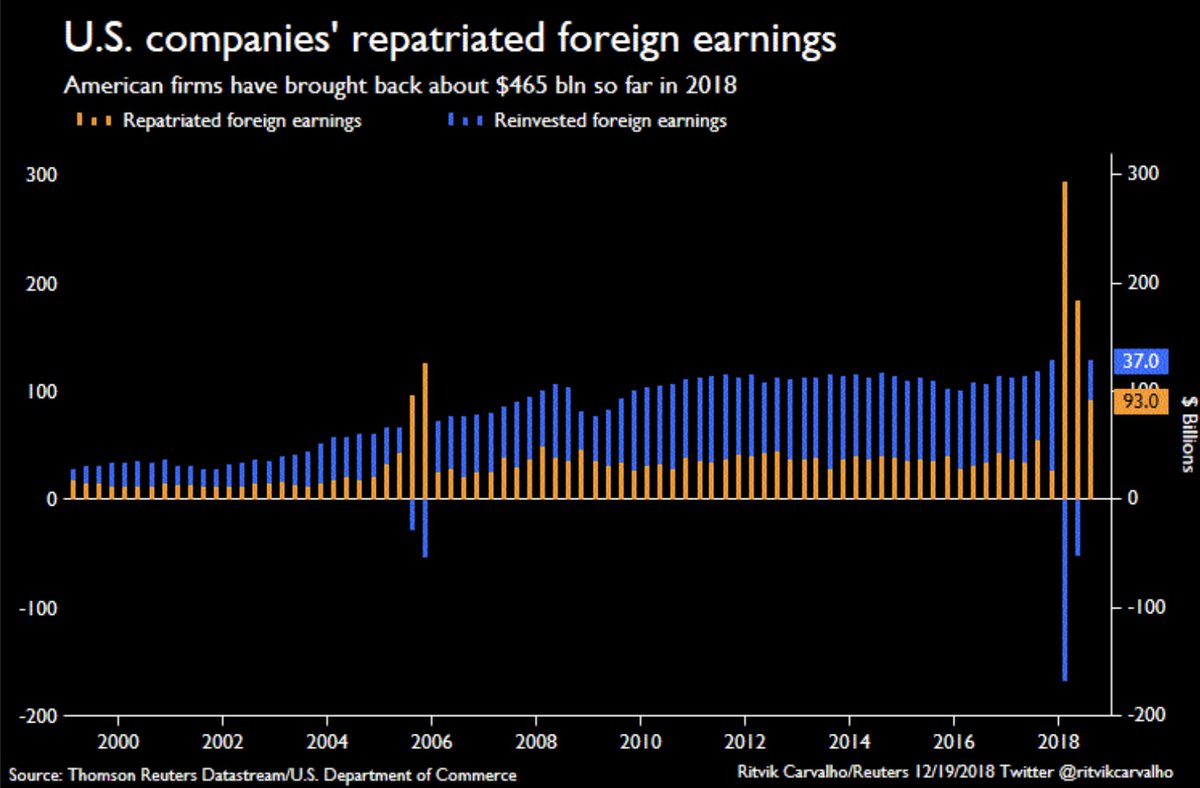

Popular belief has it that gold prices have not performed especially well despite some egregious geopolitical and economic factors. Well measured in 72 currencies, gold is at … or within a few percentage points … of being at an all time high for people in those countries. Not on the list are the British Pound, the Swiss Franc, the Euro and Chinese Yuan – but we are not far off in all of those currencies too. Only in USD does gold lag – and not all of us live in the US.

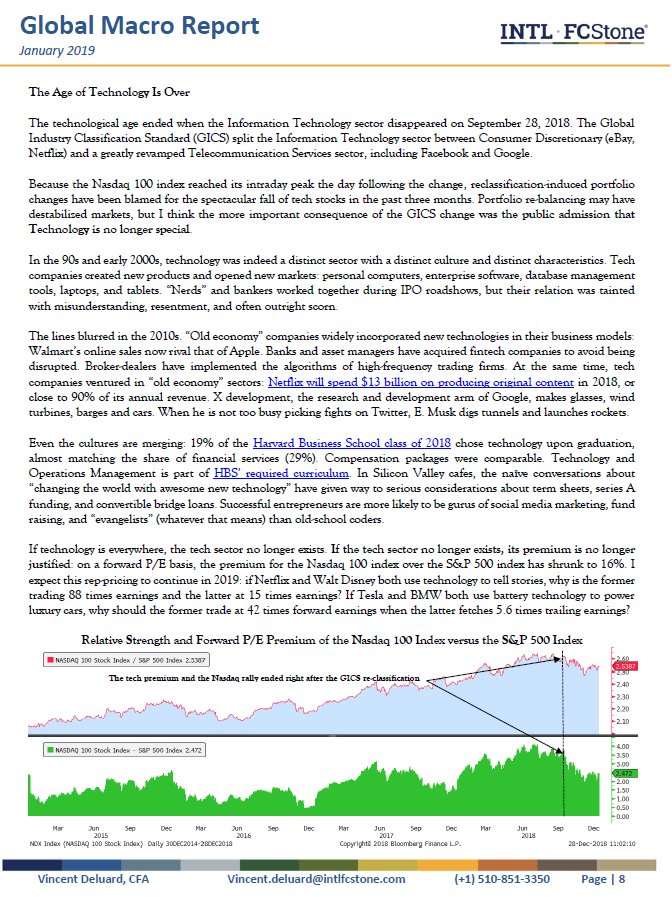

The age of Technology is over- Vincent Deluard

If technology is everywhere, the tech sector no longer exists. If the tech sector no longer exists, its premium is no longer justified: on a forward P/E basis, the premium for the Nasdaq 100 index over the S&P 500 index has shrunk to 16%. I expect this rep-pricing to continue in 2019: if Netflix and Walt Disney both use technology to tell stories, why is the former trading 88 times earnings and the latter at 15 times earnings? If Tesla and BMW both use battery technology to power luxury cars, why should the former trade at 42 times forward earnings when the latter fetches 5.6 times trailing earnings?

