“This year, 88% of advisors indicated that they currently use or recommend ETFs with clients, compared with 70% for mutual funds. 45% of advisors said they plan to increase their usage of ETFs over the next year, compared with just 19% for mutual funds” https://wealthmanagement.com/mutual-funds/slow-demise-mutual-funds…

Bank of Canada Governor Stephen Poloz is no fan of Modern Monetary Theory: MMT “is offering us a free lunch, and most of us know there is no such thing…it has been tried many times in the past, and the record is not pretty.”

Lookout. Strongest negative correlation between gold & yields ever! Completely unsustainable. The Fed’s printing machine is officially on. Gold probably at early stages of a bull market & yields likely bottomed. It’s all fun and games until monetary policy comes at a cost

This again. China agreeing to make $50 billion in U.S. agricultural purchases in 2020. The RECORD value for annual U.S. ag product exports to China was in 2012 at just under $26 billion. Compare commodity prices then and now. For reference, 2017 was $19.5 billion.

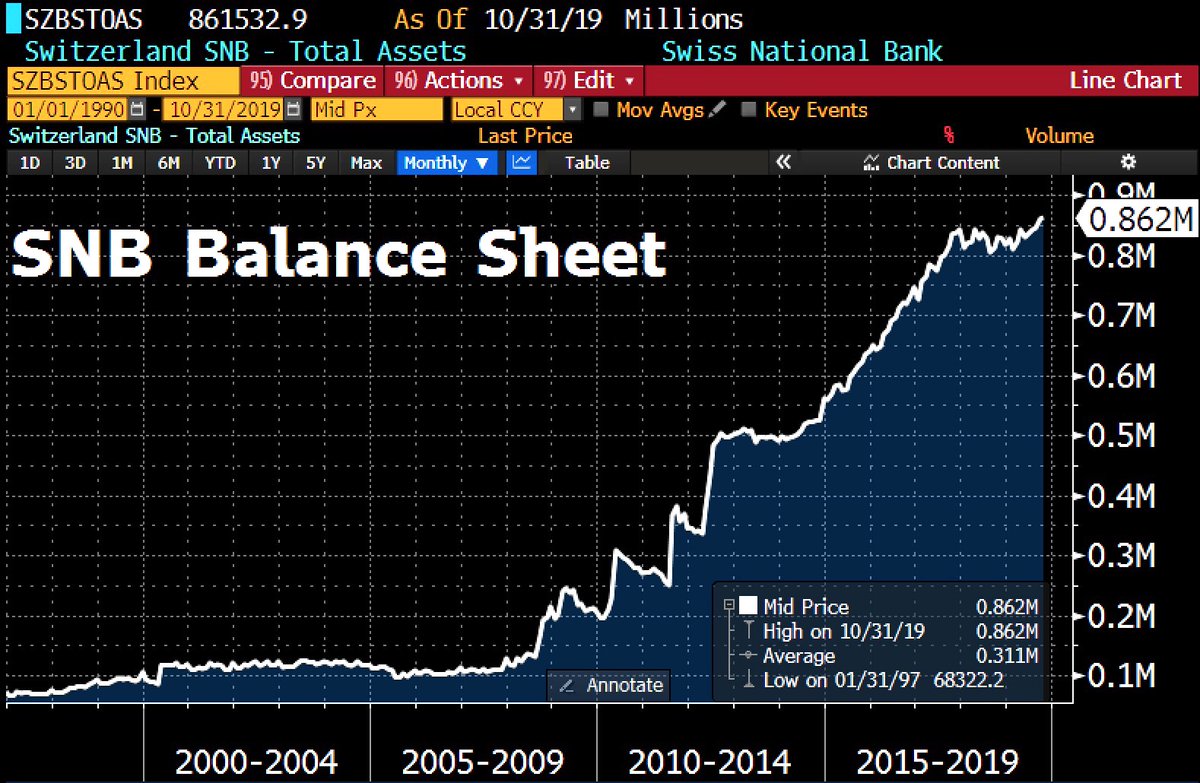

Swiss Central Bank could be required to pull its $800bn balance sheet out of investments in fossil fuel comps in a move by one of world’s biggest reserve banks to tackle climate change. Swiss lawmakers are preparing a campaign. http://news.trust.org/item/20191210104145-back7/…

Investing is all about probabilities. If the perceived odds of an event are high, certain securities will be priced based on those expected probabilities. The corollary is that when an event is perceived as almost impossible, securities do not price in any chance of it occurring. If that event does occur, all sorts of securities need to re-price—often quite rapidly. I like to spend my time pondering what potential events the market completely ignores. Of all potential economic outcomes, the one that is least anticipated and least priced in, is an uptick in inflation.

It is said that generals always fight the last war. In terms of macro-portfolio wars, Japan’s experience with deflation colors all views. This seems odd to me because we have over two millennia of history showing inflation and currency debasements to be universal constants, with one outlier in Japan. The question is if Japan is the new normal or a true outlier?

Academics have studied the causes and effects of inflation ever since emperors and kings fixated on halting its effects. Despite a massive body of work, there is little agreement amongst experts on the causes of inflation. Since I tend to ignore “experts,” let me start by giving you the Kuppy definition of inflation. “Inflation is when too much of a certain currency chases a scarce resource and pushes its price higher when defined in terms of that currency.” Using that definition, we’ve actually had rather dramatic inflation over the past decade—it just hasn’t shown up yet in the core consumer goods that central bankers are often concerned about.

Did they time-stamp the cyclical low in yields?

When a country prints money, no one knows where within the economic ecosystem it will ultimately flow. If a resource is scarce, it tends to experience inflation—when it is artificially scarce, it has even more extreme inflation. Just think of where the money printing has ended up this cycle; bonds (central banks restricted supply by buying them), stocks (PE and buybacks have restricted supply), gateway city residential housing (local municipalities have restricted supply), medical costs (systematic dysfunction has restricted supply), vintage wines (they aren’t being produced anymore), college education (supply restricted again), I can go on, but you get the point. Meanwhile, traditional inflation stalwarts like food and energy have remained suppressed due to technological advancements, reduced logistical costs and excess liquidity, which has allowed capacity to overshoot and lead to price deflation. To say that we’ve not had inflation over the past decade is wrong, we just haven’t had inflation in places that are key components of the CPI basket.

However, that may be changing. I believe that the number of sectors with restricted supply are starting to expand. Let’s look at labor, which historically has been a primary source of inflation. It’s no secret that US unemployment is at historic lows, laborers now have bargaining power and wages are rapidly increasing—with increases made more extreme by minimum wage laws, healthcare inflation and new mandates in various states. The cost of labor goes into almost every finished good—particularly in a labor-intensive service economy. Politicians on both sides seem willing to pass laws that give labor a bigger share of the pie—what will that do to inflation?

Now think of energy; it’s a crazy world out there and global energy security is no longer guaranteed. Prices have been suppressed for the past few years by excess production due to uneconomic shale—that’s clearly reversing as the funding has been cut off. Where do you think energy prices go if shale growth flat-lines or goes in reverse? What about when key producing regions devolve into chaos? Tanker rates are also expanding—that increases energy prices as well.

Now think about consumer goods; the past few decades were all about increased globalization where manufacturing migrated to the cheapest possible location. Trade wars and regional balkanization upend this trend. Now there ought to be an implicit geopolitical risk premium priced into gross margins on every good. Supply chain disruptions further increase costs. If globalism was deflationary, isn’t the reverse inflationary?

