We hereby want to inform you that as of last

week friday, our proprietary inflation indicator has switched from a “50%

RISING INFLATION” to a full blown “RISING INFLATION” signal.

At a point in time where disinflation and deflation scare once more seem to be

the name of the game in financial markets, we are receiving an opposing

indication from our inflation signal. We therefore want to take some time to

discuss this signal change and explain our investors how this will impact our

investment strategy.

Our view on the current market environment as well as an elaborate

interpretation of our recent inflation signal signal can be found in the

following document:

The hunt for taxes is moving into high gear in Germany. Prior to 2017, it was possible to buy gold anonymously in quantities up to €15,000. In 2017, this limit was reduced to €10,000. Now, Merkel has drastically reduced this limit to just €2,000 beginning in 2020. Any transaction greater than that amount requires the buyer to prove their identity and give their data to the gold trader.

Martin Armstrong writes in his blog… The Merkel government has been making a concerted effort to introduce a total surveillance state and track the finances of its citizens. There is chaos in Europe with negative and punitive interest rates, high bank charges, and a declining euro. All of this is mixed with a prolonged economic recession in Europe since 2007 as we approach a 13-year decline in 2020. More and more Europeans are looking for ways to safely and anonymously invest their savings, which have been under direct assault by the government. This has been leading to the hoarding of US dollars and now the change in legislation on gold is only going to increase the switch to dollars.

I look at everything from Capital flow point of view and believe fundamentals follow Liquidity or Capital flows. Shift enough Capital into one place and you will start seeing all assets going up irrespective of fundamental valuations..

Martin Armstrong writes in his blog…

Canada will benefit from the capital inflows to North America which will not be as intense as those into the USA because of your government’s punitive actions against foreign investors and its sheer stupidity in understand international trends.

Canadian real estate will be a hedge for an Emerging market investor looking to buy asset which maintain the purchasing value of money.

He further writes… Here is an illustration of our Canadian Real Estate Index in both Canadian dollars and in Chinese yuan. You can see that from the Chinese perspective, Canadian real estate is still rising as a hedge against their currency.

Here is the Canadian Real Estate Index in terms of Euro. Again, we are witnessing breakouts that are stronger in foreign currency than in Canadian. As we head into the Monetary Crisis Cycle, capital flight from Asia and Europe will continue and this will distort the profits they think they are making in real estate not understanding that they are playing the currencies.

Nevertheless, the is all part of the shift from Public to Private assets. While the “real terms” perspective of “value” may not be making new highs in purchasing power, this is still part of the shift from public assets. Some people will buy equities, others will go into real estate, and still others gold or other precious metals. The end game is to divest yourself of public assets and stay away from “fixed rate” investments where you are the creditor. Borrowers should be fixing their loans.

He concludes….The majority of people just look at the price and do not understand that the currency swings can make a bad investment look good. You must always look at this from an international perspective.

We are still miles away from a true bull market in crude. Could that happen? For sure. But the fate of the energy market still lays in front of us. The bulls should temper their enthusiasm.

Yet I am by no means sanguine about the energy market. What am I worried about? I am concerned that a Saudi Arabian military response will cause a crude oil move that would be epic. I am not predicting that by any means, but the one thing I have learned over the decades is that markets can move way more than almost anyone can imagine.

This recent volatility is unusual given the last decade’s muted price action, but make no mistake, further escalation in the Middle-East will result in limit-up moves in crude oil futures.

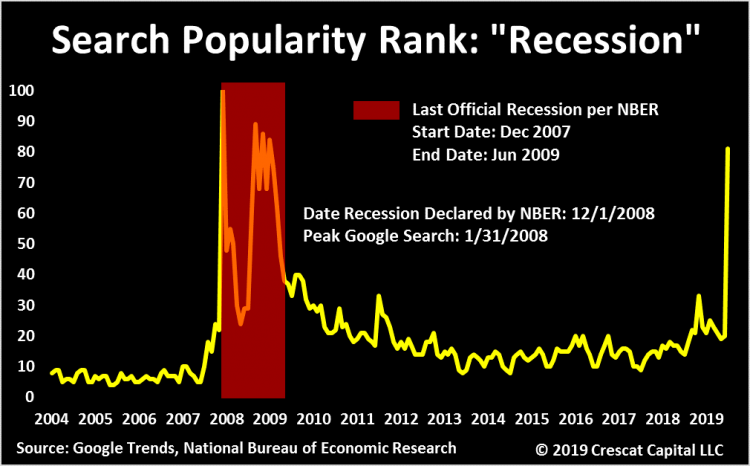

Recessions become self-fulfilling prophesies late in an economic expansion at a point when people finally start believing and acting like one is imminent. It is particularly true when asset bubbles are present. A huge spike in concerns about the economy as measured by Google Trends analysis of the search word “recession” was not a contrary indicator at all at the very beginning of 2008. Indeed, it proved to be the start of the economic contraction. NBER, the official recession-calling body of economics PhDs, did not declare it until twelve months later as typical. We believe the current late-cycle spike in Google recession searches will prove prescient once again.

