Rick writes …..Shades of Smoot-Hawley!? Stocks plummeted for the second time in less than 24 hours Monday when Trump signaled to China’s trade negotiators that he means business. A long-delayed, $200 billion hike in tariffs will take effect on Friday because the Chinese reneged on commitments they’d already made. I don’t say they allegedly reneged or that they reportedly reneged, since no one ever believed for a minute that the scumbags were interested in giving the U.S. an honest deal. Why should they want to play fair when their goal is to cultivate trade with Europe, Asia and the rest of the world at America’s expense? It will simply taking them longer now, since, besides raising levies, Trump will take strident measures to thwart China’s epic theft of intellectual property, and push back more aggressively against Beijing’s generous subsidies to key industries

1. The immediate consequence looks likely to be a shift in lending market share from the NBFCs to private sector banks (especially private banks with strong CASA franchises). Given the issues already plaguing the wholesale money market in India (IL&FS, Essel, Debt mutual funds’ challenges, etc) this shift in market share in favour of private banks is already underway. A sustained rise in the US 10-year bond yield could make this shift more long lasting.

2. The medium term consequence looks likely to be a rise in household financial savings (India’s household savings rate has fallen sharply from 25% in FY10 to 17% in FY17) and a drop in discretionary consumption (which has boomed over the last decade). Such a shift could create further issues for sectors like residential real estate and auto. The challenge could also extend to next rung down of discretionary consumption eg. electricals, consumer durables. On the other hand, the rise in household financial savings should help India’s banks (most of whom are struggling to attract deposits).

3. The longer term consequence looks likely to be a drop in the price of land, real estate and fixed assets as the world and India gets accustomed to more expensive capital. (On this issue, my colleague, Salil Desai has written an interesting piece: http://marcellus.in/blogs/marcellus-three-degrees-of-disruption-in-home-buying-in-india/) It is hard to gauge the full consequences of such a readjustment in fixed asset prices. Perhaps it will lead to a renewal of interest of gold as a safeharbour asset. Alternatively, it could lead to greater household financial savings as highlighted in the preceding bullet.

“Every brand, typically on the premium side, has to justify its value to the customer every day. As soon as you’re not the big brand, you’re a niche player”, says Jim Weber who runs Brooks Sports (Bloomberg).

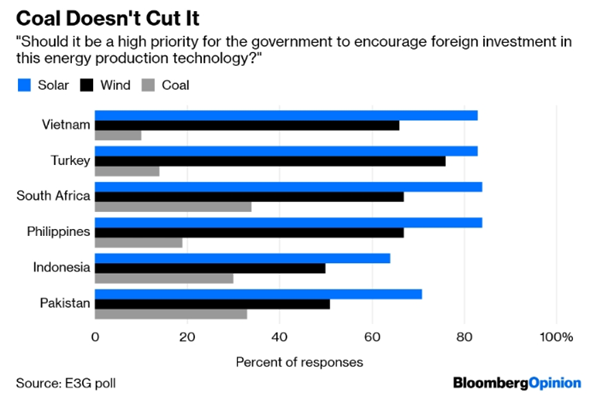

As per Nat

Bullard, “As per study by E3G, polled citizens of the above countries voted for

increased foreign investment in renewable energy followed by fossil fuels.

Public views investment in solar and wind energy as high priority compared to

coal. In economic terms, coal fared poorly w.r.t countries in the survey as

coal trails far behind wind and solar energy in terms of being good for the

economy. Since the beginning of the year, four Asian banks have announced

restrictions on financing new coal plants. Don’t ask leaders or lenders about

coal’s future. Ask the people.”

“The energy sector has the lowest earnings growth rate (-26.2%) of any sector. It is expected to earn $11.3B in 19Q1, compared to earnings of $15.3B in 18Q1. The oil & gas refining & marketing (-57.4%) and integrated oil & gas (-38.1%) sub – industries have the lowest earnings growth in this sector.”

