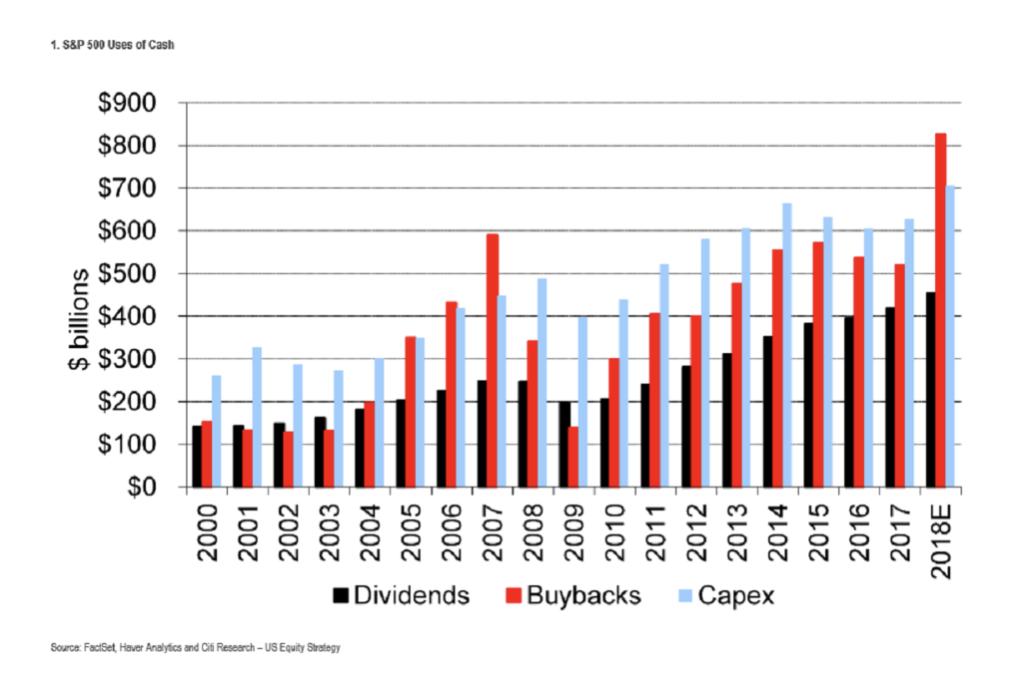

“Companies in the S&P 500 probably repurchased more than $800 billion of shares last year, an amount that surpassed the total they invested in new or upgraded plant and equipment. It’s the first time since 2008 that buybacks topped capital expenditures”Bloomberg

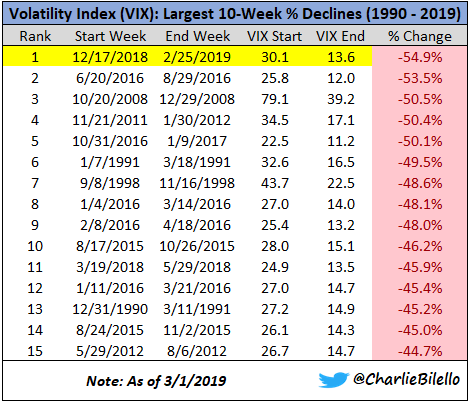

The Volatility Index has fallen 55% over the past 10 weeks, the largest 10-week decline in history. So much for Global Uncertainty