US and Global Macro Indicators

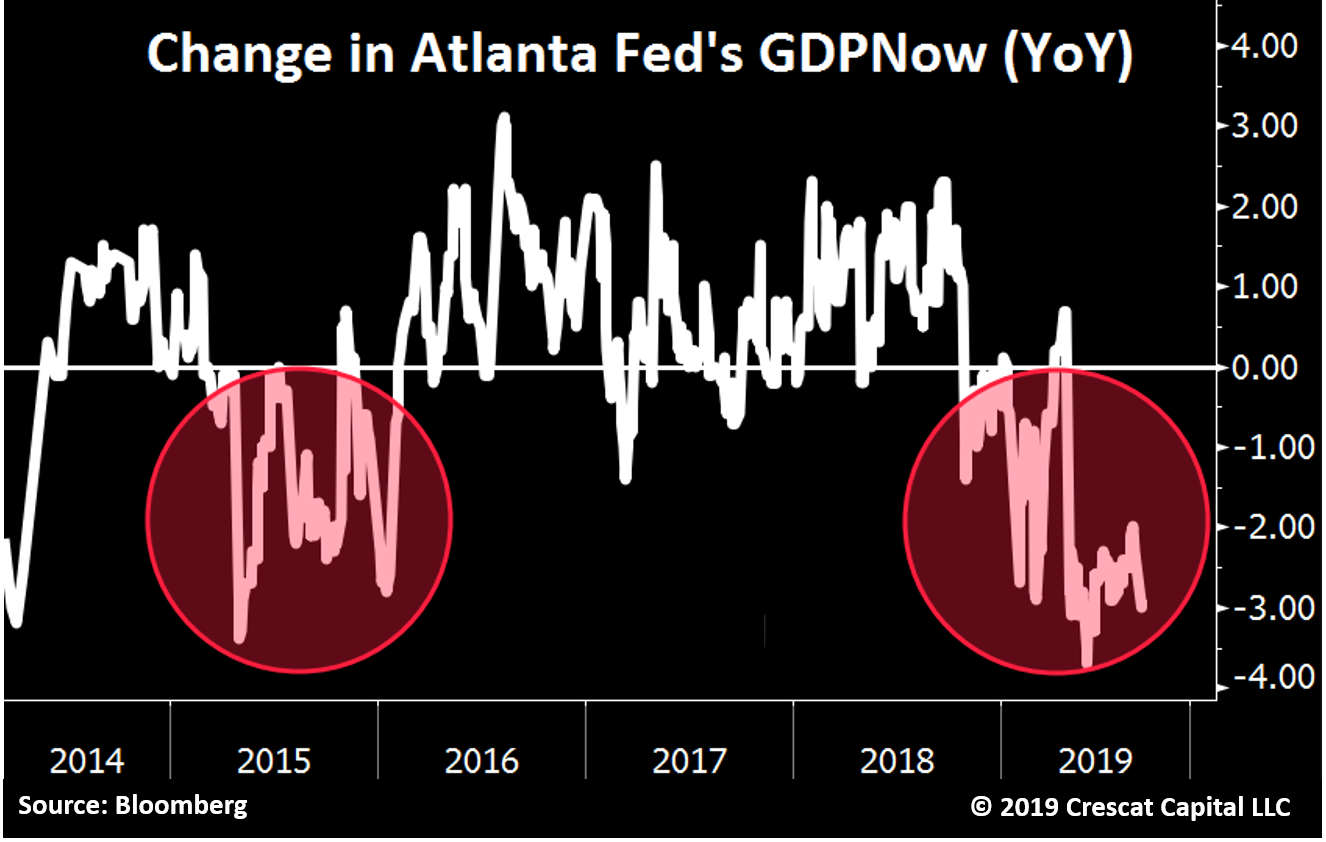

Beware the narrative that the US economy is still strong when it is being spun by conflicted central bankers, politicians, and investment professionals. The truth is that the macro indicators have been turning down materially all year as we can see by the year-over-year change in the Atlanta Fed’s GDPNow macro model.

It’s like in early 2018, when the predominant storyline was “synchronized global growth”. That narrative persisted throughout the year, but global stocks (ex-US) peaked in January. Surveys of global manufacturing purchasing managers have been in decline ever since and have gone into recessionary territory over the last three months.

But the US stock market is still near an all-time high. And today, hand-holding market pundits still cling to the dying notion that the US economy is strong, kept alive by hopes that a new round of Fed easing, the so-called “mid-cycle adjustment” can reverse the deteriorating conditions. Bulls are ignoring deteriorating material macro indicators like the US Bureau of Labor Statistic’s “preliminary” 500,000 jobs reduction for early 2019, the dismal August ISM manufacturing report, and the big drop in last month’s Michigan Consumer Sentiment Index.

The last time US macro data was deteriorating this badly, it was 2015 and several emerging markets went into recession at the same time as the Chinese stock market crashed and its currency began to devalue. US recession was averted after the Fed hiked just once at the end of 2015 then paused for a year. The Fed executed a rare soft landing and the business cycle was extended for more than three years now to what is the longest expansion in US history. But the Fed hiked rates eight more times from December 2016 to December 2018 and engaged in $650 billion of quantitative tightening through May of this year. The economic outlook today is much more foreboding than it was in late 2015, particularly as China is now facing much bigger recessionary pressures of its own.