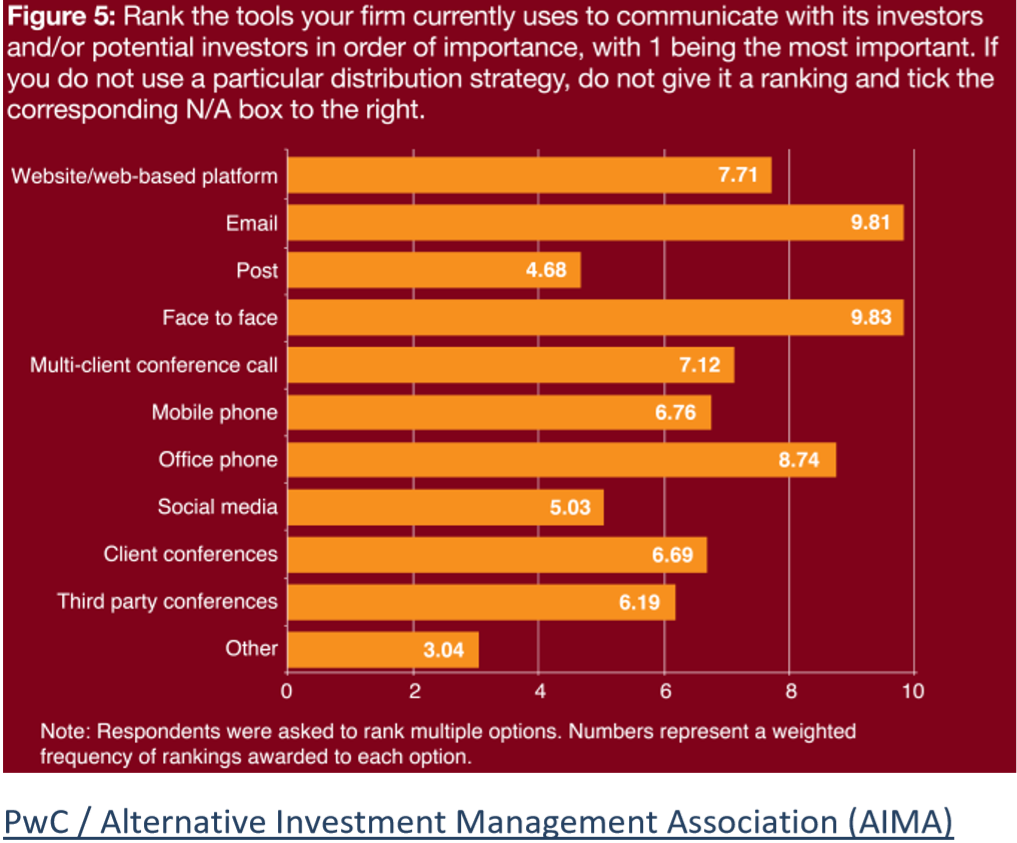

Face-to-face access still prized above all else

Is 2019 going to be the year of the profit margin problem?

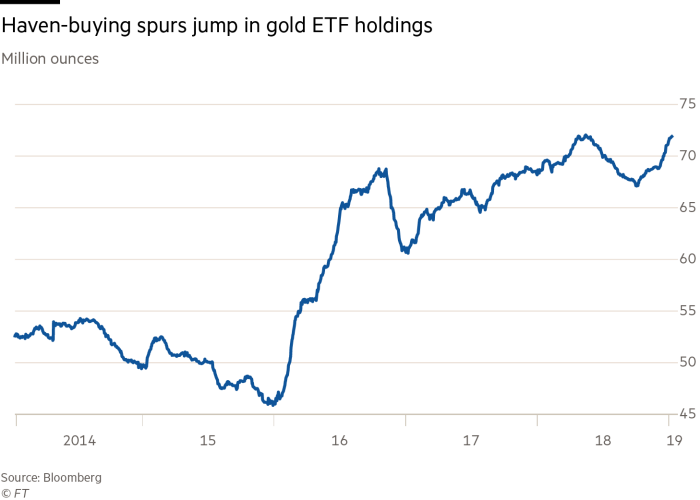

If we continue to see elevated levels of macroeconomic uncertainty and risk adversity, then gold will probably continue its positive momentum

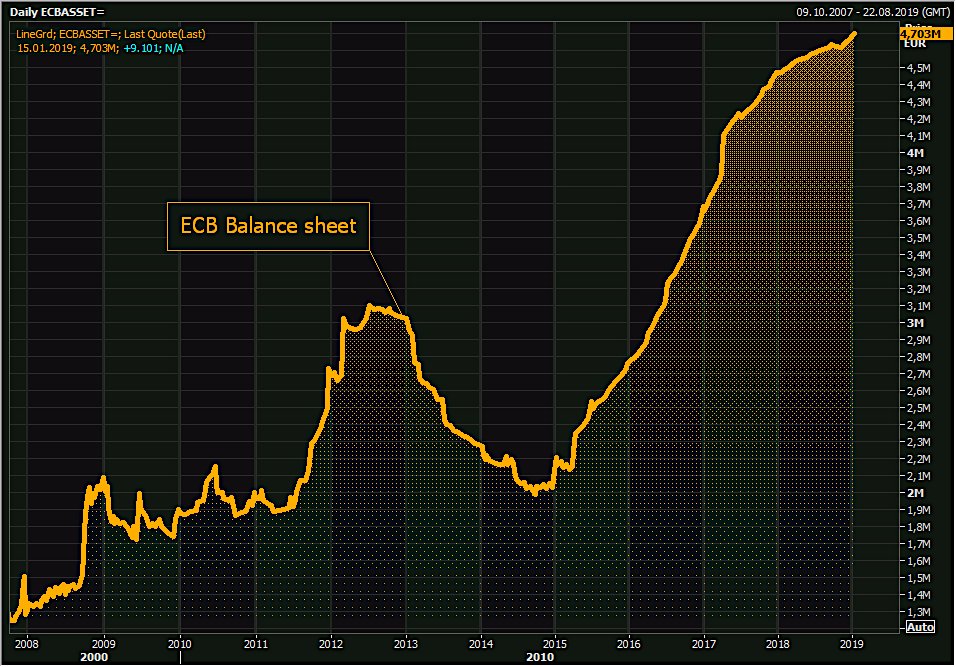

ECB Balance sheet hit fresh all time high at €4,703.4bn as QE reinvestments higher than redemptions. ECB balance sheet now equates to record 42% of Eurozone GDP while Fed’s balance sheet has shrank to 19.6% of US’ GDP.

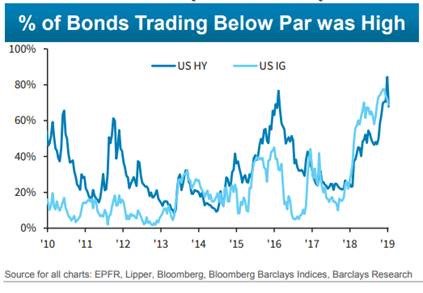

Higher yields + wider spreads in 2018 have left nearly 80% of corporate credit trading below par – highest % in the last decade.

