While everyone is looking at gold in USD, have a quick look at this chart. Gold in World Currency is running like it stole something the last couple of weeks. That’s the breaking of a 7 year old resistance .(Laurenz)

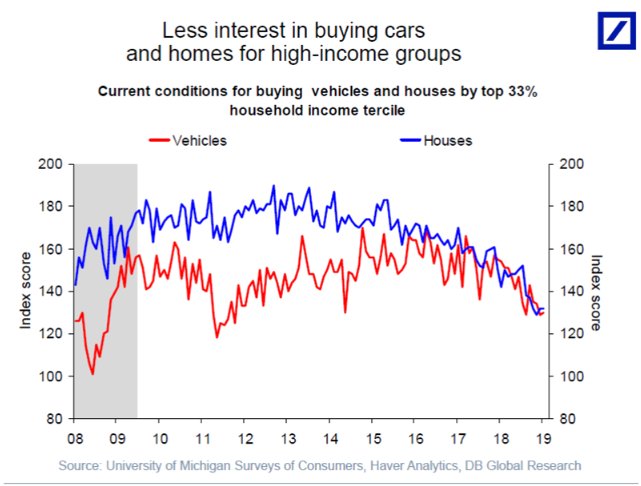

“We are getting more worried about downside risks given the declining appetite among consumers for buying cars and homes, in particular among high-income households:” Deutsche Bank’s Torsten Slok, who created this chart:

Global stocks drift ahead of Fed meeting. Investors expect dovish Fed, focus on balance sheet. Apple outlook gives tech shares a lift. Yuan climbed to highest since Jul as US-China trade talks get underway in DC. Pound falls after UK parliament vote. Bonds steady w/ US 10y at 2.71%.Lets see if FED changes its tune today and bow down to the market tantrums

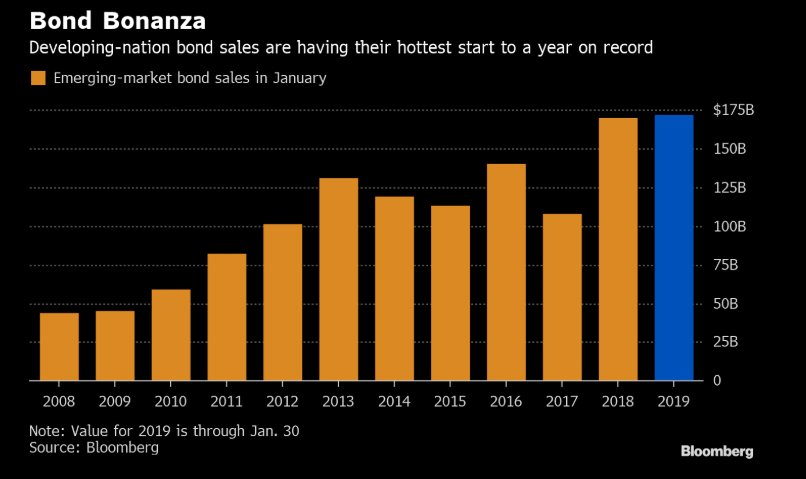

This month has been the most-active January for emerging-markets bond sales on record.

This US china trade war is not about few hundred billion of trade deficit US runs with China. Neither it is about China holding leverage over US in the form of its Treasury holding. This game is about Tech dominance and US knows that if it allows China to dominate in Tech world then it looses its edge and leverage.

There are links to video below where Bloomberg Businessweek’s Ashlee Vance heads out into a city where you can’t use cash or credit cards, only your smartphone, where AI facial-recognition software instantly spots and tickets jaywalkers, and where at least one factory barely needs people. This is the society that China’s government and leading tech companies are racing to make a reality, with little time to question which advancements are net positives for the rest of us.

More signs of Chinese capital outflows rising again: China’s imports of precious stones accounted for 69% of overall imports from Hong Kong last month. Highest % since the mini yuan devaluation in August 2015. Via @Bloomberg & @RBC

The number of electric vehicle sales is expected to rise to 64 million annually in 2040, from basically zero in 2016. For reference, global total vehicle sales totaled 83 million in 2016 (latest available number).

The shale industry has relied heavily on debt to finance its growth, with E&P companies raising about $300bn from bond issuance over the past 10 years. As crude prices started to slide last October, that source of capital was choked off. https://www.ft.com/content/0a18f0b0-1eab-11e9-b126-46fc3ad87c65 …

China’s Corp Debt has increased >100,000% in less than 20 years. But this is not just a China problem, it’s global, and not just in corp debt. When this implodes, central banks will print and #Gold and #Silver will explode higher. h/t @mike_maloney

Pretty stark chart from JPMorgan. The US stock market has grown by $13.7tn since the end of the financial crisis, helped in large part by nearly $5 TRILLION of buybacks. That’s bigger than the Fed’s entire QE programme.