In the history of the federal funds rate, 1995, 1984, and 1966 were the only mid-cycle adjustments (cuts after hikes) that led to soft landings and extensions of the business cycle. The 2016 pause mentioned above was arguably another. It’s too late in the expansion to work now. Asset bubbles are too big.

We are record late in an expansion in the US with several inversions in the Treasury yield curve having breached levels that historically have a perfect track record of predicting an oncoming recession. These include the 3-month versus 5-year and 10-yr spreads as well as Crescat’s own percentage of inversions indicator. More than 70% of the US yield curve has inverted already in this cycle, a level that has preceded every economic downturn since the 1970s.

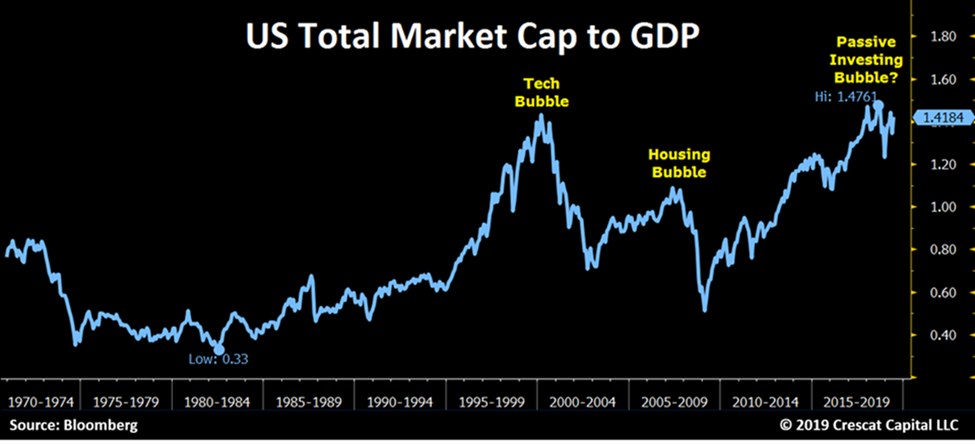

Asset bubbles are much bigger today than they were in late 2015, particularly the US stock market. Michael Burry of Michael Lewis’ Big Short notoriety recently made a call in a Bloomberg interview that we are in a passive indexing bubble that will end like the subprime CDO debacle that led to the global financial crisis. In the history of the Wilshire 5000, the total US stock market index, stocks recently reached their most expensive ever relative to the underlying economy, higher than the peak of the tech bubble in 2000.

We believe based on our macro modeling that 2019 is the downturn that is highly likely to continue into a hard landing. It’s too late for a Fed mid-cycle adjustment to keep the expansion going. That ship sailed post 2015. With the latest excesses in passive investing, the world has reached a level of gross valuation ignorance that could make the coming bear market particularly brutal.

Our composite of macro indicators says that the crash window is open. Recessions are necessary, normal, and inevitable. The longer they are postponed through government intervention, the greater the mal investment, the bigger the speculative bubbles, and the more violent the downturn.

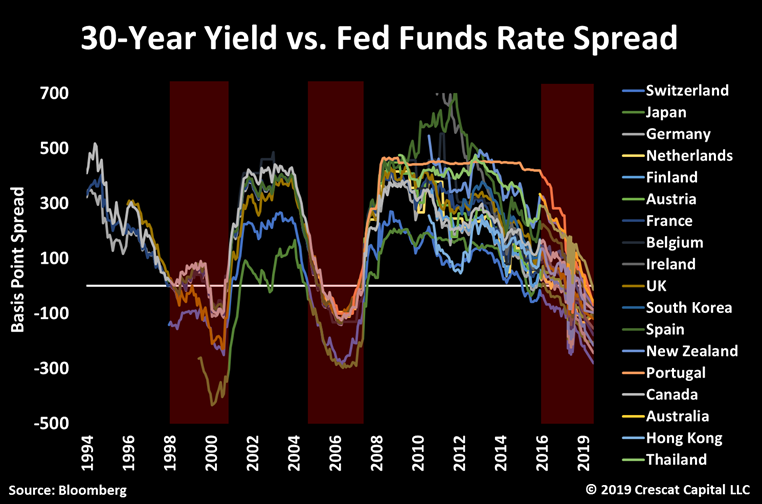

The global yield curve continues to be as inverted as other market peak times. The chart below is just an update of these 18 economies that now have their 30-year yields below the Fed funds rate. Thailand just recently joined the pack. These distortions are just another ominous sign for the global economy.

As history has shown us repeatedly, when the South Korean won breaks down, global stocks tend to follow. The chart below is another macro timing indicator at a critical level today. South Korea heavily relies on exports and its currency is a barometer for financial conditions worldwide. The won is now re-testing a major support line and further depreciation could be detrimental for equity markets globally.

