Redbook retail data from the early parts of 2019 indicate a horrible start to the year for retail sales as well (on top of the bad December reading).

80% of Chinese people’s wealth is in the form of real estate, totaling over $65 trillion in value — almost twice the size of all G-7 economies combined. A significant slowdown could, therefore, have a substantial impact on citizens’ financial health

Germany is the only Exception to the Global sovereign Debt Explosion

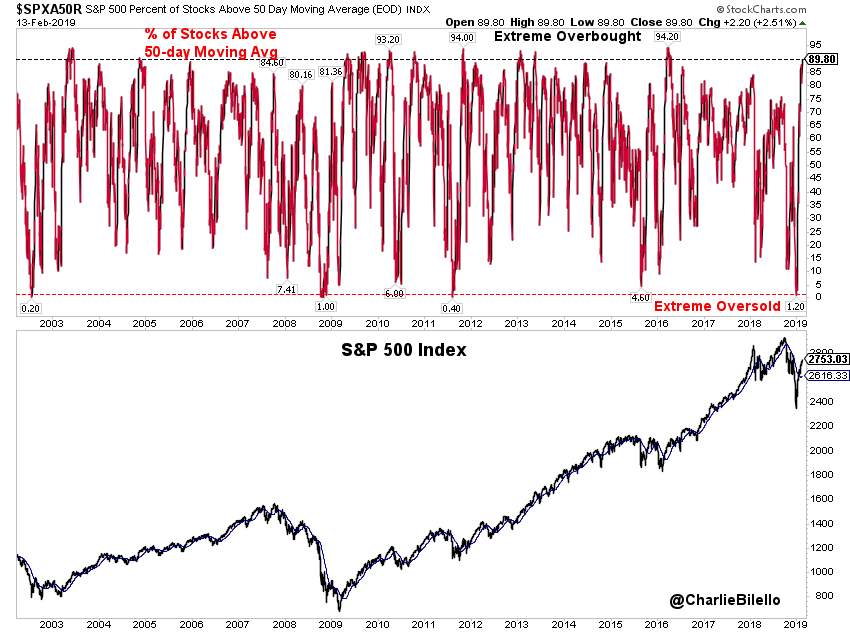

On Dec 24, only 1% of stocks in the S&P 500 closed above their 50-day moving avg, one of the most extreme oversold levels in history. After a 17% vertical rally, that number now stands at 89.8%, highest since April 2016 & in 97th percentile of historical readings. Mission Accompalished

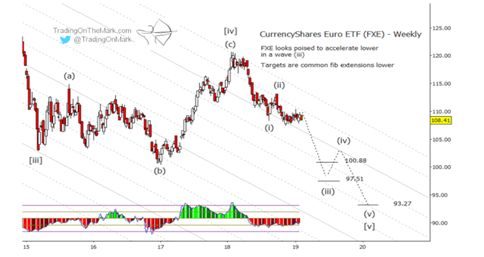

Going back in time when markets fell in 2007-08 Financial Crisis, US Dollar rebounded when the dust settled and Dollar continued to dominate world foreign exchange reserves followed by Euro. Surprisingly, Euro managed to capture only 20 percent of market share till today. Such difference in dominance is credited to higher liquidity of Dollar by Commission.After 2018 rate hikes in US, US Dollar surged 9 percent since April 2018 but it is now back to its 200 daily moving average yet the Euro/USD volatility is nearing to 15 year low. Unfortunately, Euro has become a puppet of risks and vagueness of Europe’s indecision.

While Pound is

expected to remain volatile owing to ambiguity surrounding Brexit in March 2019

and is bearing an intense selling pressure accompanied by weak economic data,

Euro is shrouded by negatively moving clouds which are not settling anytime

soon. The risks causing Euro’s fickle movements are found in nearing Brexit

day, German auto tariffs, US – China trade war and Russian sanctions so it’s

not hard to imagine volatility in European markets.

The bearish outlook of Euro is also revealed in Elliot wave patterns and it is quite revealing. The chart is very bearish Euro and bullish Dollar as can be seen below.

Above shown are

plots of Euro ETF and British Pound ETF indicating clearly the weakness of Euro

in comparison to Pound which recently surged after indecision on Brexit came

into view.

This month, the

Bank of England issued its strongest warning to EU that “its lack of adequate planning for Brexit has created growing risks for

almost 70tn pounds of complex financial contracts. EU firms have about 69tn

pounds of outstanding derivatives contracts that are handled through a process

known as ‘clearing’ in UK while as much as 41tn pounds maturing after Britain

exit EU in March 2019.”

Conclusion

A weak currency is a boon for exporters and also leads to higher imported inflation but eurozone GDP is not only stagnating its exports are also struggling, not to mention falling inflation and inflation expectations . I would have expected eurozone equities to get a tailwind but most European indices are showing weakness compared to US equity indices. I am firmly of the opinion that capital is leaving Europe for US shores and this is not good news for Euro or Eurozone assets. If our view is right, then we expect to see parity on Euro/Dollar before this year is over.

