PRINCIPLE NUMBER ONE: THE SHORT-TERM, RISK FREE INTEREST RATE ON U.S. TREASURY BILLS SHOULD NOT BE THE HIGHEST INTEREST RATE IN THE DOLLARIZED WORLD.

An uncontroversial principle of investing is that investors seeking safety should accept lower risks for a lower return, and investors seeking to earn better returns should be willing to take more risks. The yields available on the shortest-term U.S. government debt are those most referred to as the return on the risk-free asset. Greater risks that investors could take to earn higher returns come in many forms, as I explain below.

Just to name a few, examples of such risks that should lead to higher returns include 1) duration, the risk of loaning your money out for a longer period of time, 2) credit, the risk of loaning money to weaker quality debtors, 3) equity, which is after all just another form of credit risk, and 4) illiquidity, the risk of not being able to get your money back immediately. Make no mistake: in investing, you take the risk first. Any potential return you may earn comes only later – after you take the risk.

All the potential higher returns named above come from taking higher risks. Isn’t it logical to assume that investors would want to get compensated for taking those higher risks? Otherwise, after all, why not just own the risk-free asset and earn its lower, but safer, returns? This is where the problem lies today, in our inverted yield curve.

I have always enjoyed Rohit Srivastava’s (Indiacharts) work on markets and he was gracious enough to share some snippets of his Long short report with all of you

He writes

On US Dollar

“The Moment we start discussing the Fed, interest rates, and the reflation trade, we need to look at what the dollar is doing. If anything has me confused in the last few months it has been the dollar. After the dollar hit the 97.50 mark For the first time I started out believing that it would reverse into a 3rd wave decline. However as the currency did not fall right away and made higher highs I changed my view on the dollar and thought it would have a negative impact on commodities and precious metals. While the weakness in commodities has played out precious metals went on to do their own thing on the back of negative real interest rates. Thus watching the dollar was useful in some cases and not in others. The rising dollar did have the negative impact on emerging market stocks and currencies as anticipated. But now after several months the dollar index itself has really not gone that far. Every time it reaches the top end of the range shown by the channel on the chart below sentiment based on the daily sentiment index crosses the 90% marks and becomes over bullish. Each time it has been followed by a small reaction and another attempt to move up. This pattern has repeated this week and we are again at 92% bullish. Having almost touched the top end of the line the case for a falling dollar is back on the table. We are two weeks ahead of the FOMC meeting that is expected to cut rates. The expectation of lower rates has therefore been putting downward pressure on the dollar while the global demand for dollars in a risk off environment has been putting upward pressure on it. Eventually if a weakening US economy does not respond to lower rates immediately or rate cuts are slow at first the market will anticipate more cuts ahead and it could lead to the resumption of the dollar bear market. “

Commodities,Reflation and Stagflation

What I can say however is that commodity prices that were earlier in decline have started to become oversold some of them are already bouncing back and others might follow. This might lead to a near-term reflation trade. At this point we do not know if the Fed will go into overdrive on rates. If it does then the reflation trade could actually have bullish undercurrents for better stocks and cyclicals. Equities respond differently to stagflation and reflation. A reflation trade can be bullish stocks whereas a stagflation trade causes interest rates to go up and pushes down stock prices. In a hyperinflation almost everything goes up and is a completely different scenario. At this stage we should be ready to deal with the first two.

On INR

What concerns us most though is the USDINR That recently broke out above 69 and started a larger 5th wave long-term. We are now in the third wave of that pattern. From July to September we have witnessed wave 1 of 3 and may now pull back in wave 2 of 3. The depth of such a retracement is not clear however once complete the larger up trend should resume. Keeping an eye on short-term momentum indicators might help in finding the turning points. This might also help us pinpoint the next turn in equities. Wave 3 of 5 goes to 82 and wave 5 itself goes to 90 based on fractal analysis.

On GOLD

The chart has a rising channel that stretches all the way up to $ 4000. These are a multi-year trends. On the gold Mcx chart below prices have reached the top end of smaller channel in wave 3 of 5 near 40,000 INR. The larger channel from 1980 stretches all the way to 63,000 INR. In this case I have data only from 1977 and the wave counts are marked accordingly. 5=1 is closer to 135000 INR long term.