Think about what venture capital has done to costs. Thousands of businesses are losing hundreds of billions a year to gain market share in rather prosaic industries. Think about what Uber has done to transport costs or Chewy has done to the cost of dog food. These are all subsidized by VC firms so they can dump IPOs on unsuspecting retail bag-holders. As these businesses are forced to raise pricing in order to become sustainable, what will that do to consumer inflation? Won’t all sorts of sectors also gain pricing power, now that they don’t have to compete with someone who sells a Dollar for 80 cents hoping to make it up with volume? Isn’t the collapse of the Ponzi Sector bubble inherently inflationary?

What about all the supply restriction as ESG takes its toll on economies? If you can’t get permits to build a new coal mine or oil pipeline, yet demand keeps growing, won’t pricing increase as well?

I can go on and on. All the trends that were deflationary are slowly going in reverse. We haven’t seen the effects of this show up in the data yet, largely because the global economy is rapidly deteriorating, which is putting a brake on the demand side. However, even with the global economy slowing, inflation is starting to tick up in the US. Can the rest of the world be far behind us?

Of course, government policy drives all of this. I think it is obvious that we’ve finally reached the limits of monetary policy. Does the ECB taking rates 10 basis points more negative do anything but accelerate the bankruptcy of the Eurozone banking system? Does it increase consumption or capital expenditures? Of course not. If anything, it just starves the system of capital by taking everyone’s return on capital investment down towards zero and below. Who invests when expected returns are negative? What the world needs is a big reset of the system where leveraged firms default, solvent firms pick up the pieces and get to earn excess returns due to their past fiscal sobriety. Since we live in a democracy, that won’t happen, instead we will have extreme fiscal stimulus in order to kick the can further down the road.

In October, I spent 15 hours in the Sheremetyevo airport in Moscow (damn connecting flight never showed). It hasn’t seen a dollar of cap-ex in years, but it’s still light years ahead of LaGuardia or LAX. Just wait until corporations learn how much they can make from a never-ending airport renovation project. Now multiply that by hundreds of airports in America that desperately need capital investment. Now add bridges, roads, bullet trains, water infrastructure and our electrical grid. Why are all the lobbyists trying to get us into wars with third world nations? Corporations would make more money fixing our infrastructure and it’s going to be a lot less politically contentious.

If you think deflation is a fact of life, you clearly haven’t paid attention to history. Governments around the world have experienced a unique decade where they ran deficits and printed money without “bad inflation” which upsets voters. They think this is a new normal with no consequences. It isn’t. They’re already panicking with the S&P a few ticks from all-time highs. Soon politicians will go into ludicrous mode with fiscal stimulus.

What will fiscal stimulus do to the equity market? I’m reminded of the 1970s—inflation is no friend to most stocks. What happens to trillions in negative yielding long-dated bonds if inflation ticks up? What happens to bond proxies like global large-cap equity indexes or real estate? What happens to risk-parity funds that are leveraged a few times over expecting bonds and equities to increase over time? What if both legs of the trade drop at the same time? No one is ready for inflation, but I believe it’s coming. Maybe not today or next week, but there is a powder keg of monetary supply just waiting to be unleashed by governments who think that inflation can never happen again. At first, markets will cheer a bit of inflation—then they’ll panic. The markets often do whatever the fewest people are positioned for. Who’s positioned for inflation? That’s about as contrarian as buying Argentine sovereign debt.

I think the road-map ahead is a market crash, followed by obscene fiscal stimulus. As always, I’m trying to think a few steps ahead here. I’m making a list of beat-down sectors who benefit from this change in government policy. I want to be ready to buy as soon as they get serious about unleashing the stimulus. You need a crisis that’s severe enough that both political parties can agree on stimulus. We’re not there yet, but we will be. If you thought QE was nutty, wait until you see what drunken sailor mode looks like. Inflation is coming. Be VERY careful if you own assets with duration risk.

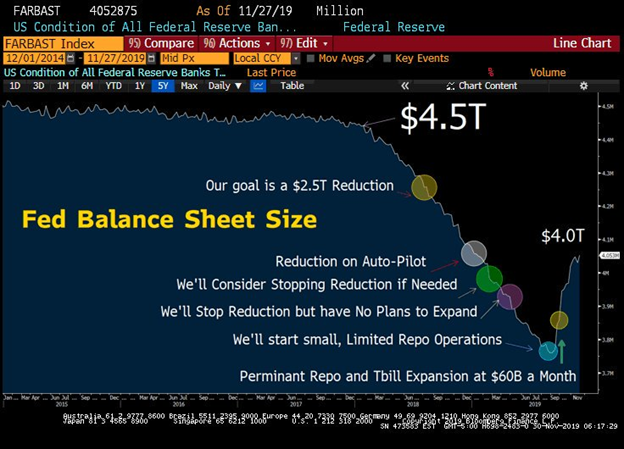

What kept the markets rally going in November? The chart below has all the answers. Fed’s balance sheet at $4.05 trillion, highest level since Jan 9, up $293 billion over the last 3 months.

But as per Jerome Powell “This

is not QE.”

I think we will see even faster growth with year-end funding pressure, surpassing in a few months the all-time high of $4.5T in Jan 2015.

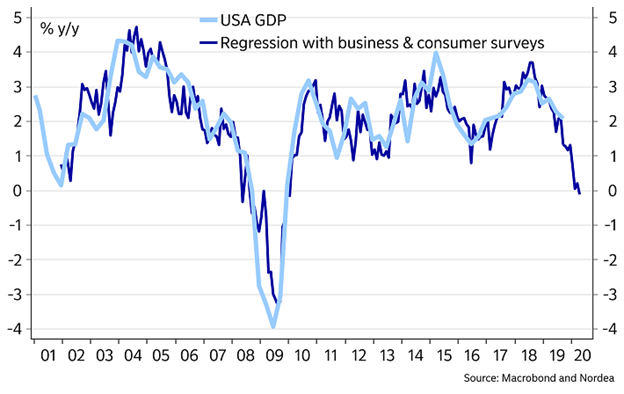

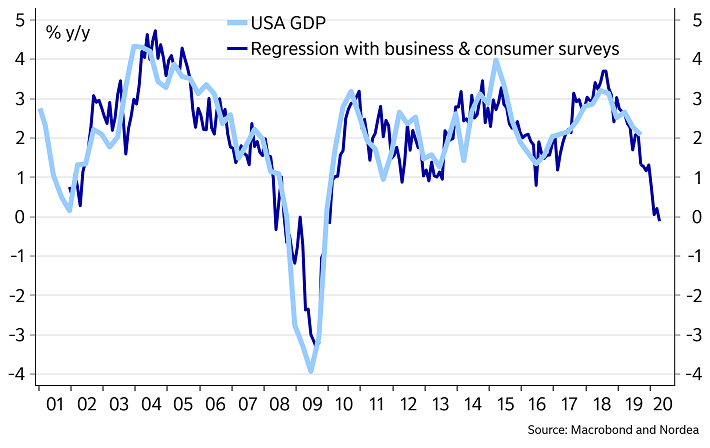

The FOMO (Fear of Missing Out) continues as I had outlined in my previous month outlook. The economic data continues to worsen except for Chinese PMI (in case you believe the Chinese data). US GDP growth for Q4 and Q1 2020 is tracking 0%, yes that is Zero as per Nordea. This is what a trillion-dollar fiscal deficit buys for you now a days. Yikes!

Markets are now completely detached

from reality because we are in PE expansionary phase supported by monetary

policy.