China & Hong Kong

The Chinese economy is at the outset of a debt and currency crisis. No other country has grown debt so aggressively for so long and in such an extreme manner. China built an oversized banking system that now undergoes a rising nonperforming loan problem, a precarious housing bubble, and a political leadership that remarkably resembles a crony-kleptocracy. China’s declining current account problem imperils its entire mercantilist approach, while its push towards a consumer-driven growth model never seemed so far-fetched. Rising social unrest, trade tensions, and food inflation are just icing on the cake for these macro inconsistencies.

The yuan just had its worst month since 1994, even bigger than the 2015 devaluation. We expect much further currency dilution as the PBOC continues to mobilize aid for its failing banking system. We are at the early stages of all these issues. Just this year, the Chinese government was forced to engineer three bailouts: Baoshang Bank, Bank of Jinzhou, and Hengfeng Bank. In aggregate these banks hold close to $420 billion in total assets. Although accounting for a small portion of China’s $42 trillion colossus on-balance-sheet banking system, it’s a sign that the economy is under severe pressure. We expect much larger loan losses to soon surface. According to Bloomberg, China’s central bank recently concluded its first review into industry risk and 420 firms, all rural financial institutions, were considered “extremely risky” and just two received a top rating. China’s debt levels are overwhelming, and a significant currency devaluation is likely on the way.

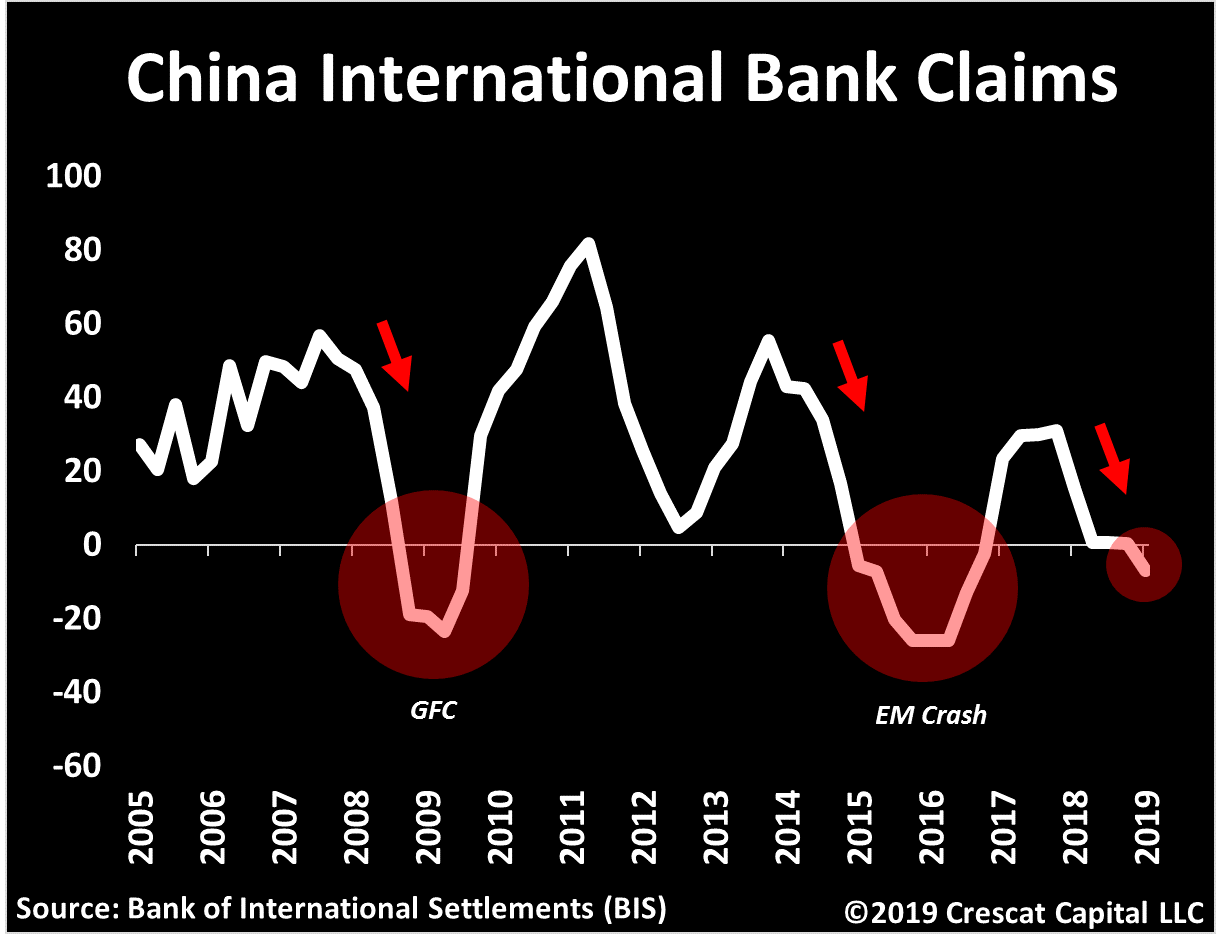

Per the Bank of International Settlements (BIS), China’s total international bank claims have just contracted for the first time in three years reflecting an early warning sign of financial stress. These claims, valued at $920 billion, comprise cross-border transactions in any currency plus local claims of foreign affiliates denominated in non-local currencies. Chinese banking activity similarly faltered during the emerging market crisis in 2015 and the global financial crisis.

