Nick writes on an interesting topic which is a taboo in our society..”MONEY”

One advisor told me a story about the time they were having a one-on-one with the grandson of a billionaire when the grandson told them, “I won’t view myself as being successful unless I, independently of family connections, make a billion.” The advisor said that this was a common problem in ultra-high net worth (UHNW) families, who make risky investment decisions in hopes of solidifying their own independent fortunes.

I had another advisor reach out and tell me about the difficulty of discussing the cost of fertility treatments with middle-aged couples who wanted children. They stated:

So let’s start on the low end, freezing sperm and eggs. That’s roughly $500/year (sperm) – $10,000 (eggs). Then, if you want to try fertility treatments, it can be $5,000-$10,000 per treatment. If you have multiple treatments and iterations? Some couples spend $50,000 on pregnancy, most of which is not going to be covered by insurance.

If you think talking about money is hard, imagine trying to discuss this and your client’s impending decline in fertility.

There was the man who recounted how his business partner’s tax problems with the IRS almost cost him his advisory business. The IRS threatened to send a letter to all of his clients unless they got a monthly payment to pay off the partner’s tax liabilities. Long story short, the man was able to create a new company and move over his clients while ending the relationship with his deadbeat business partner. Morale of the story: Run a credit check on someone before you start a company with them.

Another common theme in the messages I received was how difficult it was to deal with money and family. One advisor, who was managing his parents’ money, found it hard to get his parents to agree to the same spending plan. Another advisor confessed that he had so much difficulty trying to make financial decisions with his wife that he had to hire an outside financial planner to make the process easier.

Nick writes…. Why Personal Finance is a Bit Too…Personal

Though you have probably never heard of Wally Jay, he is considered one of the greatest judo instructors of all time. Despite never once competing in judo (only in jiujitsu), Jay consistently produced champions in judo and other martial arts. One of Jay’s key insights was that not everyone learned like he did:

The biggest mistake is for an instructor to teach exactly the way he was taught. Once a teacher said to me, “All of my boys fight like me.” Then when we got on the mat, not one of his students could beat one of mine. Not one. So I told him that he had to individualize his instruction.

This lesson seems to be lost on many financial commentators/bloggers who provide personal finance advice based on their own experiences, which are typically outside the norm. The exceptions become the rule and then personal finance becomes a bit too…personal. I am reminded of the words of Richard Hamming:

Please remember that what made you great is not appropriate for the next generation.

In this post Sam breaks down his journey to $1 million by age 28. If you don’t have time to read the whole thing, the summary comes down to: have one incredible lucky trade in the Dot Com bubble (make 50x), earn a boat load of money in finance, and live a relatively frugal lifestyle. And for his age, Sam was making a “boat load” of money.

500 Startup’s innovation

director, global ambassador and mentor for Vital Voices, multi-lingual and Argentine

tango dancer, Vera Futorjanski, also shakes a leg with almost 40% of world

nations as global investor and believer of better returns from investing in

emerging markets with those having gender inclusive culture, allocating about 26%

of investments in at least one female founder company relying on the research which

proves such start-ups outperforming by 63% than those with exclusive male

teams. However, a shocking truth as per TechCrunch is, only 2% of US VC dollars

go to women led start-ups. Vera Futorjanski encourages more women to tap into

VC space.

Investing icon & BRK.A

controller since 1964, having more than $100 billion annually invested in

factor focused products, Warren Buffett, have created immense value for

shareholders even in high volatility environment due to implied leverage.

Analysis suggest that BRK.A’s positive exposure to value, size, low volatility

& quality factors and negative exposure to growth and dividend yield have

consistently outperformed S&P 500 clearly demonstrating his unprecedented

skills in selecting factors, constructing a multi factor portfolio and adapting

the factor mix overtime.

There are now more than 70

times as many indexes as there are stocks globally, investors new preferred

destination, ‘indexed annuities’ sales for 2018 rose 27% YoY to a record of

$69.6 billion as per LIMRA. However, investors are reminded of three important

factors, first, they track rules based trading strategies designed to manage

asset class exposure as means of maintaining a set volatility target, second, performance is often calculated net

of servicing cost & on an excess return basis and lastly, live &

simulated returns may be conflated in annuity illustrations and marketing

material, for which NAIC Working Group has proposed doubling from 10 to 20

years as the minimum amount of time an index or its constituents must exist for

it to be used in annuity illustrations and GIPS recommends performance be

provided to clients, prospects or consultants who have sufficient experience

and knowledge.

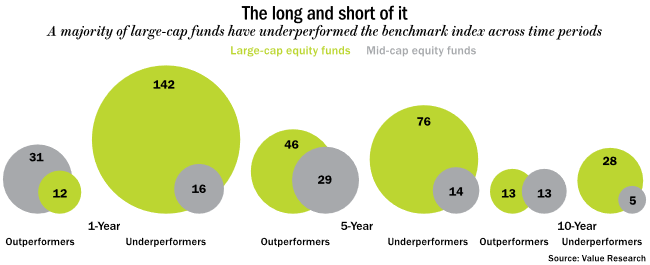

Kripa Mahalingan writes “ “Playtime is up for asset management companies, who have been designing imaginative schemes, as SEBI steps in with new regulations. Now it is time for fund managers to colour within the lines “

Outlook money presents us with the following chart:

Indian Portfolio managers will obviously want to defend their turf but the advancement is technology has taken away the asymmetry in information and democratized the information which is slowly getting priced at or moving quickly to ZERO.