“Nine of 11 sectors anticipate revenue growth for the quarter with energy sector having the weakest anticipated growth compared to 18Q1. The energy sector has the lowest revenue growth rate (-0.8%) of any sector. It is expected to earn $238.0B in 19Q1, compared to revenue of $240.0B in 18Q1.” (Lipper Alpha Insight)

As per

Investopedia, energy infrastructure is a relatively under followed sub – sector

of the broader energy sector. Here is one opportunity if you wish to diversify

your portfolio as buy and sell levels are in well-defined range.

In this

regard, as renewable energy is becoming more affordable, wind energy stocks,

solar energy stocks are placed to give enormous returns in coming years.

Hindustan

Unilever (HUVR) has been trading at 60x earnings multiple. As per Sanjiv Mehta,

Chairman and MD, HUL on Bloomberg, “You must accept that FMCG sector is

recession resistant but not recession proof. At the end of the day, it depends

on money in the hands of consumers.”

When consumer stocks were trading at 35 times

their earnings, S Naren, executive director and chief investment officer at

ICICI Prudential Asset Management Company, considered them expensive. But the

valuations rose to 50-60 times. Interest-rate arbitrage helped consumer stocks

in 2008 and the valuations are so expensive now that there could be a time

correction, Naren said on BQ Edge, BloombergQuint’s on-ground initiative. There

is no clarity that the products made by consumer goods companies can be

replaced because the pace of change is lower in this sector, he said.

S Naren adds, “When you have zero percent

interest rates and you know that in India soap, toothpaste and detergent demand

will go up then it is very easy to bet that this will grow, and you are getting

funding at zero percent. So, you are getting money at zero percent and you are

investing in Indian consumer stocks, you are taking zero percent money to

invest in something which will surely grow.

If you look at power as a sector, do I see in any country’s

electricity being replaced then the answer is no. For the last 10 years, there

has been no returns in most of the power stocks.” But “in the last 10 years,

the demand has gone up 50 percent.”

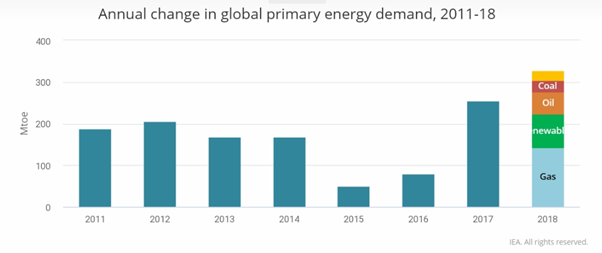

As per IEA, global energy consumption in 2018 increased at nearly twice the average rate of growth since 2010, driven by a robust global economy and higher heating and cooling needs in some parts of the world. Demand for all fuels increased, led by natural gas, even solar and wind posted double digit growth. High electricity demand was responsible for over half of the growth in energy needs.

The demand

for all fuels rose, with fossil fuels meeting nearly 70% of the growth for the

second year running. Renewables grew at double digit pace, but still not fast

enough to meet the increase in demand for electricity around the world, as per

IEA.

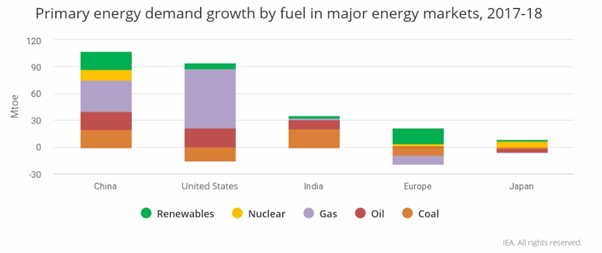

Quoting them further, higher energy demand was propelled by a global economy that expanded by 3.7% in 2018, a higher pace than the average annual growth of 3.5% seen since 2010. China, United States and India together accounted for nearly 70% of the rise in energy demand.

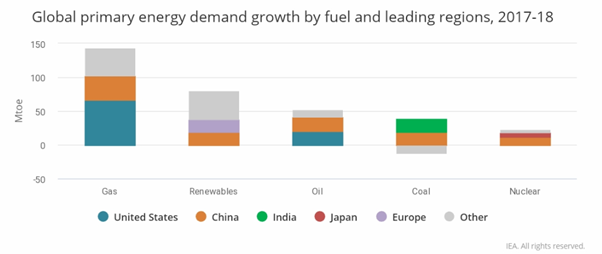

Inputs to the power sector accounted for 95% of China’s growth in energy demand, as generation from all technologies, especially coal, expanded to meet an 8.5% jump in demand for electricity. In 2018, China also had the world’s largest increase in solar and wind generation.