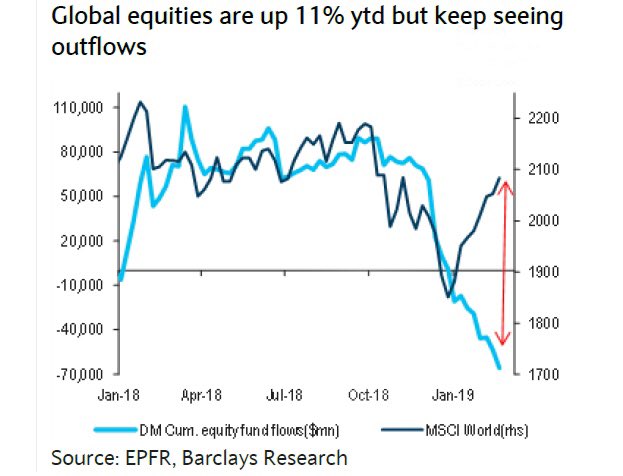

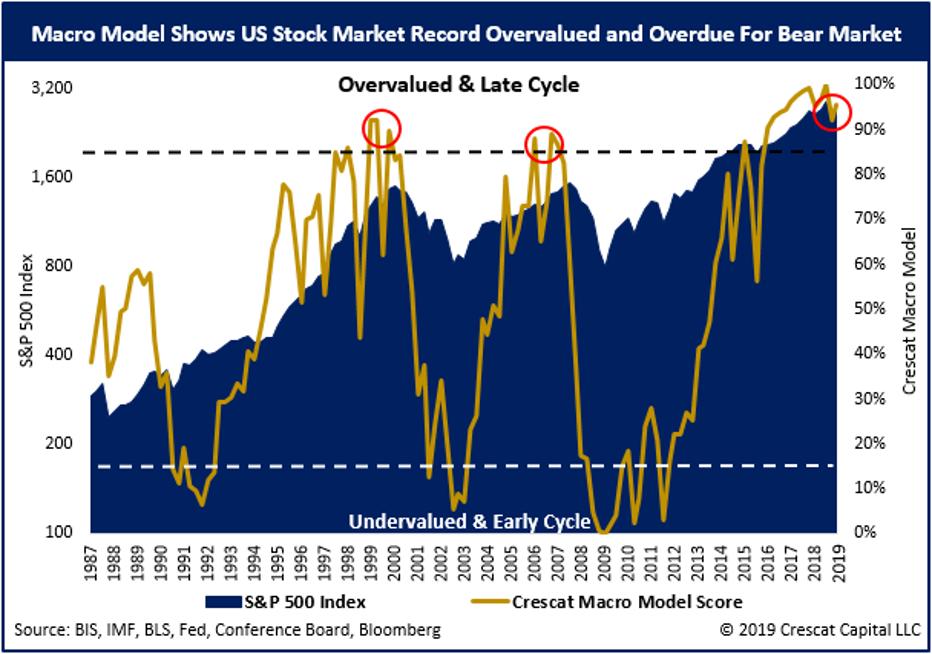

Looks like december finally put an end to the buy-the-dip mentality as equity fund outflows continue. Will they come back chasing? This is also happening in India where Fatigue and disillusionment is setting it.

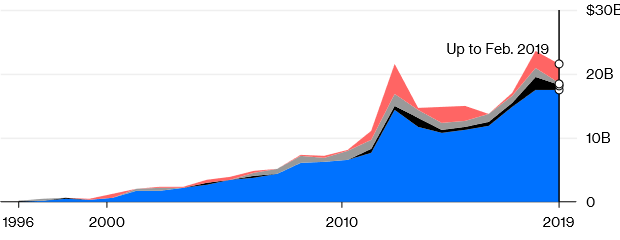

The $22 Billion that is spooking the Indian Bond Market

The quantum of such semi-hidden public financing outside the Indian Govt books is around $22 billion, based on bond and loan-issuance data compiled by Bloomberg for the current fiscal year. With a month to go, this figure could surpass last year’s record of about $24 billion – and even that’s an understatement. The Food Corp. alone has borrowed $28 billion this year, according to an analysis by BloombergQuint, though more than four-fifths of that may have been from non-market sources such as the employees’ provident fund, postal savings and the Life Insurance Corp. of India. All this leads to crowding out where even lowering of interest rates also don’t help because the LIQUIDITY is getting sucked out.

Let’s embark on

a journey that began in the year 2000, one that was greeted with joy, now is

shunned by investors and called a ruin. A process called Fracking was

discovered in mid 2000s with which US created Shale wells and once a country

hugely dependent on crude oil imports plummeted to lowest level of crude imports

since 1967. Federal Reserve’s decision to keep interest rates about zero

percent in 2007 further bolstered the shale business and lured investors with

capital in exchange of promising lucrative returns and stable growth. How could

they have known that the energy with which shale boomed could also be doomed!