This is quite evident in the performance of actively managed large cap funds where underperformance percentage in both short term and long term is quite stark.

Even among midcaps funds,almost 30% of funds are not beating the benchmarks over 5 year period and most of the this underperformance has come about due to change in regulations and narrowness of this rally during last three years.

This is no different than US where 5 stocks have contributed to 30% of S&P returns over last 3 years.

Investing environment

The world is slowly moving towards oligopoly and this market concentration among few players is also leading to concentration in market share and profitability. This is quite evident in US and as Jonathan Tepper writes in The Myth of Capitalism “tells the story of how America has gone from an open, competitive marketplace to an economy where a few very powerful companies dominate key industries that affect our daily lives. Digital monopolies like Google, Facebook and Amazon act as gatekeepers to the digital world. Amazon is capturing almost all online shopping dollars. We have the illusion of choice, but for most critical decisions, we have only one or two companies, when it comes to high speed Internet, health insurance, medical care, mortgage title insurance, social networks, Internet searches, or even consumer goods like toothpaste. Every day, the average American transfers a little of their pay check to monopolists and oligopolists”.

India is also following the same path of capitalism and it would be reasonable to assume this will lead to profit and market concentration. This environment of ” WINNERS TAKE ALL ” requires a paradigm shift in thinking by fund managers if they hope to beat the benchmarks. The other headache is Value vs Growth with growth outperforming value for so long that most active fund managers have become growth fund managers and do not hesitate to justify the overvalued growth stocks.

I think a combination of market concentration and growth investing mentality is going to make life tough (and not easy) for most active fund managers and although nobody can predict the future, I will hazard a guess that active portfolio managers underperformance is going to get more stark in this brave new world of oligopolies and tricky economic environment.

Philip Grant writes for Almost Daily Grant…China’s Shanghai Composite fell by nearly 2% today, following a Friday statement from the politburo describing first quarter economic conditions as “generally stable and better than expected.” Of course, an abundance of new credit figures prominently in that better than expected start to 2019, as total new financing expanded by an amount equal to 9% of last year’s GDP, rivaling the full-year pace of 2009’s massive economic stimulus (Almost Daily Grant’s, April 12).

The politburo statement potentially

signifies that the burst of credit growth will be soon abating. Dai Ming, fund

manager at Hengsheng Asset Management Co., told Bloomberg that “people have

come to a clear consensus that there won’t be any aggressive stimulus that

floods the economy with excessive liquidity, indicating limited room for

valuation recovery.” Valuations have already been fattening. Even after

yesterday’s pullback, the Shanghai Composite has been the best performing stock

market in the world, up 29% year-to-date.

As Beijing hints that it may tap the

monetary brakes, China’s corporate sector races to raise cash. Bloomberg

relays today that since January, nine companies have announced plans to issue

rights offerings totaling RMB 40.5 billion ($6 billion), more than double the

full-year 2018 figure. Anne Stevenson-Yang of J Capital Research concurs,

noting in a report today that 200 Chinese firms have conducted initial public

offerings across the local A-share, Hong Kong and U.S. markets over the past 12

months, as companies look “to grab everything that is not nailed down.”

Stevenson-Yang cautions that financial shenanigans are particularly prevalent

among this cash-raising cohort:

Investors know well—or should

know—that fraud is thick on the IPO playing grounds in China, and the

incentives to generate nosebleed valuations by fraudulent means are core to the

playbook. After all, there are no penalties in China for committing securities

fraud in the U.S., where Chinese authorities believe U.S. regulators should

look out for their own.

As we recently reported, three

insiders at UXIN Ltd., an online dealer and financier of used cars that listed

in the U.S. at the end of June last year, managed to take home around $450

million in cash before lock-up had even expired. Listing in an overseas market.

. . is the lowest-risk way known to man of robbing a bank.

Among the tricks

employed by Chinese IPO candidates to achieve more favorable valuations:

Making up profits and, then, overstating capital expenditures to explain away

the lack of cash on the balance sheet, generating revenues by selling products

below cost (i.e. the Uber model) and using up-front fees generated from a

franchise network business model to goose gross revenues on a one-time

basis.

Alternative investments are characterised by high leverage, more illiquid and subject to less regulation. Countering with the argument that make acquiring companies through debt illegal a valid point? Or is it that in this business, taking Sears in focus, political corruption exists? Or would one blame neither of the firms in transaction, but the ‘enablers’? Does this all boils down to flow of capital in Wall Street with such ease caused the ‘damage’ leaving big banks happy and reduced liquidity in debt markets will be a boon or bane to them?