“Debt owed by governments, businesses and households around the globe is up nearly 50% since before the financial crisis to $246.6 trillion at the beginning of March” .The only way out is default through Devaluation

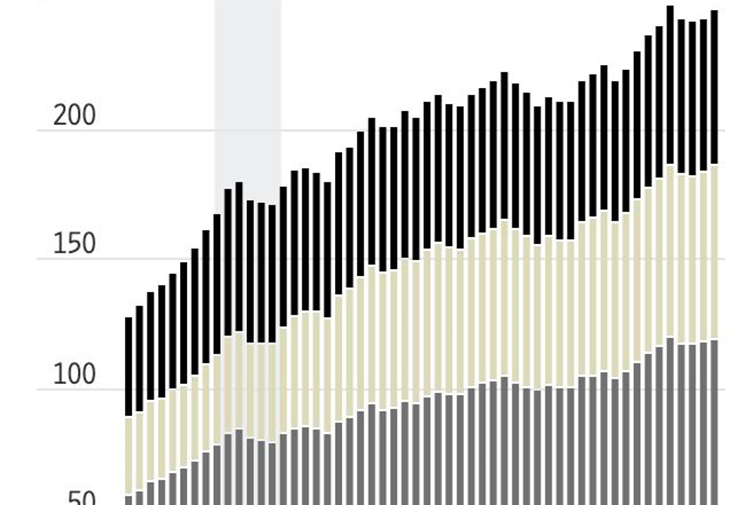

Capex investments, a key driver of future growth expectations have taken a back seat to buybacks and dividends.

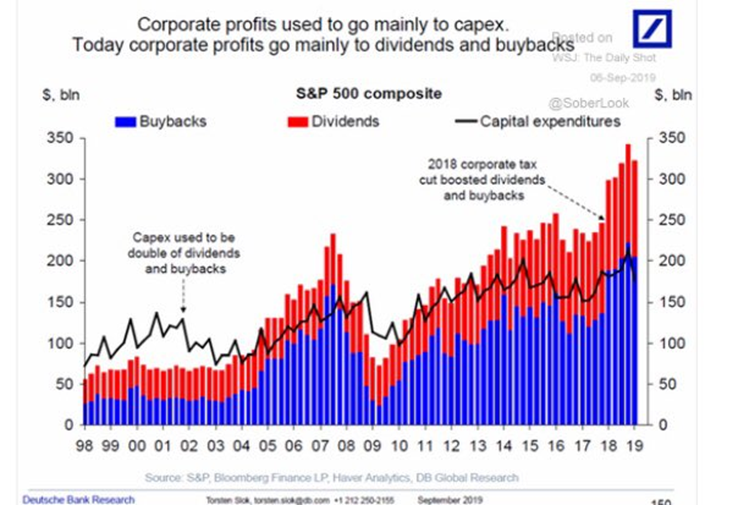

Canadian real GDP per capita growth is ZERO percent over the past year.

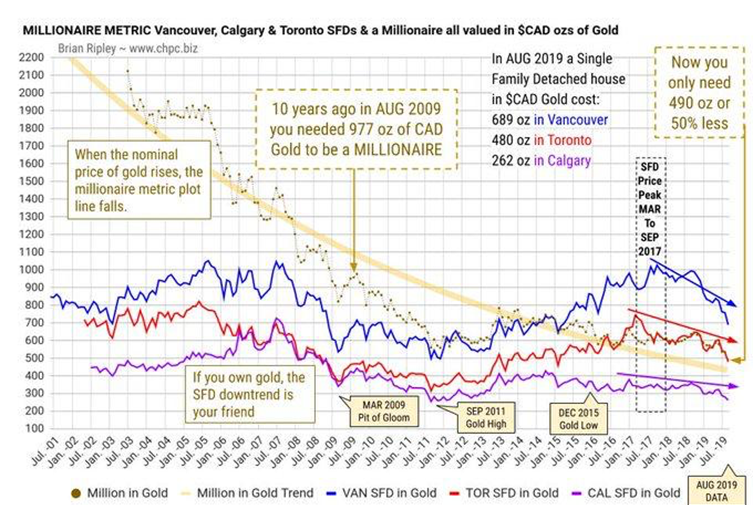

MILLIONAIRE METRIC Vancouver, Calgary & Toronto Single Family Detached and a Millionaire all priced in $CAD Ounces of Gold 10 years ago one needed 977 oz of CAD gold to be a millionaire. Now only 490 oz or 50% less are required.