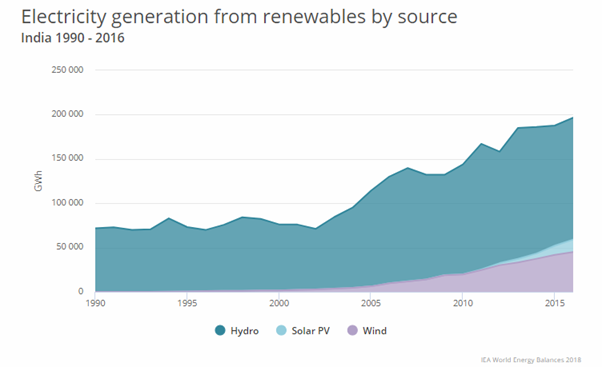

India saw primary energy demand increase 4% or over 35Mtoe, accounting for 11% of global growth, the third largest share. Growth in India was led by coal (for power generation) and oil (for transportation), the first and second biggest contributors to energy demand growth, respectively.

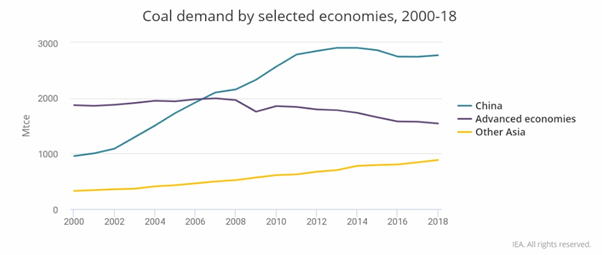

India’s 7% economic growth, the highest among large economies, created strong demand for coal, especially for electricity generation and steel production as India surpassed Japan to become world’s second largest steel producer behind China. New solar and wind capacity met less than a third of the growth in electricity demand, while coal supplied the bulk of additional electricity generation. As a result, coal demand in India grew by around 5%, as per IEA.

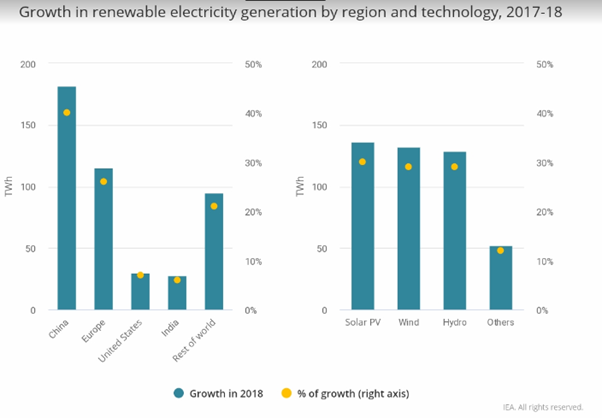

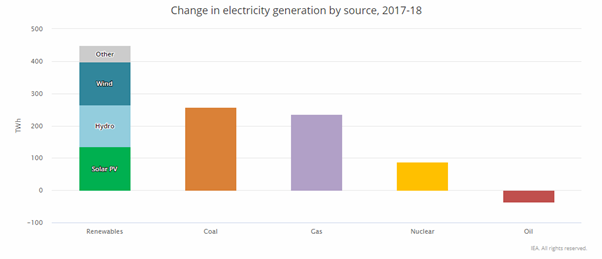

Renewables increased 4% in 2018, the power sector led the growth with renewables based electricity generation increasing by 7% compared to 6% average annual growth rate since 2010. Solar, PV, hydropower and wind each accounted for about a third of the growth with bioenergy accounting for majority of the rest. Together, renewables were responsible for almost 45% of the world’s increase in electricity generation. They account for almost 25% of global power output, second after coal, as per IEA.

