target interest rate at its December meeting, expressly saying that the economy remains strong. They said that in fact the economy is so strong that few central bank officials currently saw any need to cut interest rates over the next 12 months. This is because the capital flows are still pointing into the USA while the rest of the global economy is showing major signs of stress. The Fed cannot lower rates when the pressures are for rates to rise due to risk factors nobody will talk about publicly.

“This year, 88% of advisors indicated that they currently use or recommend ETFs with clients, compared with 70% for mutual funds. 45% of advisors said they plan to increase their usage of ETFs over the next year, compared with just 19% for mutual funds” https://wealthmanagement.com/mutual-funds/slow-demise-mutual-funds…

Bank of Canada Governor Stephen Poloz is no fan of Modern Monetary Theory: MMT “is offering us a free lunch, and most of us know there is no such thing…it has been tried many times in the past, and the record is not pretty.”

Lookout. Strongest negative correlation between gold & yields ever! Completely unsustainable. The Fed’s printing machine is officially on. Gold probably at early stages of a bull market & yields likely bottomed. It’s all fun and games until monetary policy comes at a cost

This again. China agreeing to make $50 billion in U.S. agricultural purchases in 2020. The RECORD value for annual U.S. ag product exports to China was in 2012 at just under $26 billion. Compare commodity prices then and now. For reference, 2017 was $19.5 billion.