“The unfortunate backstory is that US department stores are losing

market share as fast as they are downsizing employees, so it still takes 8

employees for $1 mn in sales per year despite job losses. Meanwhile, e-commerce doubled

its share of “core” retail sales in the last 10 years.”

Robin Brooks Chief economist IIF

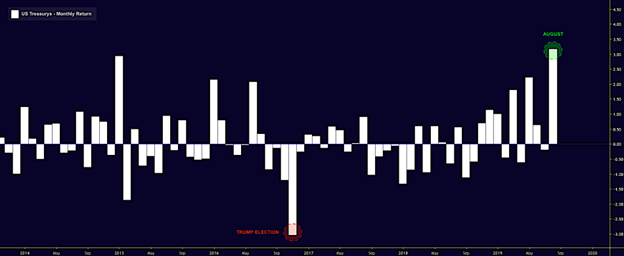

Congrats are for anyone who

came into August convinced that the bond rally had (much) further to run,

despite 10-year US yields having already fallen some 80bps in the first seven

months of 2019. When it was all said and done, US Treasury’s posted their best

monthly gain since the Lehman crisis in August, spurred along by the

intensification of global growth fears, trade escalations, Brexit jitters and

hedging flows into a thin market.

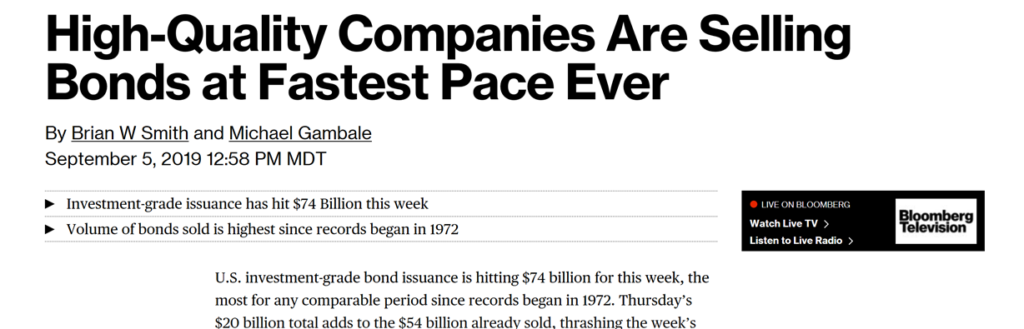

A benchmark index for US debt returned more than 3% for the month. I mean WOW

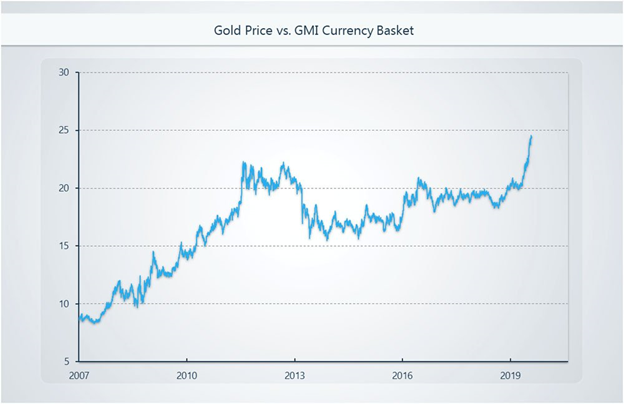

Central Bank Actions in August… Hong Kong: 25 bps cut New Zealand: 50 bps cut India: 35 bps cut Thailand: 25 bps cut Philippines: 25 bps cut Peru: 25 bps cut Mexico: 25 bps cut Paraguay: 25 bps cut Indonesia: 25 bps cut Jamaica: 25 bps cut Iceland: 25 bps cut Global easing……as if interest rate cuts is going to help the indebted economies get out of stagnation The world’s reserve currency (USD) also strengthened against all but one major emerging-market peers since the Federal Reserve cut interest rates in July. The trade-weighted dollar index (which is broader based than just dollar index) touched an all-time high, pushing past a peak seen in 2002.