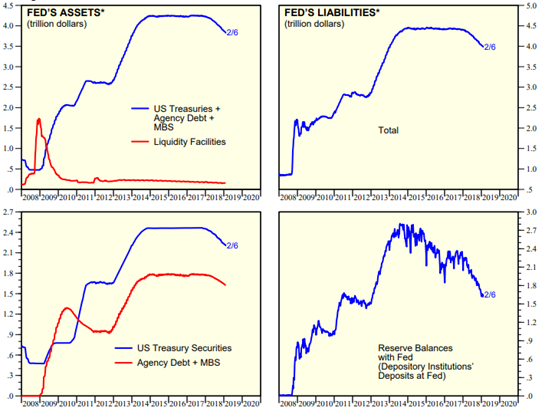

With sizeable increase in individuals who put their faith in central bank and corporates by investing in bond mutual funds to earn regular income or capital appreciation ,have been given a warning recently by Fitch explicitly mentioning that these bond funds are ‘a potential source of financial instability’.

The causes for the instability and probable crash in credit markets are designated by terms “global QE, prolonged low yields, technology and a wave of regulation”. The daunting new reality of dramatic fall in bond markets LIQUIDITY is yet to be learned by markets and investors.

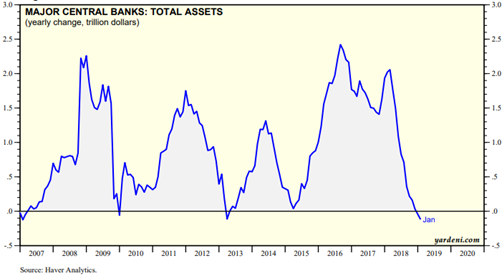

All these fancy terms hide the fact that there have been shocks in the market since Federal Reserve released a statement in 2014 about its expected approach to its Balance Sheet Shrinkage after which followed the global QE or commonly said as ‘normalization of interest rates’.

Goldman Sachs economists wrote at the start of QT that “FOMC will begin to reduce the Balance Sheet at the end of 2017. They assume that the Fed will allow two thirds of maturing debt to run off in 2018 and rest all of it in 2019. If this happens in hawkish manner it may indicate that the total Balance Sheet assets of global central banks will start to fall as a percentage of world GDP for first time since the Financial Crisis of 2009. It would be crucial at this time that the markets and investors learn to get along without massive bond purchases from central banks.“. Goldman it seems turned out to be right on mark as markets are yet to come to terms with shrinking bond market liquidity

With falling interest rates and lower yields to investors from the bond funds, the run on the fund is evitable which will complicate market health thereby leading to instability.As more and more fund managers increase their share of holding in technological companies (FAANG +M) as investors desire returns at least equivalent to market return, the more is the market overvaluing those corporates leading to bigger increase in stock prices but time is not far when the wave to invest in corporate bonds and irrationality among investors having blind faith in system and managers who are passively managing funds yet again will come crashing down.

Fitch pointed out, “Bonds of higher quality liquid issuers in recent times have traded down a percentage point or two, whereas lower quality, less- liquid names dropped three to five points…”

They further explains, “…while previous periods of micro – level stresses in bond fund universe did not threaten financial stability, the rapid growth in open end credit – funds and the significant distortions to credit market caused by QE mean that market conditions look very different now.” And indeed they do. With the crash of Third Avenue’s bond fund in late 2015, markets did react but it did not lead to tumbling down which is now the fear among most.

Conclusion

Knowing when to exit is the most fundamental aspect that people miss and they find themselves in bed with the rocks when they could have plucked flowers and walked away. Climate is changing and you’d be better off by acknowledging that this might be necessary on a macro scale and by taking responsibility by not being a part of contagion that has begun but by taking calculated risks and investing intelligently.

This is now the widest drop in Consumer Confidence Present Situation vs. Expectations since the Tech Bust. Every other cyclical decline in the past 50 years led to a recession @hussmanjp

