Brett writes…In the end, central banks can keep pumping liquidity and suppress interest rates to make markets appear risk free, but the harsh reality will set in sooner than later. It’s not a question of if, it’s a question of when will this market collapse. On top of this you have an ever going issue of pensions, endowments, and the general public loaded up on stocks more so than ever due to yield chasing which is a by product of the low and negative interest rates we’ve seen the past decade. Combine that with the largest generation of American’s in the process of retiring or nearing retirement, baby boomers, and you have your recipe for disaster. Price discovery is broken and this will cause for a violent selloff once things begin to tumble. The fundamentals are much worse now in April 2019 than they were in the beginning of October 2018. The IMF continues to cut global growth forecasts and with geopolitical risk rising, we are likely to see market shocks. France is a perfect example, where production has slowed down heavily due to over five months of “yellow vest” protests. We will soon see how the last decade really wasn’t a recovery and when shit hits the proverbial fan it will be more apparent than ever, especially when 69% of Americans have less than $1,000 in total savings

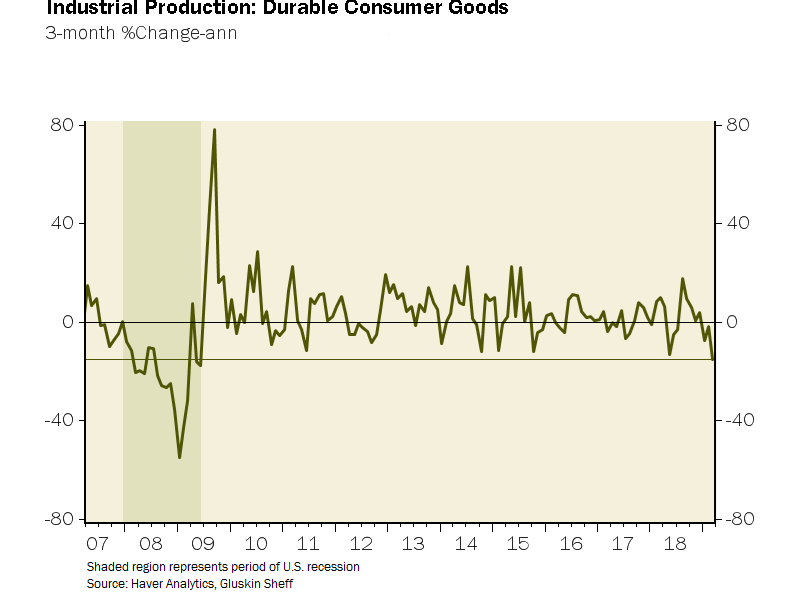

The three-month trend in production of consumer durable goods has collapsed to a -15% annual rate – this takes out 2016 and takes us back to the late stages of the 2008-09 recession.

