• How to deal with an accumulation of public & private debt without inflation ? • Asia (mostly China) will lead in new technology and will shape Globalization on its on terms

• China+India = 44% of global growth contribution by 2024

• Low growth and perception of higher inequality will lead to more frequent social unrest (Helicopter Money? Tax on robots?)

• End of CB independence Investment

Investment

• Reduced returns due to lowflation, low interest rates and equity valuations

• Investors are likely to favor stocks over bonds

• Pension funds at risk

• Japanization of the European banking sector

• Monopolistic break-up of IT-giants

• More regulation Basel IV, V, VI etc.

• World of low/no asset management fees – Charles Schwab

The ratio line of large cap (Nifty) versus midcaps (Nifty Midcap Index).

For the first time in almost two years, the ratio is

shifting in favour of midcaps. Generally, such a shift would imply, emergence

of risk on attitude, rally getting broadbased. The midcap underperformance may

be ending too, leading to stock specific activity from the mid cap side of the

market.

Historically, a late surge in midcaps is also indicative

of the final move in the preexisting general bullish trend.

The chart presented above is a weekly…hence request to review it by the end of this week.

why I changed my dollar index view from positive to negative and falling dollar is generally associated with rising Emerging Markets and precious metals. It is possible that we see action in beaten down mid and small cap index vs the large cap index

M2 money supply has increased $796 billion y-t-d to $15.245 TN. With two months to go, 2019 M2 growth is on track to easily exceed 2016’s record $854 billion expansion. Recent M2 growth is nothing short of spectacular. M2 has jumped $329 billion in ten weeks, about an 11.5% annualized pace. Over 26 weeks, M2 surged $677 billion, or 9.3% annualized. One must go all the way back to the restart of QE in late 2012 to see a comparable surge in the money supply. Since the end of 2008, M2 has inflated $7.027 TN, or 86%.

Money Market Fund Assets (MMFA) have similarly exploded this year. Total MMFA have increased $517 billion year-to-date (to $3.555 TN), an almost 20% annualized rate. Like M2, six-month growth in MMFA has been extraordinary: expansion of $472 billion, or 35% annualized.

With MMFA at the highest level since 2009, bullish market pundits salivate at the thought of a wall of liquidity coming out of cash holdings to chase a surging equities marketplace. A Tuesday Wall Street Journal article (Ira Iosebashvili) is typical: “Ready to Boost Stocks: Investors’ Multitrillion Cash Hoard: Nervous investors have socked $3.4 trillion away in cash. But stocks are rising and their nerves are calming, leading bulls to view the huge cash pile as a sign that markets have room to go higher.”

And while MMFA are back to the 2009 level, it is worth pondering that money fund growth hasn’t been this robust since 2007. After ending April 2006 at $2.031 TN, money fund assets began growing rapidly, ending 2006 at $2.382 TN. And after expanding $154 billion, or 13% annualized, during 2007’s first-half, things went a little haywire. MMFA proceeded to surge $1.000 TN, or 53% annualized, over the next nine months. Recall that subprime erupted in the summer of 2007, with equities stumbling before regaining composure to trade to all-time highs in October.

August 17, 2007: The FOMC’s extraordinary inter-meeting policy adjustment: “To promote the restoration of orderly conditions in financial markets, the Federal Reserve Board approved temporary changes to its primary credit discount window facility. The Board approved a 50 bps reduction in the primary credit rate to 5-3/4%…” The FOMC then cut Fed funds 50 bps on September 18th, then another 25 bps both on October 31st and December 11th. The FOMC then slashed rates 75 bps in an unscheduled meeting on January 22, 2008, and another 50 bps on January 30th and another 75 bps on March 18th (to 2.00%).

Conventional thinking has it that market instability and risk aversion were behind the surge in MMFA. Yet there was also a notable acceleration of M2 money supply growth. After expanding at a 5.5% rate during 2007’s first-half, money supply growth surged to a 7.1% pace over the subsequent nine months.