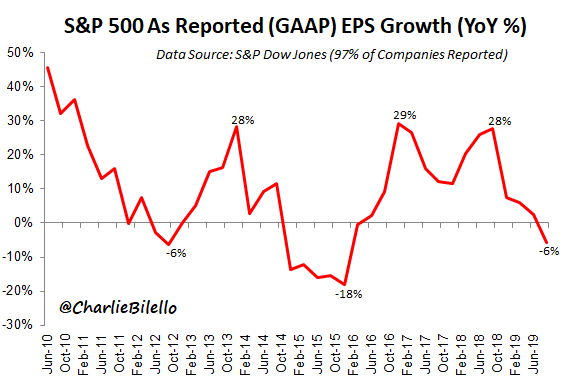

97% of companies reported S&P 500 GAAP earnings were down 6% over the past year – largest decline since Q4 2015 https://twitter.com/charliebilello

One more chart to satisfy you that we are living in a utopian world

How many of you missed the most important news headlines over last few days? No, it is not about trade war or North Korea, but an almost silent generational change in monetary and fiscal policy.

This one freshly baked out of ECB oven.

And now for the new role for Ex BOE governor.

FED wants to allow inflation

to run “ HOT” , ECB wants a role in funding “ GREEN BONDS” out of its balance

sheet and Mark Carney is there at UN to help shape world policy on funding

climate change because we are told it is an “ existential threat”.

The new MMT (Modern Monetary

Theory) is taking shape under the guise of preventing “CLIMATE CHANGE”.

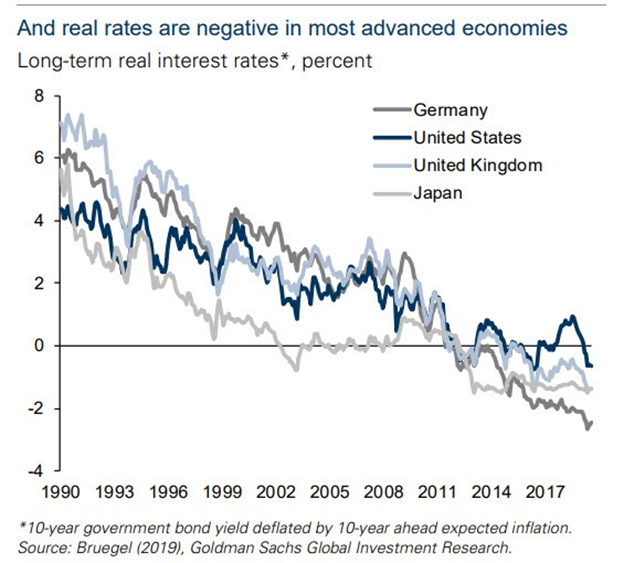

Thankfully for those who are playing this game, they have support in the form of negative real rates across the developed world which will soon be replicated in developing world. This will force more and more savers to consume or seek out risk assets rather than save and pension funds to take on more risk to maintain the desired level of promised returns.

Market outlook

Well I could sense the change in monetary policy but chose to play by going long commodities and volatility over Equity (I sometimes hate that I am ahead of the curve) and since we are all conditioned by environment and career risk in short term, portfolio managers did what they are supposed to do in November to keep their bonus and job intact by buying what matters most “ EQUITIES” in the face of rising inflation and wage pressure. Never mind, the winds are changing, and precious metal and other commodities equities have now started outperforming the Global Equities. This trend change is still in nascent stage and I expect it to pick up steam as we enter into the first quarter of next year.

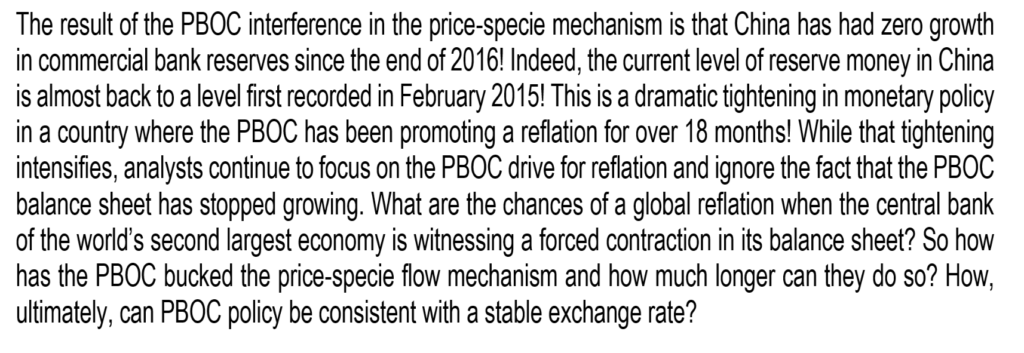

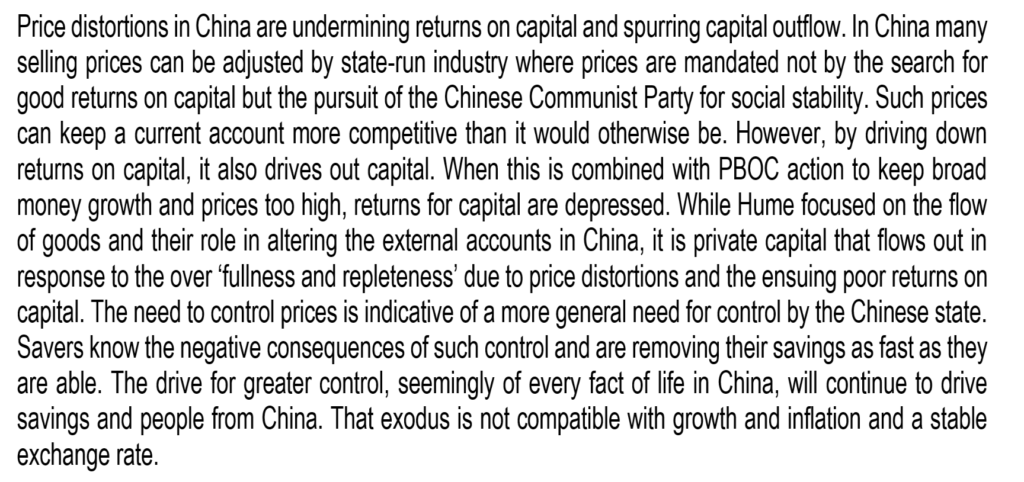

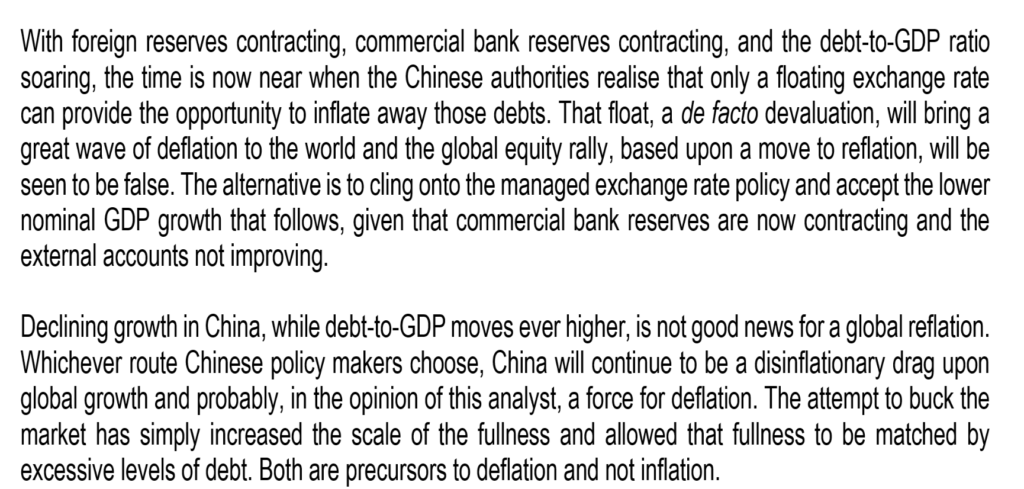

Russell is my all time favourite strategist and this article https://www.eri-c.com/news/303 on the dilemma facing the People Bank of China is a must read.