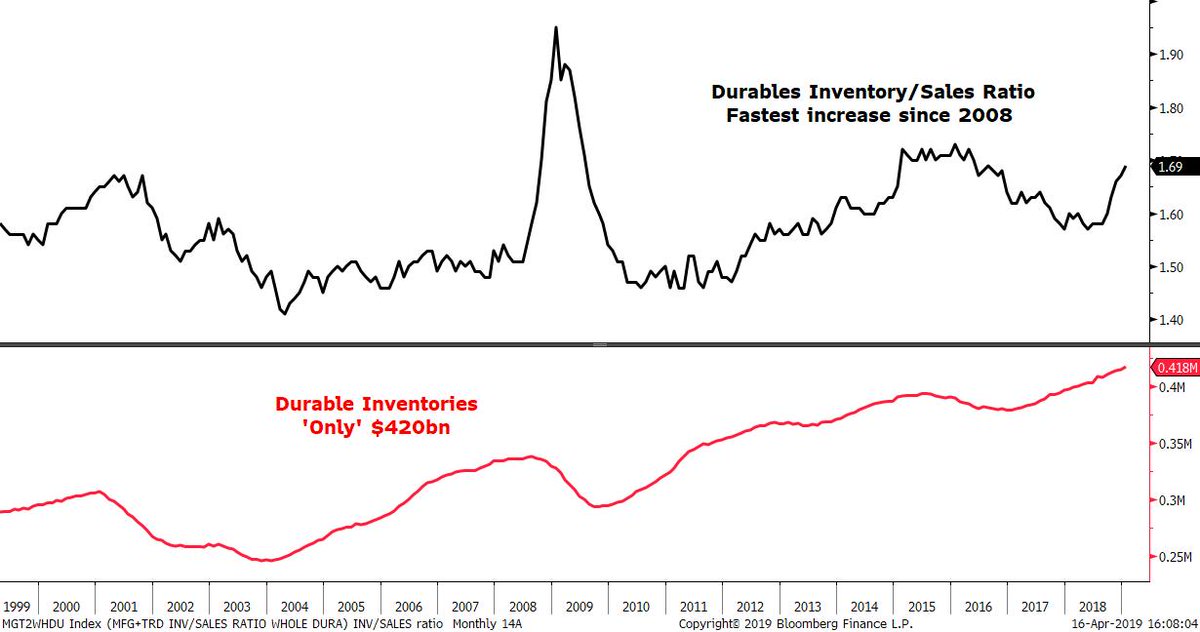

It might get worse with Inventories at record highs and Inventory/Sales ratio rising at the fastest pace since 2008.

Stock market is disconnected to the reality because of excess LIQUIDITY which can also be seen in the volatility collapse

The race to zero?

So either the data improves or volatility rises. This will not continue for long

Employment by a big company is perhaps, the best job a young educated aspirant would look forward to. Government jobs are preferred in general, to private sector jobs. But, the better educated usually prefer jobs in large private companies. Jobs offered by the large private sector companies are always in good demand.

In fact, it matters less whether the company is a public sector undertaking like say, State Bank of India or Bharat Heavy Electricals or a private sector enterprise like say, HDFC Bank or Tata Motors. Large companies are usually considered to be the best employers.

We take a look at how good have companies been in increasing their head count in recent years.

All Indian companies are not required to reveal the number of people they employ. Only listed companies are required to disclose this. Even this disclosure was made mandatory only in 2014-15. This is a good beginning and deserves to be extended to be applicable to all companies at the earliest.

A proxy for growth in head-count would be the growth in what the companies spend on compensation to employees. Growth in this would reflect a growth in the head-count and the growth in wages paid. We find that this growth rate has been falling.

CMIE’s Prowess database shows a steady fall in the rate of growth of compensation paid by companies to employees since 2013-14. The Prowess database includes performance information on a large sample of listed and unlisted companies of all sizes and industries.

Compensation to employees grew by 25 per cent in 2013-14. The growth rate halved to 12 per cent in 2014-15 and then it fell further to 11 per cent in 2016-17. In 2017-18, the growth rate fell to 8.4 per cent. From this, it wouldn’t be entirely wrong to infer that the corporate sector’s appetite for new hiring has been declining quite sharply.

2017-18 saw the slowest growth in the past eight years, or since the year after the Lehman crisis of 2008 when the compensation to employees grew by only 7.7 per cent.

The Prowess database also shows that the corporate sector registered a fall in growth in fixed assets to 6.9 per cent in 2017-18. Growth of investments into the job-creating plant and machinery part of fixed assets was even lower at 5.9 per cent. Both were the lowest since 2004-05. Evidently, the two declines in growth rates – plant and machinery and wages go hand-in-hand. Lack of investments into fresh capacities is hurting growth in employment.

We see the same fall in investments in another dataset – CapEx and the same fall in employment in yet another dataset – Consumer Pyramids Household Survey.

The evidence of falling growth in investments and employment during the recent past is therefore overwhelming.

Some of the growth in compensation to employees can be explained as a consequence of inflation and given that inflation has been much lower in recent years compared to the past, it would be good to correct the growth numbers for inflation. We do this using the consumer price index for recent years and the consumer price index for industrial workers for earlier years.

Now we see inflation-adjusted compensation to employees grow by only 4.6 per cent in 2017-18. This is lower than the already-low average growth of 5.5 per cent seen in the preceding three years.

The average real, i.e. inflation-adjusted, compensation to employees grew at the rate of 5.3 per cent per annum in the four years between 2014-15 and 2017-18.

The industry-wise distribution of this growth in inflation-adjusted compensation to employees show some sharp variations between major sectors.