As conceptual check, LBO managers seek to add value

– from improving company operations and growing revenue and ultimately

increasing profits and cash flows. The potential returns are to a large extent

due to the use of leverage. If debt financing is unavailable or costly, LBOs

are less likely to occur. A buyout deal may use a combination of bank loans

(leveraged loans) and high yield bonds. In Leveraged Buyouts, assets of the

target company serves as collateral for the debt and the cash flows of the

target company are expected to be sufficient to service the debt. The debt

becomes a part of the capital structure of the target company if the buyout

goes through making the target company after the buyout a privately owned

company.

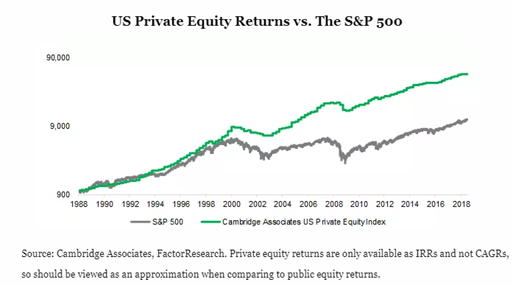

The goal for private equity is to improve new or underperforming businesses and exit them at higher valuations, so the holding period could be from 6 months to over ten years. Although private equity funds diversify your portfolio, in short term, it may not provide returns above stocks but holding it for a longer term like shown for 20 years, private equity funds outperform. (However, PEPI isn’t a reliable measure and in absence of liquid market, investments may not be marked to market.)

American Investment

Council, “Private equity continued its ability to generate the highest

long-term returns, net of fees, for investors, according to the American

Investment Council’s (AIC) Performance Update Report 2016 Q3, released today.

“Private equity

prioritizes a long-term approach, rather than focusing on short-term gains,”

said AIC President and CEO Mike Sommers. “This approach is why no other

investment strategy can compete with private equity over a 10-year horizon,

especially the public markets.”

The report found that annualized private equity investments over the 3- and 10-year time horizons outperformed the Russell 3000 index by 0.7 percent and 3.3 percent, respectively. Private equity also outpaced S&P 500 total returns over a 10-year time-frame, generating 10.7 percent annualized profit for investors.”

According

to the Spectrem Group’s 2010 study of American investors with assets greater

than $25 million, more than half have allocations to hedge funds, private

equity and venture capital with 20 percent of total portfolio allocated to

alternative investments. The increasing interest by institutions and high net

worth individuals in alternative investments has resulted in significant growth

in each category since the beginning of 2000. The Private Equity Council

estimated that private equity leveraged buyout deals were approximately $720

billion in 2007 compared with $100 billion in 2000.

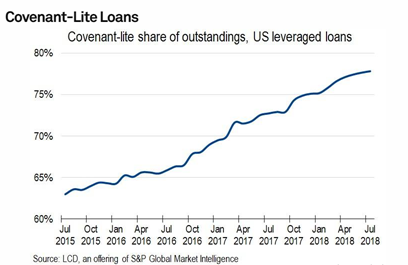

One of the key differences between leveraged loans and bonds is that leveraged loans are generally senior secured debt and the bonds are unsecured in case of bankruptcy. Therefore, even given covenants, because of the amount of leverage employed, the bonds issued to finance the LBO are usually high yield bonds that receive low quality ratings and must offer high coupons to attract investors.

Alternative to high yield bonds, mezzanine

financing may be used. This type pays even higher coupon and in addition to

interest or dividends, this also offers a potential return based on increases

in the value of common equity. From 1990 – 2009, Sharpe Ratio of private equity

was 0.34, global stocks 0.12, global bonds 0.50 and hedge funds with 0.62. In

these two decades, private equity had -23.4% worst monthly return (VC, Real

estate, commodities on more downside), hedge funds with -7.5%, global stocks at

-19.8% and global bonds with -3.8%.

There are examples of successful retail private

equity deal. For example Tops Market, it had a roller coaster ride. (Wikipedia)

At

12:01 am on December 2, 2007, Morgan Stanley Private

Equity became the new owner of Tops Markets. Ahold‘s subsidiary Giant Food of

Carlisle provided operational and support services for up to one year after the

sale. Max Henderson, Executive Vice President of Tops, resigned his position

from the company, and Frank Curci, a former Tops Friendly Markets CEO, returned

as CEO of the company.

Tops Friendly

Markets brought back approximately 100 corporate positions in marketing,

merchandising and finance to Buffalo, New York. Recently, those positions had

been based in Carlisle, Pennsylvania by Giant Food. Existing

stores resumed upgrades and remodelling, and plans for new stores

continue. Tim Hortons full-service

restaurants or self-serve kiosks as well as Anchor Bar wings

were added to all stores. A growth rate of more than 10% is expected over

the next four to five years.

In

November 2013, Tops Markets announced a management buyout. The buyout, which is

expected to be completed by the end of 2013 involves Morgan Stanley Private

Equity selling all remaining shares to Tops management, including CEO Frank

Curci. As a result, all decisions return to being locally made. In addition, it

makes Tops Markets one of the largest privately owned companies in the Buffalo area.