In 2014, oil

prices crashed, there was heavy crude sell – off, embedded options on oil

prices which were considered safe resort were no safer and they kept spiralling

down until February 2016! Shale producers revamped the production at the

expense of their longevity, depleted their long term reserves to maximise their

current production and now are under the gun by investors. Even though oil

prices rose considerably from its lowest in 2016, Capex remains 25 – 35% lower

than what it had in 2012 – 2014. According to Dealogic, companies raised about

$22bn from equity and debt financing in 2018, less than half the total in 2016

and almost one third of what they raised in 2012.

Shale industry

has had negative cash flows since its beginning and as Denning pointed out it

has not posted a return on capital above 10 percent any year since 2006 and IEA

estimated cumulative negative free cash flow of over $200bn between 2010 –

2014. Many however, overlooked the fact that McLean highlighted in the book ‘Saudi

America’ which said, “The ability of oil and gas exploration companies to tap

into underground formations is a result not only of technology but just as

important of cheap capital. The fracking boom has been fuelled mostly by

overheated investment capital, not by cash flow.” WSJ phrased this as, “A feature of shale, not

a bug.”

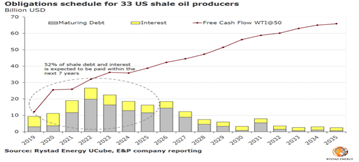

McLean further indicated that the very structure of shale business had fault lines. “For all the hoopla about the surge in US oil and gas production from fracking, most people overlook an important feature of the boom: The average shale well produces most of its oil or gas in first two years. That means oil companies must keep drilling new wells to keep production steady. To maintain production of 1 million barrels per day, shale requires up to 2,500 wells while production in Iraq can do it with fewer than 100.” Now, shale companies are under the radar and investors demand them to either be self – supporting or to return their invested cash. They find themselves straddled with depleting reserves and stalling gains from shale exploration productivity. Rystad Energy Senior Analyst Alisa Lukash said in her statements that, “E&P struggles to please equity investors and reduce leverage ratios simultaneously. Despite a significant deleverage last year, estimated 2019 free cash flow barely covers operator obligations, putting E&Ps on thin ice as future dividend payments in question.” Rystad finds that over half of the total debt pile for 33 companies it analysed is due within next seven years. Ultimately the industry will have to erase $4bn promised dividend payments.

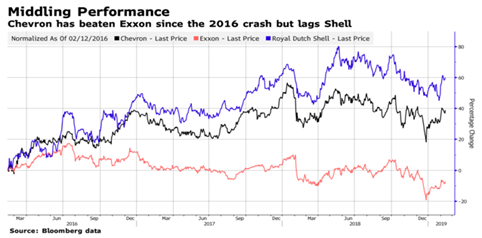

Amid dark clouds, the two big players ExxonMobil and Chevron remain optimistic. ExxonMobil recently said that its oil and gas reserves rose nearly 23 percent last year driven mainly by increases from holdings in US Shale (Permian basin), offshore Guyana and Brazil. US crude oil production has hit a milestone in August when it exceeded 11 million barrels for the first time according to Federal Energy Information Administration. When the survival of small shale companies is on the edge, many investors argue that M&A activity where the big multinationals absorb small shale companies could be profitable for everyone with big companies keeping more shale basins and small with continued operations.

West Texas

Intermediate (WTI) futures hit the highest level in February since November

with a barrel for March delivery at $55.93. The rally is driven by political

uncertainty, OPEC cuts and worries about slowdown in shale production is seeing

a rush out from short positions. Hedge funds abandoned their short selling bets

in January after oil had its best month in three years.

I would end this journey by quoting McLean, “Even today, it is unclear if we look back and see fracking as the beginning of a huge and lasting shift or if we wistfully realizing that what we thought was transformative was merely a moment in time.”

How will a US-China trade deal take market share from other countries who sell to China? This is a zero sum game with US being the only winner at the expense of basically everybody else.