I have take screen shot of some interesting paragraph which will tell you that china is in serious trouble.

China has seen zero growth in their commercial bank reserves since 2015

why is China see huge capital outflows and the return on capital is so depressed in china

why the endgame can only be global deflation

My two cents

The only way out for China is by currency devaluation or getting more capital inflows than outflows to increase the bank’s reserve and liquify the economy. This is why China made adjustments for its markets to be included in MSCI and Barclays indexes. IF those inflows don’t materialize then China will have no choice than to either allow its domestic economic growth to collapse or inflate away its debt be devaluing

“ESG stands for “Environmental, Social and Governance.” I can certainly understand why some individuals or groups may object to investing in various industries. It’s their capital and they can choose to allocate it as they see fit. When they are sizable clients, they can force portfolio managers to divest certain businesses and not make new investments in certain sectors. This all seems logical—the client is always right. However, at this point, ESG has been taken to such an extreme that it is bordering on silly.

Keep in mind that the vast majority of portfolio managers under-perform their benchmarks and only attract fund flows through their marketing departments. Why miss out on fee-earning capital because you haven’t adapted an ESG mandate? Coal? Nope. Oil and gas? Won’t touch it. Tobacco? Bad. Those are obvious, but where will they draw the line? Why not ban soda? That’s just diabetes in a can. Is social media next? What about entertainment—that’s sure to offend someone. What if you don’t agree with a country’s politics? Do you write off whole continents? Clearly, there’s a problem here. You could end up with large portions of the global economy on the no-go list. Once again, I respect an individual’s decision to forgo a particular investment for ideological reasons, but as a consequence, whole sectors of the economy are now cut off from capital.”

Asset price is a simple case of demand and supply. The following words from Agnico eagle CEO ( one of the largest gold miner in the world) will tell you the supply situation. Smart investors already know about the demand picture

There is just so much demand for money printing these days from latin american countries like Venezuela and Argentina then it is strange for one of the biggest currency printer to in the world (De La Rue) to shock the markets with financial loss and cancel dividend.

below is the stock price chart in British Pound

People aren’t moving and I am scratching my head “why”?

Yes it is a myth. Dollar and Gold have absolutely no long term correlation. The only thing GOLD responds to is real rates ( Nominal- Inflation). If they are negative then GOLD will go up otherwise ” why should the GOLD go up”

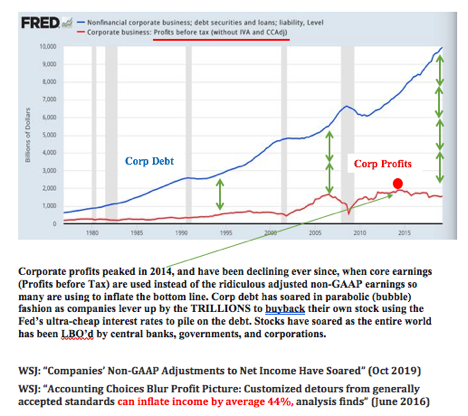

Corporate Management teams are LBO’ing themselves with cheap debt (Thx Fed) to reduce share counts and increase stock values (time shift) now to enrich themselves at the expense of employees and future investors stuck with all the debt.( @MI_investments)

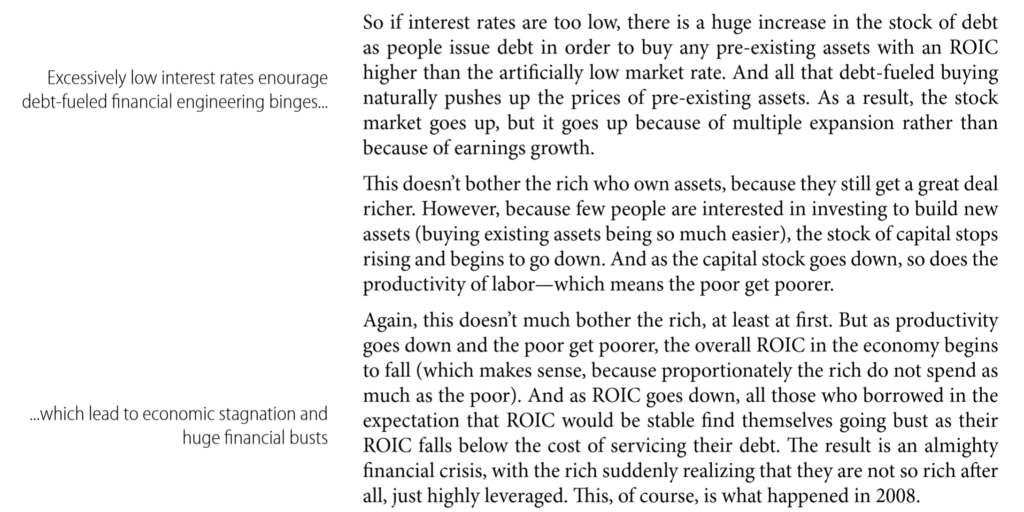

Why low interest rates do not encourage Investment but promote consumption (Gavekal Research)

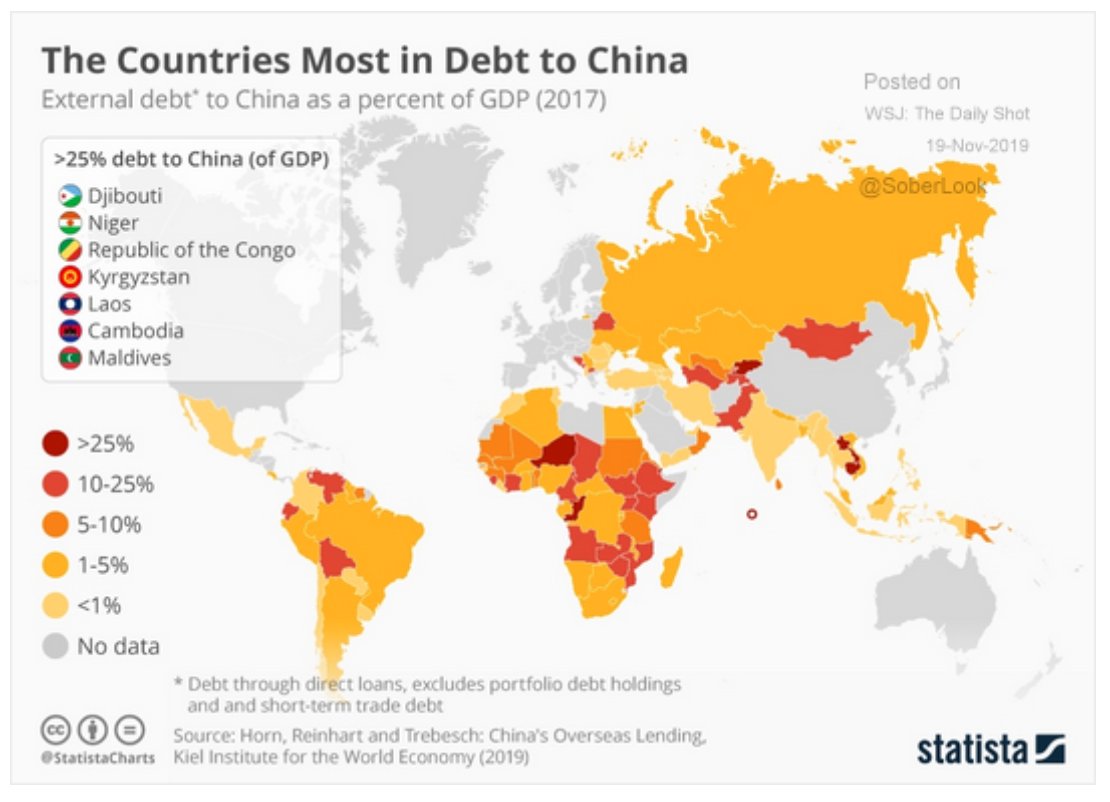

What do Dijbouti, Niger, Republic of Congo , Kyrgyzstan, Laos, Cambodia, Maldives have in common? They all owe China debts worth more than 25 % of GDP.