On February

21, 2018, Tops filed for Chapter 11 Bankruptcy. None of the stores day-to-day

operations are to be affected. According to the Securities and Exchange

Commission, the reason for filing is due to Tops’ $720 million debt. This

opportunity is being used to restructure financially so it can grow and be more

competitive.

On August 30,

2018, Tops announced they would be closing ten underperforming locations by

November, including two in Syracuse, one on West Genesee Street (NY 5) at

Westvale Plaza, and another on South Salina Street (US 11) at Valley Plaza, two

in Rochester, one on Lake Avenue and another on North Winton Road, and one each

in Perinton, Lyons, Geneva, Fulton, Elmira (the South Main Street location) and

Saranac Lake (at the Lake Flower Plaza).

Tops Markets announced they emerged from bankruptcy on November

19, 2018.

However, not many retailers are likely to end up with the

same fate as this grocery retailer. Debtwire tells us that about 40 percent of

all US retail bankruptcies in last three years were private equity backed.

Retail businesses under any circumstances is a difficult business to sustain

and threats are from various domains.

“One example, Debenhams, a 200 year old British department store ended its operations last week. It was purchased by Texas Pacific Group in 2003, they a while later, promptly began selling assets, dramatically cutting costs and awarded themselves large dividends. Threats come from e-commerce, oversupply of retail, rising rents, tighter margins and OVER GEARED BAANCE SHEETS. Payless Shoes, Toys ‘R’ Us, Gymboree, Sears holding, Mattress Firm and Radio shack – all companies at some point were owned and controlled by private equity firms have filed for Chapter 11”, writes John McNellis on Wolf Street.

Toys ‘R’ Us

story: Wolf Richter

on Wolf Street writes, “On June 29, its

remaining stores in the US will close. And then it’s over of the iconic

retailer — one more victory for PE firms that have ploughed into retail during

the leveraged buyout boom before the Financial Crisis, loaded them up with

debt, and watched them collapse in what I have come to call the brick-and-mortar meltdown.

Toys ‘R’ Us is just one of them.

PE

firms Kohlberg Kravis Roberts (KKR), Vornado Realty Trust, and Bain Capital

Partners acquired the publicly traded shares of Toys ‘R’ Us via a $6.6 billion

LBO in 2005. They funded the acquisition in large part by loading up the

acquired company with debt — hence “leveraged buyout.” In other words, the PE

firm had little skin in the game, and over the years extracted $400 million in

fees even as the retailer died.

The

33,000 employees, when it is all said and done in a few days, will be out of a

job.

In

a sense, the end came very rapidly, after 13 years of building up to it under

the PE-firms’ iron cost-cutting fist. The meltdown started in early September

when rumors emerged that Toys ‘R’ Us had hired a bankruptcy law firm. Its bonds collapsed on the spot. On September 18, the company

buckled and filed for bankruptcy, assuring everyone that it would go on as a going concern. In

early March, it became apparent that liquidation would be next. On March 15, the company announced it would liquidate all its

operations in the US and Puerto Rico. And it began “final liquidation sales” at

all its remaining Toys“R”Us and Babies“R”Us stores.

Among

the biggest investors in PE firms are public pension funds. They provide about

20% of the $3 trillion in assets managed by PE firms. Public pension funds like

the accounting of investing in PE firms: These investments are considered

illiquid and long-term and don’t get marked-to-market. This gives pension funds

the illusion of stability during times of market turmoil, and they don’t mind

the sky-high fees. And PE firms love public pension funds because that’s where

the money is – and the sky-high fees. It’s a symbiotic relationship.

But

the Toys ‘R’ Us demise under the auspices of KKR, Bain Capital and Vornado

Realty Trust has rattled some nerves, including at the $129-billion Washington

State Investment Board (WSIB), which has been investing in KKR for over 30

years, making it one of the earliest backers. According to the Wall Street

Journal, it invested in at least 23 KKR funds, including $1.5 billion in the

fund that contained the Toys ‘R’ Us investment.

The

WSIB held a meeting last Thursday discussing its investment in KKR and KKR’s

account of the Toys ‘R’ Us debacle. A recording of the meeting was heard

by Bloomberg

News:

“Did

anyone at KKR lose their job over the failure of Toys ‘R’ Us?” asked WSIB

member Stephen Miller. “Did anyone have their bonuses cut? Did anyone have

their compensation cut significantly? Because that’s one of the consequences of

free-market capitalism.”

This

is another retailer that was bought out by a PE firm, saddled with $8 billion

in debt, and now grapples with its fate.”

Matt Levine writes

on Bloomberg Opinion, “And in fact the financial press is absolutely full

of stories of creditors

complaining about private equity firms putting one past

them, finding clever ways to get paid themselves while stiffing the creditors.

But that’s just the typical conflict. There are

other possibilities. For instance here is the story of a time that

Apollo Global Management LLC acquired a company and got its executives to pay Apollo to work

there.

The dust-up involves

CEVA Logistics AG, a Swiss company that Apollo acquired more than a decade ago.