The technology is changing dramatically and rapid innovation will mean that the companies and industries that do not understand this phenomenon and more importantly do not invest a significant part of their budgets in R&D will have hard time competing. There is an exciting ETF ( I have written it before also) known as Knowledge Leaders ETF ( KLDW) which invests in these highly innovative companies. Below is a small three minute video link to their presentation.

Indians investors looking to diversify are allowed to invest in this ETF through LRS route.

Fed conundrum: the S&P 500 (black) is back to its average level in 2018, but market pricing has swung from 2 hikes on average for 2019 to 20% of a cut (blue) and gone from flat in 2020 to 100% chance of a cut (red). This decoupling from financial conditions is unsustainable…

That did not age well

Just your regular reminder that the Fed cuts rate on average 5 months after their last hike

The estimates keep on getting trimmed

Global economic growth forecasts continue to fall. In the past two months, another cut, led by the Eurozone and Japan.Focus economics

The correlation between Chinese stocks and CNY is at its highest level in history! This relationship is poised to break. New PBOC stimulus is unlikely to be positive for both stocks and currency. China can’t have its cake and eat it too. Something has to give.

The incredibly shrinking US stock market is not an isolated phenomena, we’re seeing the same thing across other developed markets (while capitalization continues to increase) via Bernstein

US Housing starts collapse -10.9%, biggest drop in 8 years

“In 30 years, I’ve never seen anything like this”: CEO of warehouse operator Pacific Mountain Logistics.

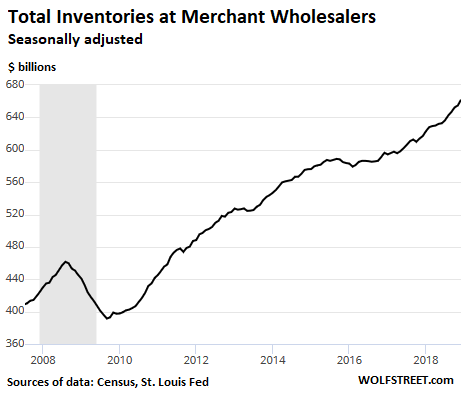

Sales at merchant wholesalers (except manufacturers’ sales branches and offices) fell 1% in December 2018, compared to November, to $497.2 billion on a seasonally adjusted basis, and inched up only 1% compared to December 2017, according to the Census Bureau estimates this morning.

But inventories at these wholesalers rose 1.1% from November and jumped 7.3% from December 2017, to $661.8 billion. Over the two-year period through December, inventories have risen 11%. This includes inventories of durable and non-durable goods (we’ll look at them separately in a moment):