European debt

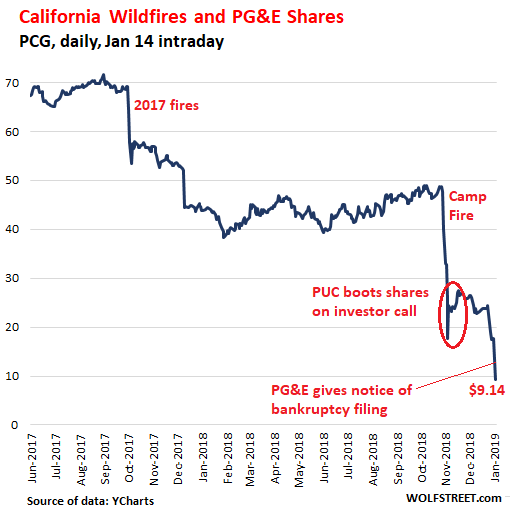

Utility companies are safe? Think again. Bankruptcy Next, PG&E Says. Shares Down 90% in 15 Months. From “Investment Grade” to “Default” in Three Weeks

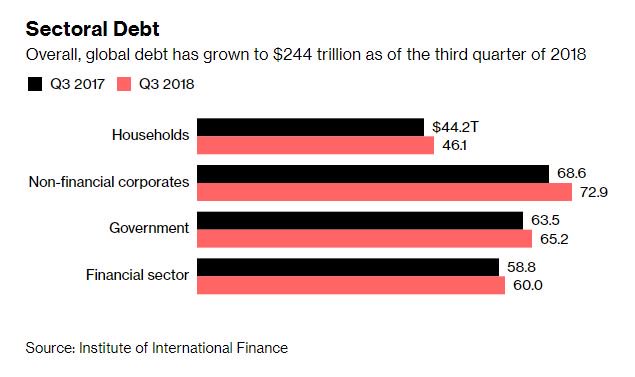

The world’s debt pile is hovering near a record at $244 trillion

Political risks remain high in 2019 as critical elections could lead to policy turns or surprise outcomes: In EM, India, South Africa and Argentina are elections w/ highest stakes this year. In DM, Europe will be closely watched. Standard Chartered runs electoral heatmap 2019.

Interesting chart from TD Securities

Corp earnings were grossed up artificially by a doubling of US gov’t spending and debt, far above what US consumers had to use. The debt spiral we’re in now makes statistics

The NY Fed recently updated its recession-risk model – up to 21.4% in December, from 15.8% in November and 14.1% in October. The odds have doubled in the past year and haven’t been this high since August 2008.

Relative sizes of global asset classes….gold is currently at roughly 7 trillion

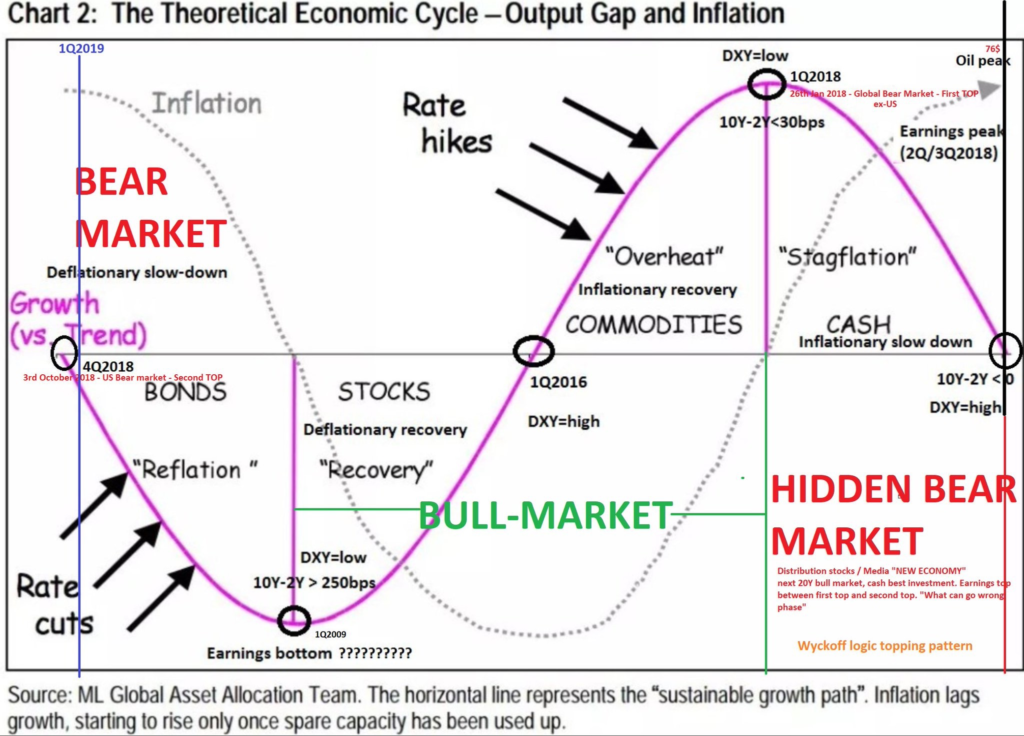

An excellent chart from Merill – I think this deflation will move into stagflation this year.

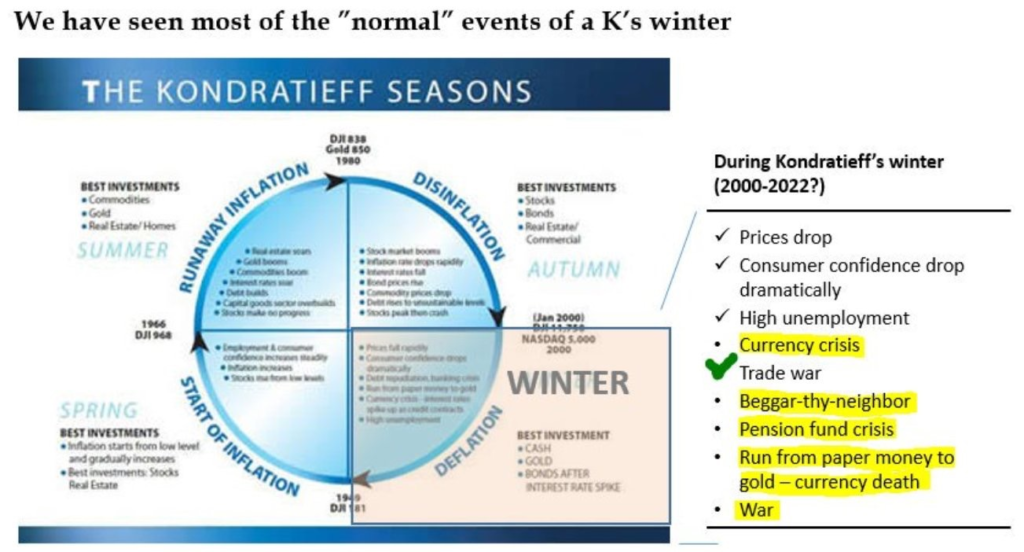

This is how Kondratieff Winter plays out-Henrik

US govt has been spending 5 times the rate of GDP growth. what if they stop spending?

