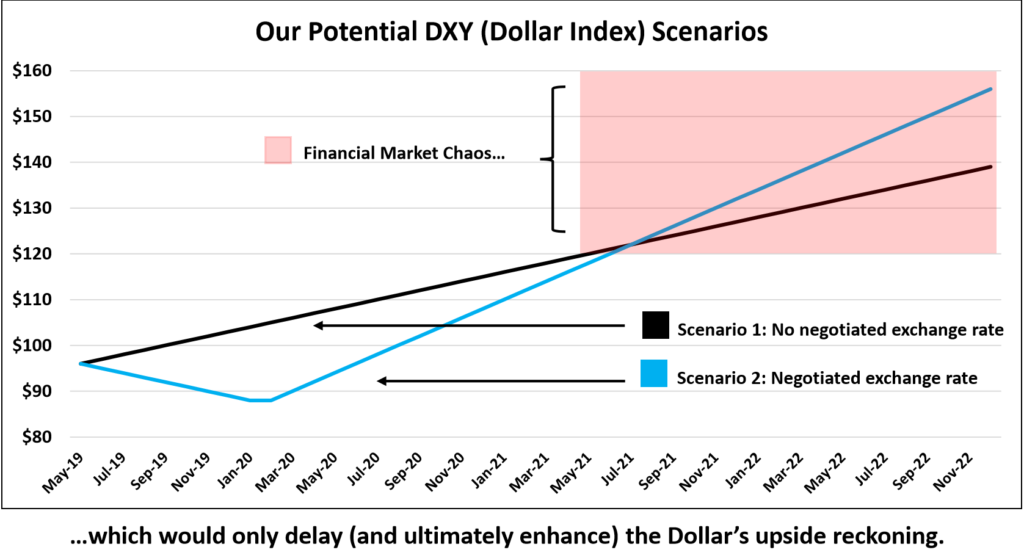

Two path for Dollar as per santiago Capital. I agree with the blue line

The Blackstone GSO credit fund is loaded with lower quality (B rated) leveraged loans. It’s interesting with stocks ripping to new highs, B rated loans are under meaningful selling pressure as downgrades mount. If credit is weakening at this pace with a U.S. economy near full employment, what will happen when stresses mount?

“ESG stands for “Environmental, Social and Governance.” I can certainly understand why some individuals or groups may object to investing in various industries. It’s their capital and they can choose to allocate it as they see fit. When they are sizable clients, they can force portfolio managers to divest certain businesses and not make new investments in certain sectors. This all seems logical—the client is always right. However, at this point, ESG has been taken to such an extreme that it is bordering on silly.

Keep in mind that the vast majority of portfolio managers under-perform their benchmarks and only attract fund flows through their marketing departments. Why miss out on fee-earning capital because you haven’t adapted an ESG mandate? Coal? Nope. Oil and gas? Won’t touch it. Tobacco? Bad. Those are obvious, but where will they draw the line? Why not ban soda? That’s just diabetes in a can. Is social media next? What about entertainment—that’s sure to offend someone. What if you don’t agree with a country’s politics? Do you write off whole continents? Clearly, there’s a problem here. You could end up with large portions of the global economy on the no-go list. Once again, I respect an individual’s decision to forgo a particular investment for ideological reasons, but as a consequence, whole sectors of the economy are now cut off from capital.”

“The raid on Deutsche Bank in Germany back in September over the money laundering probe of Danske Bank, which is the biggest lender in Denmark, contributed to the sudden collapse in confidence. The governments are desperate for money and they are hunting it on a global scale. Deutsche Bank served as a correspondent bank to Danske’s Estonia branch. That is where the latest money laundering is alleged to have occurred. The banker there in the Estonia branch of Danske, Aivar Rehe, was found dead by police there in Estonia. He had been previously questioned by prosecutors and was considered to be THE key witness in the money laundering probe. As always, just like Jeffrey Epstein, his death was declared to be a suicide. This is standard whenever they need to cover something up. Boris Berezovsky suddenly commits suicide being very remorseful for making billions I suppose. Anyone who could expose things others do not want always seems to commit suicide.”

The crisis in liquidity is that American bankers will NOT lend to Europe. Because of the European Banking Crisis, banks just do not trust banks. Nobody knows who will be standing after a failure at Deutsche Bank. The Fed has had to step in to be the neutral lender NOT because of a crisis in the USA, but because of the collapse in confidence in Europe’s banking system as a whole. Stay alert – this is just getting started.