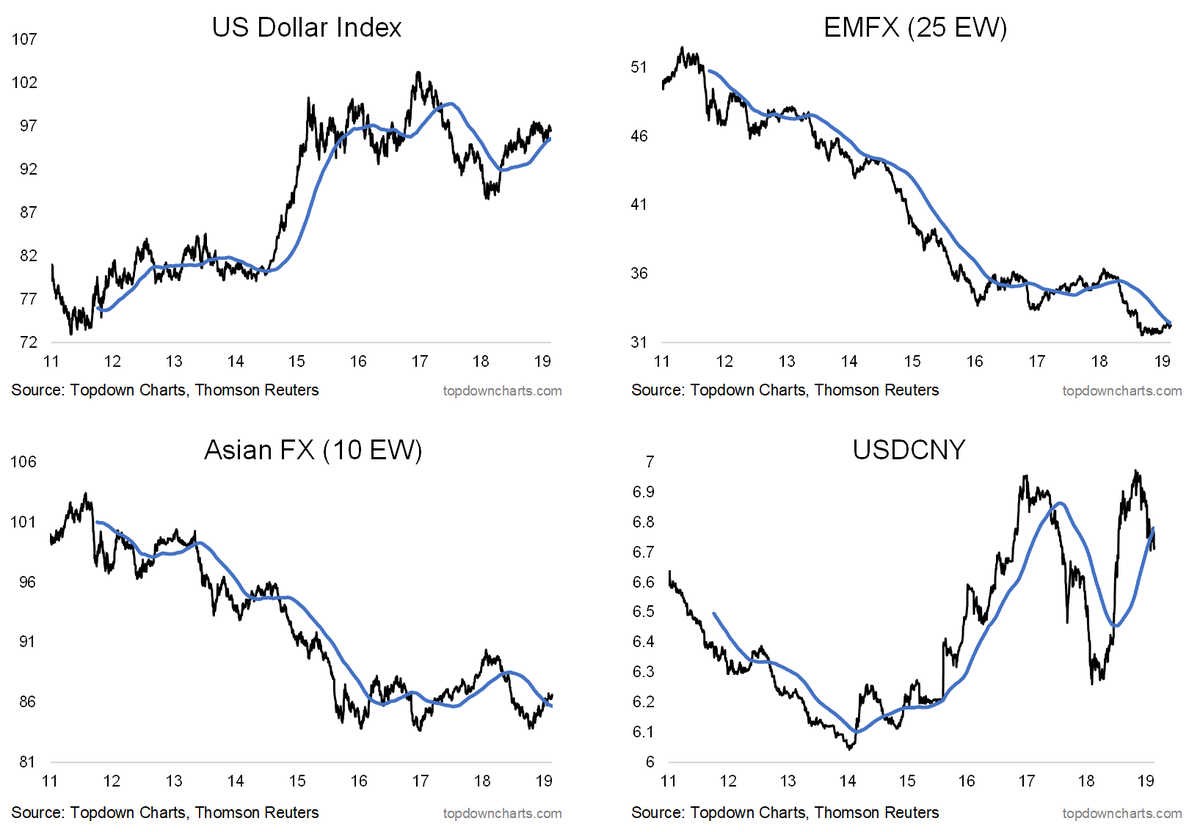

Pay attention to these 4 charts as the US-China trade negotiations continue… if a strong/stable Renminbi is part of the deal it could be a major catalyst to extend the moves that are clearly already underway in EM/Asian FX https://www.linkedin.com/pulse/top-5-charts-week-callum-thomas-14d/ …

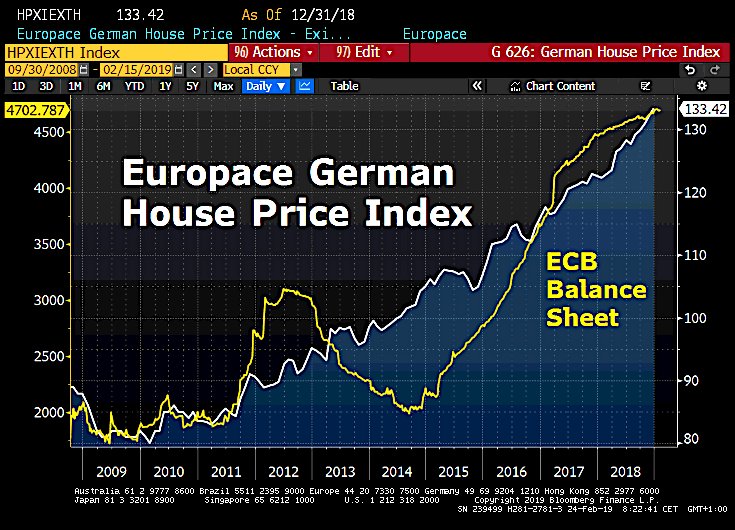

This is where the QE from ECB flowing into….GERMANY, where the housing boom has accelerated as Germans are buying real estate for fear of rising rents. Europace House Price Index has risen in tandem with ECB Balance sheet. Gained 8.8% in 2018, the strongest increase ever in its history.