And we thought Dollar is the only reserve currency. Gold prices denominated in 27 major countries (including INR) touched an all-time high.

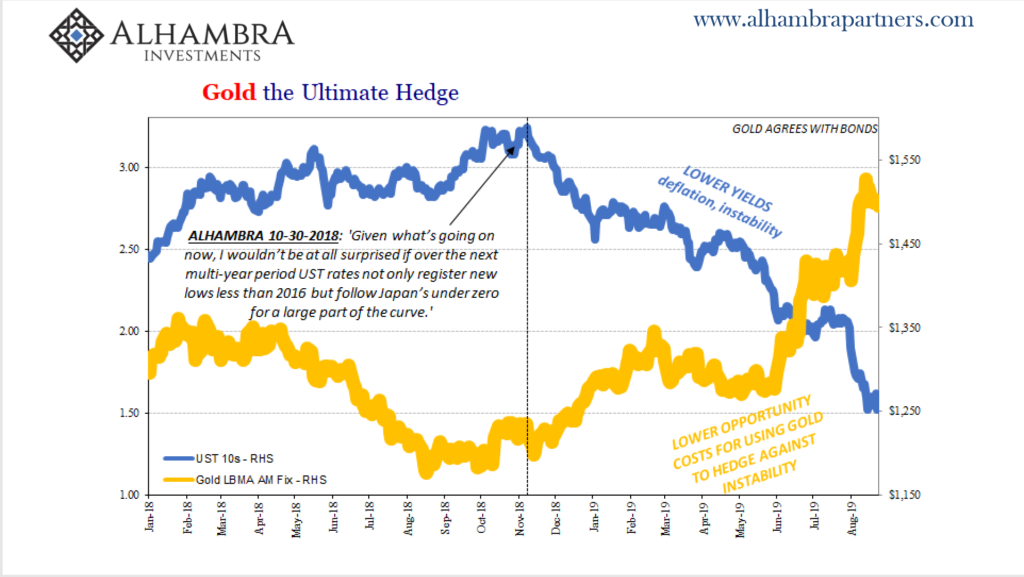

This is surprising because Gold and Dollar generally have negative correlation, but I will again reproduce an excerpt from my favorite analyst Russell Napier below.

So if you read the above you will

realise the importance of Dollar and Gold rising together.

There is an added headwind of China. I don’t trust any data coming out of china, but it is an undeniable fact that Developed world assets (Bonds and Properties) over last 10 years has seen a huge influx of Chinese money looking to diversify. So, the following news from Chinese regulator along with depreciating currency just add one more dimension to the problem Global economy face at the current moment.

Market outlook

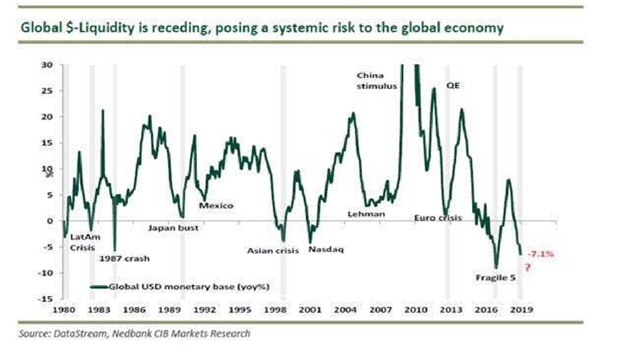

Every asset is a function of Dollar Liquidity (more dollar are good for risk assets and less dollar bad for risk assets) and as Mehul at Nedbank writes “Global $-Liquidity indicator (US $-Liquidity + Proxy for Offshore $-Liquidity) remains in negative territory and will keep on declining (deflationary bust) – the world needs liquidity”

We are at the cusp of a big

change in market characteristics and it has already started with Central

bankers admitting that lowering interest rates is not working anymore. There is

just too much debt in the world and interest rates alone will not pull the global

economy out of stagnation. What is needed is a fiscal spending to kickstart the

global economy. The murmurs of spending are already getting louder in the most fiscally

conservative economy in the world i.e. Germany. I think in more and more

countries burden of growth will shift to Govt from central bankers.