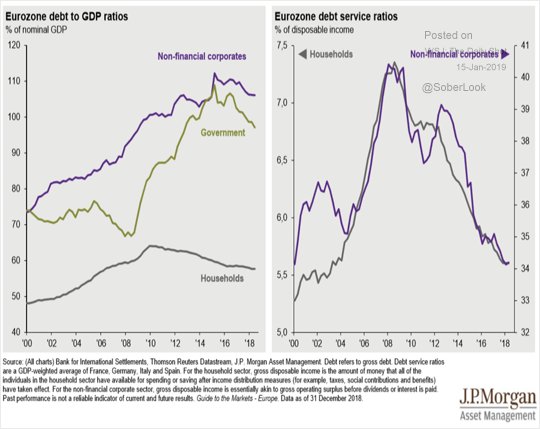

Why Europe is in a bigger trouble than US

US vs Europe Stocks…. US stocks are much less indebted than Eurozone ones, yet most of the focus of analysts is on US companies’ leverage. The difference between the S&P 500 and the Stoxx 600 is enormous. ( Danielle)

Shorting Bunds is the new widow maker trade: Bill Gross’s bond fund assets decline below $1bn from February’s all-time high of $2.24bn as fund lags most peers amid misplaced bets that rates on US Treasuries and German bunds would converge.(Holger)

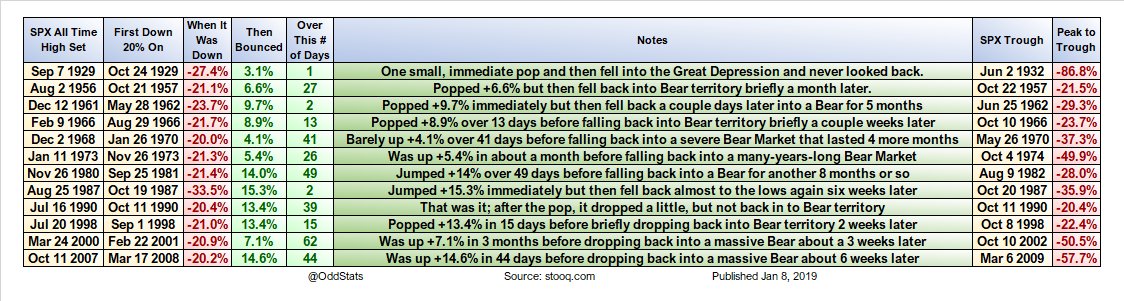

Here is every prior Bear Market in SPX history (-20% drop from a unique All Time High) with dates/notes on the initial bounce after first entering Bear territory and then what it did next. The NOTES column is the most important.

Goldman writes….Equity prices have tracked negative earnings revisions, but earnings season will represent an important litmus test for the near-term path of the S&P 500. FY2 EPS revisions sentiment, defined as the number of positive EPS revisions less the number of negative EPS as a share of total revisions, has slipped into negative territory. The path of S&P 500 returns has generally tracked this revision sentiment. Earnings revisions briefly stabilized at the end of 2018, but AAPL’s guidance set in motion further negative revisions, with sentiment declining from –14% to –23% in the past week. With no nascent signs of slowing negative revisions, the strength of 4Q results and management commentary around the outlook for 2019 will take on heightened importance for whether earnings estimates (and returns) stabilize in the near term.

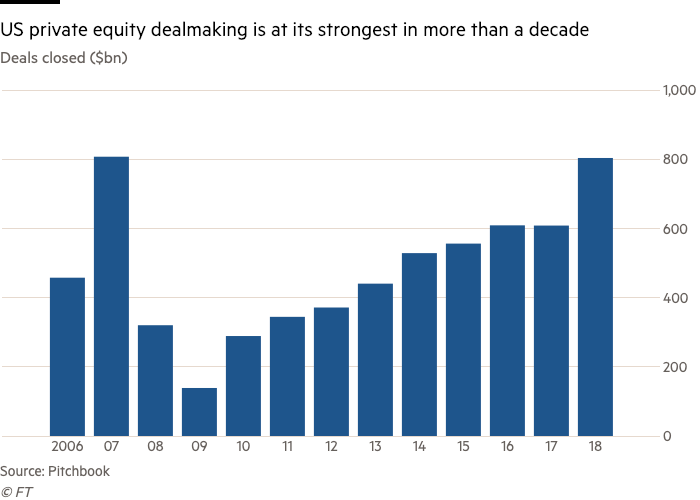

Private equity dealmaking in America last year reached the highest level since 2007, with investors buying $800bn of companies and a record proportion of deals involving richer-than-usual valuations.More than three-fifths of the transactions were struck at a purchase price that was at least 10 times higher than the acquired company’s annual profits, according to an analysis by data provider Pitchbook. That was the highest rate on record, showing that dealmakers showed increasing appetite for expensive acquisitions even in a year when stock market valuations fell sharply.

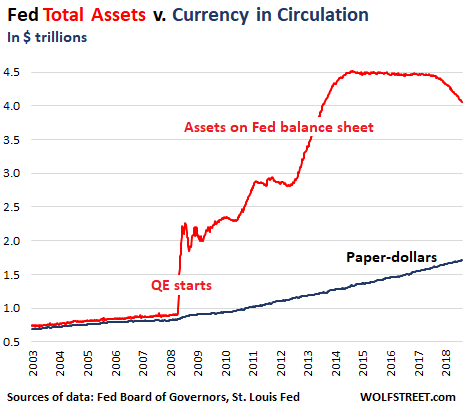

The relationship between currency and assets is key. This is what Powell referred to when he said that the level of assets “would depend really on the public’s appetite for our liabilities, specifically currency.”