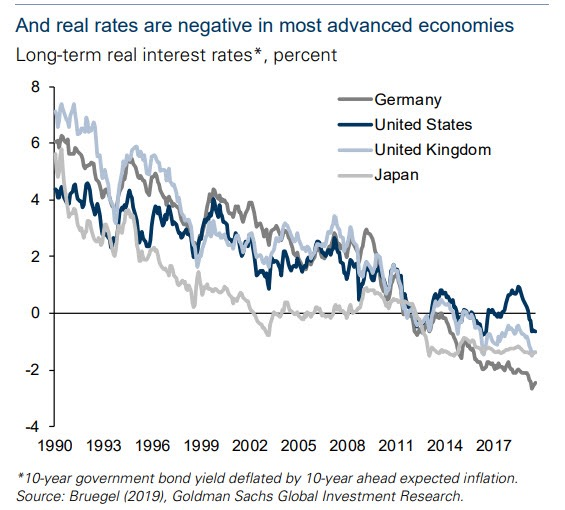

Real rates are now negative across the developed world. Government wants you to borrow, spend and consume.Smart people are running into assets which have positive yield.This is why there is relentless bid in different asset classes irrespective of fundamentals

There is a laundry list of dangerous assets bubbles in the global financial markets today that have built up over a record long US economic expansion:

Highest ever global debt to GDP levels;

A passive investing and ETF craze that has led to historic lofty US equity valuations across a composite of fundamental measures tracked by Crescat;

Impossibly valued currency and credit markets in China at an extreme for any large country relative to the size of its economy;

China’s banking assets are valued at USD 41 trillion, including substantial hidden non-performing loans in our analysis, a major mismatch compared to its much smaller and stumbling 13.6 trillion GDP economy;

Record $17 trillion of negative yielding sovereign debt which may have just peaked in August 2019;

Private equity/VC excesses in opaque assets, highly leveraged companies, and frequently unprofitable businesses masquerading as new economy disruptors;

Record indebtedness of US public and private corporations combined relative to GDP;

Crowded “risk parity” positioning among large hedge funds and institutions who are long stocks paired with leveraged long bonds, a strategy that worked exceptionally well in a forty-year backtest as well as the last ten years that it has become popular, but it’s a strategy that would likely get decimated in a rising inflation paradigm;

Fashionable short volatility strategies which are yield enhancement strategies for an income starved world, but the extra yield is earned in exchange for accepting asymmetric downside risk;

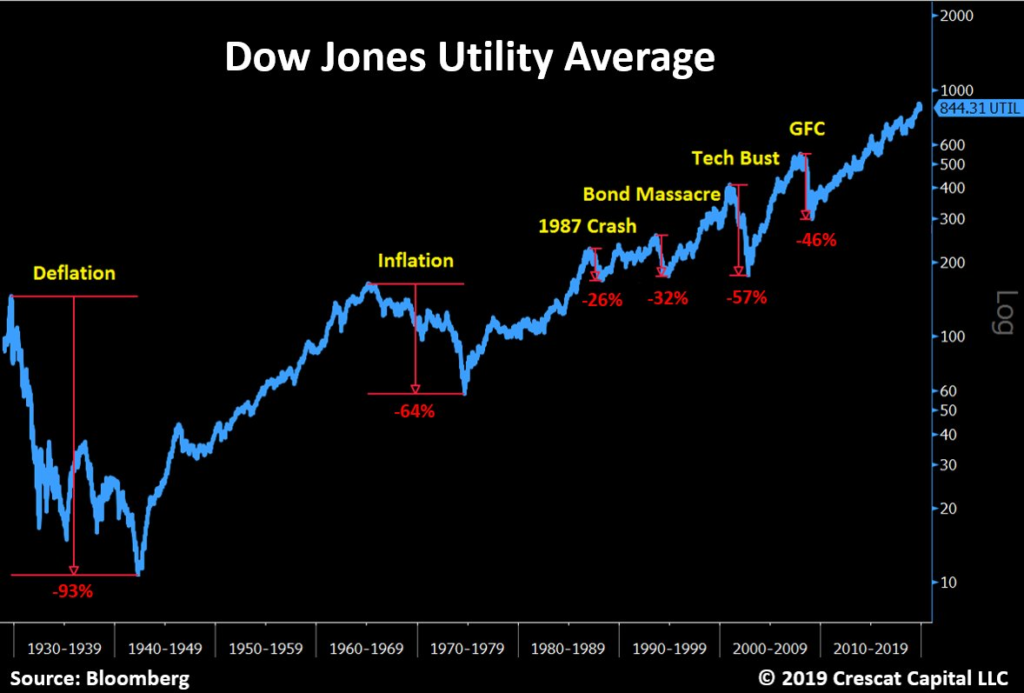

High valuations and crowding into sectors traditionally viewed as defensive (including utilities, REITs, and consumer staples) with utilities being the most fundamentally questionable among them in our view; and

Tech bubble 2.0 with extraordinary valuations in SaaS, certain FANG+ stocks, many recent IPOs.

Catalysts

The unwinding of these imbalances is likely to be highly destructive to the investment portfolios of unprepared global savers today. Below, we list the confluence of macroeconomic timing signals, including social and geopolitical forces, now bearing down for an assault on overvalued financial assets. Most of these have been uncanny warning signs directly ahead of past bear markets and business cycle peaks.

In the US:

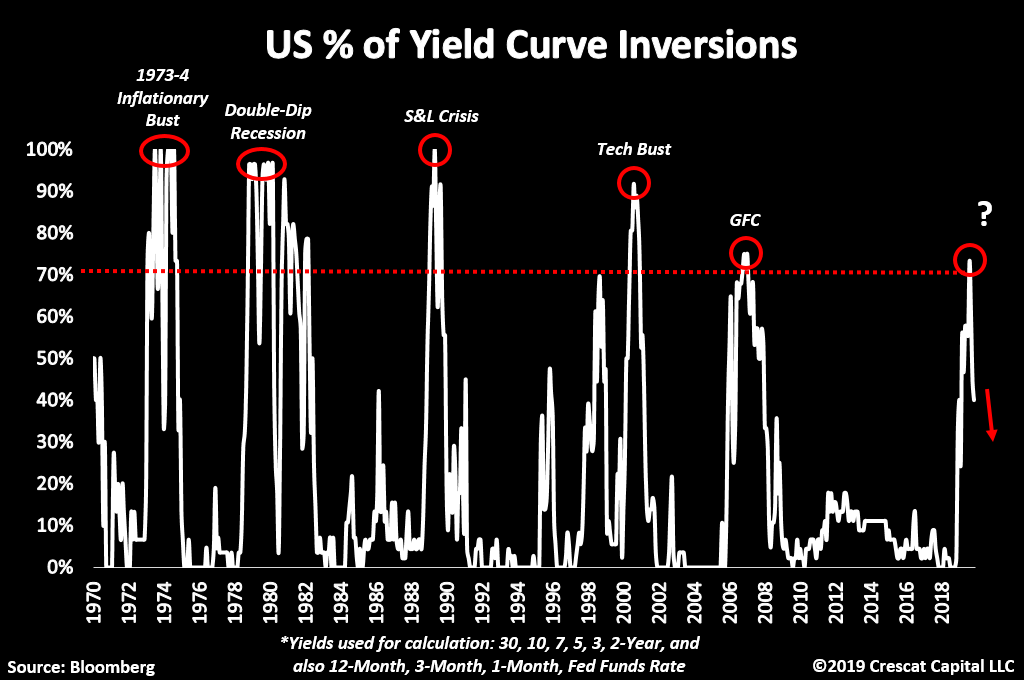

The Treasury yield curve recently exceeded the critical 70% inversion threshold that has preceded each of the last six recessions with no false signals;