I look at markets from Capital

flow perspective and not from technical or fundamental point of view. I continue

to believe that US is the cleanest dirty shirt in the world and Capital will

flow from rest of the world (periphery) to US (Core). US does not see any

benefits in sharing its GDP with any other country and hence picking fight wherever

it has trade deficit. This only increases the allure of Dollar in the short

term because most countries and corporates outside US have dollar denominated

debt and global trade is still settled mostly in US Dollar.

Short answer is Interest rates and with public part of yield curve inverted, the cost of owning GOLD is actually less than cost of owning a bond and that’s why GOLD is rising along with US Dollar.

The other reason is that negative interest rates are spreading across the globe which again makes GOLD a risk free asset to hold.

Part 2 is the “meat” of the series. Part 1 began with the high level political argument for why Digital Currency will change the world. Part 2 goes deep on monetary concepts and distributed ledger technology.

Ironically, Eric Townsend book was released on the same day Christine Lagard fulfilled one of its predictions by publicly calling for CBDCs. The central prediction of this video is that the U.S. Dollar will be replaced by a new digital global reserve currency. Now on the very day that he released these videos, BOE chief Mark Carney pitched the idea of a digital reserve currency [the central prediction of my book and these videos] at Jackson Hole.

This two-part series explains the Digital Currency Revolution to Central Bankers, Elected Officials & Government policymakers. The focus is NOT on cryptocurrency, but rather what’s coming next, AFTER cryptocurrency. This series explains why all money will be digital within 25 years, and why government has been slow to understand the sea change already in motion.

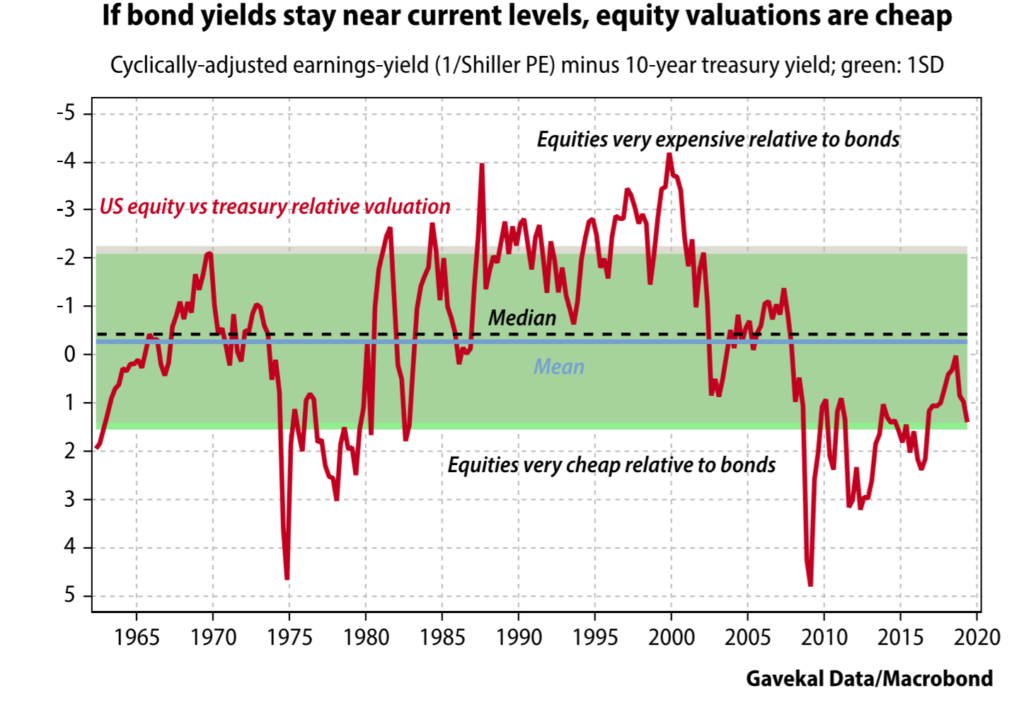

Anatole Kaletsky writes in “when the world goes to hell”