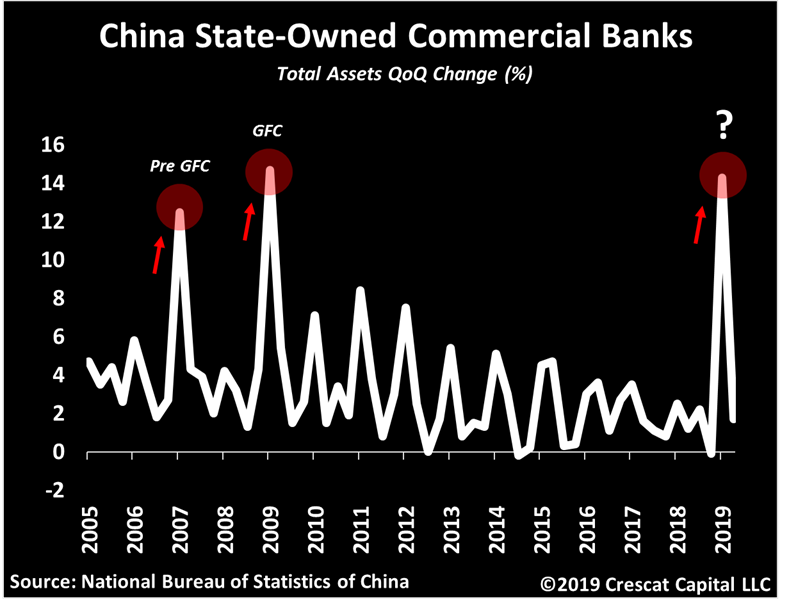

In our previous letters we noted that the median Chinese stock had fallen close to 40% during the 4th quarter of 2018. Since then, the PBOC has attempted to revive its economy through aggressive monetary policies that continue to put downward pressure on its currency to depreciate against the dollar. The Chinese central bank targeted specific forms of liquidity injection, one of them being through its state-owned commercial banks. Their quarterly rate of change in total assets just surged as much as it did times prior to and during the global financial crisis.