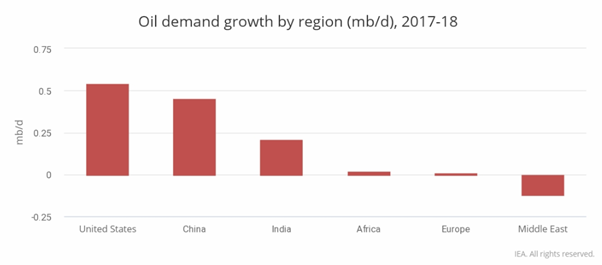

Global oil demand growth slowed down in 2018 as higher oil prices partially offset robust economic activity around the world. Indian oil demand grew 5% in 2018 compared to 2017, a year when demand was lower due to implementation of GST and demonetisation. However, the sharp increase in oil prices in 2018, amplified by currency deterioration, contributed to slowing growth in second half of the year. Rapid industrialisation and fast pace of growth in vehicle fleets have caused severe air quality problems and policies are being put in place to try to tackle the problem, as per IEA.

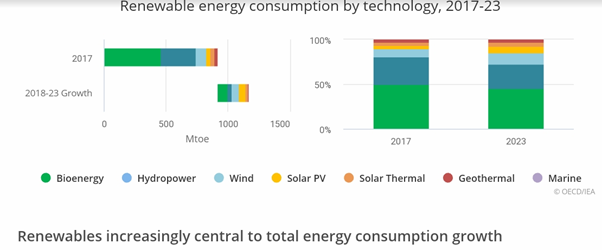

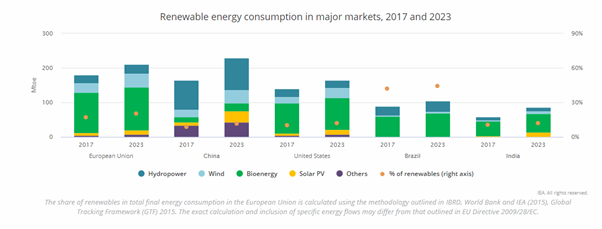

The share of renewables in meeting global energy demand is expected to grow by one-fifth in the next five years to reach 12.4% in 2023. Renewables will have the fastest growth in the electricity sector, providing almost 30% of power demand in 2023, up from 24% in 2017. During this period, renewables are forecast to meet more than 70% of global electricity generation growth, led by solar PV and followed by wind, hydropower, and bioenergy. Hydropower remains the largest renewable source, meeting 16% of global electricity demand by 2023, followed by wind (6%), solar PV (4%), and bioenergy (3%), as per IEA.

Solar PV alone represents half of the additional growth in the accelerated case forecast. Driven by faster cost reductions that make the technology more competitive globally, annual additions are expected to reach 140 GW by 2023. Commercial, residential, and off-grid PV applications together account for most of the extra growth, which indicates untapped potential in these segments, especially in China, India, Europe and Latin America.

As per IEA, renewables and nuclear power met a majority of the increase in power demand.

India’s power demand

increased by around 65 TWh, or 5.4%, a slower rate than the previous year. The

increase was driven by higher demand in buildings, especially coming from air

conditioning, as well as higher access to electricity. Last year, India

completed the electrification of all its villages, with electricity

connections extended to around 30 million people in the last 2 years, as per

IEA.

However, this expansion is not all rosy.

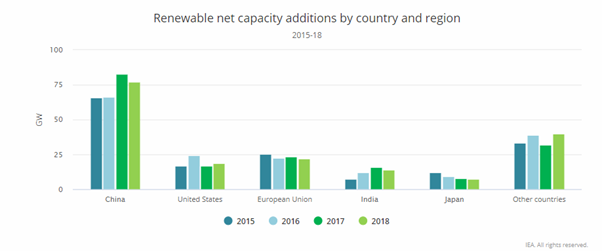

As per IEA, After nearly two decades of strong

annual growth, renewables around the world added as much net capacity in 2018

as they did in 2017, an unexpected flattening of growth trends that raises

concerns about meeting long-term climate goals.

Last year was the first time since 2001 that growth in renewable power capacity failed to increase year on year. New net capacity from solar PV, wind, hydro, bioenergy, and other renewable power sources increased by about 180 Gigawatts (GW) in 2018, the same as the previous year, according to the International Energy Agency’s latest data.