The services sector has seen a very small growth in compensation to employees in 2017-18. Compared to the overall growth of 4.6 per cent, the services sector saw a growth of only 2.2 per cent. Within services, it was the telecommunications sector that saw a fall, of 3.6 per cent, in real compensation. This was the fifth consecutive year of fall in inflation-adjusted compensation to employees in this industry. Information technology companies saw a less-than two per cent growth in real wages. Air transport services was another dampener.

In contrast, financial markets showed a healthy 8.1 per cent growth in inflation-adjusted wages in 2017-18. Banks recorded a growth of 6.5 per cent and most non-banking financial services industries recorded double-digit growth rates. However, we know that the non-banking finance companies fell into problems in 2018-19.

The weak growth in real wages in the IT sector and the apparent implosion in the NBFCs are possibly symptomatic of the despondency over decent jobs in recent times.

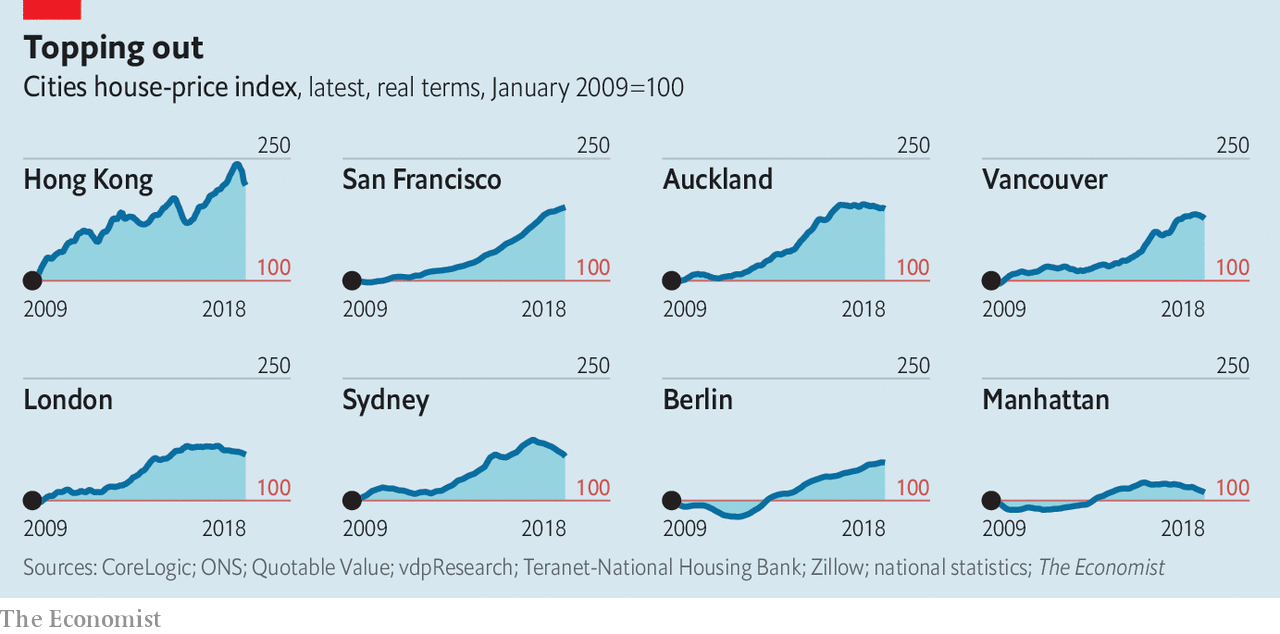

The reason is simple. Budget deficits are rising, state and Municipalities are now having more pension obligations with falling revenues. It is easier to tax an immovable asset like property than movable assets because then technically you can move to low tax jurisdiction with your money.

I am seeing more and more evidence of states trying to squeeze the property markets. Simon Mikhailovich tweeted

“Got an annual letter from our coop board announcing a 9% (gulp, gulp) increase in the monthly maintenance. One key reason: “Manhattan buildings have been targeted by the City of New York, which has significant pension liabilities that it must address.”

This is the situation when interest rates are at an all time low and Global economy is still expected to grow around 3% this year as per IMF. Years of low inflation coupled with low interest rates have increased the shortfall in government pension liabilities and the only way this hole can be filled is by increasing the taxes. With interest rates near bottom, real estate owners are facing a double whammy of rising mortgage payments and rising property taxes and maintenance.