High yield issuance relative to total issuance at a decade low. it seems the Party is getting over..

US inflation about to surprise negatively. In my view US bonds are quite cheap compared to US equities

Leading indicators still point to a significant global slowdown. ECRI Weekly Leading Index Update: YoY at 6+ Year Low

Global Industrial Slowdown to Worsen With Chinese industrial growth prospects fading further, a disinflationary drag will continue to propagate through international supply chains. Plunging Pace of Production The global industrial slowdown we first forecast a year ago is in full swing and set to worsen. Meanwhile, with purchasing managers indexes actually lagging last November’s peak in global industrial production growth, the consensus was caught behind the curve. Since then, growth in the Global Industrial Production Index (GIPI) has plummeted to its lowest reading in nearly two years (Chart 1, bottom line). But, with Global Leading Manufacturing Index (GLMI) growth approaching its lowest reading since late 2015 (top line), GIPI growth is poised to fall further still. In other words, the global industrial slowdown is set to intensify in the coming months. In line with this cyclical downturn, growth in ECRI’s Industrial Price Index (IPI) – a measure of commodity price inflation – has nosedived deep into negative territory, having dropped to its worst reading in more than 2½ years (not shown). Given the downturn in GLMI growth, there is still more downside risk for IPI growth. Notably, this is a broadbased decline in IPI growth. Specifically, growth in the IPI’s Petroleum Products Sub-Index, having turned tail a couple weeks ago, is now approaching the lows that followed the abortive supply-driven spurt early this year. Growth in the IPI’s Textiles Sub-Index plummeted recently to its lowest reading since early 2015. Finally, growth in the IPI’s Metals and Miscellaneous Products SubIndexes tumbled lately to their lowest readings since early 2016

JPMorgan reported growth of 1% from a year earlier in commercial and industrial loans, down from 4% in the prior quarter, which Chief Financial Officer Marianne Lake said was partly because the bank had pulled back from lending in particular areas and partly because of a general slowdown in the economy. The bank also increased loan-loss reserves in its commercial-banking book moderately. On a conference call, Ms. Lake characterized the reserve build as being in “a handful of names in a handful of sectors, nothing that points to a systematic deterioration in a particular sector.” Nonetheless, it signals increased caution by the bank that the credit cycle is set to turn following years of historically low defaults.

JPMorgan Chief Executive James Dimon was frank that the bank wouldn’t hesitate to pull back more on lending if needed. “We have no problem seeing the loan book shrink,” he told analysts. “We are not going to be stupid.”

This tightly correlated chart would suggest that your forward equity returns are going to be very disappointing…

@TihoBrkan: High exposure by the US households towards equities — like we see today — has historically been a predictor of poor subsequent returns. The correlation between this indicator and $SPY 10-year annualized return is close to 90%.