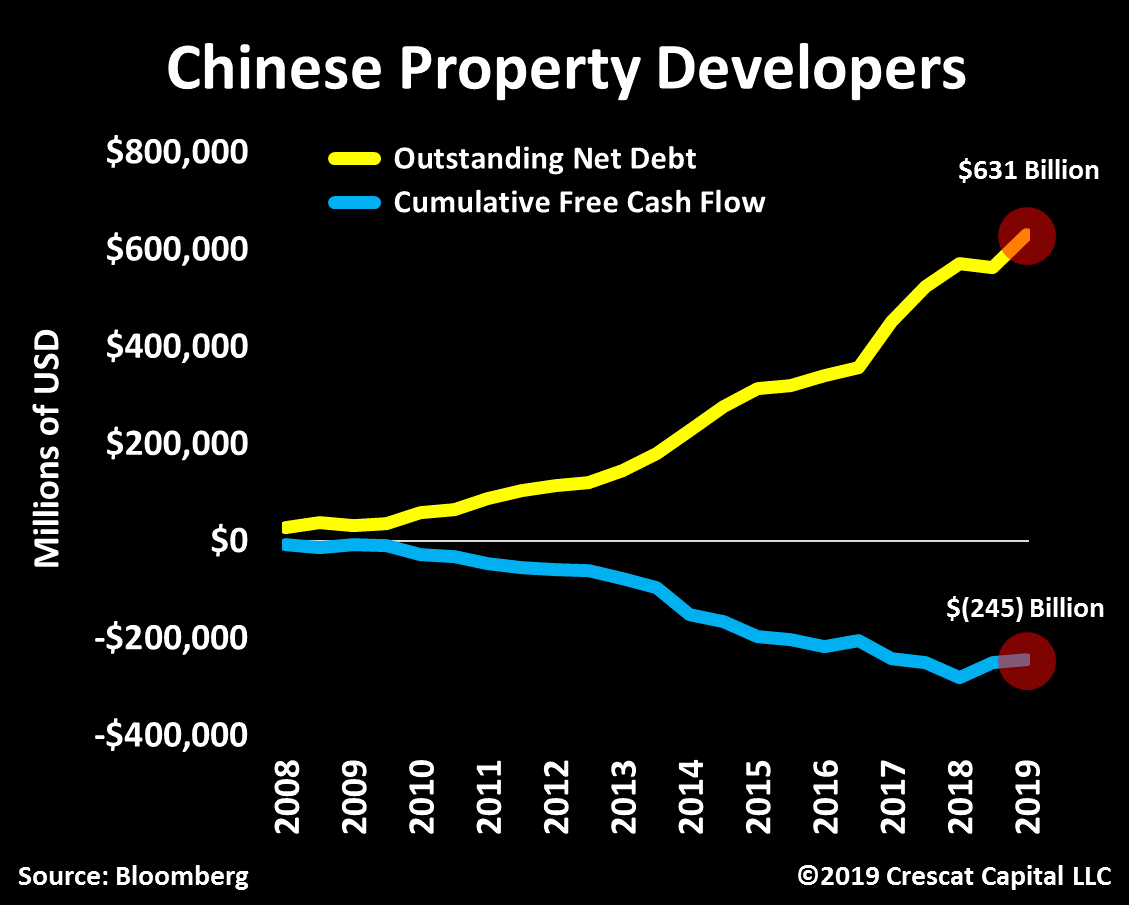

Large sums of investment into non-productive assets, that’s China’s real estate conundrum. Across publicly traded companies, the industry of Chinese property developers and homebuilders is now worth over $1.25 trillion in enterprise value. In contrast however, these businesses only generated about $1.5 billion of free cash flow in the last 12 months, in aggregated terms. Also, close to 55% of Chinese property developers aren’t even profitable on a free cash flow basis, according to their latest report. These companies have now accumulated close to $631 billion in outstanding net debt while total equity value accounts for $585 billion – or equivalent to 108% net debt-to-equity ratio. To put into perspective, that’s the exact same proportion US homebuilders had right at the peak of the housing bubble.

Since 2008, Chinese property developers have accumulated close to $245 billion in free cash flow losses while debt levels continue reaching record levels!

Just recently, we noted China Evergrande, a heavily indebted property developer, reporting that its profits were cut in half, down 52% on a year-over-year basis. Per Bloomberg, 47% of Evergrande’s debt matures this year. The stock is now down 44% in the last 5 months. We think this could be the canary in the coal mine for China’s debt debacle.

China’s sales of commercialized retail and office buildings are down 13 and 10% for the month of June. Its residential market continues to rise, but historically it tends to follow these other two markets closely. It’s important to note that office buildings are now falling the most since the global financial crisis.

House prices in Hong Kong have risen to absurd levels adding to the country’s banking and currency risks. Its secondary residential market is up 40% this year and now valued at over $1,700 per sq. ft.! In our view, these prices are completely unsustainable. Rising mortgage rates, social unrest, political crisis, and capital flight should all be catalysts for a major economic downturn in Hong Kong.

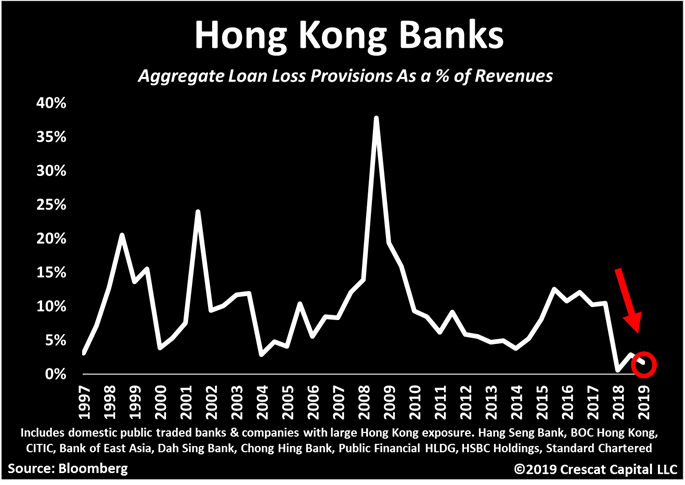

China’s financial gateway to the world is falling apart. Every Hong Kong bank is breaking down from a major support line. Refer to the sequence of charts in the appendix at the very end of this letter. These charts resemble US banks during the global financial crisis when they broke similar trend lines in early 2008 right before the bigger collapse. Hong Kong’s banks are clearly signaling challenging times ahead. We believe capital is fleeing the financial hub portending a likely de-pegging versus the US dollar.

Hong Kong banks are also provisioning only 1.7% of their revenues for loan losses. That’s close to a record low, and even below levels prior to the Asian Crisis. Are HK banks accurately depicting the potential for credit losses? Their historical average is about 12% of revenues.

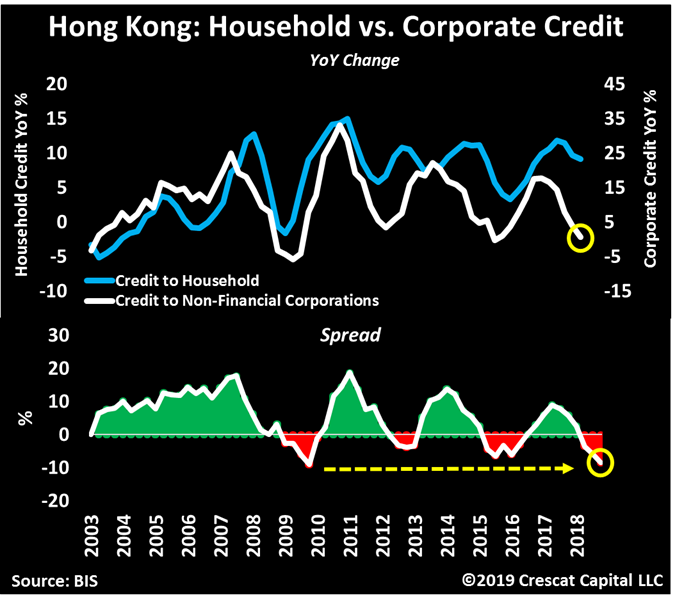

Hong Kong’s corporate and credit growth are also diverging the most since the global financial crisis, another leading indicator of financial stress.