The Conference Board’s consumer expectations survey has diverged strongly to the downside compared to its unsustainably high present situation index;

Job openings are declining while the lagging and contrarian unemployment rate is at cyclical lows;

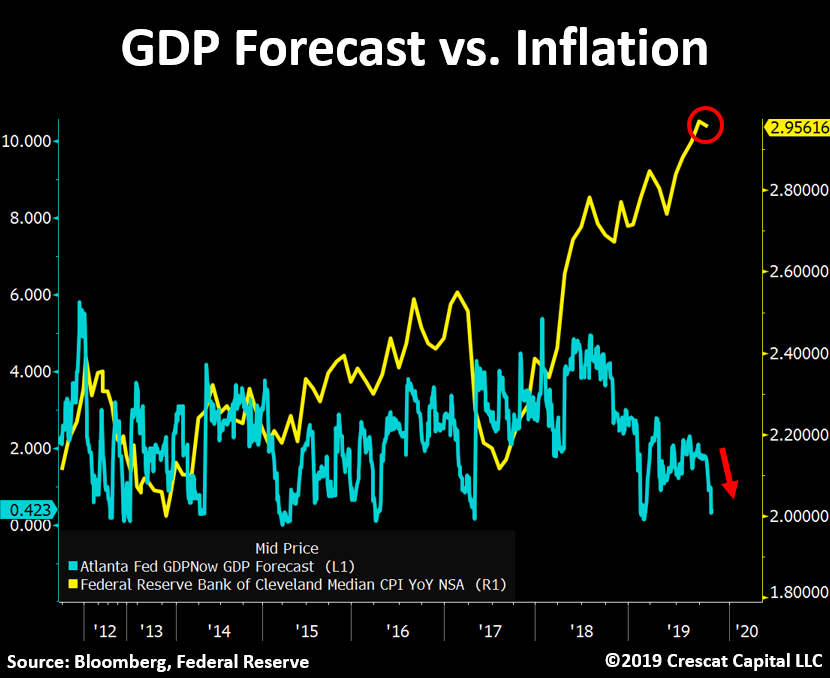

Both the Atlanta and New York Fed’s real-time GDP trackers have been trending steadily down for almost two years and appear to be approaching recessionary levels;

Corporate earnings of the Russell 3000 already contracted on a year-over-year basis in the last reported quarter;

US share buybacks are now 30% lower than 2018;

Increased insider selling of stocks;

Declining CEO/CFO confidence surveys;

M&A transactions drying up;

ISM manufacturing PMI at recessionary levels;

Construction spending declining;

Bearish deteriorating stock market breadth while indices reach highs;

Implied volatility for stocks retesting low levels that preceded previous selloffs;

Smart money flow index diverging from the recent run-up in the S&P 500;

Leveraged loans stumbling;

Busted/delayed/cancelled IPOs;

Recent liquidity crisis that spiked interest rates in the overnight US Treasury rehypothecation market;

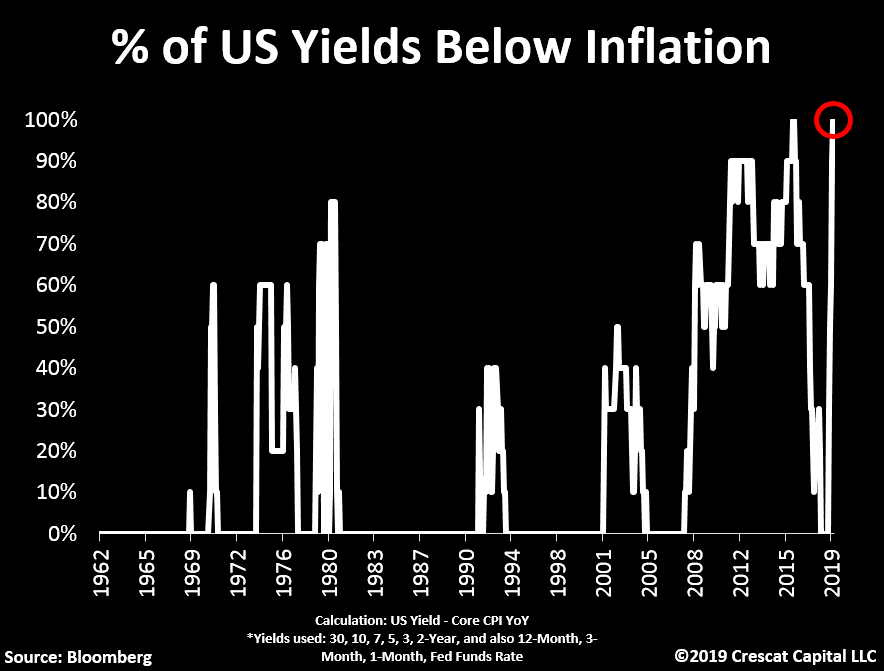

Inflation rate above the entire Treasury yield curve;

Core and median CPI at 10-year highs diverging from long-term inflation expectations at 40-year lows;

Capacity utilization now falling;

Commercial & industrial loans declining the most since the housing bust;

Auto loan spreads rising as delinquency rates rise;

Net exports of services now falling the most since the GFC and tech bust;

Increased election uncertainty and rising political polarization creates an unknown binary outcome for future tax policy which is now friendly for financial markets but could swing 180 degrees;

Trump impeachment proceedings might impair his credibility in maintaining a hyped-up economic narrative in face of deteriorating macro fundamentals; and

New bipartisan willingness to embrace fiscal stimulus and rising government deficits could change the inflation paradigm sooner rather than later and be detrimental to financial assets.

Worldwide:

Yield curve inversion with the US dollar as the world reserve currency versus an unprecedented 19 economies now with 30-year yields below USD Libor overnight rates;

Like the US, Hong Kong, Canada, and Japan all recently breached critical 70% inversion levels within their own yield curves;

Emerging market currencies have been falling despite recent easy Fed policies indicating that dollar liquidity globally is still tight amidst record dollar-denominated foreign debt;

Ongoing trade and cold war between the world’s two leading economies with diametrically opposed political systems, each with its own historically extreme financial imbalances;

China yuan recently broke the key 7 level and looks poised for an accelerated devaluation that would almost certainly take global investors by surprise;

Tariff increases that go into effect in December are a catalyst for an RMB shock if trade negotiations continue to stall which is our base case;

Accelerated yuan depreciation is the rhino in the room that would be a likely contagious global risk-off event feeding back to US, European, as well as other Asian and emerging markets as we have seen on multiple occasions already since 2015 with only minor devaluations;

There have already been material disruptions in the global manufacturing supply chain due to the trade war;

Frontloading of Chinese semiconductor inventory and CAPEX spending in 2019 amidst the threat of escalating US intellectual property purchase restrictions sets up earnings weakness ahead for this market leading but cyclically vulnerable industry;