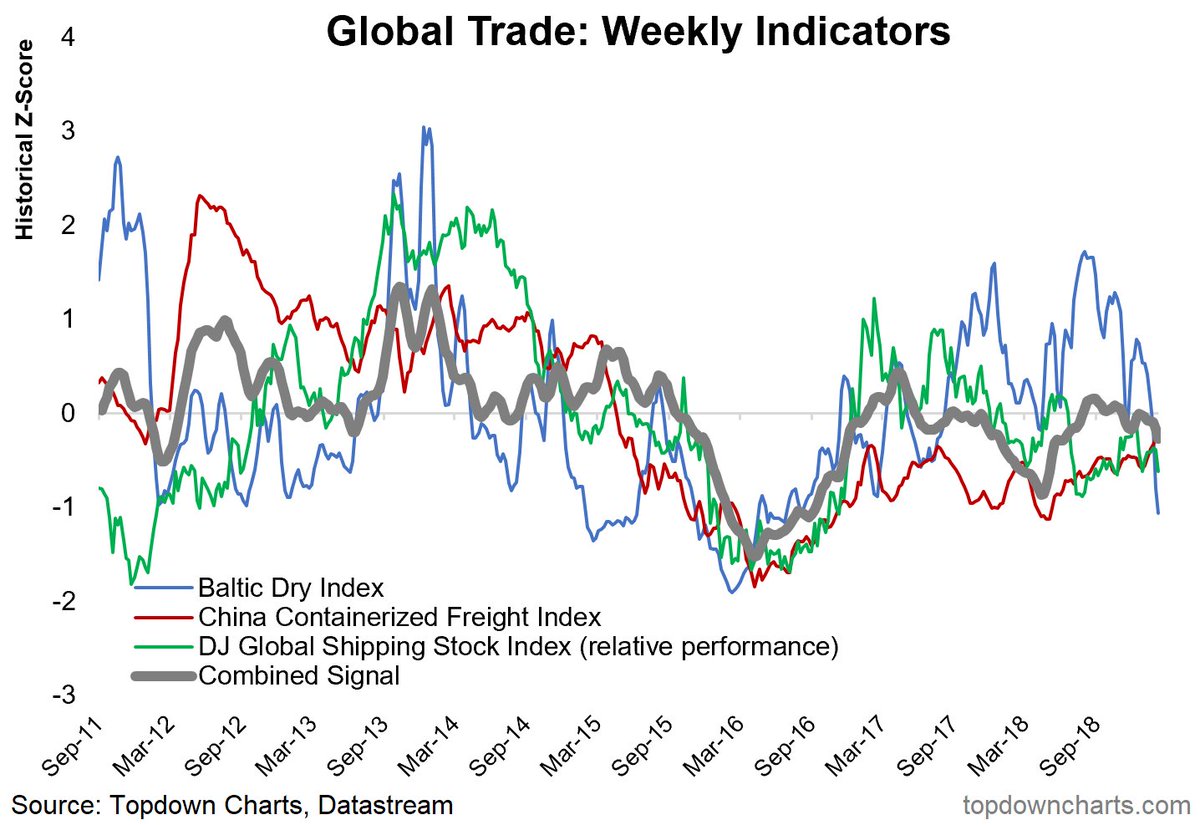

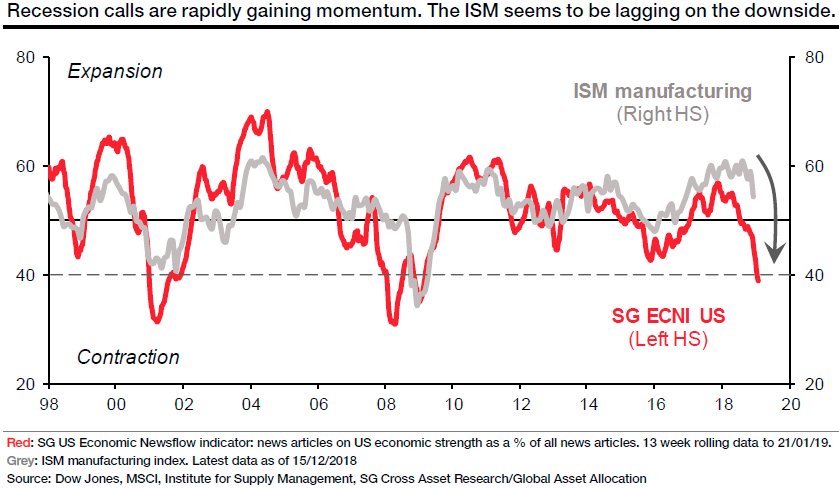

The BALTIC DRY INDEX continues to decline today It’s already very difficult to explain this only in seasonality … Is the world trade simply frozen ?

We are seeing record divergence. Either the Fed gets hawkish again, or the economy rolls over hard. This spread is historic and CANNOT hold. Something has to break one way or the other. Neither is good for stocks.

Something is at a Nine year high except that it is not pretty.

Some 485,000 U.S. workers were involved in 20 major strikes and lockouts last year, the largest number since 1986. what am I missing in the best economy ever?

Australia’s new credit growth is still in free fall and suggest much further downside for house prices ahead..

