I got the call on Macro investing right coming out of covid fall because I had faith in our central bankers ability to liquify the banking system and hammer the credit spreads lower. Here we are ,with everybody and their dog chasing a rally in almost all assets except US dollar and US treasuries.

I found below article , referencing Albert Edwards interesting on what can go wrong and I am also leaning in the same direction. Unlike Albert I don’t have a crystal ball of what will go wrong but I always invest based on “Connecting the dots” and it seems some of the dots are not making any sense to me anymore.

Albert Edwards: The 10-Year Yield is Heading to Zero

by Robert Huebscher, 12/16/20

Investors should brace for a deflationary shock that will drive 10-year Treasury yields to zero or below, according to Albert Edwards.

{kind=link}

Edwards is the global strategist for Société Générale and is based in London. He publishes a weekly strategy report, upon which this article is based.

Edwards is known for his “ice age” thesis, which posited that, beginning in 1996, the correlation between bond and stock yields would break down, and 10-year bonds would outperform stocks. His template was Japan and its “lost decade” of growth, which began in 1990. That forecast has been largely accurate, although it was disrupted temporarily by quantitative easing (QE).

He is optimistic that global economies are going through the last act in the ice age. One final bust will take place over the next three to six months before we transition to what he calls the “great melt.”

Deflation and a drop in real yields will accompany that final bust.

Economic growth has stalled despite a fiscal stimulus of about 3.5% of U.S. GDP. There is substantial unemployment, and the impact of the pandemic is crushing economic activity – through lockdowns and changed consumer behavior. That is the underlying cause of the short-term deflationary hit facing the U.S. Outside the U.S., core inflation measures have already collapsed.

In the U.S., core CPI is 1.6%. Some analysts say it may pick up, but Edwards disagrees. The signs of inflation, such as a spike in used car prices, are anomalies. Beneath the surface, the U.S. is behaving similarly to Europe and Japan.