2007 was a period of Extraordinary Monetary Disorder that manifested into acute market instability. Despite the dislocation that engulfed high-risk mortgage finance, Wall Street finance was “still dancing” right through the summer of 2007. Not only did stock prices ignore subprime ramifications, crude oil prices went on a moonshot – surging from about $70 mid-year to a high of $96 in November. After trading as low as 161 in August, the Bloomberg Commodities Index surged as much as 15% to trade to 186 in November. By June 2008, Monetary Disorder saw crude spike above $140, with the Bloomberg Commodities index almost reaching 240.

My long-held view is the Fed’s aggressive monetary stimulus in 2007 was a major contributor to late-cycle “Terminal Phase Excess” – and resulting Extraordinary Monetary Disorder – that came home to roost during the 2008 crisis. After trading as high as 5.30% in early June 2007, ten-year Treasury yields were 100 bps lower just three months later. Ten-year yields ended 2007 just above 4.00% and were as low as 3.31% by mid-March – a full 200 bps below yields from nine months earlier.

I believe a surge in speculative leverage played an instrumental role in the expansion of marketplace liquidity – that flowed into a rapid expansion of MMFA as well as M2 money supply. It’s worth noting the Fed’s Z.1 “Fed Funds and Repo” category posted Extraordinary growth during this period. After ending 2006 at $3.858 TN, “repos” increased $799 billion over five quarters to $4.657 TN (end of Q1 ’08).

Wall Street was indeed “still dancing” hard through the end of 2007. The Fed moved to bolster the economy in the face of heightened financial instability. The impact of stimulus measures on the real economy is debatable. My own view is that late-cycle stimulus is problematic, as it tends to stoke already overheated sectors and exacerbate imbalances and maladjustment. The impact of stimulus on finance should be indisputable. The upshot of deploying stimulus in a backdrop of market speculation is dangerous speculative Bubbles.

With the enormous growth of M2 and MMFA during 2007 and into 2008, how was it possible for markets to turn disastrously illiquid in the fall of 2008? Because the monetary expansion was being fueled by a precarious expansion of the “repo” market and securities speculative finance more generally. While markets – Treasuries, corporate Credit, equities, crude and commodities – were being driven by what appeared sustainable liquidity abundance, the source of this underlying monetary stimulus was acutely unstable speculative leveraging. And as the Fed cut rates, yields collapsed, stocks shot skyward and commodities went on a moonshot, the self-reinforcing nature of speculative excess (and leverage) fomenting acute Monetary Disorder.

Speculative blow-offs are a late-cycle phenomenon. Over the course of a boom cycle, financial innovation gathers momentum. The most aggressive risk-takers have proved the most successful, in the process attracting huge assets under management. The laggards come under intense pressure to chase performance with riskier portfolios. Out of necessity, caution is thrown to the wind. Between new instruments, products and strategies, market structure adapts to an environment of heightened risk-taking and leverage. In short, a speculative marketplace takes on a strong inflationary bias (upward price impulses). In such a backdrop, central bank monetary stimulus is extraordinarily potent – perhaps not so much for a late-cycle economic cycle, yet remarkably so for a ripened speculative cycle susceptible to “melt-up” dynamics.

I have posited that late-cycle dynamics turn increasingly precarious due to the widening divergence between a faltering economic Bubble and runaway speculative market Bubbles. This was certainly the case in the second-half of 2007 and into 2008. I believe this dynamic has been more powerful, more global and much more problematic over the past year.

The Shanghai Composite is up 18.9% y-t-d, the CSI 300 32.0% and the ChiNext index 36.8%, despite economic deterioration and heightened risk. Chinese apartment prices continue to inflate a double-digit rates, as ongoing rapid Credit growth increasingly feeds asset inflation as the real economy struggles. Germany’s DAX equities index enjoys a 2019 gain of 25.3%, France’s CAC40 24.5% and Italy’s MIB 28.4%, in the face of economic stagnation. ECB stimulus measures have fueled a historic bond market Bubble and formidable equities Bubble, while the real economy barely treads water. Stocks in Russia are up 25.5%, Brazil 22.5%, Taiwan 19.0% and Turkey 13.0%, as EM keys off booming global liquidity excess while disregarding mounting risks. Here at home, the S&P500 has gained 23.4%, the Nasdaq Composite 27.7% and the Semiconductors 50.4%, as the Fed’s “insurance” rate cuts stoke speculative excess.