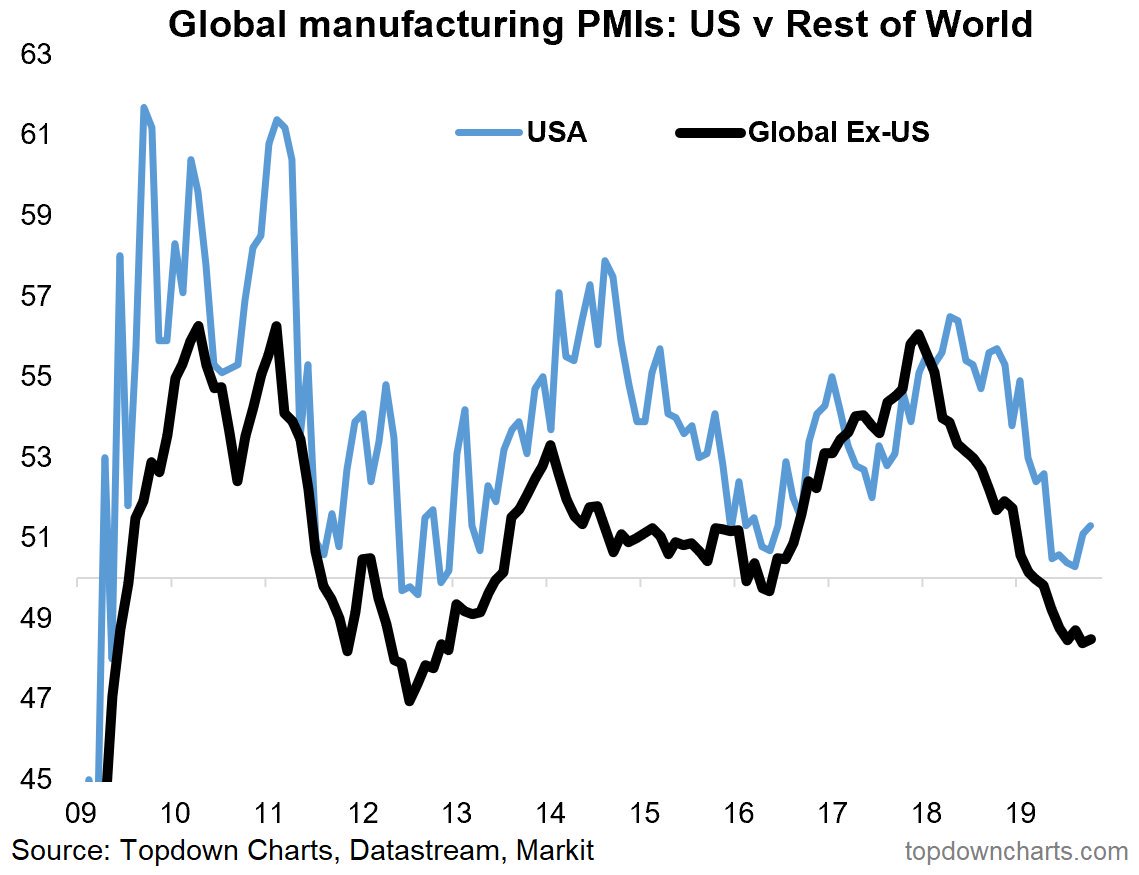

The global manufacturing PMI has already dropped to recessionary levels;

Multiple political and economic crises have already been erupting in emerging and frontier markets;

Rising populism and nationalism more generally around the globe is causing disruption in world trade and financial markets; and

Last but not least, Brexit.

The two closest analogs to today’s excessive fundamental valuations for US stocks were the 2000 Tech Bubble and the culmination of the Roaring Twenties in 1929. Our work suggests that today’s valuations are even higher than those two periods. The nifty fifty stock mania of 1972 is another comparable period that featured excessive valuations in a popular group of large cap growth stocks that became widely regarded as “blue-chip” buy and hold positions. Institutions and retail investors were taught to cling to these stocks through thick and thin, throwing fundamental analysis and valuation principles out the window. The same idea is the prevalent passive investing dogma of today.

From today’s valuations, a mere cyclical mean reversion in stock market multiples implies a 50+% drawdown in prices. Yet, too many investors remain oblivious to these valuation risks. Many today have further been lulled into believing that central banks have their backs and will keep markets rising. Such bullish sentiment on the heels of recent Fed liquidity injections has emboldened a late cycle speculative push higher in the indices even as the market internals have been noticeably deteriorating. Never mind that the last two Fed easing cycles after tightening cycles coincided with and were confirmations of major bear markets and recessions underway rather than prevention of them.

A Perfect Predictor of Recessions, so Far

The recent distortions in the US Treasury yield curve are among the most relevant macro indicators supporting Crescat’s bearish thesis and positioning today. Our comprehensive calculation shows that across all 44 spreads of the yield curve, the percentage of them that are inverted spiked to 73% just three months ago in August. This is a critical timing signal as we show in the chart below, because in the five prior business cycle expansions that we studied, we found that when 70% or more of the yield curve first inverts, a recession soon follows. In all but one case, those recessions were accompanied bear market declines in stocks. Three of them were close to 50% collapses in the S&P 500 Index.

How to Profit from Yield Curve Inversions

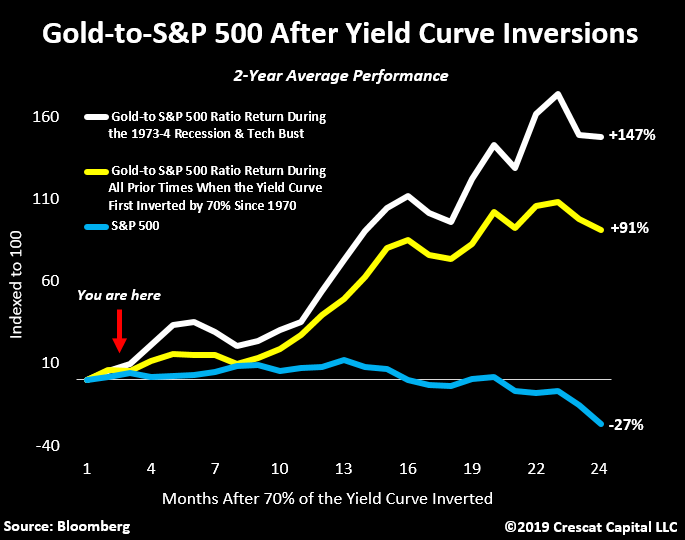

From a portfolio management perspective, we have determined that buying gold and selling stocks is one of the most compelling macro investment ideas after inversions reach excessive levels. Since 1970, our analysis shows that when the yield curve first exceeds 70% inversions in a business cycle expansion, the gold-to-S&P 500 ratio performed exceptionally well on average in the following two years returning close to 90% while stocks lost almost 1/3 of their value on average. The only time buying this ratio didn’t work was during the S&L crisis. Yet, back then, equity valuations were quite the opposite from today. We think the 70%+ inversions that immediately preceded the 1973-4 inflationary recession and tech bust have the most comparable setups to today. Both of those times, the numerator and denominator of this ratio worked extremely well for the ensuing 2-year period resulting in an average gain in the gold-to-S&P 500 ratio of 147% excluding dividends! The intriguing fact here is that the commodities-to-equity ratio was near historic lows at the peak of those two stock bubbles (Nifty Fifty and Tech) as shown by the first chart in our letter above. Today’s macro set up looks remarkably similar, perhaps even more extreme. Gold is near record undervalued relative to the size of global monetary base and money supply. At the same time, equity valuations relative to their underlying fundamentals are arguably at their highest ever.