And so, he said, the balance sheet “will be substantially smaller than it is now,” but given the surge in currency in circulation, it will be “nowhere near what it was before.”

At the demand rate for currency over the past 10 years, there will be about $2.2 trillion of currency in circulation in 5 years. That means that the balance sheet, if it is going to be just 10% larger than currency (see the chart) in circulation, would need to be near $2.4 trillion in order for the old pre-QE relationship to be re-established. This means, the Fed would have to shed an additional $1.6 trillion in assets over the next five years.

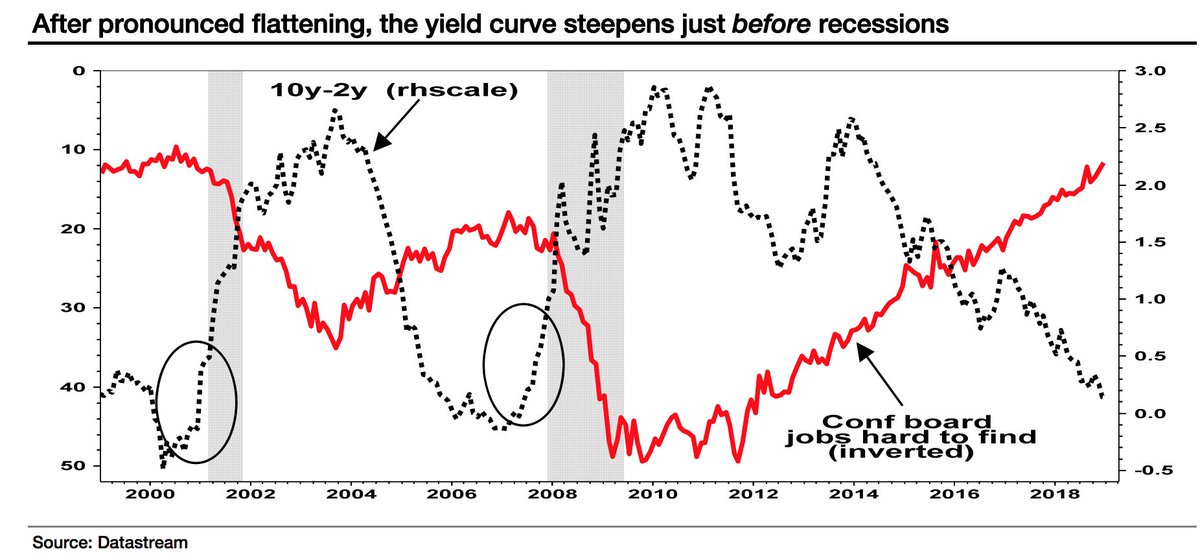

Latest US curve steepening, after a period of pronounced flattening, is a good indication of imminent recession despite continued strength in the labour market, SG’s Edwards says. The yield curve steepens just before recessions.

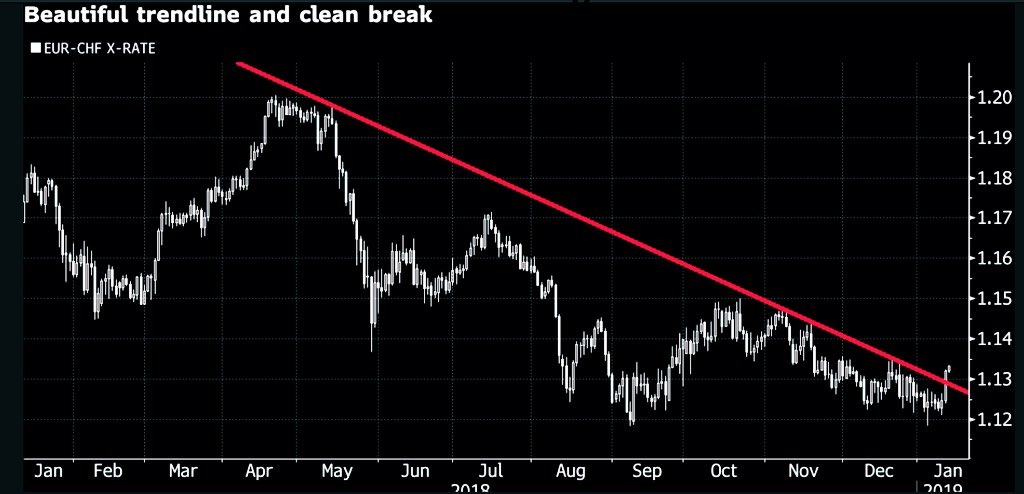

Thursday’s sharp weakness in Swiss Franc could be the start of a fresh medium-term trend. CHF is comfortably the most expensive currency in the world, according to IMF PPP metrics. And yet it offers the most negative yields in the world. Is something changing there?