By the time the collapsing mortgage finance Bubble finally (after several close calls) triggered a run on Lehman money market liabilities (inciting major deleveraging), the system was acutely fragile. “Blow-off” speculative excess had stoked inflation across the asset markets, price distortions increasingly vulnerable to any interruption in the flow of market liquidity. Yet it went much beyond interruption, as the abrupt reversal of speculative leverage caused a collapse in market liquidity. I believe 2007’s excesses – spurred by Fed stimulus measures that fueled speculative “blow-offs” and gaping divergences between market Bubbles and the vulnerable real economy – sowed the seeds for an unavoidable crisis. Rate cuts only exacerbated late-cycle excess and worsened financial and economic dislocations.

I have that same uncomfortable feeling I had in 2007 – just a lot worse. The global financial system is self-destructing. Reckless monetary policies have inflamed late-cycle excess. I believe the scope of speculative leverage is much greater these days – on a global basis. The Fed in 2007 (and into ’08) extended a dangerous mortgage finance Bubble. Central bankers these days are prolonging catastrophic global financial and economic Bubbles. The global economy is much more fragile today, with a faltering Chinese Bubble posing an Extraordinary risk. Highly synchronized global financial Bubbles are a risk much beyond 2008. Moreover, central bankers have used precious resources to sustain Bubbles, ensuring much greater fragilities will be countered by limited policy capabilities.

We will now await the catalyst for an inevitable bout of de-risking/deleveraging. There could be a few Lehmans lurking out there – in Asia if I was placing odds. China remains an accident in the making, with another ominous week in Chinese Credit (see “China Watch”). And near the top of my list of possible catalysts would be a surge in global yields. Sinking bond prices are problematic for highly leveraged holdings. Indeed, it is no coincidence that “repo” market issues erupted the week following a sharp reversal in market yields.

It was a notably rough week for global bond markets. Ten-year Treasury yields surged 23 bps to 1.91% (high since July 31). German bund yields rose 12 bps to negative 0.26% (high since July 12). Japanese yields jumped 13 bps to negative 0.05% (high since May 22). Italian yields surged 20 bps to 1.19%, and Greek yields rose 13 bps to 1.30%. Brazilian (real) 10-year yields surged 30 bps. Eastern European bonds, in particular, were under heavy selling pressure.

It’s worth noting bond prices are down sharply since last week’s Fed rate cut. Meanwhile, stock prices have continued to melt up. One could similarly argue that the expanding Fed balance sheet has been benefiting equities – bonds not so much. In general, monetary stimulus tends to inflate the asset class with the strongest inflationary bias. Bond prices peaked two months ago. And bonds have good reason to fret aggressive global monetary stimulus. Booming stock markets and resulting loose financial conditions underpin growth and inflationary pressures.

November 9 – Bloomberg: “China’s consumer inflation rose to a seven-year high last month on the back of rising pork prices, complicating policy makers’ decision on whether to further ease funding for the country’s weakening industrial sector. The consumer price index rose 3.8% in October from a year earlier, up from 3% in the previous month.”

A negative print (down 0.3%) for Q3 Nonfarm Productivity and Unit Labor Costs up 3.6% are supportive of inflationary pressures here in the U.S. But it’s massive supply as far as the eye can see that must have the Treasury market on edge. The uncomfortable reality of a highly levered marketplace, with downward pressure on prices and fiscal deficits approaching 5% of GDP. Yet negative fundamentals can be ignored so long as China’s Bubbles are about to implode. But with a trade deal somewhat postponing China’s day of reckoning – while holding additional global monetary stimulus at bay – the bond market risk versus reward calculus loses much of its appeal.

It’s possible that a de-risking/deleveraging cycle commenced in early-September. The Fed’s eight-week $270 billion balance sheet expansion accommodated some deleveraging. But at some point the Fed will apparently settle into $60 billion monthly T-bill purchases – that won’t be much help in a de-risking environment. Stocks are fired up at the prospect of a year-end melt-up. The surprise would be a global bond market beat down – the downside of Extraordinary Monetary Disorder.