In Conclusion

The truth of asset bubbles and economic weakening matters more than the hope from imminent Fed easing. We believe the global economy along with its many over-valued equity and credit markets are likely to soon head into a severe downturn. The Fed’s polices of near-zero interest rates and quantitative easing since the global financial crisis have created a lack of price discovery in stocks and corporate credit. Investors’ speculative behavior is a natural reaction to cheap money and has played an integral role in inflating these markets. Just as asset prices rise in a positive feedback loop of easy credit, investor speculative behavior, consumer and business spending, so they decline in the opposite self-reinforcing fashion. Such is the natural ebb and flow of the business cycle.

PRINCIPLE NUMBER ONE: THE SHORT-TERM, RISK FREE INTEREST RATE ON U.S. TREASURY BILLS SHOULD NOT BE THE HIGHEST INTEREST RATE IN THE DOLLARIZED WORLD.

An uncontroversial principle of investing is that investors seeking safety should accept lower risks for a lower return, and investors seeking to earn better returns should be willing to take more risks. The yields available on the shortest-term U.S. government debt are those most referred to as the return on the risk-free asset. Greater risks that investors could take to earn higher returns come in many forms, as I explain below.

Just to name a few, examples of such risks that should lead to higher returns include 1) duration, the risk of loaning your money out for a longer period of time, 2) credit, the risk of loaning money to weaker quality debtors, 3) equity, which is after all just another form of credit risk, and 4) illiquidity, the risk of not being able to get your money back immediately. Make no mistake: in investing, you take the risk first. Any potential return you may earn comes only later – after you take the risk.

All the potential higher returns named above come from taking higher risks. Isn’t it logical to assume that investors would want to get compensated for taking those higher risks? Otherwise, after all, why not just own the risk-free asset and earn its lower, but safer, returns? This is where the problem lies today, in our inverted yield curve.

I have always enjoyed Rohit Srivastava’s (Indiacharts) work on markets and he was gracious enough to share some snippets of his Long short report with all of you

He writes

On US Dollar

“The Moment we start discussing the Fed, interest rates, and the reflation trade, we need to look at what the dollar is doing. If anything has me confused in the last few months it has been the dollar. After the dollar hit the 97.50 mark For the first time I started out believing that it would reverse into a 3rd wave decline. However as the currency did not fall right away and made higher highs I changed my view on the dollar and thought it would have a negative impact on commodities and precious metals. While the weakness in commodities has played out precious metals went on to do their own thing on the back of negative real interest rates. Thus watching the dollar was useful in some cases and not in others. The rising dollar did have the negative impact on emerging market stocks and currencies as anticipated. But now after several months the dollar index itself has really not gone that far. Every time it reaches the top end of the range shown by the channel on the chart below sentiment based on the daily sentiment index crosses the 90% marks and becomes over bullish. Each time it has been followed by a small reaction and another attempt to move up. This pattern has repeated this week and we are again at 92% bullish. Having almost touched the top end of the line the case for a falling dollar is back on the table. We are two weeks ahead of the FOMC meeting that is expected to cut rates. The expectation of lower rates has therefore been putting downward pressure on the dollar while the global demand for dollars in a risk off environment has been putting upward pressure on it. Eventually if a weakening US economy does not respond to lower rates immediately or rate cuts are slow at first the market will anticipate more cuts ahead and it could lead to the resumption of the dollar bear market. “

Commodities,Reflation and Stagflation

What I can say however is that commodity prices that were earlier in decline have started to become oversold some of them are already bouncing back and others might follow. This might lead to a near-term reflation trade. At this point we do not know if the Fed will go into overdrive on rates. If it does then the reflation trade could actually have bullish undercurrents for better stocks and cyclicals. Equities respond differently to stagflation and reflation. A reflation trade can be bullish stocks whereas a stagflation trade causes interest rates to go up and pushes down stock prices. In a hyperinflation almost everything goes up and is a completely different scenario. At this stage we should be ready to deal with the first two.

On INR

What concerns us most though is the USDINR That recently broke out above 69 and started a larger 5th wave long-term. We are now in the third wave of that pattern. From July to September we have witnessed wave 1 of 3 and may now pull back in wave 2 of 3. The depth of such a retracement is not clear however once complete the larger up trend should resume. Keeping an eye on short-term momentum indicators might help in finding the turning points. This might also help us pinpoint the next turn in equities. Wave 3 of 5 goes to 82 and wave 5 itself goes to 90 based on fractal analysis.