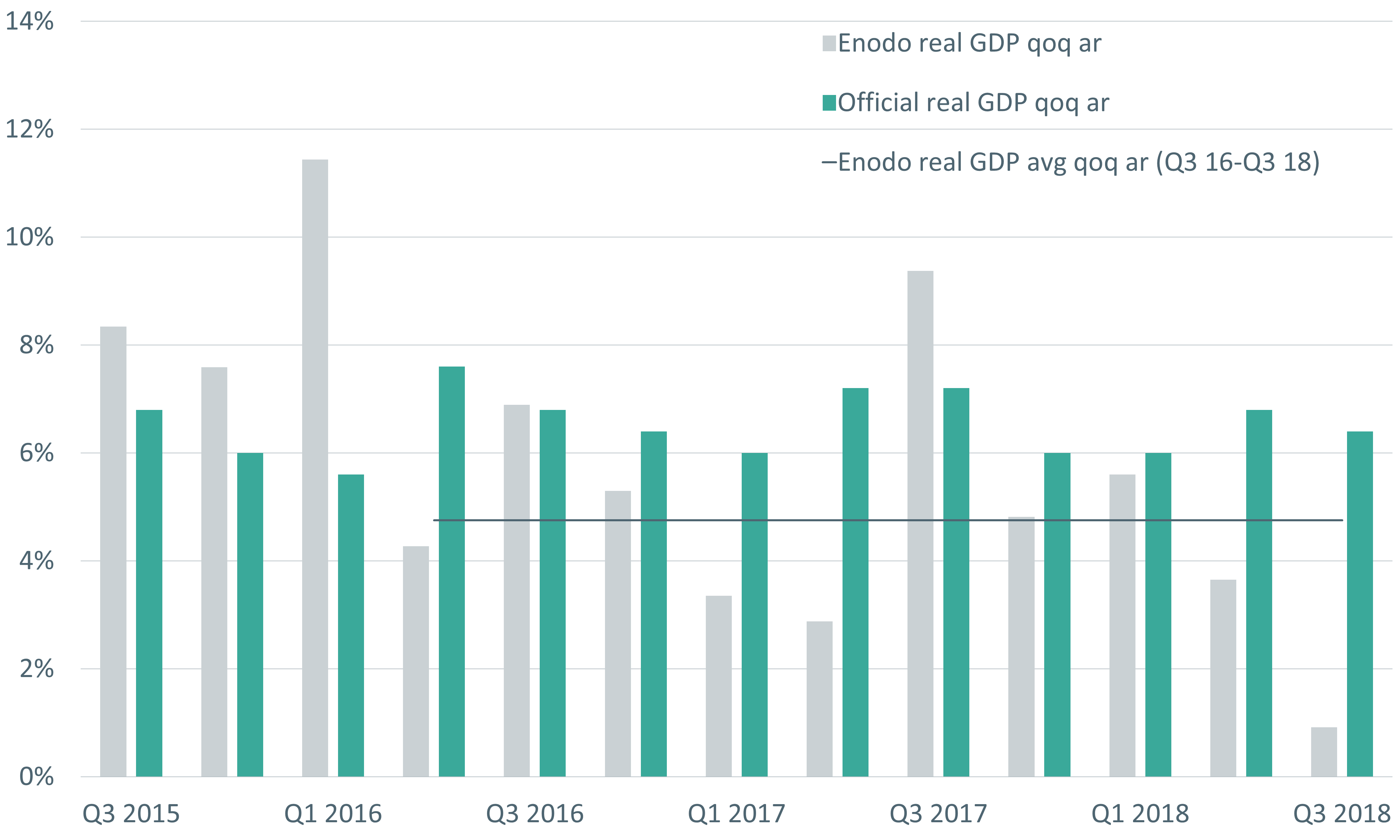

Enodo’s (my favourite china watcher) estimate put real growth at 0.9% in Q3, the weakest quarterly annualised rate since we started producing estimates in 2004 – even lower than the trough of 1.9% during the global financial crisis. Annual growth slowed to 3.7% by our reckoning, compared with 5% in the crisis.

Enodo estimate for Q3 growth is 0.9 percent qoq ar

Preliminary Enodo quarterly annualised growth

“Raising rates will lead to less borrowing….”right? but have a look at the accompanying chart what’s happening here?

An example of how corporate borrowing costs are rising: Anheuser-Busch, which packed on $95 billion of debt after purchasing SABMiller in 2016, is now trying to refinance. Its bonds sold less than a year ago have fallen by about 15 cents on the dollar.

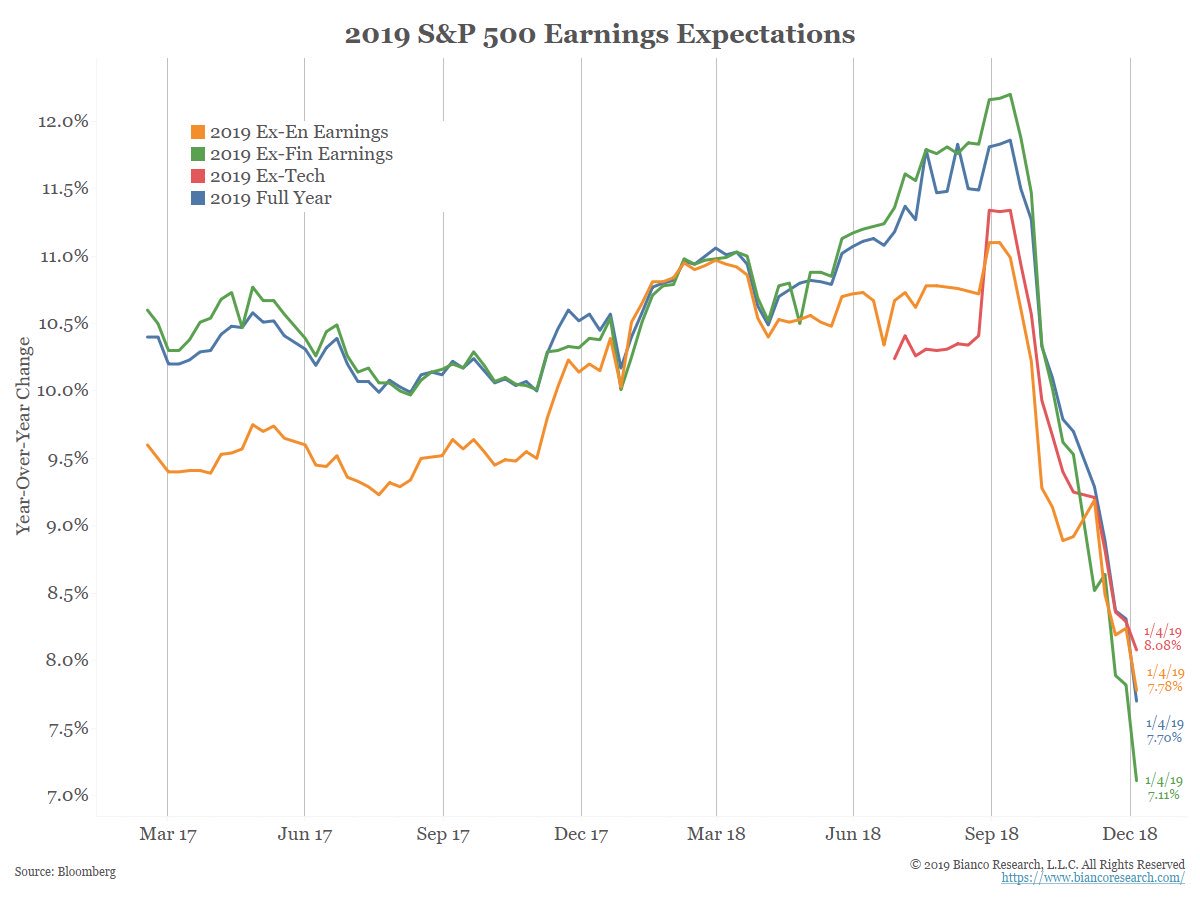

Significant plunge in 2019 S&P earnings expectations since last September @biancoresearch