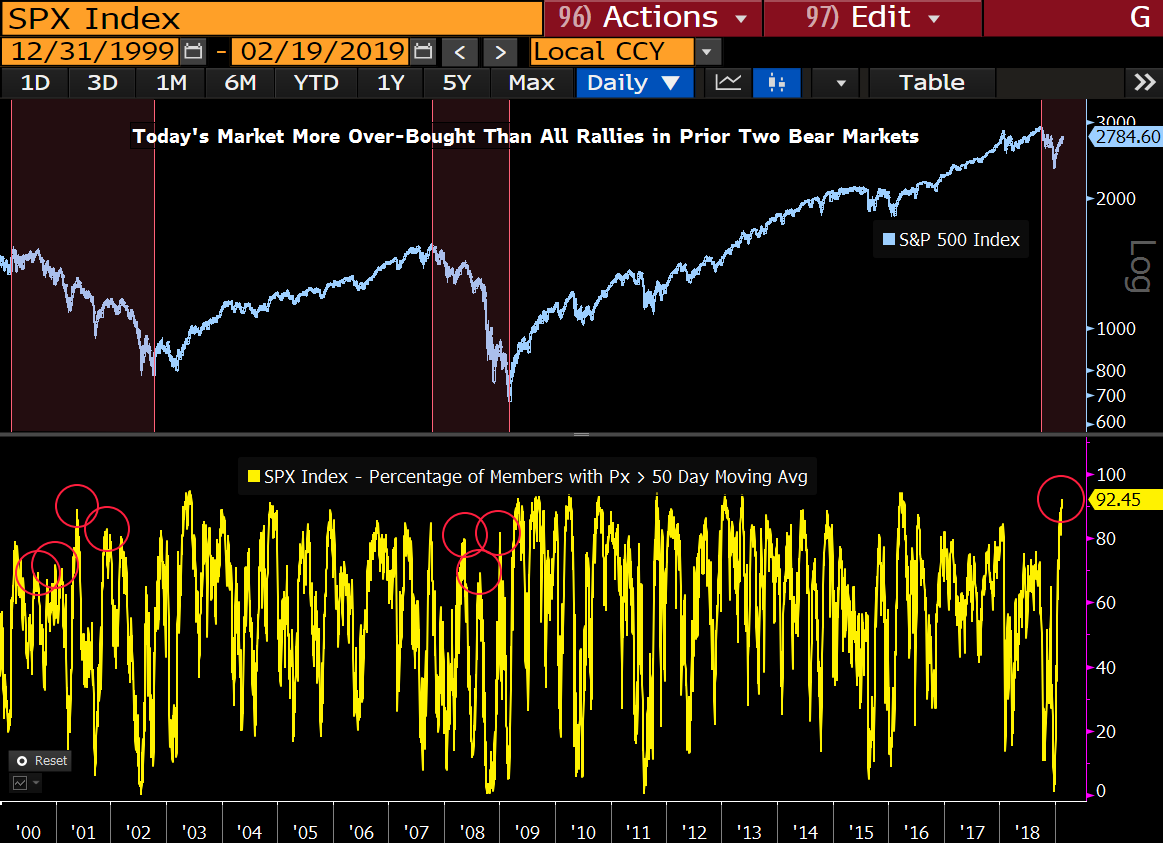

The S&P 500 is more over-bought today than after all rallies in the prior two bear markets based on the percent of stocks above the 50 DMA. Great setup for selling if one believes this is only the beginning of a bear market.

This charts highlights the reason behind the recent China rally: debt!

World’s most famous investor had one of his worst years ever in 2018. Buffett’s Kraft Heinz bet dragged down Berkshire Hathaway in 2018: Conglomerate swung to a $25.4bn loss in Q4 due to an unexpected write-down at Heinz & unrealized investment losses. He also said “Prices are sky-high for businesses possessing decent long-term prospects,”

If stock investors are celebrating the Jerome-the-Hawk to Jay-the-Dove conversion, while ignoring the deteriorating economic backdrop, they are likely falling into a trap much as they did in late 2007 and early 2008.’ https://blog.evergreengavekal.com/bubble-3-0-no-way-out/ …

QE3 and QE2 will likely both be rolled back, but QE1 will never be rolled back. The “new normal” of Feds balance sheet in Nordea FX weekly -> https://ndea.mk/2EaE4w2