The stagnant incomes and hunt for taxes will increase the cost of ownership for average homeowner and will be the reason that real estate prices (especially in developed countries) are headed for steep fall in coming years.

The world’s biggest economy, United states may be heading into a recession in approximately 12-18 months. But, the recent factors indicate a mild and prolonged recession with fewer tools available with Fed and Fiscal policymaker. It’s important to know what is recession to be prepared for it and allocate your financial portfolio accordingly.

Indicator

Strength

Real Retail

Sales

Weak

10 year-

3-month Government yield curve

Weak

Unemployment

gap and hourly hour worked (YoY)

Neutral

Real Fed Rate

and leading indicator

Neutral

(Deteriorating)

Monetary tools

Neutral

Fiscal Policy

strength

Weak

Housing Market

Strong

Definition of Recession

Two consecutive quarters of decline in economic growth measured by a country’s Gross domestic product is consider Recession.

Illustration of recent recession:

Housing Bubble in 2008The Financial crisis in 2008 is still the worst crisis since the great depression in 1930s. The leading cause was the bubble in housing market, an inferior asset quality which lead to subprime crisis

Dot.com bubble in Technology companies

The technology bubble experienced higher technology company valuation. The Dot.com bubble in 2001 had one of the worst bear markets as stock plummet more than 50% in technology companies.

The below graph summarizes the conclusion that we are approaching a recession; and possibly a mild recession relative to the recent crisis in 2008.

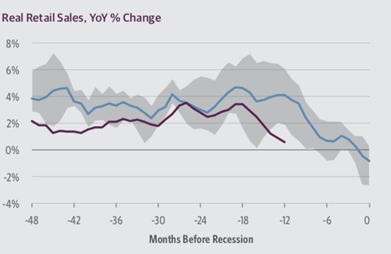

Real Retail Sales

The Real retail sales growth have fall from more than 3% to below 1% in 6 months. This is below the average sales 12 months prior to recession and also less than the lower bound of real retail sales relative to previous recession cycle. Consumer spending is a major proportion of economic activity in United States and retail sales having a significant impact on the consumer spending has seen a decrease recently. This indicates a slowdown in United States.

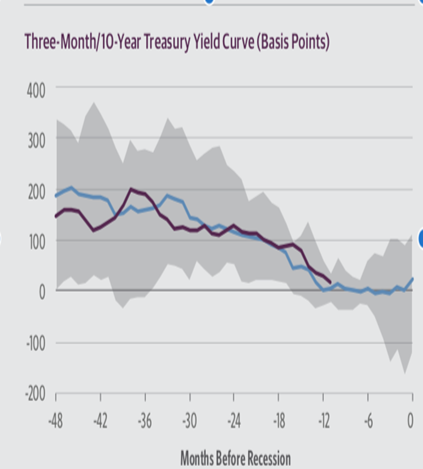

10 Year- 3-month Government Yield Curve.

The inverted 10 year- 3-month

Government yield curve has been one of the trusted sources to predict

recession. It explicitly depicts the relationship and yield for investing in

10-year treasury bond, the most liquid Government bond, and the 3-month yield,

observed in short-term lending/money market as the cost of short-term borrowing

rate by the Treasury.

Empirical evidence shows that the inverted 10 year – 3 months has served as an indicator for recession. The recent inversion indicates that the bond yields at the long-end of the curve is yielding less than the short-end of the yield curve. This implies that the long-end of the yield curve is not compensating the investor with term maturity premium but the market is comfortable holding the long end as it sees the approaching recession and subsequent rate cuts. This has increased the probability of recession in future.

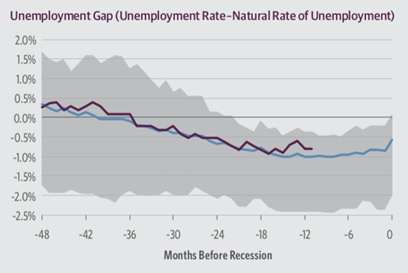

Unemployment Gap

The unemployment gap, unemployment rate adjusted for natural rate of unemployment, is negative but wider relative to average unemployment gap in prior cycle. This gives the fiscal policy makers some tools to grow economic activity by increasing employment to support economy as long as such jobs can be created. The Gross domestic product (GDP) growth and potential output has direct relation with increase in labor force and labor force participation.