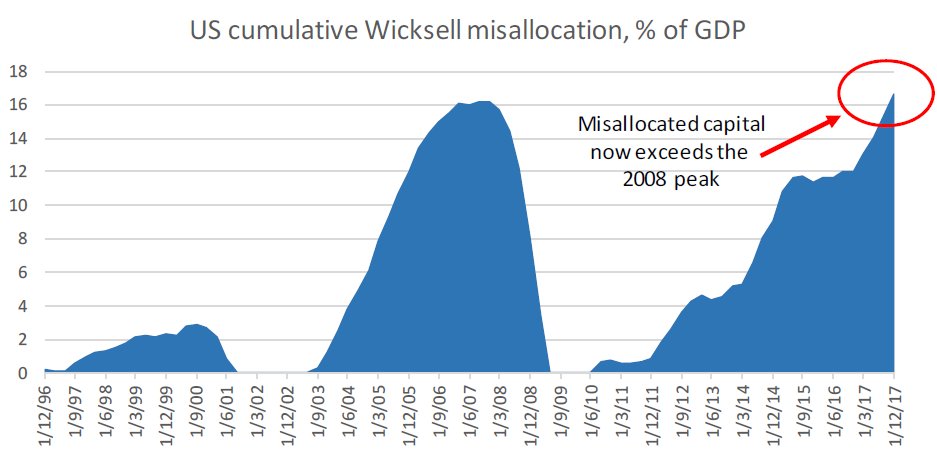

Wicksell Spread: There is a greater degree of capital misallocation today than there was on the eve of the great financial crisis and five times more than in 2000.

Euro Jumps >$1.15 on Dollar weakness following dovish Fed remarks. Fed member Bostic says policy could move in either direction: open to rate cut if downside risks all come to bear.

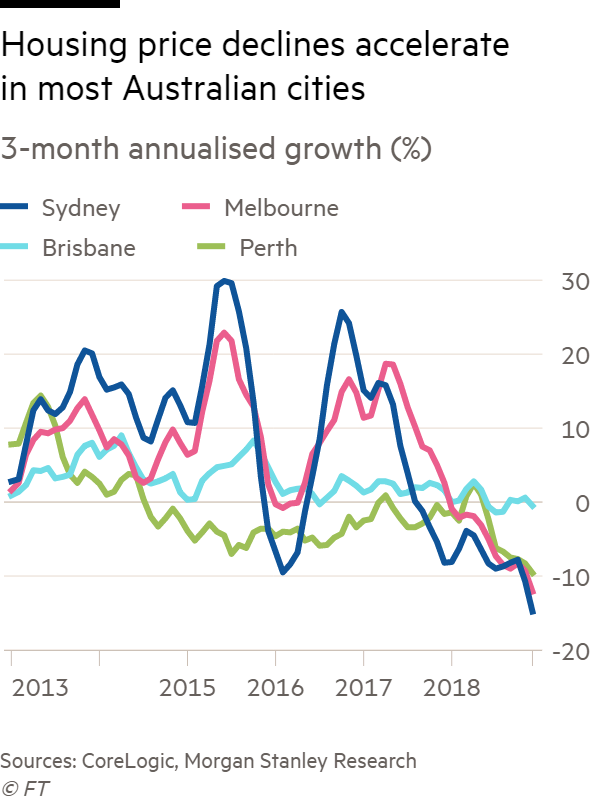

Australia’s house price slide is now the deepest in 35 years: posing a serious threat to the lucky country’s record breaking economic run

The offshore Chinese yuan climbed to the strongest level since August …..impressive and this is the invisible hand in risk rally

Great excerpt from new @Realvision interview with Diego Parrilla

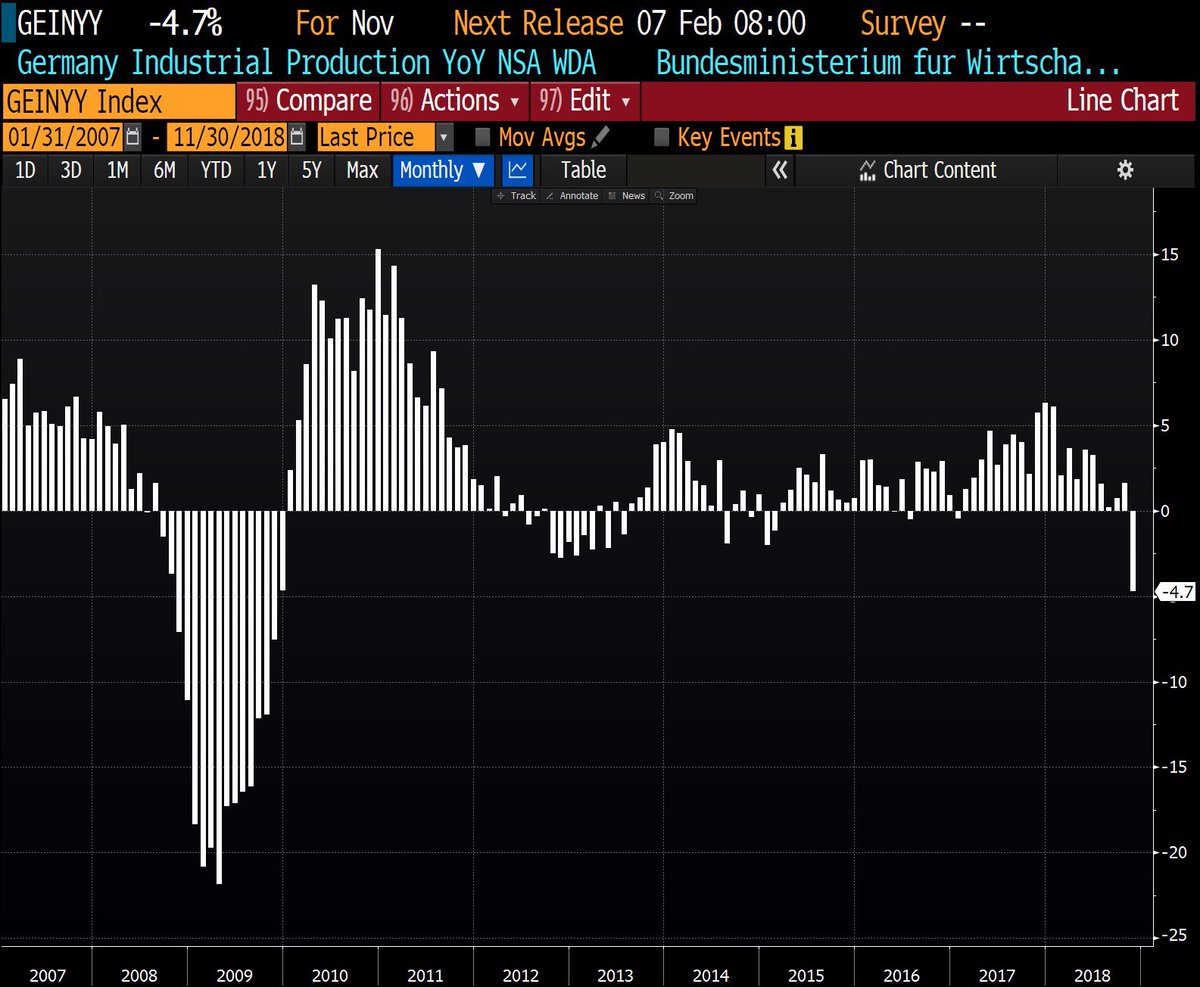

Germany industrial production fell by a whopping 4.7% YoY in December, the biggest decline since December 2009!