Money is free for those who are creditworthy because the investors who are giving it to them are willing to get back less than they give. More specifically investors lending to those who are creditworthy will accept very low or negative interest rates and won’t require having their principal paid back for the foreseeable future. They are doing this because they have an enormous amount of money to invest that has been, and continues to be, pushed on them by central banks that are buying financial assets in their futile attempts to push economic activity and inflation up. The reason that this money that is being pushed on investors isn’t pushing growth and inflation much higher is that the investors who are getting it want to invest it rather than spend it. This dynamic is creating a “pushing on a string” dynamic that has happened many times before in history (though not in our lifetimes) and was thoroughly explained in my book Principles for Navigating Big Debt Crises. As a result of this dynamic, the prices of financial assets have gone way up and the future expected returns have gone way down while economic growth and inflation remain sluggish. Those big price rises and the resulting low expected returns are not just true for bonds; they are equally true for equities, private equity, and venture capital, though these assets’ low expected returns are not as apparent as they are for bond investments because these equity-like investments don’t have stated returns the way bonds do. As a result, their expected returns are left to investors’ imaginations. Because investors have so much money to invest and because of past success stories of stocks of revolutionary technology companies doing so well, more companies than at any time since the dot-com bubble don’t have to make profits or even have clear paths to making profits to sell their stock because they can instead sell their dreams to those investors who are flush with money and borrowing power. There is now so much money wanting to buy these dreams that in some cases venture capital investors are pushing money onto startups that don’t want more money because they already have more than enough; but the investors are threatening to harm these companies by providing enormous support to their startup competitors if they don’t take the money. This pushing of money onto investors is understandable because these investment managers, especially venture capital and private equity investment managers, now have large piles of committed and uninvested cash that they need to invest in order to meet their promises to their clients and collect their fees.

At the same time, large government deficits exist and will almost certainly increase substantially, which will require huge amounts of more debt to be sold by governments—amounts that cannot naturally be absorbed without driving up interest rates at a time when an interest rate rise would be devastating for markets and economies because the world is so leveraged long. Where will the money come from to buy these bonds and fund these deficits? It will almost certainly come from central banks, which will buy the debt that is produced with freshly printed money. This whole dynamic in which sound finance is being thrown out the window will continue and probably accelerate, especially in the reserve currency countries and their currencies—i.e., in the US, Europe, and Japan, and in the dollar, euro, and yen.

At the same time, pension and healthcare liability payments will increasingly be coming due while many of those who are obligated to pay them don’t have enough money to meet their obligations. Right now many pension funds that have investments that are intended to meet their pension obligations use assumed returns that are agreed to with their regulators. They are typically much higher (around 7%) than the market returns that are built into the pricing and that are likely to be produced. As a result, many of those who have the obligations to deliver the money to pay these pensions are unlikely to have enough money to meet their obligations. Those who are recipients of these benefits and expecting these commitments to be adhered to are typically teachers and other government employees who are also being squeezed by budget cuts. They are unlikely to quietly accept having their benefits cut. While pension obligations at least have some funding, most healthcare obligations are funded on a pay-as-you-go basis, and because of the shifting demographics in which fewer earners are having to support a larger population of baby boomers needing healthcare, there isn’t enough money to fund these obligations either. Since there isn’t enough money to fund these pension and healthcare obligations, there will likely be an ugly battle to determine how much of the gap will be bridged by 1) cutting benefits, 2) raising taxes, and 3) printing money (which would have to be done at the federal level and pass to those at the state level who need it). This will exacerbate the wealth gap battle. While none of these three paths are good, printing money is the easiest path because it is the most hidden way of creating a wealth transfer and it tends to make asset prices rise. After all, debt and other financial obligations that are denominated in the amount of money owed only require the debtors to deliver money; because there are no limitations made on the amounts of money that can be printed or the value of that money, it is the easiest path. The big risk of this path is that it threatens the viability of the three major world reserve currencies as viable storeholds of wealth. At the same time, if policy makers can’t monetize these obligations, then the rich/poor battle over how much expenses should be cut and how much taxes should be raised will be much worse. As a result rich capitalists will increasingly move to places in which the wealth gaps and conflicts are less severe and government officials in those losing these big tax payers will increasingly try to find ways to trap them.