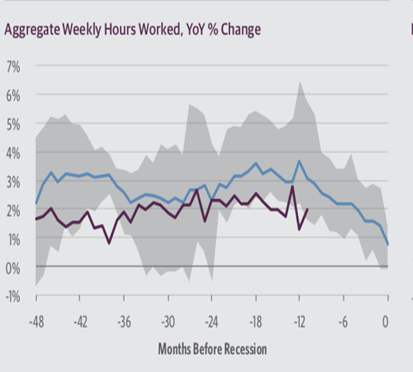

Weekly Hours Worked

The corporates increase spending

in expectation of higher demands for product and services. This can increase

the aggregate weekly hourly worked, if the increase in employment is not

feasible. The aggregated weekly hours

worked has experienced steep decline, in year on year change, recently. This

indicates that the corporates have reduced their activity, and in worst

scenario the inventory has touched the peak and it is decreasing in expectation

of lower demand for their product or services.

A reduction in corporate activity to gauge lower demand will eventually lead to reduction in the economics growth and soon and eventually contribute to the recession.

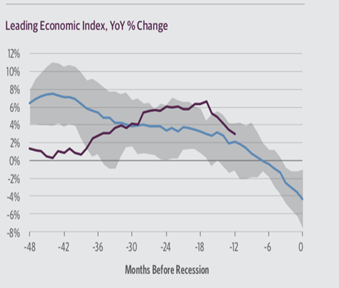

RLeading Indicators

The leading economic index have

deteriorated sharply in past 6 months.

Some of the other factors

affecting the next recession are:

Fiscal

Deficit:

The fiscal deficit is high. Although the budget deficit is countercyclical, the extended period of expansion was different. The Government budget deficit rose to 4.5% from1 from 2.9% in 2014 as a percentage of GDP. This has been due to higher fiscal spending and lower tax rate to boost economy

Less space for rate cuts to boost economy activity and valuation of assets:

The recession would be prolonged relative to earlier recession. The average fed rate cuts during recession has be 5.5%. The Fed can move to others tools like Quantitative easing (QE), Japanese type yield curve control and negative short -term yield. The corporate debt has seen a sharp rise and the fed lacks the statutory ability to purchase corporate debt for quantitative easing, but who knows the desperation level of FED in next recession. None the less, the Fed has more purchasing power to boost economy relative to other central banks as Fed holds only 20% of GDP as its balance sheet, where Euro central bank and Japan hold 40% and 100% 3respectively.

Global

slowdown:

The world is experiencing a global slowdown and this would add to the concern of global slowdown of U.S. China provided credit easing and infrastructure spending in the 2008 crisis. It is unlikely to provide the same stimulus, even if it provides any, in the next recession.

Conclusion:

In the middle of slower global economic outlook and uncertainty regarding the Brexit, the data from US is indicating that the world’s largest economy is heading to a recession in a year to 18 moths from now.

The inverted 10 year – 3-month yield curve, dovish stance by Fed, deteriorating leading indicators and real retail sales, and reduction in the weekly hours’ worked growth rate are some of the signs towards a recession in the mid of 2020. The hope is that the severity of the recession will be less relative to recent recession, majorly due to stronger balance sheet of banks, but it will take longer time to heal as the monetary policy has less power to stimulate economy by reducing interest rates it has lower spread before reaching the zero-interest floor. The significant increase in corporate debt and the contribution of fiscal deficit to the extended period of business expansion has placed the credit market and fiscal policymaker with less tools to counter the recession“

The Food Corporation of India (FCI) has taken a loan of Rs.600 billion from the National Small Savings Fund (NSSF), as per a report in Financial Express. The government has resorted to the NSSF loan for the third year in a row to ensure that the FCI’s operations are unaffected owing to its funds constraints. Such arrangements also indicate that normal government expenditure is being substituted with loans instead of cash on fears that fiscal deficit will go for a toss if it is shown as the government borrowing, as per industry sources. The budgeted food subsidy through FCI for 2018-19 was Rs.1.4 trillion. Of which, the Centre has paid about Rs.800 billion from the Budget. With the latest loan, the outstanding debt of FCI (from the NSSF) is estimated to have touched Rs.1.8 trillion. The Centre’s dues to the FCI has now touched Rs.1.9 trillion and unless it finds budgetary resources soon to salvage the situation, it could be looking at a debt trap, but don’t worry like always the can will be kicked into the future .