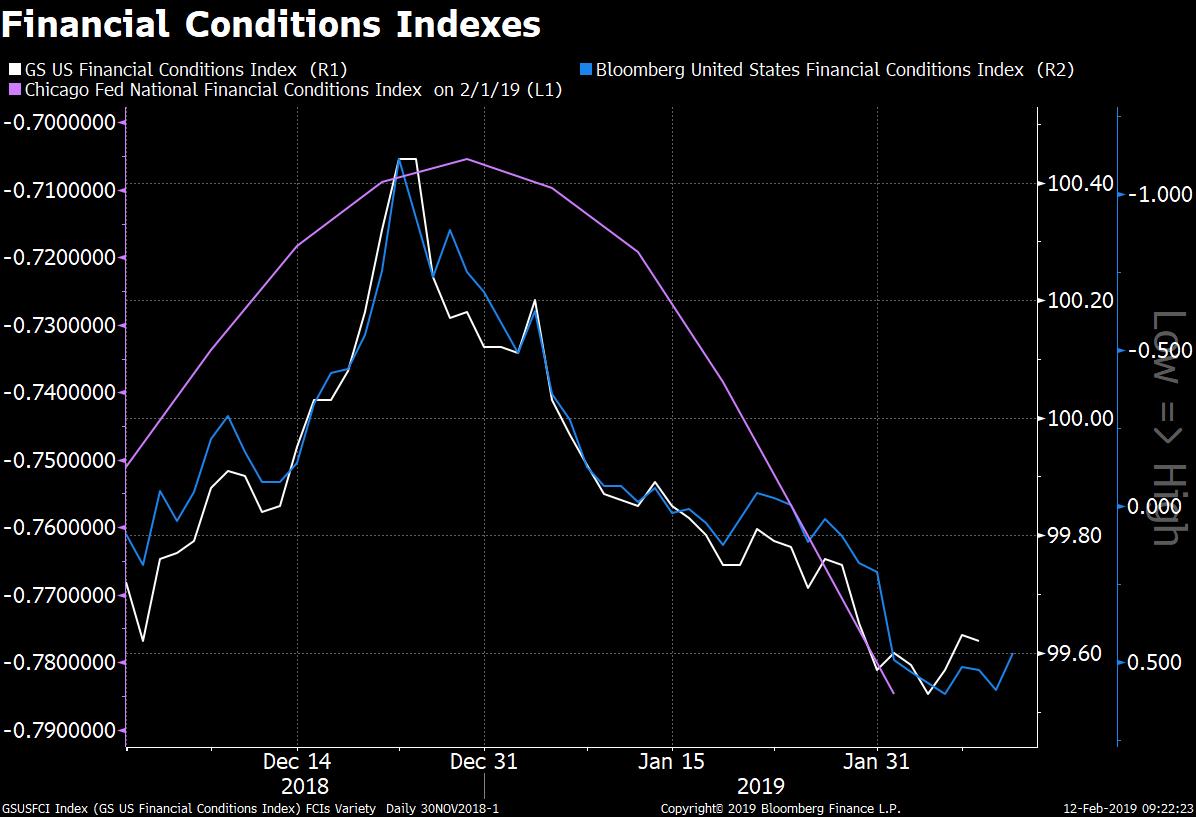

Financial conditions indexes are in easier territory now than they were at the start of December. Liquidity in the system has been improving since US govt shutdown….. why? because in shutdown US govt cannot borrow money from market and has to run down its cash balances for emergency conditions… like shutdown. The loosening of condition has coincided with a bottom in US equity markets as more LIQUIDITY is good for financial markets.

Conclusion: Shutdown is good for LIQUIDITY and LIQUIDITY is good for financial markets

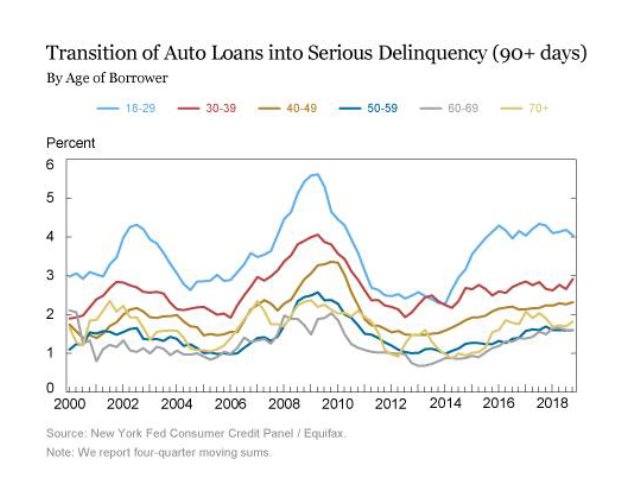

A record 7 million Americans are 90 days+ behind on their auto loan payments, a red flag for the economy, @NewYorkFed reports. It’s a million more people behind than during the financial crisis era. Many are under 30 years old and Powell just mentioned. “NATIONAL LEVEL DATA SAYS ECONOMY IS GOOD”