At the same time as money is essentially free for those who have money and creditworthiness, it is essentially unavailable to those who don’t have money and creditworthiness, which contributes to the rising wealth, opportunity, and political gaps. Also contributing to these gaps are the technological advances that investors and the entrepreneurs that I previously mentioned are excited by in the ways I described, and that also replace workers with machines. Because the “trickle-down” process of having money at the top trickle down to workers and others by improving their earnings and creditworthiness is not working, the system of making capitalism work well for most people is broken.

This set of circumstances is unsustainable and certainly can no longer be pushed as it has been pushed since 2008. That is why I believe that the world is approaching a big paradigm shift.

Harris Kupperman when asked about his thoughts on ESG in an interview with Real vision

“I think that ESG as being excessive stock price growth. When you look at sectors, this whole parts of the market that just can’t get financing right now, two weeks ago, Peabody tried– their large cooking coal miner, they tried to roll over some debt that was due for a few years out. They’re trying to lower interest rates, and they took it to market and Peabody’s a very profitable company. It has minimal net debt, it should be a very easy debt to roll over and reduce the interest rate on. It turned out that no one wanted to own cold debt because everyone’s mandate suddenly is ESG. It’s a marketing pitch really, and if one mutual fund doesn’t, one bond funds doesn’t. They all have to.

When you look around the world, everyone’s adopted ESG because if you don’t, you can’t raise money, which means that a company like Peabody can’t roll their debt. If Peabody can’t roll their debt, what does that say for Peabody when the debt comes due? They’re going to have to pay it off. They’re not going to be able to roll at any price. What does that say for building a new coal mine? What does that say for expanding your coal mine? I think there’s going to be no new coal production really, and yes, everyone’s mad at thermocol, thermocol, it produces carbon dioxide and everything else. Without cooking coal, you don’t have solar panels, you don’t have wind farms, you need cooking coal. It’s the key ingredient still.

It’s illogical to be against cooking coal because it has the word coal in it. If you go to something like uranium, uranium is the base load for America’s utility. It’s the base load for most countries’ utilities right now. You need baseload power. We just don’t have the technology yet to use batteries to store the solar in the wind. We will, but it’s going to take a few years. Right now with ESG, who’s going to fund a new uranium mine? It’s on the blacklist. It’s up there with coal.

You have a situation where globally, the demand for uranium is about 200 million pounds a year and supply is like 130 and there’s a bit of secondary supply. Maybe you’re looking at like 160, you’re looking at a decent size deficit. As they go through the above ground stocks, which is happening rapidly, the price of uranium is going to go from 25 where it is today to some price above the cost of producing it, which is probably in the 40 to 50 range. Even then, how are you going to add 30, 40 million pounds of uranium plus future growth when no one wants to fund this thing because of ESG?

There’s no bond fund who’s going to fund it. Who’s going to fund it on the equity side? It’s going to be some hedge fund that’s going to want some obscene return on capital, and even most of my hedge fund friends, because their mandate is to raise capital and grow, well, who do you raise capital from? Pensions endowments, other guys with ESG mandates. It’s a circular thing. You have whole sectors of the economy that are cut off, which means that investing in them likely has excess returns and excess stock price growth. That’s ESG to me.”

“Ideas become part of who we are. People get invested in their ideas, especially if they get invested publicly and identify with their ideas. So, there are many forces against changing your mind. Flip-flopping is a bad word to people. It shouldn’t be. Within sciences, people who give up on an idea and change their mind get good points. It’s a rare quality of a good scientist, but it’s an esteemed one.”-Daniel Kahneman

The below quote is by William White, one of

the few global policymakers to publicly warn of the GFC ahead of time. Given

that US has “a very bad fiscal situation, a key question investor should be

asking themselves is what does ‘I am out of here’ look like in the US?