The most convincing reason, “why equity investors should disregard the bond market’s apparently bearish message. Let us suppose that that bond markets really do know more than equity investors or economic forecasters about the economic outlook and that yield curve inversion actually is a reliable indicator of recession. In that case, the Fed and other central banks around the world are certain to keep cutting interest rates, or if their rates are already zero or negative are certain to restart QE. And, even more importantly, both short-term and long-term interest rates are certain to remain near zero for the next ten years or more. In that case, even if the world does experience a recession, the discount rates applied by equity markets to cyclically-adjusted corporate profits, the cap rates assumed by property investors and hurdle rates used by business managements, are bound to keep falling and will eventually end up near zero. In other words, if bond markets are right in predicting a world in which interest rates will stay forever near zero, then US equities on a cyclically adjusted price-earnings ratio of 29—equivalent to an earnings yield of 3.4%—are still quite cheap.

Larry summers, the former treasury secretary and an influential policy maker in US write in Project syndicate op-ed

“If reducing rates will be insufficient or counterproductive, central bankers’ ingenuity in loosening monetary policy in an environment of secular stagnation is exactly what is not needed. What is needed are admissions of impotence, in order to spur efforts by governments to promote demand through fiscal policies and other means.

Instead of more old New Keynesian economics, we hope, but do not expect, that this year’s gathering in Jackson Hole will bring forth a new Old Keynesian economics.“

The German finance minister also acknowledged the failure of monetary policy when he was quoted

“Finance Minister Olaf Scholz suggested Germany could muster 50 billion euros ($55 billion) of extra spending in an economic crisis, putting a number on a possible fiscal stimulus for the first time.”

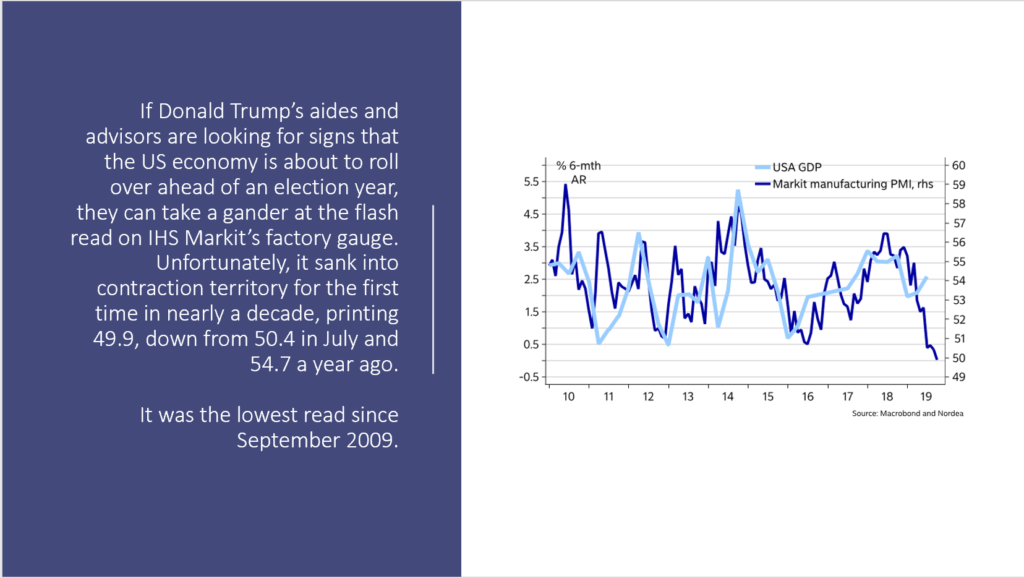

what is missing from a picture is “Recession”

In my view we might not have to wait more than couple of months to see Germany slipping into recession.

The other country which is in news for slowing growth” India” also takes some measure for boosting growth and this is over and above monetary policy easing and will entail higher fiscal deficit.

Winds are changing and whereas monetary policy was instrumental in creating Asset inflation… we might be at an inflection point in world where baton is passed on to fiscal policy for growth revival.