Investors have thrown caution to

the wind as they bid up FAANG stocks to imprudent heights and provide overly

generous bids for a few others that face serious jeopardy, including Tesla and

Boeing. Even so, the herd evidently had second thoughts about one stock on

Friday, pummeling the shares of Netflix when competitor Disney announced a new

streaming service that will be bargain priced at $6.99 a month. Apple was

another story, however. After getting hit early in the session, the stock

actually closed higher despite the fact that the company will soon be competing

with Disney, Netflix and others in the well-saturated entertainment sector.

AAPL is arguably the most overpriced of the bunch, since the shares had already undergone a ballistic rejuvenation weeks ago after the company announced it would produce and stream movies and TV shows. Investors who have bid up Apple stock 42% since January are betting the company will be able to offset weakening iPhone sales with such fare, but this is unrealistic, to put it mildly. There are already far too many deep-pocketed players in the game, producing many more shows than any of us has the time or interest to watch. And even if Apple were to create TV good enough to steal viewers from Netflix, Disney et al., profit margins would not come close to what they’ve been from selling pricey mobile phones to iCult buyers.

Lotus-Eaters Love Uber

Uber is another company that

lotus-eating investors and the supposedly smart money have got all wrong.

Although Wall Street recently lowered its sights by 16%, to $100 billion, for

the upcoming IPO, this is still an insane valuation for a business that may

never turn a profit. A Wall

Street Journal story published last week suggested the dimensions

of the problem: Behind Uber’s

Slowing Growth: Onslaught of Global Competition Takes a Toll. But

the article considered competition only from bonafide companies that are

already visible in the ride-hailing field. The real competition will eventually

come from every Tom Dick & Harry – i.e., your neighbors, acquaintances and

their friends who are looking to make some spare change. All of them will soon

be able to buy software that will enable them to create their own ride-hailing

micro-companies practically overnight.

This could usher in a brave new world with no unemployment — only massive underemployment as millions of entrepreneurial drivers try to beat the pants off each other in order to survive. The ride-hailing concept pioneered by Uber is creative destruction at its most powerful and most consequential in dollar terms. In pricing the Uber IPO at a tulip-o-mania threshold of $100 billion, the Masters of the Universe — at least those who lack the good sense to dump their insider shares at the first opportunity — are headed for a fall.

Facebook Is Becoming Un-Cool

Facebook and Tesla are two other

‘dead stocks walking’ for reasons I’ve written about here before. Millennials

are increasingly deserting Facebook, and even with two billion subscribers, the

social-media platform could become un-cool faster than you can say “America

Online”. And check your own Facebook page if you need to be convinced that the

firm’s advertising-based model has run amok. These pages have come to literally

run themselves for the benefit of Facebook and its advertisers. No wonder the

company and its founder, Mark Zuckerberg, have become pariahs in the eyes of

all who value privacy. At the same time, regulators have grown increasingly

eager to rein in the company, and to fine it billions of dollars as Brussels’

elites have been doing regularly to internet giants. Facebook’s solution?

They’ve announced a pivot toward a business model that would emphasize paid

services over laser-targeted advertising. But this is no more likely to sustain

revenues than Apple’s planned foray into television.

As for Tesla, it remains a

bankruptcy bet, depending on which Model 3 sales data you believe. Is Tesla

hitting its numbers? It would appear not; but even if they are, serious

problems with the sales channel, quality control and long waits for repairs

have been taking a heavy toll on the company’s reputation. It won’t help that

generous tax credits to car buyers of up to $7500 are about to be halved. And

whereas Tesla had no competitors just a couple of years ago, many auto

manufacturers have recently entered the electric-car niche and more are coming.

Hubris Won’t Save Boeing

Then there is Boeing. The company

may be too big, and too important to America’s manufacturing prowess, to fail,

but investors appear to be recklessly underestimating the difficulties the

aircraft maker will face as a result of two fatal collisions involving its

best-selling 737 Max. The stock, which has held its ground lately, gained

2.5% on Friday, bolstered by a deftly managed PR campaign that most recently

spun the impending fix for the 737 as a potential big winner globally. Hubris aside, click here to understand why the

jet-makers problems are only likely to grow, along with a sales-killing taint

of scandal. Would you go out of your way to book a 747 Max flight if

alternatives were available? Of course not; and neither should we expect

airlines to order 737s with the same enthusiasm as before when attractive

alternatives are available from Airbus. Look for cancellations of Boeing orders

in the future, even if investors seem for the moment to be ignoring this risk.