The Fed Gives Up on Inflation

This interesting paragraph from Lance Roberts echo’s my

viewpoint –

Last Wednesday the Fed cut rates for the third time this year,

which was widely expected by the market.

What

was not expected was the following statement.

“I think we would need to see a really

significant move up in inflation that’s persistent before

we even consider raising rates to address inflation concerns.” – Jerome Powell 10/30/2019

The

statement did not receive a lot of attention from the press, but this was the

single most important statement from Federal Reserve Chairman Jerome Powell, so

far. In fact, I cannot remember a time in the last 30 years when a Fed

Chairman has so clearly articulated such a strong desire for more inflation.

Why do I say that? Let’s dissect the bolded words in the quote for further clarification.

“really

significant”– Powell is not only

saying that they will allow a significant move up in inflation but going one

better by adding the word significant.

“persistent”– Unlike the prior few Fed Chairman who

claimed to be vigilant towards inflation, Powell is clearly telling us that he

will not react to inflation that is not only well beyond a “really significant”

leap from current levels, but a rate that lasts for a period of time.

“even

consider”– If inflation is not

only a significant increase from current levels and stays at such levels for a

while, they will only consider raising rates to fight inflation.

I

am stunned by the choice of words Powell used to describe the Fed’s view on

inflation. I am even more shocked that the markets or media are not making more

of it.

Now, I was looking for a

final spike in dollar to 110 on DXY (currently at 98) as world is awash in

dollar debt which needs to be rolled over and any dollar spike due to this

shortage is bad for risk assets. But then REPO fiasco happened and FED had to

support the systemic liquidity by announcing various forms of Repo (which they emphasized

should not be called QE) and it led to FED balance sheet expanding by USD

250 Billion in couple of weeks reversing

the last six months of Quantitative tightening.

The question which arises

is, if US deficit is crowding out the market and FED is stepping in to support

the market players with enough liquidity to buy US treasuries then FED is

willing to supply unlimited amount of dollars to support the market and

effectively fund (indirectly) US 1 trillion dollar deficit.

Now Thankfully Economic

101 taught me

“Increase in supply

(of Dollars) with demand remaining constant always leads to lower prices.”

There is one more

UNDERAPPRECIATED reason “Why is the market continuing to get FED cuts,

liquidity support in the form of Repo operations (restart of QE) in the face of

lowest unemployment in last 50 years”?

Never in the history of the country has the economy’s prospects been so closely tethered to that of the stock market.

Now Thankfully Economic

101 taught me

“Increase in supply

(of Dollars) with demand remaining constant always leads to lower prices.”

There is one more

UNDERAPPRECIATED reason “Why is the market continuing to get FED cuts,

liquidity support in the form of Repo operations (restart of QE) in the face of

lowest unemployment in last 50 years”?

Never in the history of the country has the economy’s prospects been so closely tethered to that of the stock market.

Sadly, financial assets

are holding the policy makers hostage. If they allow the self-correcting

mechanism to play out, then US will go into depression possibly worse than

Great Depression.

With this kind of Corporate profitability, you would be scratching your head on the strength of the US equity markets.

But Ladies and Gentlemen

this is the LIQUIDITY driven market and the FED has just back stopped this

market LIQUIDITY.

Remember

“Markets can remain

irrational longer than you can remain solvent”

My experience has taught me to always analyze supply and

demand. Do the math! The supply of negative yielding debt since

early 2016 has expanded by 13 times as much as the available gold supply from

the world’s mines in dollar terms. In fact, it has grown more than the

entire amount of gold that has been mined in the world since the beginning of

history! Let that sink in for a moment. Governments created negative

yielding liabilities, in less than four years, in more than the amount

in dollars of all the gold ever mined in the history of the world. Are

you paying attention now?

Looking at it in another way, assume only 1% of the value of

negative yielding debt was moved into the world’s gold ETFs, that would be $128

billion of new demand for gold, more than an entire year of newly mined gold

supply and more than all the gold currently in those ETF’s. This is a

potential supply/demand mismatch worth pondering.