More

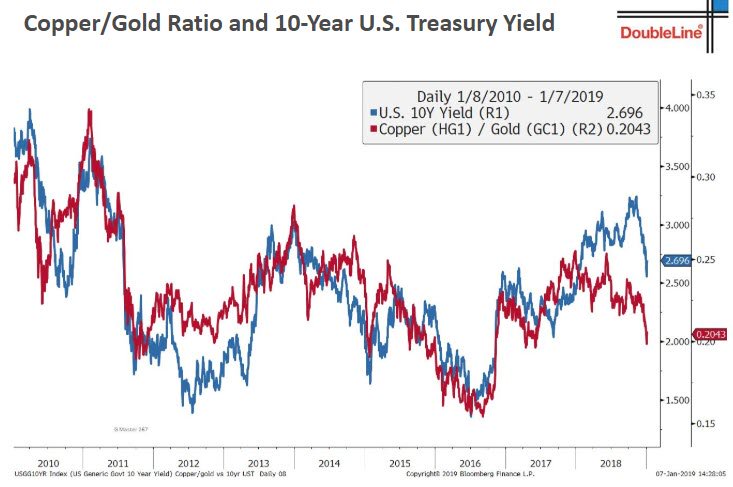

Jeff Gundlach: The Treasury vs copper/gold ratio suggests that 10Y yields are going much lower…… I agree

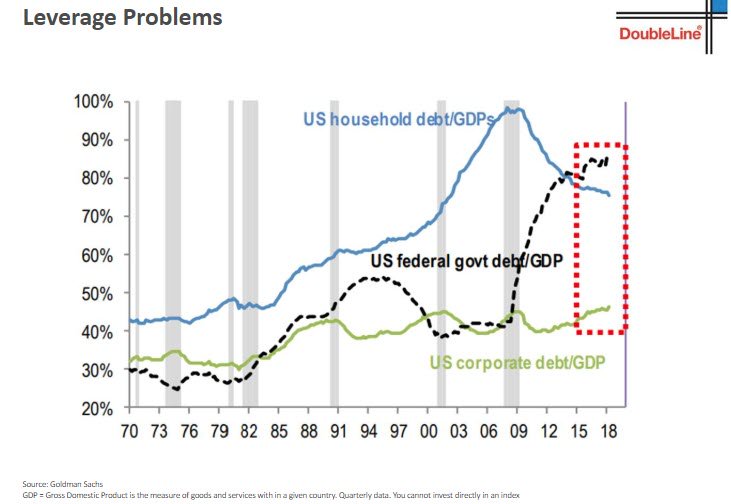

Household are leveraged. Govt spending is what is supporting the economy and Corporate sector does not want to take any more debt ( except for buybacks)

This is a completely horrific situation” – Gundlach

JP Morgan says recent sell-off in global markets has a striking similarity to the one in late 2015, which may offer a glimmer of hope for 2019. In 2016 recession didn’t materialise. What stopped the rot were Fed, USD & China stimulus; all these could be inflecting again.

Goldman cut a swathe of global 10-Year yield calls, says we have seen the cycle top for U.S. 10-Year Treasury yields

Indiacharts writes….We are a world under pressure. It is brewing below, the Nifty cannot see it, and bank nifty thinks banks will make money even if there is a slowdown in consumption. But global growth has given in and the pressure is not going away any time soon.

Few are watching the French revolution and it is a surprise as Italy should have been the one on the streets. But social mood develops in crowds and it takes one leader to identify that trend. The roots may lie in the poor French economic data

A few days ago then CMIE released a follow up to its June data that again shows slowing projects growth just when the street is talking about a Capex revival. I am not sure if the two are linked as the Capex talk also comes on the back of capacity utilisation levels. But for now we have this

and simultaneously we have no new project announcements. With elections around the corner I do not think we will see a change in these trends very fast as the government plays a role on this front.

On the other hand this chart from Hedgeye.com goes on to explain why the recent wage growth data is ominous. I showed the wage inflation chart in the Long Short report and the first thought that comes to mind is Stagflation. But there is a more important point to that. the wage inflation itself can become cause for an earnings contraction if you look at the impact on margins here during late-cycle.

All of that then feeds into earnings expectations eventually. This time around it started from countries other than the US but is now getting built into expectations, source twitter posts.

We are rejoicing in the headlines that tell us that our growth is bigger than the rest in % terms. Furthermore the troubles in Europe recently led to the Market Cap of Germany falling below the Market Cap of India. Unusual for a country that hardly would stand a chance to compete against German exports because of both pricing and technology. Germany commands a premium for a lot of its equipment for that reason. It is not on a price war based on labor arbitrage, like India.

But the business cycle today has created an unusual difference that does not even mean that our per capital incomes are comparable. But in a world where capital must find the cleanest shirt to hide in, the result is a record valuation premium.

But how long does it take a white shirt to get stained especially if you are playing in the same arena. The dirt will fly and you cannot escape it forever. As we are about to find out. Several Research houses are cutting back forecasts for the Dec-2018 quarter on earnings but still maintaining 25%+ growth for FY2020. This after doing so repeatedly for 3 years in a row. Now it is banking a lot on base effects and sure that is just math, but is it reason enough? [chart as reported in ET]

One data point that just came in last week is the Debt to GDP ratio after adjusting for latest NBFC data in the RBI report released a week ago. I peg it at 161% of GDP govt+Bank+NBFC debt combined for FY2018. The surprise number however is going to be for NBFCs in FY2019, as the first half into SEP shows almost 100% growth in new loans and advances. In % terms NBFC credit to GDP is now a sizeable 20% this year. Yes that is where the economic growth for this year came from then. After all in a credit based economy credit=growth.