Former executives

today say Apollo double-crossed them. In a $34 million class-action lawsuit

against Apollo and CEVA, they say the buyout firm looked out for its own

interest and used a deft stroke of financial engineering that ended up wiping

out their equity. Apollo denies wrongdoing. …

Interviews with 35

current and former CEVA managers, as well as presentations made to prospective

executives, reveal how Apollo and CEVA persuaded, pressured or required

managers to put their money in. Over the years, Apollo and CEVA told executives

they could make as much as 15 times their investment when Apollo eventually

took CEVA public.

“It didn’t even

enter my mind that I could lose this money,’’ said Smit, who signed a document

promising she wouldn’t sue over the investment. “It feels like they robbed

hundreds of people by legal means.’’

Apollo bought most

of the equity of CEVA in a buyout, and let (or required)

executives buy some equity too “since it would give them ‘skin in the

game.’” When CEVA ran into trouble you might have expected Apollo to

maximize the value of the equity even at the expense of its creditors. But

instead Apollo bought a bunch of CEVA debt cheap, became a creditor, and then wiped out the equity:

Apollo started buying CEVA debt at a discount in

2007, according to the lawsuit and an Apollo document. That made it possible

for Apollo and other big creditors in 2013 to swap debt for equity in

a new company that would own CEVA. The lawsuit says the move erased the

shareholders’ stake and let Apollo maintain control with minority ownership of

a going concern with less debt.

This wiped out Apollo’s equity (but then Apollo got new equity in

the recapitalization), and it also wiped out the

executives’ equity (and they got nothing).

In response to the lawsuit, Apollo and CEVA said

they had no fiduciary duty to CEVA executives, and that even if they did, it

wasn’t breached. Apollo said it lost its equity stake, too, and that

a recapitalization was needed because CEVA was close to defaulting on some

interest payments.

Huh. Look, this is

fine. Executives ought to be compensated in part through equity ownership of their

company, and when a company can’t pay its debts, that’s supposed to wipe

out the equity, including

the equity owned by the

executives. Their equity is supposed to be at risk, to pay off if the

company works and not if it doesn’t. “It didn’t even enter my mind that I

could lose this money” is a terrible thing to say about paying cash to buy

illiquid unlisted stock in your own highly levered employer, come on.

There is one general lesson here, which is that when a portfolio company runs into trouble, a smart aggressive private equity firm will tend to do a good job of maximizing the value of its own stake in that company rather than the total return to all stakeholders. (Also it will do that openly and proudly, saying things like “what, we had no fiduciary duty to anyone else”: Every unsympathetic story like this makes Apollo look great to its actual investors, who are pleased to see it working hard and smart on their behalf.) There is also a more specific lesson, which is don’t pay Apollo to work at one of their companies. Honestly, when you write a check to Apollo to work at their portfolio company, and then you sign a document saying you won’t sue about it, what do you think is going to happen?” Looking back a year, in 2018, alternative investment firms have more than $1.8 trillion in ‘dry powder’ reserve with more than half with private equity funds.

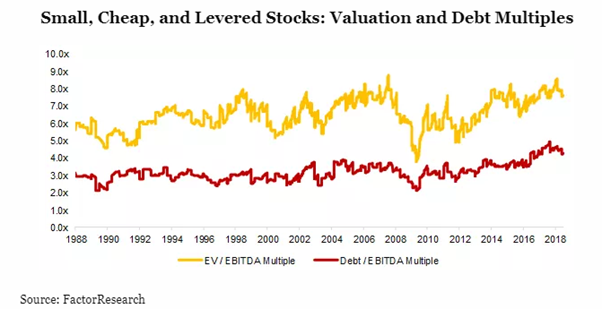

Nicholas Rabener

writes on Enterprising Investor, “Exposure to

small caps likely explains private equity returns. Liquid alternatives to

private equity can be created simply by buying small, cheap, and levered

stocks.

Some have reached similar conclusions and proposed that the nature

of locked-up capital is what makes private equity so advantageous. It keeps

investors from redeeming their funds at market lows and helps private equity

firms weather storms like the global financial crisis. But the same fund

structure can be replicated through public equities at a fraction of private

equity fees.

Furthermore, with $1.8 trillion sitting on the side-lines, too

much money may end up chasing too few deals, creating high acquisition

multiples that don’t augur well for expected returns.

Of course, high valuations are now the rule in both private and public markets. And corporate debt levels are at all-time highs.

Neither of these developments bode well for

expected returns. So investors might be wise to reconsider direct private

equity allocations and their liquid alternatives altogether.”

Barbarians at the Gate a docudrama and a comedy is based on a book about leveraged buyout of food giant RJR Nabisco. It is a story of greed, egos, and lust for luxury, high stakes, and treachery. After the expensive failure of a smokeless cigarette, the CEO of RJR Nabisco draws up plans to buy the company outright. But an influential LBO guru, who initially gave the CEO the idea for the LBO, is unhappy that the CEO is using his idea without involving him, and they end up in a bidding war. As the LBO guru puts it, “It’s not the company. It’s the credibility. My credibility. I can’t just sit on the bench and let other people play the game. Not my game. Not with their rules.” Among other things, the movie also shows that a CEO may have little to do with the success of his company — and much to do with its failings. The movie features many humorous but telling lines, such as: “You know the three rules of Wall Street? Never play by the rules, never tell the truth, and never pay in cash.”