If both sovereign debt and gold have no yield, which one would

you rather own? I view gold as

a potential superior substitute to those trillions of dollars of negative

yielding debt, because gold may not yield anything, but that is more than a

negative yield and it has no default risk. The same cannot be said with

certainty of any bond in the world especially when every central banker is

willing to tolerate higher inflation.

Stated differently

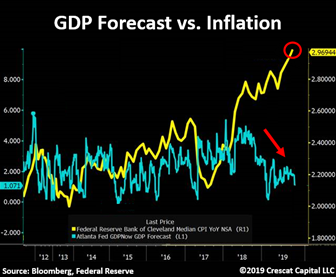

US GDP NOW forecast are now cut to 1% while Median CPI is at 3%

FED just printed $260B in 2 months

3 rate cuts in 3 months

The entire treasury curve now below inflation- CB easing worldwide $13+ Trillion of negative yielding Bonds

Can anyone survey

today’s world and feel confident that they fully understand it? Negative

interest rates, political unrest, a global crisis in government

legitimacy?

I think a lot about what may happen, which means thinking

through potential scenarios such as I outline above. I am certainly

intrigued about the potential demand for gold as a substitute for negative

yielding bonds. It’s hard to say exactly what this would mean for the

price of gold, but my best guess is higher.

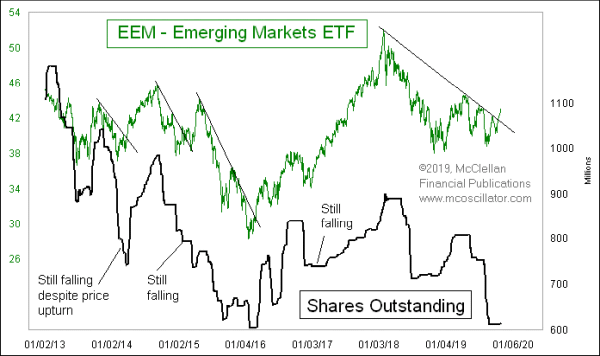

Emerging Markets

EEM has the fun

property that when it disagrees with the SP500, that is usually useful

information. When there is a divergence or other disagreement, EEM

usually ends up being right about where both are headed.

The hint which

EEM gave us recently was in the form of breaking its own declining tops line

ahead of the SP500 breaking its downtrend line. It did this same thing

coming out of the Dec. 2018 bottom, and in that instance, it had also shown a

bullish divergence versus the SP500 by making a higher low…… are EM smelling

Dollar depreciation?

One additional reason to expect the new uptrend to continue, is that investors are still not interested in coming back into EEM. Here is a chart showing that fund’s number of shares outstanding.

Market

outlook

Fed and other central banks have already cracked open

the floodgates of money-printing to provide liquidity to boost markets and/or

cap yields. I think dollar index is headed lower to 92-93 levels (currently 98) which will lift

all depressed risk assets. Emerging markets, Value stocks, Gold and

silver miners and even almost dead Agri commodities.

The most important chart (DXY)….. it is all about DOLLAR

To Summarise

That powerful force of a coming

Fed liquidity injection + another Fed cut to sustain the expansion caused a key

reversal in the macro landscape where:

USD topped out and

is starting to depreciate easing the GLOBAL DOLLAR SHORTAGE

Cyclical

equities/commodities bottomed and have started to break out higher

Interest rates

bottomed and started pricing out future Fed cuts

Yield Curves like

2s10s, that had been dormant, beginning to steepen

With that said, and this is just my own opinion, it is

just a matter of time before the dam breaks, when the gap between asset

inflation and economic growth is no longer tolerated.

The Federal Reserve has injected $278 billion into the securities repurchase market for the first time. Numerous justifications have been provided to explain why this has happened and, more importantly, why it lasted for various days. The first explanation was quite simplistic: an unexpected tax payment. This made no sense. If there is ample liquidity and investors are happy to take financing positions at negative rates all over the world, the abrupt rise in repo rates would simply vanish in a few hours.