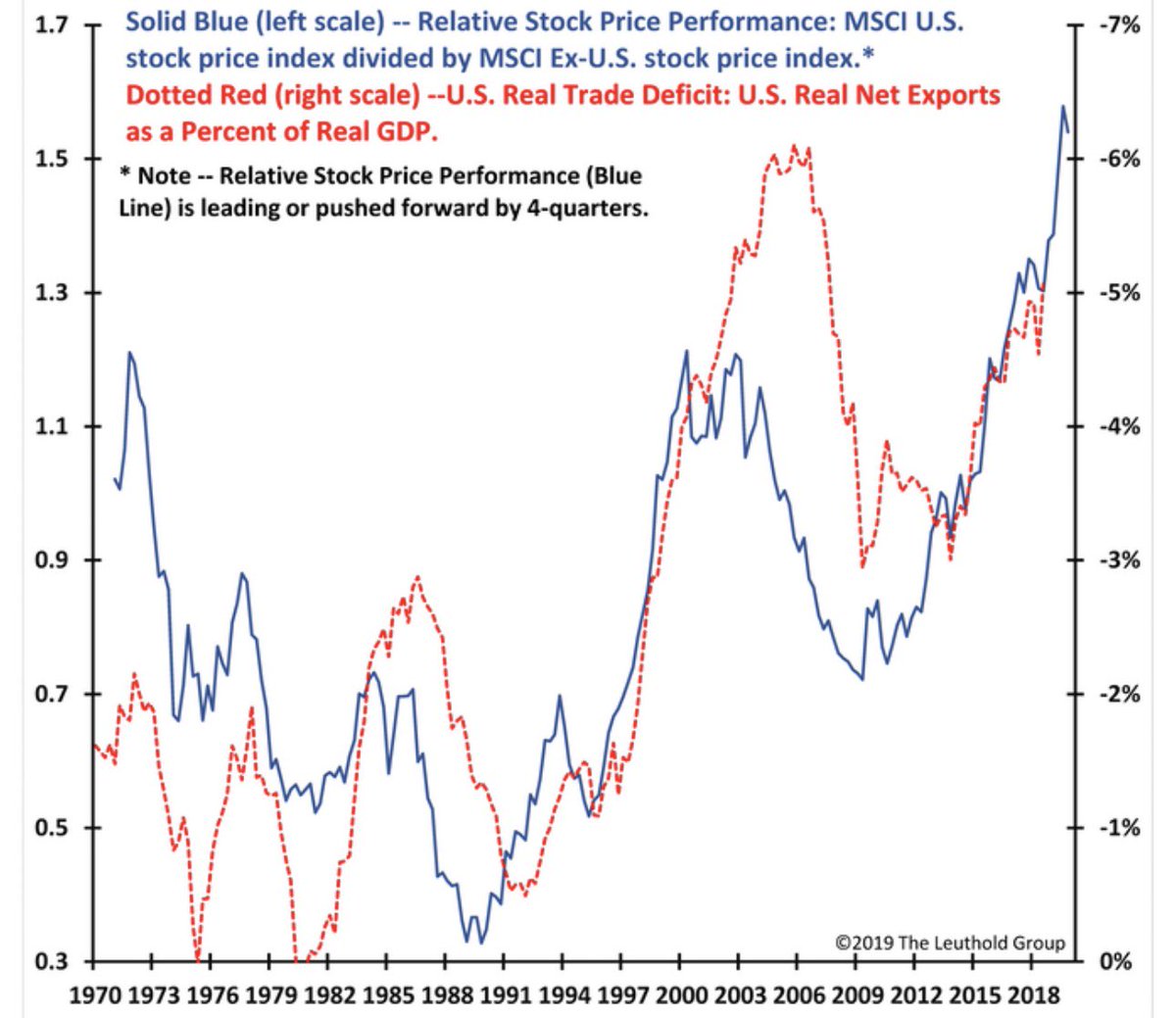

Close historical relationship between U.S. Trade Deficit & relative performance of U.S. stocks vs int’l stocks…believe it or not, since at least 1970, U.S. stocks have done best when trade deficit worsens @LeutholdGroup . You might have noticed that US trade deficit has started shrinking … not again

Domestic/foreign stock exposure & U.S. trade deficit:

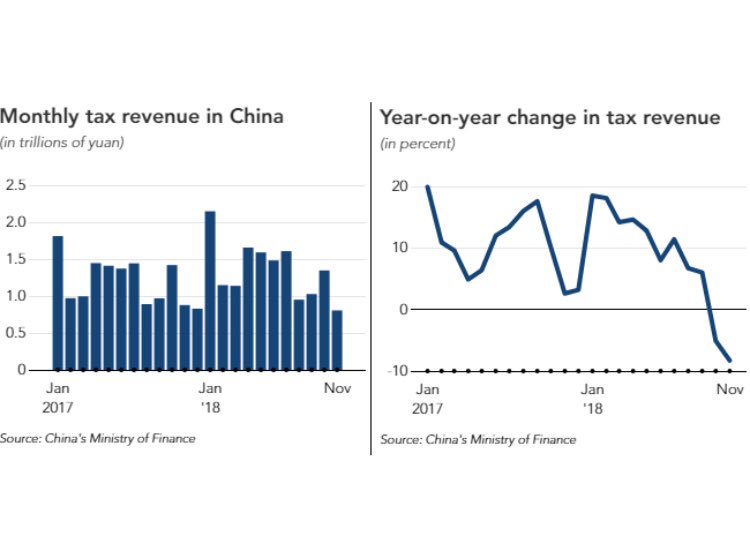

Chinese Tax revenue, post tax cuts. The US tax refunds don’t look too dissimilar. Is it the case of money left in the hands of people or there is no income left to pay for taxes.

China censors media reports about job losses, and official unemployment figures are not reliable – but you can gauge increased pressure in the labour market from the number of internet searches for ‘lay off’: from Ernan Cui of Gavekal Dragonomics

Jaguar Land Rover bonds issued in September now trading at 76 cash price.

Global stocks have lost $300bn in mkt cap this week as trepidation around growth in Europe, no progress on US-China trade issues, & disappointing earnings season result to some profit taking. Ind Production in Germany came in well short of expectations & Spain saw 1.4% mom drop.(Holger)

Forget rate hikes. Is the FED already too late in cutting the rates. The BLOOMBERG Bankruptcy Index (BNKRINDX) is +155% YTD.

German 10Y (BUND) looks sick. I think it is headed for negative yield again coupled with parity on Euro/Dollar.