The US dollar is on the cusp of making a major move. The question is which way will it go, higher or lower? The directional movement of the US dollar will have significant asset performance implications once the tug of war between dollar bears and bulls is resolved.

The US dollar index has been consolidating its 2018 gains for the better part of six months and is currently in the process of forming what market technicians call an ascending triangle formation. It’s supposed to be a bullish pattern, but the reality is that technical analysis rules of thumb rarely stand up to statistical tests of significance. Regardless, what the pattern tells us is that supply of dollars emerges as the US dollar index approaches 98 and demand emerges as it approaches 96.5. The fact that the triangle is narrowing simply indicates that one of the two sides will prevail soon.

Setting aside the chart pattern setup for a moment, we also observe an historically very low level of volatility between the US dollar and its major currency pairs. In fact, our FX volatility index (which is just the average annualized volatility of the US dollar vs six other major currencies) stands at just 5.2%, a level that has been reached only four times in the last 40 years or so. Since FX volatility is mean reverting – hovering between about 4-14% pretty much all the time – we have every reason to expect FX volatility to resurface sooner rather than later.

The coiled springs of supply and demand points converging and historically muted FX volatility means the US dollar could be in for a fierce move in one direction or the other. For asset allocators, this has huge implications for how one ought to position a portfolio. The three asset classes most at risk of dynamic out or underperformance based on the direction of the dollar move are US small caps, emerging market stocks, and gold.

John Hempton writes….I used to be of the view that suggested that buybacks were just another way of distributing to shareholders – a bit like dividends, selectively applied.

You could turn a buyback into a dividend by selling your own shares in precisely the proportion that the company bought shares back. Then your percentage ownership was unchanged and you would have (in cash) your share of the monies that the company distributed to its owners.

I used to think that. But it isn’t quite true because companies can impair themselves with buybacks in ways that you just couldn’t with dividends. Few companies support paying dividends at 2x underlying cash generation. But debt funded buybacks of this size are alas fairly common. Debt funded buybacks, applied to their illogical limit, will corrupt you, and turn you into a gebbeth – inhabited by the debt (and its evils) you have allowed into your body. First however I need to recount a parable about how leverage corrupts morality.

April 16 – Bloomberg (Rich Miller and Craig Torres): “Federal Reserve Chairman Jerome Powell and his colleagues have made an important shift in their strategy for dealing with inflation in a prelude to what could be a more radical change next year. The central bank has backed off the interest-rate hikes it had been delivering to avoid a potentially dangerous rise in inflation that economic theory says could result from the hot jobs market. Instead, Powell & Co. have put policy on hold until sub-par inflation rises convincingly.”

April 15 – CNBC (Thomas Franck): “Chicago Federal Reserve President Charles Evans said on Monday that he’d be comfortable leaving interest rates alone until autumn 2020 to help ensure sustained inflation in the U.S. ‘I can see the funds rate being flat and unchanged into the fall of 2020. For me, that’s to help support the inflation outlook and make sure it’s sustainable,’ Evans told CNBC’s Steve Liesman.”

April 15 – Reuters (Trevor Hunnicutt): “The U.S. Federal Reserve should embrace inflation above its target half the time and consider cutting rates if prices do not rise as fast as expected, a top policymaker at the central bank said… ‘While policy has been successful in achieving our maximum employment mandate, it has been less successful with regard to our inflation objective,’ Federal Reserve Bank of Chicago President Charles Evans said… ‘To fix this problem, I think the Fed must be willing to embrace inflation modestly above 2% 50% of the time. Indeed, I would communicate comfort with core inflation rates of 2-1/2%, as long as there is no obvious upward momentum and the path back toward 2% can be well managed.”

It’s stunning how dramatically the Fed’s perspective has shifted since the fourth quarter. There’s now a chorus of Fed governors and Federal Reserve Bank Presidents calling for the central bank to accommodate higher inflation. Watching the inflation data (March CPI up 1.9% y-o-y), it’s not readily apparent what has them in such a tizzy. And with crude prices surging 40% to start 2019, it takes some imagining to see deflationary pressures in the pipeline.

The Fed’s (and global central banks’) dovish U-turn was clearly in response to December’s global market instability. Quickly, the global system was lurching toward the precipice. Acute fragility revealed – and central bankers were left shaken. And witnessing the speculative fervor that has accompanied central bankers change of heart, the backdrop is increasingly reminiscent of Bubble Dynamics following the 1998 LTCM bailout. A Bloomberg headline from earlier in the week caught my attention: “Evans Sees Lessons From 1998 Rate Cuts for Fed Policy This Year.” It said, “For the Chicago Fed president Charles Evans the situation recalls the Asian financial crisis of 1998. According to Evans, ‘The risk-management approach taken by the Fed is not unusual. It served us well in similar situations in the past.’”