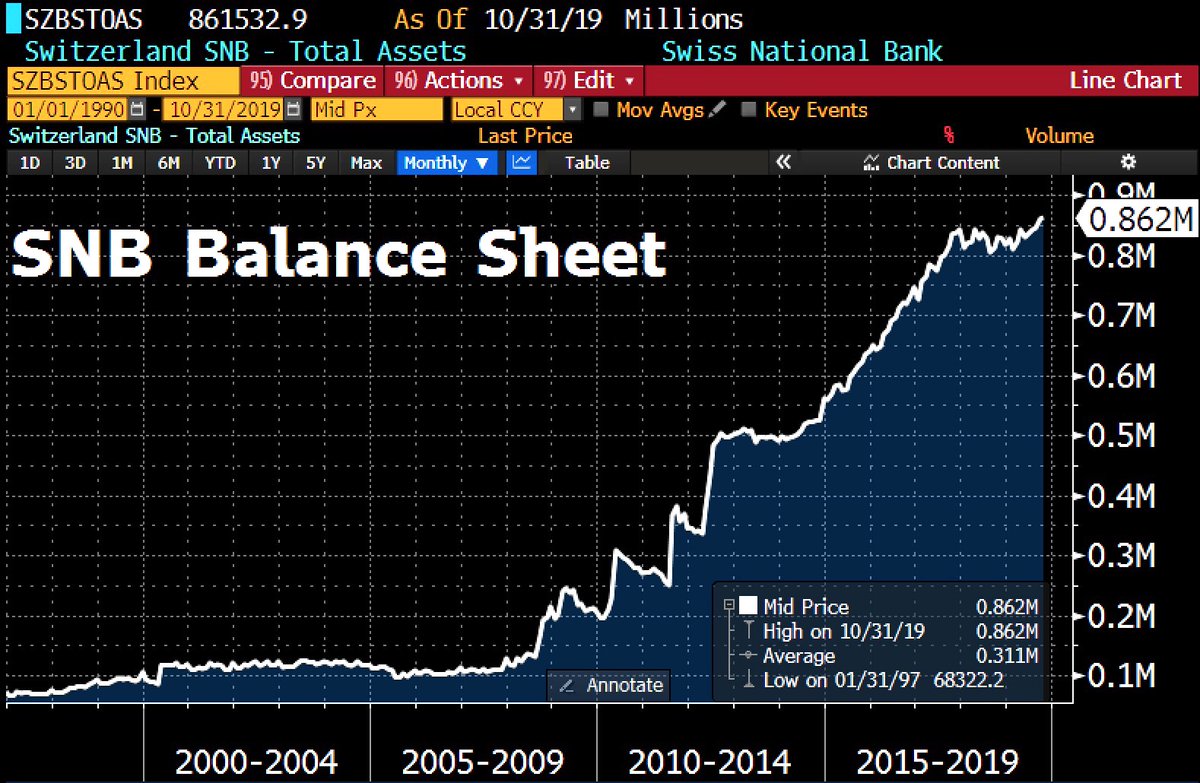

Swiss Central Bank could be required to pull its $800bn balance sheet out of investments in fossil fuel comps in a move by one of world’s biggest reserve banks to tackle climate change. Swiss lawmakers are preparing a campaign. http://news.trust.org/item/20191210104145-back7/…

Investing is all about probabilities. If the perceived odds of an event are high, certain securities will be priced based on those expected probabilities. The corollary is that when an event is perceived as almost impossible, securities do not price in any chance of it occurring. If that event does occur, all sorts of securities need to re-price—often quite rapidly. I like to spend my time pondering what potential events the market completely ignores. Of all potential economic outcomes, the one that is least anticipated and least priced in, is an uptick in inflation.

It is said that generals always fight the last war. In terms of macro-portfolio wars, Japan’s experience with deflation colors all views. This seems odd to me because we have over two millennia of history showing inflation and currency debasements to be universal constants, with one outlier in Japan. The question is if Japan is the new normal or a true outlier?

Academics have studied the causes and effects of inflation ever since emperors and kings fixated on halting its effects. Despite a massive body of work, there is little agreement amongst experts on the causes of inflation. Since I tend to ignore “experts,” let me start by giving you the Kuppy definition of inflation. “Inflation is when too much of a certain currency chases a scarce resource and pushes its price higher when defined in terms of that currency.” Using that definition, we’ve actually had rather dramatic inflation over the past decade—it just hasn’t shown up yet in the core consumer goods that central bankers are often concerned about.

Did they time-stamp the cyclical low in yields?

When a country prints money, no one knows where within the economic ecosystem it will ultimately flow. If a resource is scarce, it tends to experience inflation—when it is artificially scarce, it has even more extreme inflation. Just think of where the money printing has ended up this cycle; bonds (central banks restricted supply by buying them), stocks (PE and buybacks have restricted supply), gateway city residential housing (local municipalities have restricted supply), medical costs (systematic dysfunction has restricted supply), vintage wines (they aren’t being produced anymore), college education (supply restricted again), I can go on, but you get the point. Meanwhile, traditional inflation stalwarts like food and energy have remained suppressed due to technological advancements, reduced logistical costs and excess liquidity, which has allowed capacity to overshoot and lead to price deflation. To say that we’ve not had inflation over the past decade is wrong, we just haven’t had inflation in places that are key components of the CPI basket.

However, that may be changing. I believe that the number of sectors with restricted supply are starting to expand. Let’s look at labor, which historically has been a primary source of inflation. It’s no secret that US unemployment is at historic lows, laborers now have bargaining power and wages are rapidly increasing—with increases made more extreme by minimum wage laws, healthcare inflation and new mandates in various states. The cost of labor goes into almost every finished good—particularly in a labor-intensive service economy. Politicians on both sides seem willing to pass laws that give labor a bigger share of the pie—what will that do to inflation?

Now think of energy; it’s a crazy world out there and global energy security is no longer guaranteed. Prices have been suppressed for the past few years by excess production due to uneconomic shale—that’s clearly reversing as the funding has been cut off. Where do you think energy prices go if shale growth flat-lines or goes in reverse? What about when key producing regions devolve into chaos? Tanker rates are also expanding—that increases energy prices as well.

Now think about consumer goods; the past few decades were all about increased globalization where manufacturing migrated to the cheapest possible location. Trade wars and regional balkanization upend this trend. Now there ought to be an implicit geopolitical risk premium priced into gross margins on every good. Supply chain disruptions further increase costs. If globalism was deflationary, isn’t the reverse inflationary?