“The world cannot afford to press “pause” on

the expansion of renewables and governments need to act quickly to correct this

situation and enable a faster flow of new projects,” said Dr Fatih Birol, the

IEA’s Executive Director. “Thanks to rapidly declining costs, the competitiveness

of renewables is no longer heavily tied to financial incentives. What they

mainly need are stable policies supported by a long-term vision but also a

focus on integrating renewables into power systems in a cost-effective and

optimal way. Stop-and-go policies are particularly harmful to markets and

jobs.”

Since 2015, global solar PV’s exponential

growth had been compensating for slower increases in wind and hydropower. But

solar PV’s growth flattened in 2018. The main reason was a sudden change in

China’s solar PV incentives to curb costs and address grid integration

challenges to achieve more sustainable PV expansion. Moreover, lower wind

additions in the European Union and India also contributed to stalling

renewable capacity growth in 2018, as per IEA.

“These 2018 data are deeply

worrying, but smart and determined policies can get renewable capacity back on

an upward trend. We are helping all 38 members of the IEA Family, and all other

countries around the world, in their energy transitions with targeted policy

advice aimed at accelerating investment in a global portfolio of renewable

energy technologies, as well as energy efficiency, carbon capture, utilisation

and storage, and all other clean-energy technologies,” said Dr Birol.

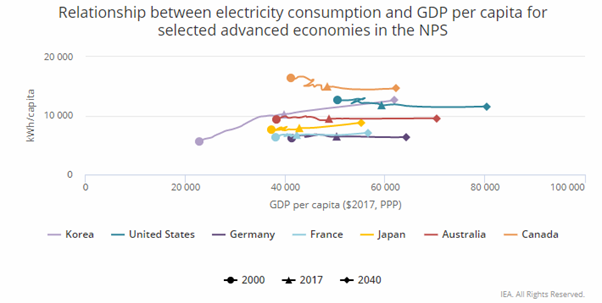

Population growth in many advanced economies is barely exceeded by electricity demand growth, meaning that further growth in GDP per capita does not lead to an increase in electricity demand per capita (as an exception, the industry sector in Korea accounts for a large share of electricity demand, and so it is one of the few advanced economies that sees industry contribute to overall electricity demand growth on a per capita basis), as per IEA.

Investors

should be cautious when it comes to purchasing a stock to reap dual benefits of

capital appreciation and growth in value of the company hence high multiples.

Exposure of a portfolio should be diverse and a constant scan of the market is

essential to enter at budding stage and exit when the growth is over expanding.

Those who are value investors and want to remain invested for a long time

should also search for opportunities when they could enter a segment so as to

witness a sectors’ complete growth.

Conclusion in simple words , it is high time Indians diversify out of their comfort zone and start looking into other places!

This is getting interesting and probably the reason that investors are preferring to invest in financial markets rather than real economy.

Wolfstreet writes .. More and more companies either choose not to invest in other countries or are prevented from doing so.

Global foreign direct investment flows plunged by another 27% in 2018, to just $1.1 trillion, the equivalent of 1.3% of global GDP, the lowest level since 1999, according to new data released by the OECD. The plunge was the fourth consecutive annual fall in global FDI flows, as more and more companies either choose not to invest in businesses or assets in other countries or are prevented from doing so.

Investing is now a commodity. If you think differently, you’re in denial. Take a look around, the market is flooded with investment products and platforms capable of getting you properly invested for little to no cost at all. It’s true. You can own a fully diversified portfolio of mutual funds for free.

Obviously, not everyone invests on their own or for free. There are billions upon billions of dollars currently invested with online platforms, called robo advisors, and with investment professionals. Generally, for a fee that’s based on the value of your account, either one can manage your for you

These are the three ways you can invest. Period. You can do it on your own or outsource it to a human or computer based intermediary. One method isn’t necessarily better than the other. Each option carries its own advantages and disadvantages, and I believe it’s important for you understand what those are.

The bullish narrative for U.S. equity risk makes sense only if one accepts a narrative that the Fed will proactively move to prevent a U.S. slowdown before it happens.