Historical revisionism. For starters, the Asian crisis was in 1997. The Fed aggressively reduced rates from 5.50% to 4.75% in the Autumn of 1998 in response to the simultaneous Russia and Long-Term Capital Management (LTCM) collapses.

From Evans’ April 15, 2019 speech, “Risk Management and the Credibility of Monetary Policy:” “Later, in the autumn of 1998, the fallout on domestic financial conditions from the Russian default led to a downgrading of the economic outlook and an aggressive 75 basis point easing in the funds rate over a two-month period. When making the first of those cuts, the FOMC noted that easing would ‘provide added insurance against the risk of a further worsening in financial conditions and a related curtailment in the availability of credit to many borrowers.’”

Clearly many borrowers – and the system more generally – should have faced much tighter Credit Availability by late-1998 – certainly including those aggressively partaking in leveraged speculation (equities, fixed-income and derivatives) and debt gluttons in the real economy – including the highly levered telecom companies (i.e. WorldCom, Global Crossing, XO Communications and a long list) and others (i.e. Enron, Conseco, PG&E, etc.).

Evans, not surprisingly, skips over LTCM. That the Fed orchestrated a bailout of this renowned hedge fund sent a very clear message that the Federal Reserve and global central banks were there to backstop the new financial infrastructure that was taking control of global finance (Wall Street firms, derivatives, the leveraged speculating community, Wall Street structured finance and securitizations). If the Fed had allowed the system take the harsh medicine in 1998 the world would be a much safer place today.

Evans: “How did this risk-management strategy turn out? In the end, the economy weathered the situation well. Productivity accelerated sharply, and by early 1999 growth was on a firm footing. Subsequently, the FOMC raised rates by a cumulative 175 basis points by May of 2000.”

Evans leaves out the near doubling of Nasdaq in 1999, along with what I refer to as “terminal phase” Bubble excess. The bottom line is the Fed aggressively loosened policy while the system was in the late-stage of a significant Bubble, and then failed to remove this accommodation until mid-November 1999.

And let’s not forget that the subsequent bursting of the so-called “tech bubble” led to what was, at the time, unprecedented monetary stimulus – including Dr. Bernanke’s speeches extolling the virtues of the “government printing press” and “helicopter money.” These measures were instrumental in fueling the mortgage finance bubble that burst in 2008. That collapse then led to a decade-long – and ongoing – global experiment in zero rates, open-ended money-printing and yield curve manipulation.

This whole fixation on deflation risk and CPI running (slightly) below target gets tiring – after a few decades. Clearly, the evolution to globalized market-based finance has profoundly altered the nature of inflation. CPI is no longer a paramount issue – especially with the proliferation of new technologies, the digitization of so much “output,” the move to services-based economies and, of course, globalization. There is today a virtual endless supply of goods and services – certainly including digital downloads, electronic devices and pharmaceuticals – that exert downward pressure on aggregate consumer prices. Importantly, consumer price indices are no longer a reliable indicator of price stability, general monetary stability or the appropriateness of central bank policies.

Central bank officials today lack credibility when they direct so much attention to consumer price inflation while disregarding the overarching risks associated with unrelenting global debt growth, highly speculative and leveraged global financial markets, and deep global economic structural maladjustment. In the grand scheme of things, consumer prices running just below target seems rather trivial. What’s not trivial are central bankers that now appear to have accepted that they will accommodate financial excess and worsening structural impairment. At this point, it appears Full Capitulation.

In the same vein (and same day) as Evans’ speech, former President of the Federal Reserve Bank of Minneapolis, Narayana Kocherlakota, posted a Bloomberg editorial: “The Fed Needs to Fight the Next Recession Now. Its tools are limited, so the central bank must compensate by being aggressive.”

“Almost 10 years after the Great Recession ended, the growing threat of a new economic slowdown raises a troubling question: When the next recession strikes, what can the world’s central banks do? With interest rates low and their balance sheets still loaded with assets bought to fight the 2008 crisis, do they have the tools to respond? ‘What, then, can the Fed do?’ In my view, it needs to be much more aggressive in using the limited tools that it has. For one, if your medicine chest is nearly empty, you want to keep your patient as healthy as possible. That means cutting interest rates now to lower the unemployment rate even further. Doing so could also boost demand during any recession: If people come to expect stronger recoveries, they will be more likely to keep spending even in downturns. A pre-commitment to strong growth could also help. In the last recession and ensuing slow recovery, the Fed treated its low-interest-rate policy largely as an emergency step that would be removed within the next year or two. Instead, the Fed should publicly commit now to maintain maximum stimulus after a recession until the unemployment rate falls below 3%, as long as the year-over-year core inflation rate remains below 2.5%. Such a promise, much stronger than any used or even suggested during the last recovery, would help minimize the damage and speed up the rebound.”

It’s simply difficult to believe such analysis resonates – yet it sure does. These are strange and dangerous times. Kocherlakota: “If your medicine chest is nearly empty, you want to keep your patient as healthy as possible.” Noland: If you’re running short of medicine, you better not encourage your patient to live a reckless lifestyle. You certainly don’t want to convince the foolhardy that you possess an elixir that will cure whatever ails them. These central bankers have really lost their minds: What they administer is anything but medicine.