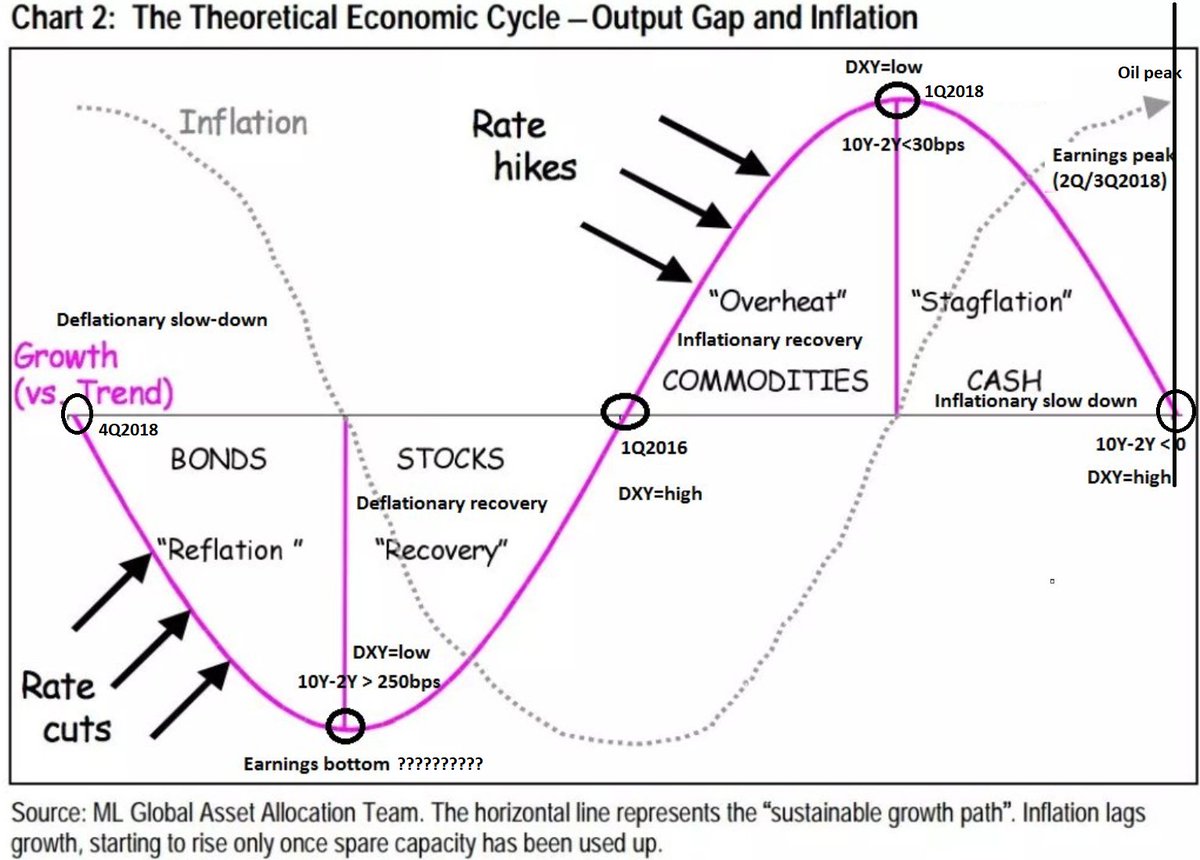

So, as expected in June2018 prediction oil has peaked around 3Q2018, so inflationary expectations. Earnings have peaked around 2Q/3Q2018 with much weaker expectations for future. We are entering rate-cuts period and market expects to go into recession starting 1Q/2Q2019..@analyst_G

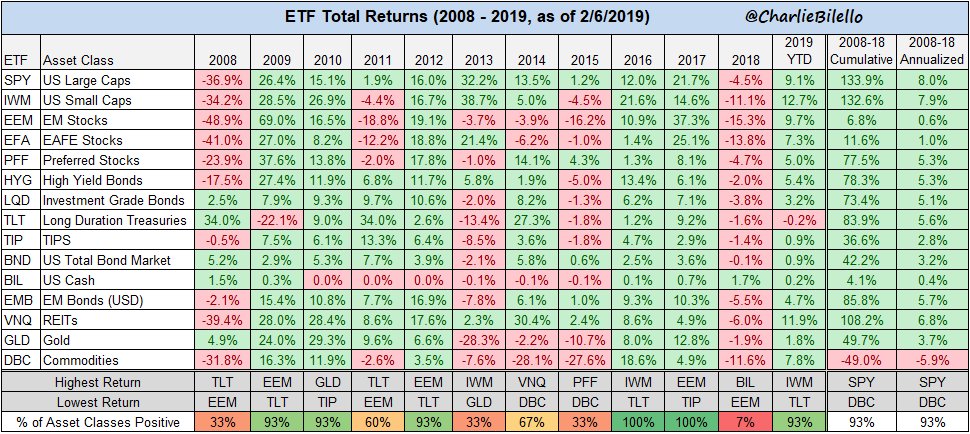

In 2018, out of 15 major asset class ETFs, only 1 finished positive (Cash). In 2019 thus far, only 1 is negative (long-term Treasuries)… TILL NOW

Severe damage to global growth has been spotted – prepare for a rough ride in the months ahead. I don’t think the policies were/are in place by CBs to counter this rapid slowdown. Any monetary policy maneuver by CBs work in 4 to 6 months lags. Alastair Williamson

I will Gladly will take the other side of this

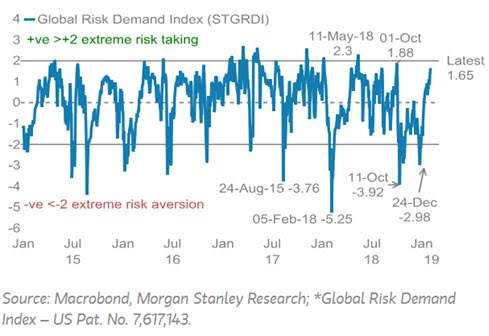

Risk appetite soars….