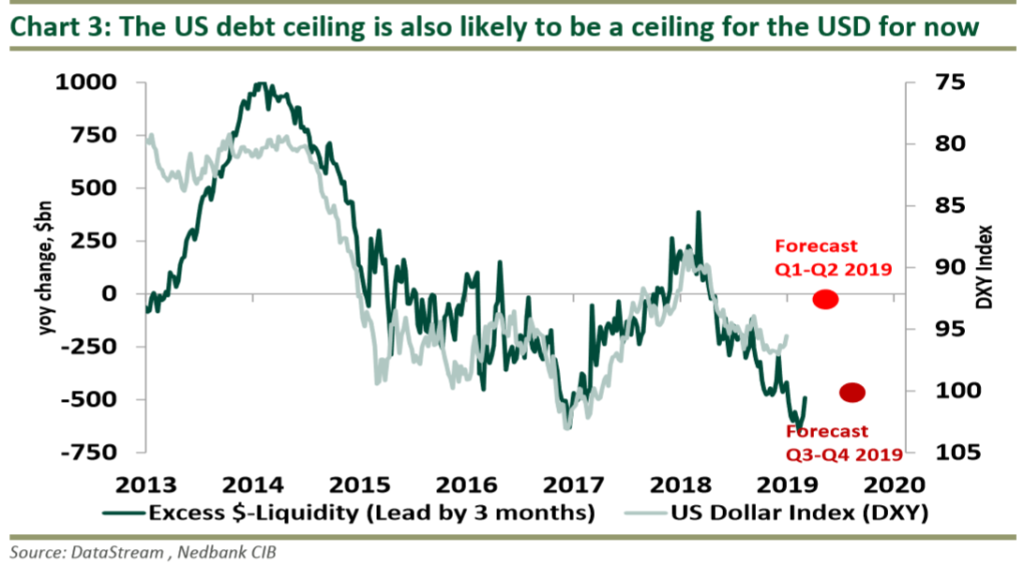

Nedbank writes…$-Liquidity is set to improve over the next three to six months amid reaching the US debt ceiling. We estimate that the excess $-Liquidity stemming from the US Treasury will offset the Fed’s “quantitative tightening” (QT) programme. This will likely be a temporary boost to $-Liquidity in the global financial system, which should ease financial conditions and support financial markets, particularly risk assets (EM) which are sensitive to the US Dollar.

The US debt ceiling (USD22tn) is a legislative debt limit on the amount of national debt that can be incurred by the US Treasury, limiting how much money the government may borrow. When the debt ceiling is reached, the US Treasury cannot issue more debt. As a result, the US government would find it difficult to fulfil many of its obligations, with unintended negative consequences for the US economy. However, the US Treasury can utilise the TGA (US federal reserve and US treasury) to inject cash into the US economy only if there is no agreement on the debt ceiling between the Democrats and Republicans before the deadline: 1 March 2019. Rarely in history has an agreement been reached before the deadline. We believe this time will be no different given the current political environment in Washington. Therefore, we believe the US Treasury will have to inject dollars into the economy and banking system via its TGA . The rise in $-Liquidity should ease financial conditions and support risk sentiment towards risk assets inside and outside of the US.