Let us start with definitions. The repo market is where borrowers seeking cash offer lenders collateral in the form of safe securities. Repo rates are the interest rate paid to borrow cash in exchange for Treasuries for 24 hours.

Sudden bursts in the repo lending market are not unusual. What is unusual is that it takes days to normalize and even more unusual to see that the Federal Reserve needs to inject hundreds of billions in a few days to offset the unstoppable rise in short-term rates.

Because liquidity is ample, thirst for yield is enormous and financial players are financially more solvent than years ago, right? Wrong.

What the Repo Market Crisis shows us is that liquidity is substantially lower than what the Federal Reserve believes, that fear of contagion and rising risk are evident in the weakest link of the financial repression machine (the overnight market) and, more importantly, that liquidity providers probably have significantly more leverage than many expected.

In summary, the ongoing — and likely to return — burst in the repo market is telling us that risk and debt accumulation are much higher than estimated. Central banks believed they could create a Tsunami of liquidity and manage the waves. However, like those children’s toys where you press one block and another one rises, the repo market is showing us a symptom of debt saturation and massive risk accumulation.

When did hedge funds and other liquidity providers stop accepting Treasuries for short-term operations? It is easy money! You get a safe asset, provide cash to borrowers, and take a few points above and beyond the market rate. Easy money. Are we not living in a world of thirst for yield and massive liquidity willing to lend at almost any rate?

Well, it would be easy money… Unless all the chain in the exchange process is manipulated and rates too low for those operators to accept even more risk.

In essence, what the repo issue is telling us is that the Fed cannot make magic. The central planners believed the Fed could create just the right inflation, manage the curve while remaining behind it, provide enough liquidity but not too much while nudging investors to longer-term securities. Basically, the repo crisis — because it is a crisis — is telling us that liquidity providers are aware that the price of money, the assets used as collateral and the borrowers’ ability to repay are all artificially manipulated. That the safe asset is not as safe into a recession or global slowdown, that the price of money set by the Fed is incoherent with the reality of the risk and inflation in the economy, and that the liquidity providers cannot accept any more expensive “safe” assets even at higher rates because the rates are not close to enough, the asset is not even close to being safe, and the debt and risk accumulated in other positions in their portfolio is too high and rising.

The repo market turmoil could have been justified if it had lasted one day. However, it has taken a disguised quantitative easing purchase program to mildly contain it.

This is a symptom of a larger problem that is starting to manifest in apparently unconnected events, like the failed auctions of negative-yielding eurozone bonds or the bankruptcy of companies that barely needed the equivalent of one day of repo market injection to finance the working capital of another year.

This is a symptom of debt saturation and massive risk accumulation. The evidence of the possibility of a major global slowdown, even a synchronized recession, is showing that what financial institutions and investors have hoarded in recent years, high-risk, low-return assets, is more dangerous than many of us believed.

It is very likely that the Fed injections become a norm, not an anomaly, and the Fed’s balance sheet is already rising. Like we have mentioned in China so many times, these injections are a symptom of a much more dangerous problem in the economy. The destruction of the credit mechanism through constant manipulation of rates and liquidity has created a much larger bubble than any of us can imagine. Like we have seen in China, it is part of the zombification of the economy and the proof that unconventional monetary measures have created much larger imbalances than the central planners expected.

The repo crisis tells us one thing. The collateral damages of excess liquidity include the destruction of the credit transmission mechanism, disguising the real assessment of risk and, more importantly, leads to a synchronized excess in debt that will not be solved by lower rates and more liquidity injections.

Many want to tell us that this episode is temporary. It has happened in the most advanced, diversified and competitive financial market. Now imagine if it happens in the Eurozone, for example. This is, like the inverted yield curve and the massive rise in negative-yielding bonds, the tip of a truly scary iceberg.

“Stepping in as lender of last resort to the banking system is what the Fed was intended for. Stepping in as the lender of last resort to the Federal Government is now what the Fed is being used for.

To be sure, this is outright monetization of the debt, without any other intended purpose. This may be why the dollar has taken a dive this month. Keep a close eye on it and the long-end of the bond market. If the dollar and long bonds both begin to fall together it may mean the markets have figured this out.”