Such central bank crazy talk should have longer-term bonds beginning to sweat. But, then again, bond markets are confident that central bankers from across the globe will be buying plenty of bonds over the coming months and years. When central bankers talk about accommodating higher inflation, bonds hear “more QE”. And while safe haven bonds may not be overjoyed at the thought of CPI creeping higher, they remain more than fine with bubbling risk markets – prospective bursting Bubbles ensuring only more expansive QE programs. The so-called U-turn marked an inflection point from a meek attempt to return central banking to sounder principles – to a decisive breakdown in any semblance of responsible monetary management.

I was convinced in ‘98 the Fed was committing a major policy error. Like today, the Fed and global central bankers were afraid of global fragilities. Yet markets and economies do turn progressively fragile after years of excess. These days, I worry about what central bankers have unleashed with their ultra-dovishness in the face of historic late-stage global Bubble “terminal excess.”

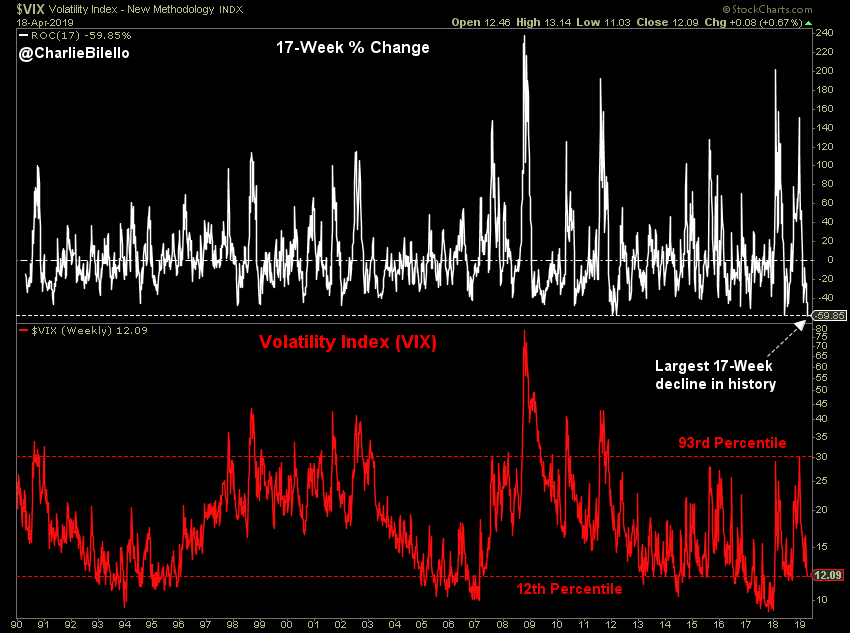

The Volatility Index has fallen 60% over the past 17 weeks, the largest 17-week decline in history.

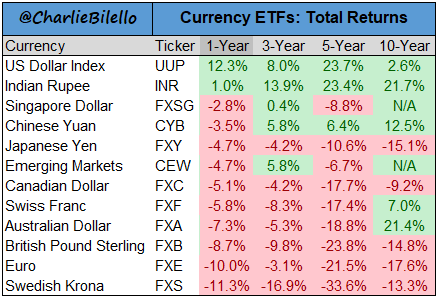

US Dollar leading all currency ETFs over the past year…

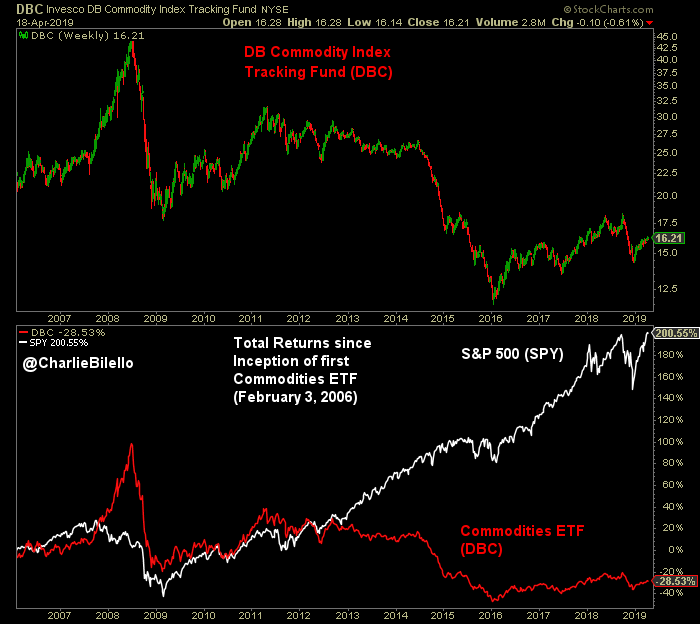

The first broad commodities ETF was launched in Feb 2006. It is down 28% since inception vs. a +200% gain for the S&P 500.

The trade headlines for today. President Xi has all time in the world but sadly President Trump does not have that Luxury. It will be naïve to think that US will prevail upon China in a trade deal