Negative Real Rates Across the Whole Treasury Curve – Uber Bullish for Gold

The entire Treasury curve now yields less than core CPI. It’s the second time in history we have seen this, the first being in early 2016. That time, the Fed had already hiked rates at the end of 2015 and was in quantitative tightening mode. This time, the Fed has cut interest rates three times in three months and has returned to quantitative easing at an alarming 45% annualized rate. With $15+ trillion worth of sovereign bonds with negative yields and central banks easing globally, we believe precious metals are in the early stages of a multi-year bull market.

Economy Weakening as Inflation Rising

When we look at the chain of events historically, it’s Fed tightening late in the business cycle that leads to yield curve inversions and then recessions. By the time the Fed starts easing, it’s a confirmation that the downturn is ripe to unfold. When such times have also coincided with stocks at record valuations, severe equity bear markets have ensued. Today, given the historic levels of debt and macro imbalances worldwide, the next decline could easily be among the worst in US history. Given all the warning signs, we think investors should prepare urgently if they have not already. In our view, a new wave of global fiat debasement policies is in its early stages and a shift in the inflation paradigm could be near. To get a glimpse of this in the US, note how the Atlanta Fed’s GDP nowcast has been declining in the face of rising consumer prices. This scenario could be extremely bullish for scarce and non-dilutable forms of haven assets such as precious metals.

At Crescat, precious metals are overwhelmingly our preferred hedge against fiat money printing and over-valued financial assets. It’s important to note that cryptocurrencies provide an additional outlet for investors to flee stocks and bonds as well as fiat currencies today and thereby to help make rising inflation in those currencies a self-fulfilling prophecy. Bitcoin is a bet on technology and cryptography as well as a vehicle to disrupt and even circumvent government control over money. Bitcoin is limited in supply like precious metals and in that sense could be a valuable call option on inflation. As the first mover, it has the network-effect advantage over other cryptocurrencies which are abundant and therefore unlike precious metals as an asset class. We believe a small position in bitcoin could provide diversification and hedging with significant upside, but we do not advocate for more than one or two percent of a portfolio at this time given its high risk. For those living under authoritarian governments with strict capital controls, it is important to note that cryptocurrencies provide a functional and disruptive means of escape which plays into our bearish view on the Chinese yuan.

In the wake of the 2008-9 crisis, central banks starved investors for yield in attempt to generate new borrowing and spending and thereby grow the economy. But in the absence of significant fiscal stimulus to go along with it, extraordinary monetary policy mainly served to generate extreme expansion in value of financial assets with only muted economic growth and real-world inflation to go along with it. Monetary stimulus alone thus increased the wealth disparity between the rich who disproportionately own stocks and bonds compared to the more generally debt-laden masses. It is thus no surprise that today we have a fertile breeding ground for rising populism and nationalism and their financial bubble bursting implications, including trade wars, and deglobalization.

Repo Liquidity Crisis a Wake-up Call to China Risks

When today’s plethora of macro imbalances begin to unwind, we fully expect that Fed intervention will again be necessary to attempt to ease the pain of collapsing asset prices. The rehypothecation (repo) liquidity crisis that we just experienced in September is a new kind of wake-up call. Like in 2008, a freeze up in the interbank credit markets is a sign that a large financial institution somewhere on the planet may be on the brink of collapse. The Fed indeed has already responded with emergency liquidity injections. We can only imagine that a large and wobbling Chinese bank needs US dollars and has been attempting to pledge Treasuries to borrow them. Perhaps other banks stepped away for fear that those Treasuries had already been pledged too many times over and nobody really knows who would get them if the music stopped. We are not saying that is what happened in September. We don’t know what exactly happened. The Fed has been carefully guarding the true story, but it has also continued in emergency QE mode for the last three months. What we are saying is that there is indeed substantial financial market risk today because of the truly insane imbalances that have built up inside the Chinese banking system. Based on our macro research, we believe the PBOC has already more than fully encumbered its foreign exchange reserves in its effort to keep its currency from collapsing to date. The recent surprise new money printing from the Fed is confirmation that there are indeed real problems beginning to surface in the global capital markets. The Fed’s role, to be clear, if China’s banking imbalances are indeed finally poised to unwind, is not to rescue Chinese banks, rather to rescue the US banks that are their counterparties.

So, while today’s US stock market has many parallels to 1929, 1972, and 2000 in terms of valuation and downside risk, it also has some to parallels to 2008 with the potential for banking liquidity crises in the interbank dollar funding markets. We are much less concerned about the risk of an actual collapse of the US banking system today because the Fed has proven its willingness and ability to swiftly step in there.

Ultimately, we believe combined fiscal and monetary stimulus will be applied in concert to combat the next market and economic downturn. We strongly believe that too many investors today are underestimating the future inflationary risk of this high likelihood. The problem is the recency bias of the post-GFC world where central bank easing failed to generate the inflation that was feared at that time. The reason it didn’t is that, outside of China, the accompanying fiscal expansion was absent. The chessboard looks much different today. The willingness to embrace new monetary and fiscal experiments today is high and they will come at a cost.

Such a political climate is particularly troublesome for stock and bond bulls today because rising inflation would almost certainly be a killer of today’s financial asset euphoria. If one is going to buy stocks at all in this environment, one area that looks extremely attractive with low valuations and improving fundamentals is gold and silver mining stocks. Many of these companies have low valuations, improving growth, and strong positive free cash flow already, after going through a bear market from 2011 to early 2016. After four years of base building, we believe they are poised to take off fundamentally and technically in a soon to be rising gold and silver price environment.

Why Crescat

Many investors are not even aware of the extreme valuations in the financial markets today at this likely critical macro inflection point in the global economy. For who are aware of these imbalances, many are not willing to do very much about them in their portfolios for fear of going against the crowd.

For those who are willing to do something about it, they may be inclined to move toward conventional defensive long positions and thereby may be crowding into a different kind of mania, such as utility stocks, which in reality have a horrific track record of protecting wealth during bear markets and recessions as we show below in the chart below going back to 1929

At Crescat, we believe have a better way of investing ahead of a probable downturn in the business cycle across multiple themes. In our global macro hedge fund, we are expressing what we believe is the macro trade of the century based on our three highest conviction themes:

Long precious metals including mining stocks;

Shorts select overvalued US and global equities; and

Short the China yuan and Hong Kong dollar through asymmetric risk put options

The truth is that not many professional money managers are willing to be significantly short stocks. Even most hedge funds tend to be net-long funds and only rarely attempt to tactically time markets. We are not perma-bears by any means but are indeed attempting to tactically time the market today based on our macro models and themes given our strong views on the current unprecedented euphoria and abundance of catalysts for an imminent downturn. Our goal is to grow and protect wealth by capitalizing on it.

We are somewhat unique as a macro fund in that we believe in security selection in addition to broad macro trades. For instance, we prefer to pick individual equity longs and shorts based on our models to express our themes and generate outperformance (alpha) rather than just getting index (beta) exposure to express a macro trade. We have demonstrated our ability to generate alpha in stocks over time in our Large Cap and Long/Short strategies.

Furthermore, we are value investors which give us intrepid confidence to hold a portfolio that we believe is worth substantially more (or less in the case of our shorts) than the market is valuing it at any point in time. Within the context of our risk model, we are willing to ride with the fluctuations in the market’s pricing of our positions knowing that is what can also drive significant upside as the true value of our holdings ultimately becomes recognized.

Thus, we can be secure in maintaining our substantial US equity net short position today in each of our hedge funds at the same time as a frenzied Wall Street is trying to squeeze the last juice out of a record overvalued market historically late in the business cycle while oblivious to many of the risks that we see.