Almost 40% of the yield curve is now inverted from the 30-year to overnight Fed Funds Rate. This is the same level as the start of the Tech Bubble and Housing Bubble collapses in 2000 & 2008 The debt market knows all. Via @TaviCosta

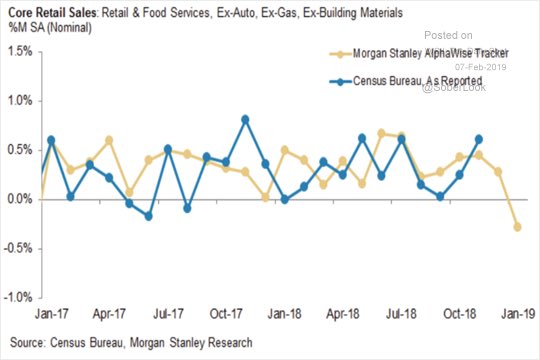

After a relatively strong holiday shopping season, retail sales weakened sharply in January…see @MorganStanley retail sales tracker @SoberLook

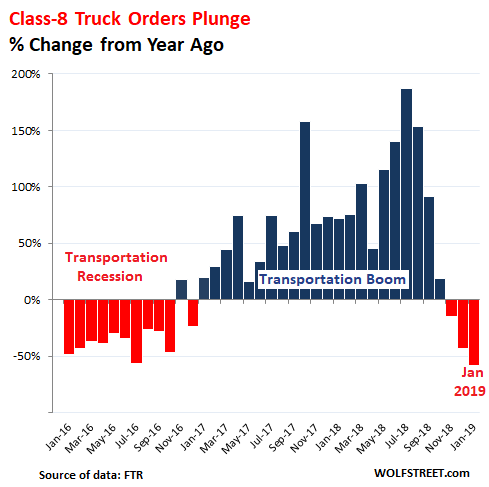

The chart below shows the percent change of Class-8 truck orders for each month compared to the same month a year earlier, which eliminates the effects of seasonality. The year-over-year plunges in December and January are on par with happened during the last transportation recession (wolfstreet.com)

The 2017 tax reform made it easier for U.S. firms to bring profits booked offshore home (no complex gymnastics required), but it did not – change the basic incentive to shift profits and in some cases jobs offshore. Brad Setser

The biggest U.S. emerging-markets debt ETF has grown at an accelerating clip, adding about $2.6 billion in new money so far this year. In the past three years, the fund has more than quadrupled its assets, to $17.5 billion, exceeding the size of the biggest HY bond ETF $HYG

Buy the dip and search for yield is alive and kicking

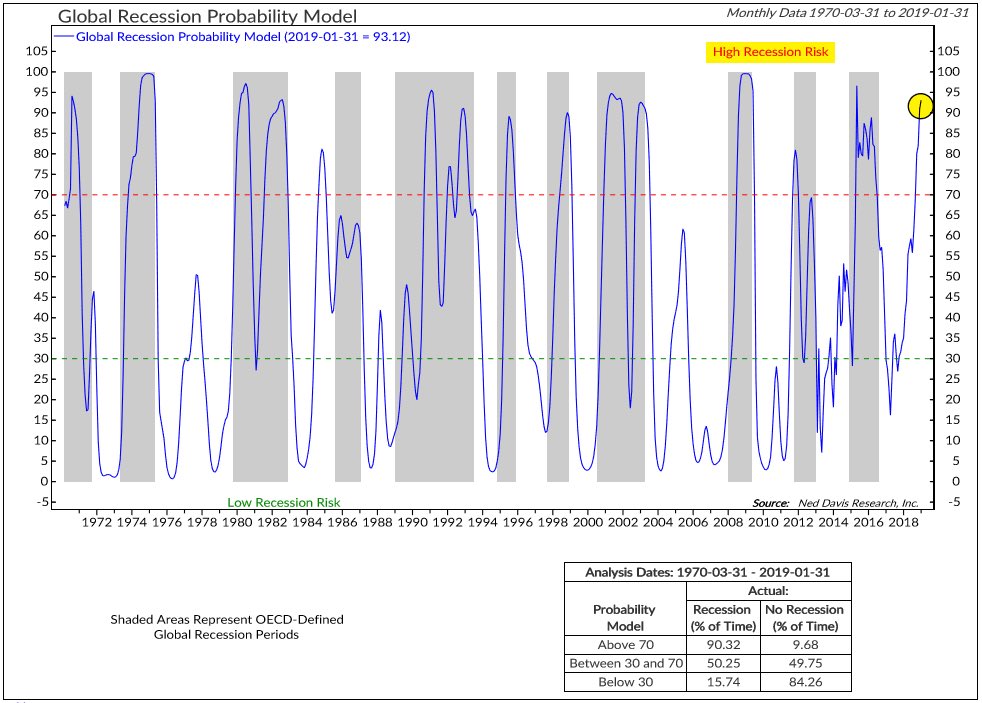

NDR global recession probability now at 93. Hmmm……

The recession risk over the next 12 months is now a whopping 49%. That is the conclusion judged by a model build on the difference between expectations vs. current conditions in the US consumer confidence data. More in our weekly -> https://ndea.mk/2MPjtRT