The bullish narrative further presumes that the current global slowdown will somehow miraculously reverse or somehow not touch U.S. growth. (We have argued that U.S. growth will fade alongside its developed market peers as the benefits of the tax cuts wane). With the exception of Japan, central banks generally have been and remain reactive rather than proactive. Before central banks act preemptively using a Japanese-style modern monetary theory (MMT) approach, two things must happen. First, they must lose their relatively well-defined, current mandates. Second, they must lose their independence. We don’t expect this to happen to the Fed until after the next risk repricing is complete. Thus, even though Fed Funds futures markets remain convinced of a cut at well over a 60% probability, market participants ought to be more skeptical.

Not many talk about it, yet, but the first and biggest driver of the risk off last year, was the EM FX space.

JPM EM FX index taking new recent lows. We have not closed this low in a very long time (the market ear). India Rupee always reacts Late

With commodities trading as they are, it is reflected in Australian Dollar

Maybe a spill over to China etc?

Watch the huge 0.7 level in the AUD carefully.

MSCI World ex Fang 6 goes nowhere. Question: Fangs 6 have increased almost 40% in value in the last 16 months, but who is on the loosing side of this coin.

The 30 year – 5 year Treasury yield has steepened by 0.4% in the past 7 months. Over the past 20 years, this happened: September 2000 August 2007 September 2015 Now (Tony Bombardia)

Ever since the first major outbreaks of Euro$ #4 last year, the balance of data has tipped further and further toward the minuses. Yesterday was a big one. US income growth in 2019 is no longer growth. Not huge declines, but minus signs where, if the prior boom narrative had been valid, large plus signs should rule unchallenged.

The business cycle used to be relatively easy and intuitive. A recession shows up, the economy quickly, violently plunges, and then just as fast back to normal. The whole thing wrapped up in a year, maybe a year and a half for the nastier ones. It isn’t fun, but everyone knows the score.

What we’ve witnessed since Euro$ #1, what people still call the Great “Recession”, is an elongation of not business but these monetary cycles and what they do to the global economy. There had always been a transition period before, these today are now almost phases unto themselves. Extended periods of economic gray.

Canada provides us with another good example. Today, that country’s government reports GDP in February 2019 was just slightly less than it was in January. According to StatCan, real output declined 0.1%. By itself, no big deal. Certainly not outright recession.

The rate was +0.3% growth in GDP during January. But there were also minus signs in three of the prior four months. February makes four negatives out of the last six. Definitely not boom, maybe not recession though perhaps an elongated transition toward one. Very much gray.

Authored by Dagny Taggart via the organic pepper blog

Experts have been warning us about potential dangers associated with artificial intelligence for quite some time. But is it too late to do anything about the impending rise of the machines?

Once the stuff of far-fetched dystopian science fiction, the idea of robot overlords taking over the world at some point now seems inevitable.

The late Dr. Stephen Hawking issued some harsh and terrifying words of caution back in 2014:

The development of full artificial intelligence could spell the end of the human race. It would take off on its own, and re-design itself at an ever-increasing rate. Humans, who are limited by slow biological evolution, couldn’t compete, and would be superseded. (source)

Elon Musk, the founder of SpaceX and Tesla Motors, warned that we could see some terrifying issues within the next few years:

The risk of something seriously dangerous happening is in the five year timeframe. 10 years at most. Please note that I am normally super pro technology and have never raised this issue until recent months. This is not a case of crying wolf about something I don’t understand.

The pace of progress in artificial intelligence (I’m not referring to narrow AI) is incredibly fast. Unless you have direct exposure to groups like Deepmind, you have no idea how fast — it is growing at a pace close to exponential.

I am not alone in thinking we should be worried.

The leading AI companies have taken great steps to ensure safety. They recognize the danger, but believe that they can shape and control the digital superintelligences and prevent bad ones from escaping into the Internet. That remains to be seen… (source)

Experts say it is time to study “machine behavior.”

Last week, a team of researchers made a case for a wide-ranging scientific research agenda aimed at understanding the behavior of artificial intelligence systems. The group, led by researchers at the MIT Media Lab, published a paper in Nature in which they called for a new field of research called “machine behavior.” The new field would take the study of artificial intelligence “well beyond computer science and engineering into biology, economics, psychology, and other behavioral and social sciences,” according to an MIT Media Lab press release.