Think about what venture capital has done to costs. Thousands of businesses are losing hundreds of billions a year to gain market share in rather prosaic industries. Think about what Uber has done to transport costs or Chewy has done to the cost of dog food. These are all subsidized by VC firms so they can dump IPOs on unsuspecting retail bag-holders. As these businesses are forced to raise pricing in order to become sustainable, what will that do to consumer inflation? Won’t all sorts of sectors also gain pricing power, now that they don’t have to compete with someone who sells a Dollar for 80 cents hoping to make it up with volume? Isn’t the collapse of the Ponzi Sector bubble inherently inflationary?

What about all the supply restriction as ESG takes its toll on economies? If you can’t get permits to build a new coal mine or oil pipeline, yet demand keeps growing, won’t pricing increase as well?

I can go on and on. All the trends that were deflationary are slowly going in reverse. We haven’t seen the effects of this show up in the data yet, largely because the global economy is rapidly deteriorating, which is putting a brake on the demand side. However, even with the global economy slowing, inflation is starting to tick up in the US. Can the rest of the world be far behind us?

Of course, government policy drives all of this. I think it is obvious that we’ve finally reached the limits of monetary policy. Does the ECB taking rates 10 basis points more negative do anything but accelerate the bankruptcy of the Eurozone banking system? Does it increase consumption or capital expenditures? Of course not. If anything, it just starves the system of capital by taking everyone’s return on capital investment down towards zero and below. Who invests when expected returns are negative? What the world needs is a big reset of the system where leveraged firms default, solvent firms pick up the pieces and get to earn excess returns due to their past fiscal sobriety. Since we live in a democracy, that won’t happen, instead we will have extreme fiscal stimulus in order to kick the can further down the road.

In October, I spent 15 hours in the Sheremetyevo airport in Moscow (damn connecting flight never showed). It hasn’t seen a dollar of cap-ex in years, but it’s still light years ahead of LaGuardia or LAX. Just wait until corporations learn how much they can make from a never-ending airport renovation project. Now multiply that by hundreds of airports in America that desperately need capital investment. Now add bridges, roads, bullet trains, water infrastructure and our electrical grid. Why are all the lobbyists trying to get us into wars with third world nations? Corporations would make more money fixing our infrastructure and it’s going to be a lot less politically contentious.

If you think deflation is a fact of life, you clearly haven’t paid attention to history. Governments around the world have experienced a unique decade where they ran deficits and printed money without “bad inflation” which upsets voters. They think this is a new normal with no consequences. It isn’t. They’re already panicking with the S&P a few ticks from all-time highs. Soon politicians will go into ludicrous mode with fiscal stimulus.

What will fiscal stimulus do to the equity market? I’m reminded of the 1970s—inflation is no friend to most stocks. What happens to trillions in negative yielding long-dated bonds if inflation ticks up? What happens to bond proxies like global large-cap equity indexes or real estate? What happens to risk-parity funds that are leveraged a few times over expecting bonds and equities to increase over time? What if both legs of the trade drop at the same time? No one is ready for inflation, but I believe it’s coming. Maybe not today or next week, but there is a powder keg of monetary supply just waiting to be unleashed by governments who think that inflation can never happen again. At first, markets will cheer a bit of inflation—then they’ll panic. The markets often do whatever the fewest people are positioned for. Who’s positioned for inflation? That’s about as contrarian as buying Argentine sovereign debt.

I think the road-map ahead is a market crash, followed by obscene fiscal stimulus. As always, I’m trying to think a few steps ahead here. I’m making a list of beat-down sectors who benefit from this change in government policy. I want to be ready to buy as soon as they get serious about unleashing the stimulus. You need a crisis that’s severe enough that both political parties can agree on stimulus. We’re not there yet, but we will be. If you thought QE was nutty, wait until you see what drunken sailor mode looks like. Inflation is coming. Be VERY careful if you own assets with duration risk.