On GOLD

The chart has a rising channel that stretches all the way up to $ 4000. These are a multi-year trends. On the gold Mcx chart below prices have reached the top end of smaller channel in wave 3 of 5 near 40,000 INR. The larger channel from 1980 stretches all the way to 63,000 INR. In this case I have data only from 1977 and the wave counts are marked accordingly. 5=1 is closer to 135000 INR long term.

“Debt owed by governments, businesses and households around the globe is up nearly 50% since before the financial crisis to $246.6 trillion at the beginning of March” .The only way out is default through Devaluation

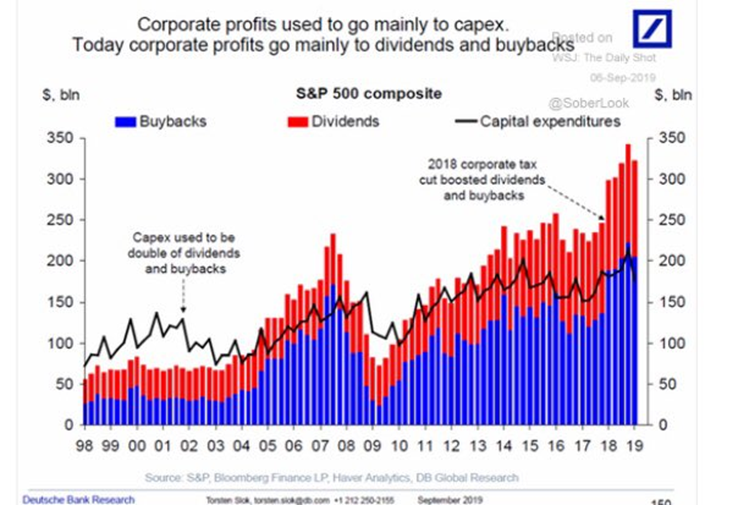

Capex investments, a key driver of future growth expectations have taken a back seat to buybacks and dividends.

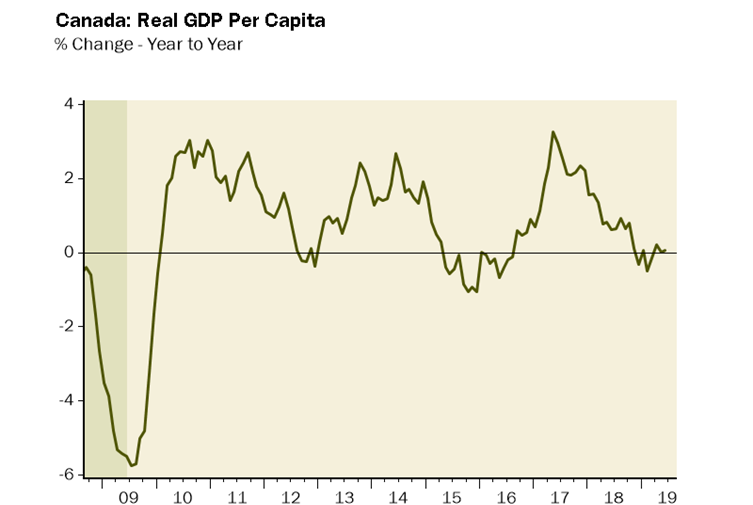

Canadian real GDP per capita growth is ZERO percent over the past year.

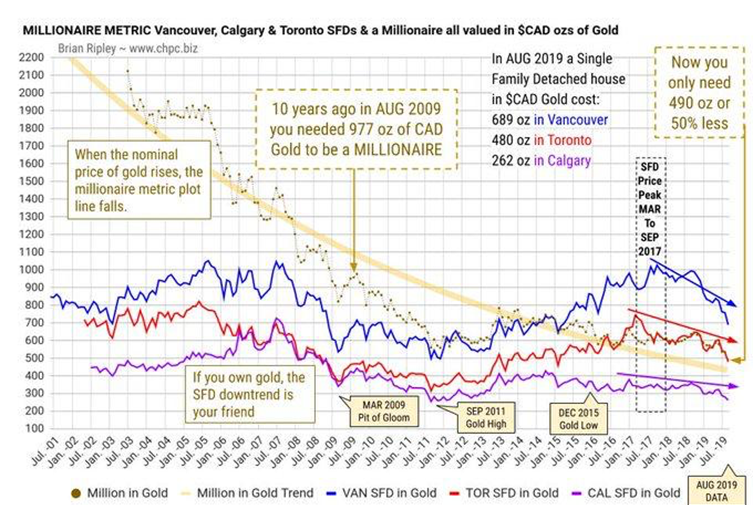

MILLIONAIRE METRIC Vancouver, Calgary & Toronto Single Family Detached and a Millionaire all priced in $CAD Ounces of Gold 10 years ago one needed 977 oz of CAD gold to be a millionaire. Now only 490 oz or 50% less are required.

“The unfortunate backstory is that US department stores are losing

market share as fast as they are downsizing employees, so it still takes 8

employees for $1 mn in sales per year despite job losses. Meanwhile, e-commerce doubled

its share of “core” retail sales in the last 10 years.”

Robin Brooks Chief economist IIF