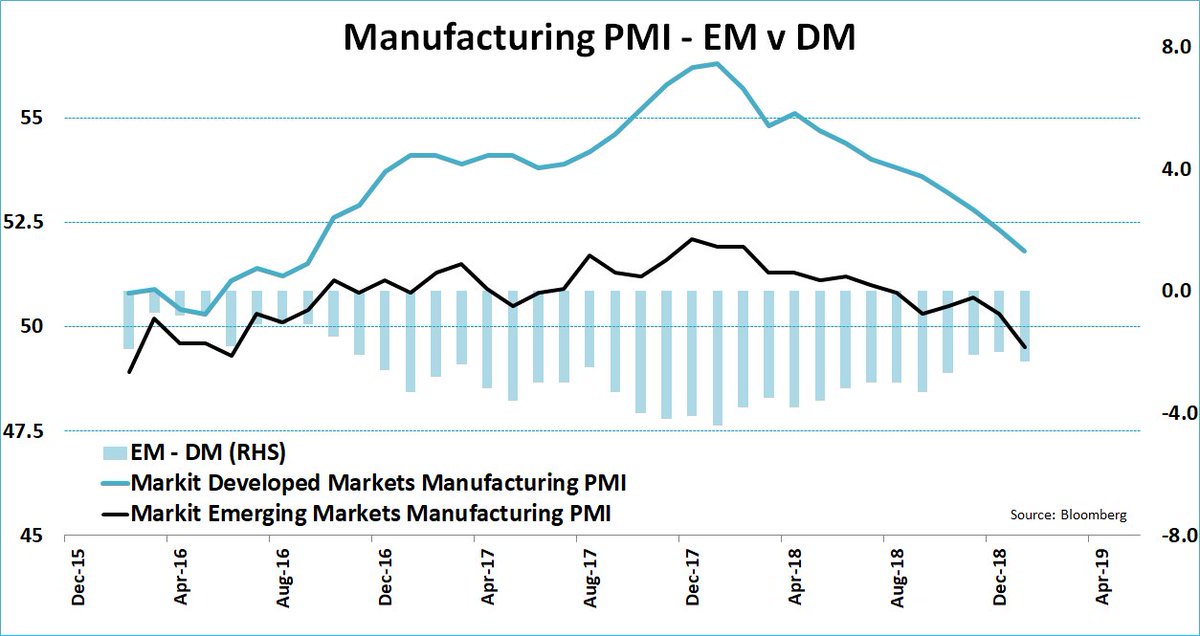

In case you missed it! The EM Manufacturing PMI fell below 50 for the first time since July 2016 in January.

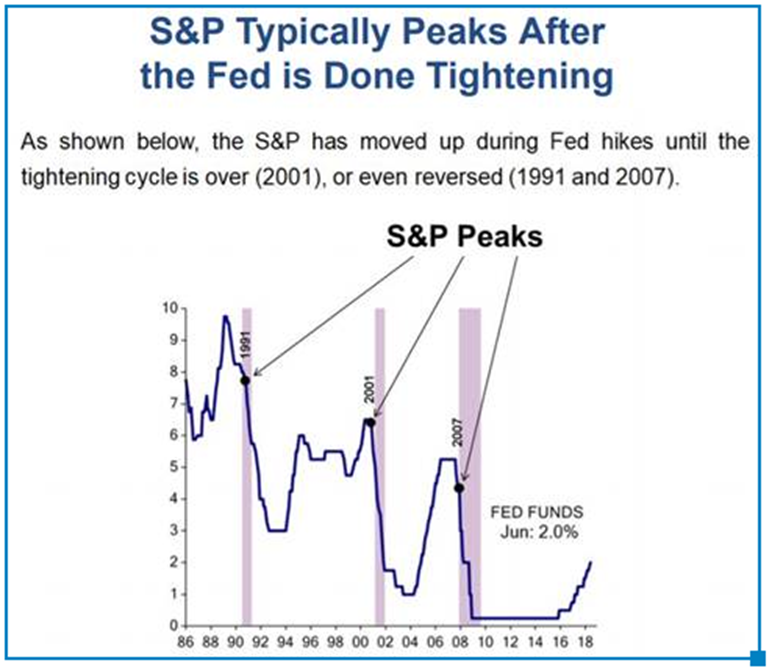

While we get excited about the Fed’s “U-turn,” we should note that the S&P 500 Index peaks after the Fed is done tightening and changes paths and not before. This next chart from Ed Hyman shows us that the last Fed interest rate hike is always the mistake. It shows us that markets peak after the Fed is done tightening and reverses course.

Panic is over. With market moving higher complacency is setting.

Substantial Downside Risk

January proved to be a welcome turn in fortune for markets. Risk assets have rebounded strongly, rally has been broad-based across not only equities and credit, but also commodities and rates, DB says. All of 38 assets in DB’s sample finished w/ a positive total return.