The heedless buying

that has helped prop up Boeing shares is of a piece with the wafting rallies in

other dead-man-walking stocks such as the ones mentioned above, and with the

$100 billion valuation of Uber. This behavior reflects malinvestment and

misjudgment on an epic scale. In the securities world, the folly of this age has

become as obvious as a billboard in Times Square.

Newly available net worth data from the Federal Reserve suggests that the “left-behind” contagion has spread to all Americans aside from the top 10 percent. While still wealthier overall than most other groups, even the upper-middle class is feeling the pinch of income stagnation. The growth rate of this group’s incomes is lagging behind that of those both lower and higher on the socioeconomic ladder.

The cost of many products and services the upper middle class buys, from autos to college educations, is outpacing overall inflation. While having access to credit, these households are increasingly tapping into costlier forms of debt.

I have always enjoyed Manish thought provoking articles and his annual letter to his Stakeholders. He writes about his investment style, learnings and deep dives into his portfolio companies.

Amazon today remains a small player in global retail. We represent a low single-digit percentage of the retail market, and there are much larger retailers in every country where we operate. And that’s largely because nearly 90% of retail remains offline, in brick and mortar stores. For many years, we considered how we might serve customers in physical stores, but felt we needed first to invent something that would really delight customers in that environment. With Amazon Go, we had a clear vision. Get rid of the worst thing about physical retail: checkout lines. No one likes to wait in line. Instead, we imagined a store where you could walk in, pick up what you wanted, and leave.

Getting there was hard. Technically hard. It required the efforts of hundreds of smart, dedicated computer scientists and engineers around the world. We had to design and build our own proprietary cameras and shelves and invent new computer vision algorithms, including the ability to stitch together imagery from hundreds of cooperating cameras. And we had to do it in a way where the technology worked so well that it simply receded into the background, invisible. The reward has been the response from customers, who’ve described the experience of shopping at Amazon Go as “magical.” We now have 10 stores in Chicago, San Francisco, and Seattle, and are excited about the future.

Failure needs to scale too

As a company grows, everything needs to scale, including the size of your failed experiments. If the size of your failures isn’t growing, you’re not going to be inventing at a size that can actually move the needle. Amazon will be experimenting at the right scale for a company of our size if we occasionally have multibillion-dollar failures. Of course, we won’t undertake such experiments cavalierly. We will work hard to make them good bets, but not all good bets will ultimately pay out. This kind of large-scale risk taking is part of the service we as a large company can provide to our customers and to society. The good news for shareowners is that a single big winning bet can more than cover the cost of many losers.

Development of the Fire phone and Echo was started around the same time. While the Fire phone was a failure, we were able to take our learnings (as well as the developers) and accelerate our efforts building Echo and Alexa. The vision for Echo and Alexa was inspired by the Star Trek computer. The idea also had origins in two other arenas where we’d been building and wandering for years: machine learning and the cloud. From Amazon’s early days, machine learning was an essential part of our product recommendations, and AWS gave us a front row seat to the capabilities of the cloud. After many years of development, Echo debuted in 2014, powered by Alexa, who lives in the AWS cloud.

No customer was asking for Echo. This was definitely us wandering. Market research doesn’t help. If you had gone to a customer in 2013 and said “Would you like a black, always-on cylinder in your kitchen about the size of a Pringles can that you can talk to and ask questions, that also turns on your lights and plays music?” I guarantee you they’d have looked at you strangely and said “No, thank you.”

Since that first-generation Echo, customers have purchased more than 100 million Alexa-enabled devices. Last year, we improved Alexa’s ability to understand requests and answer questions by more than 20%, while adding billions of facts to make Alexa more knowledgeable than ever. Developers doubled the number of Alexa skills to over 80,000, and customers spoke to Alexa tens of billions more times in 2018 compared to 2017. The number of devices with Alexa built-in more than doubled in 2018. There are now more than 150 different products available with Alexa built-in, from headphones and PCs to cars and smart home devices. Much more to come!