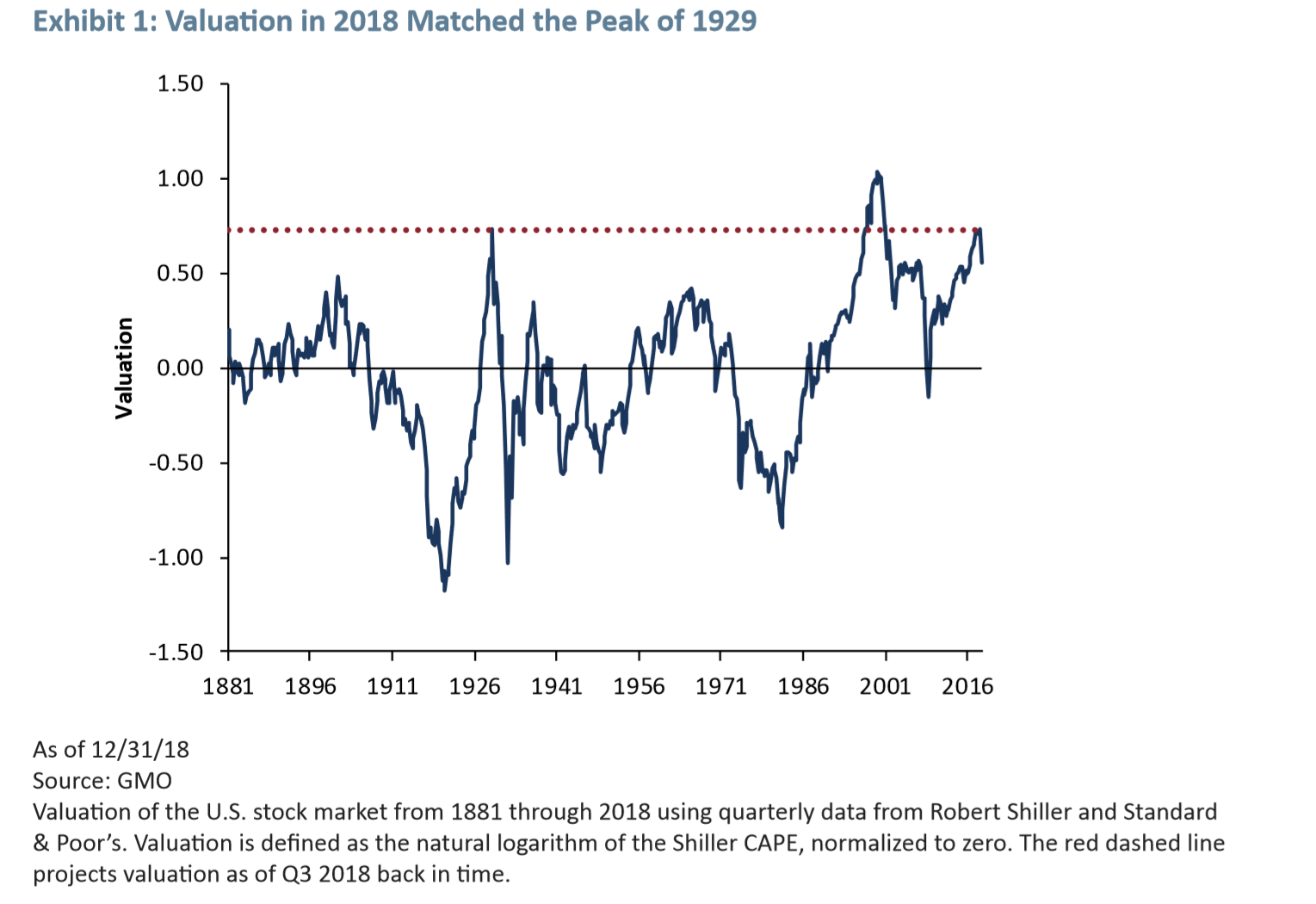

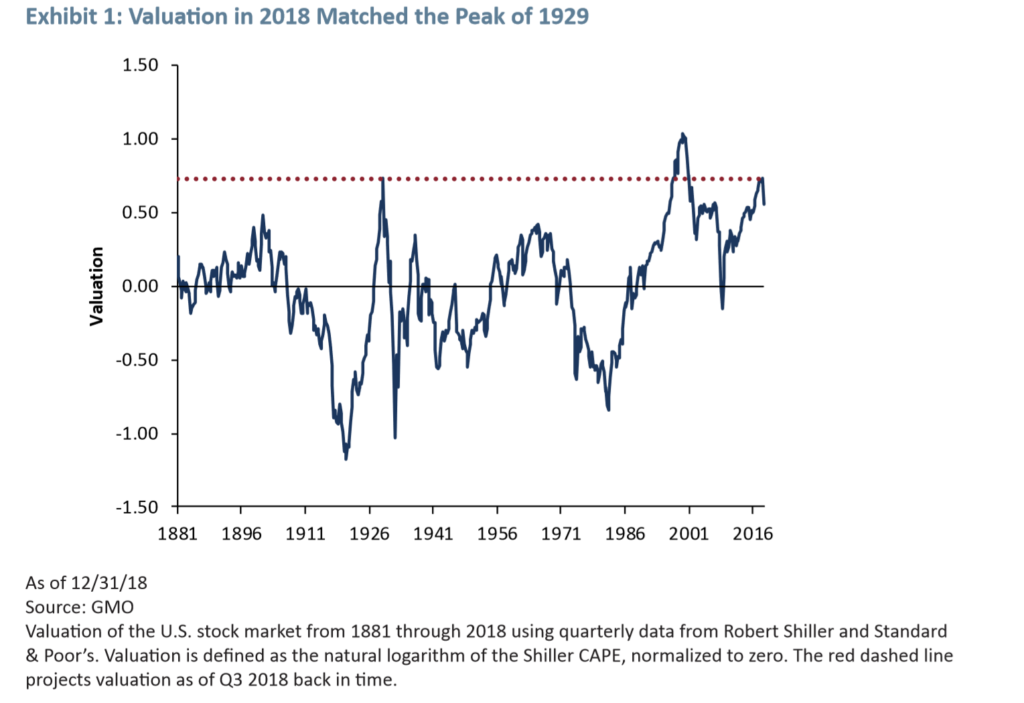

GMO writes in a white paper …Is the U.S. Stock Market Bubble Bursting? A New Model Suggests “Yes”

The paper warns “Own as little U.S. equity today as your career risk allows”

China liquidity injection at a record level. Inconsistent with a strong and healthy economy.

Probably a chart you should see

Last year the Indian government blamed the Rupee weakness on the US dollar .This year they might blame Rupee weakness on something else, but it is the incorrect monetary policy followed by the Reserve bank of India… Danielle

The biggest issue China faces is that their growth model is debt funded. Tightening put the brakes on this and growth predictably rolled over. Without large scale QE (which only makes their housing bubble worse) they are reaching the limits of what they can do to stimulate.

S&P500 vs. Bloomberg Commodity Index: At some point the crocodiles mouth will snap and financial assets will be revalued vs. real assets…

The Fed can resume hiking: Since Dec 24 financial conditions have eased by the equivalent of two and a half rate cuts

All in The last one month …

Europe’s most important river is running dry: The Rhine waterway, critical to moving coal, car parts, food and thousands of other goods, risks becoming impassable because of climate change