Scientists have studied human behavior for decades, and now it is time to apply that kind of research to intelligent machines, the group explained. Because artificial intelligence is doing more collective ‘thinking,’ the same interdisciplinary approach needs to be applied to understanding machine behavior, the authors say.

“We need more open, trustworthy, reliable investigation into the impact intelligent machines are having on society, and so research needs to incorporate expertise and knowledge from beyond the fields that have traditionally studied it,” said Iyad Rahwan, who leads the Scalable Cooperation group at the Media Lab.

Machines are making decisions and taking action without human input.

Rahwan explains:

“We’re seeing the rise of machines with agency, machines that are actors making decisions and taking actions autonomously. This calls for a new field of scientific study that looks at them not solely as products of engineering and computer science but additionally as a new class of actors with their own behavioral patterns and ecology.” (source)

“We’re seeing an emergence of machines as agents in human society; these are social machines that are making decisions that have real value implications in society,” says David Lazer, who is one of the authors of the paper, as well as University Distinguished Professor of Political Science and Computer and Information Sciences at Northeastern.

We interact numerous times each day with thinking machines, as the press release explains:

We may ask Siri to find the dry cleaner nearest to our home, tell Alexa to order dish soap, or get a medical diagnosis generated by an algorithm. Many such tools that make life easier are in fact “thinking” on their own, acquiring knowledge and building on it and even communicating with other thinking machines to make ever more complex judgments and decisions—and in ways that not even the programmers who wrote their code can fully explain.

Imagine, for instance, a news feed run by a deep neural net recommends an article to you from a gardening magazine, even though you’re not a gardener. “If I asked the engineer who designed the algorithm, that engineer would not be able to state in a comprehensive and causal way why that algorithm decided to recommend that article to you,” said Nick Obradovich, a research scientist in the Scalable Cooperation group and one of the lead authors of the Nature paper.

Parents often think of their children’s interaction with the family personal assistant as charming or funny. But what happens when the assistant, rich with cutting-edge AI, responds to a child’s fourth or fifth question about T. Rex by suggesting, “Wouldn’t it be nice if you had this dinosaur as a toy?”

“What’s driving that recommendation?” Rahwan said. “Is the device trying to do something to enrich the child’s experience—or to enrich the company selling the toy dinosaur? It’s very hard to answer that question.” (source)

There is still a lot we don’t know about how machines make decisions.

What hasn’t been examined as closely is how these algorithms work. How do they evolve with use? How do machines develop a specific behavior? How do algorithms function within a specific social or cultural environment? These issues need to be studied, the group says.

There is a significant barrier to the type of research the group is proposing, however:

But even if big tech companies decided to share information about their algorithms and otherwise allow researchers more access to them, there is an even bigger barrier to research and investigation, which is that AI agents can acquire novel behaviors as they interact with the world around them and with other agents. The behaviors learned from such interactions are virtually impossible to predict, and even when solutions can be described mathematically, they can be “so lengthy and complex as to be indecipherable,” according to the paper. (source)

And, there are ethical concerns surrounding how AI makes decisions:

Say, for instance, a hypothetical self-driving car is sold as being the safest on the market. One of the factors that makes it safer is that it “knows” when a big truck pulls up along its left side and automatically moves itself three inches to the right while still remaining in its own lane. But what if a cyclist or motorcycle happens to be pulling up on the right at the same time and is thus killed because of this safety feature?

“If you were able to look at the statistics and look at the behavior of the car in the aggregate, it might be killing three times the number of cyclists over a million rides than another model,” Rahwan said. “As a computer scientist, how are you going to program the choice between the safety of the occupants of the car and the safety of those outside the car? You can’t just engineer the car to be ‘safe’—safe for whom?“ (source)

The researchers explain that it will take experts from a host of scientific disciplines to study the way machines behave in the real world, as a press release from Northeastern University states. “The process of understanding how online dating algorithms are changing the societal institution of marriage, or determining whether our interaction with artificial intelligence affects our human development, will require more than just the mathematicians and engineers who built those algorithms.”