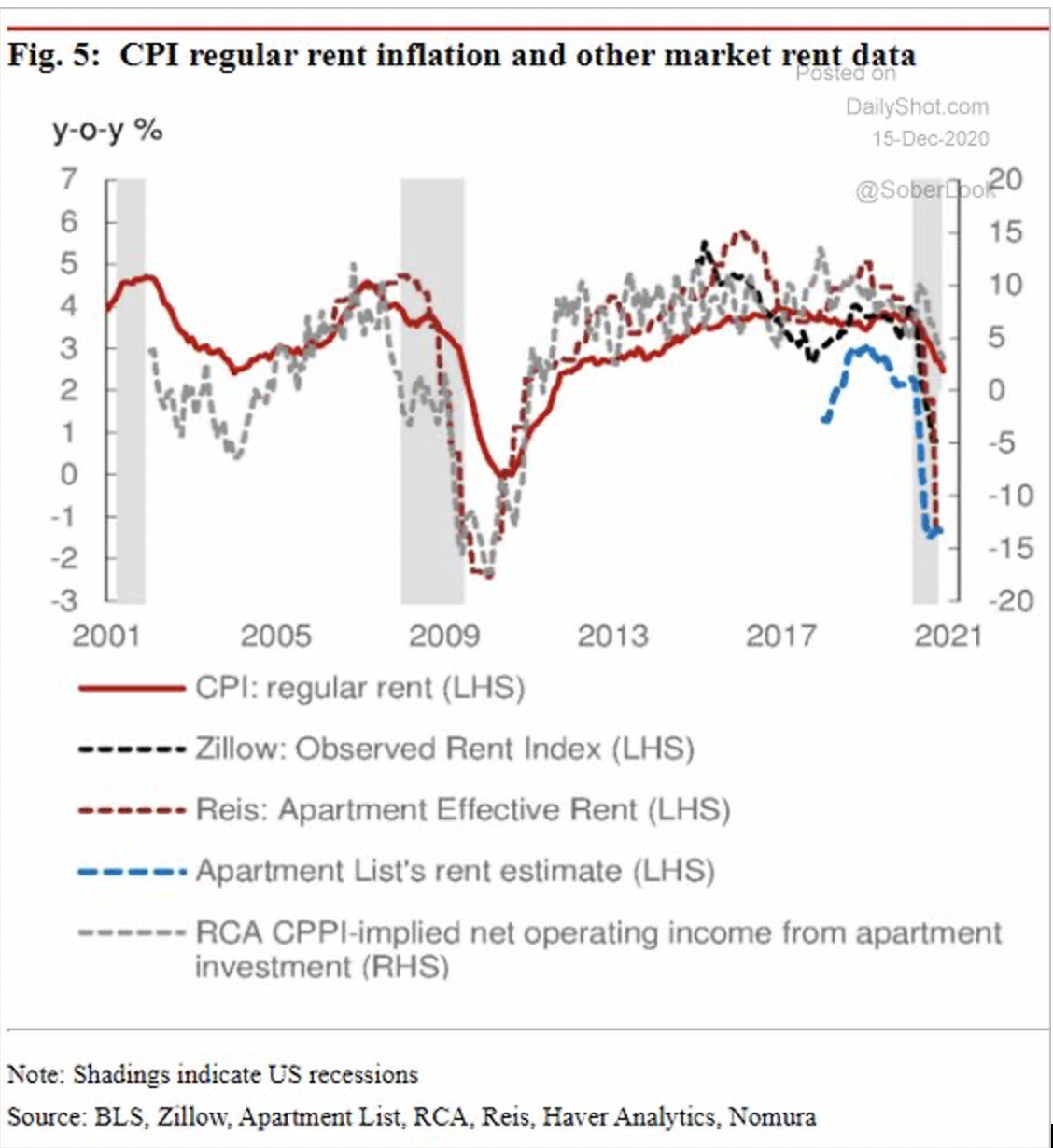

He posted the chart below on Twitter, which came from Nomura. Falling rent prices take a long way to filter through to the CPI, in part because data is sampled only once every six months. But rent is a major component of core CPI, representing nearly 40%, and it has dropped precipitously.

He predicts that U.S. core CPI will go to zero, once the fall in rent prices is reflected in CPI data.

Markets are looking ahead to the success of the vaccines and to 2022 and beyond, according to Edwards. Equity prices and the steepening of the yield curve reflect that outlook. If growth over the next few months falters, though, and core CPI and PCE goes to zero, will the markets look through that?

He doubts that the market will be that sanguine.

A faltering economy and a decline in core inflation, consistent with what has happened in Japan and Europe, will lead to an obliteration of what he calls the “cyclical rotation trade.” That is the trade based on the outperformance of value over growth during the last month or so, following a decade of dominance by growth.

That reversal will be accelerated by the extreme level of optimism shared by market participants, which is shown in a number of indicators: flows to equity funds, bull/bear sentiment and put/call ratio.

The recovery of value was very much tied to an increase in implied inflation expectations, as measured in the U.S. bond market. This is an artificial rise, though. The Fed’s QE, especially during April and May, was skewed toward TIPS to drive inflation expectations upwards, and that effect has persisted, according to Edwards.

This could also be time for a healthy equity correction, according to Edwards.

Key aspects of the Ice Age are deflation, secular stagnation and the excess of investment over savings, and are coupled with falling equity prices and the outperformance of growth over value.

The problem with a deflationary shock is that it also lowers reported economic growth – it “gaps down” – as does corporate revenue growth. That will be especially harmful to companies with excessive debt loads.

Edwards acknowledged that he missed the effect of the pandemic on tech stocks, which have led stock market performance for most of this year.

But he disagrees with Yale economist Robert Shiller and Martin Wolf, who writes for the Financial Times, who say that equity valuations and the elevated CAPE ratio are justified by low real yields. As bond yields come down, P/Es initially increase, he writes. But once yields go below 3% and move toward zero, P/E ratios contract. That is true outside the U.S., especially in Europe, but it is not true in the U.S. because of the FAANG “bubble,” according to Edwards.

If the U.S. faces an economic downturn or another recession, tech earnings, which were pulled forward by the pandemic, will fall sharply while yields are falling. This could be the catalyst that triggers a market correction, according to Edwards.

Longer term, he thinks there will be greater monetary and fiscal cooperation, and the U.S. will embrace modern monetary theory (MMT) and the monetization of its debt. This is the great melt. One sign of this, which has already happened in the U.K., is that governments are directing commercial banks to lend with government guaranteed loans. Those loans are off the government’s balance sheet – that is, until they fail. It means that governments can create money without relying on the central bank, which is important in the Eurozone.

Budget deficits will persist, according to Edwards. There will be no fiscal tightening, but there will be financial repression, and it will benefit cyclicality and value stocks. But that won’t kick in now. In the near term, the U.S. economy will suffer, especially zombie companies with outsized debt loads.

In the next three to six months, when the final wave of deflation comes – as it has in Europe and Japan – the resurgence of value will reverse and growth will be back in favor, according to Edwards.

Once the great melt is underway, the public will insist that policymakers continue MMT and similar monetization policies. Historically, when money supply growth outpaces economic growth, inflation happens. Inflation could happen next year, according to Edwards. He agrees with descriptive aspects of MMT but fears the political forces that will force it to continue indefinitely.