This isn’t meant to be a history lesson on Hong Kong, so let’s make it as short as possible.

Hong Kong was an illegitimate child of the British Empire, and as their grip on global dominance ebbed, old Maggie “Iron Lady” Thatcher saw what was inevitable (losing the territory) and began speeding up preparations so as to ensure a more peaceful transition.

Hong Kongers then had no say as to who their parent would be, and today, 22 years after the official handover, they’ve no say either.

Sure, like a child that’s grown up a bit and felt the lure of independence they want it to be the case, but this is never going to happen, and here’s why.

What you have is an autonomous state that enjoys the some of the widest forms of self expression and democracy in the world sitting on the lap of one of the world’s most totalitarian regimes in existence.

The Chinese call it “one Nation, two systems.” I call it bonkers.

Old Maggie was a sharp cookie, and one of the most adept negotiators our tea drinking, sun starved friends have ever managed to birth (incidentally, the Brits could well do with that right now, because let’s face, it Boris ain’t half a Maggie).

Anyhow, Maggie knew that they had to let Hong Kong go. It was an expiring option, and with China was growing stronger each year while Britain was sinking, she knew the option still had value to them. But with each passing year the cost of the option began to outweigh the benefits.

It had to go… and so it did.

But when the old Iron bird negotiated the transfer of Hong Kong back to Mainland China she put a spanner into the spokes, namely a 50-year treaty essentially saying, “Here, it’s yours, but for half a century you can’t really touch it.”

The problem with this agreement is that no agreement is worth a jelly donut if it can’t be enforced. Look around you and tell me who’s going to enforce the democracy of Hong Kong?

The Brits can’t. They’re balls deep in the real life comedy that is Brexit, and to be fair, there’s enough knife crime on London’s streets now that Hong Kong looks positively peaceful. So no, that dog won’t hunt.

What about NATO? Pffft! I said once, actually twice before that NATO is coming to and end.

That leaves just one: America.

If America intervenes with military, then we’re screwed. Really screwed. If they don’t, well… Hong Kong is screwed.

John Greenwood chief economist for Invesco’s view is that, broadly, we are at mid-cycle, not late cycle. He argues in an interview with macrovoices, I know the cycle has been going on for ten years almost. In fact, in June will be the 10th anniversary of the trough of the last business cycle. So we’ve been expanding for 10 years. And in July this current business cycle expansion will become the longest in recorded US financial history. But, nevertheless, I believe that it has several years to run. And, basically, I think there are three reasons for that.

First, money growth has been low and stable.

Second, private sector leverage in the US remains low, despite some concerns about the nonfinancial corporate sector.

And, thirdly, inflation is not a threat, nor do we face a major financial accident. Those are the two main causes why previous business cycles have come to a premature end.

In my view, if we take a historical analogy, we’re at something like 1995 in the cycle that went from 1991 to 2001, which was the previous longest expansion cycle. So I think we have several years to go because the central bank, the Fed, doesn’t have to take any drastic action at this point. And I don’t believe that there are serious problems in the private sector that will cause a premature end to the expansion.

•The U.S. economy: mid to later stages of the business cycle

•Projected U.S. stock returns over the next ten years: 4.0%–6.0% range

•Projected international stock returns over the next ten years: 7.5%–9.5% range

Recession watch

Key takeaway: 35% chance of a recession over the next 12 months

The yield curve (as traditionally defined by the 3-month and 10-year U.S. Treasury) briefly inverted in late March.

A key distinction about this inversion compared with others is, it’s driven almost exclusively by long-term rates dropping below short-term rates.

We see little evidence that the inversion, in isolation, is signaling a recession in 2019/early 2020.

The expected easing of global growth in the next two years—driven by a fading boost from U.S. fiscal stimulus and the continued slowing of growth in China—is fraught with economic and market risks.

Traditionally when yield curve inverts before recession, short-term real rates are significantly higher

The unemployment rate among those who had completed graduation or higher education (graduate+) has been rising steadily since mid-2017. During September-December 2018, the unemployment rate among these had reached 13.2 per cent. A year ago, the unemployment rate in this group was 12.1 per cent.

Graduate+ face the highest unemployment rate among groups of individuals organised by the level of education achieved. It is usually twice the average unemployment rate for the entire labour force. It is worse for graduate+ women.

Wolf Richter writes….The next recession, when it finally occurs, may be a different animal altogether.

On Tuesday at the close of the market, the yield curve sagged further in the middle like a limp noodle, with these characteristics:

At the short end, the 1-month yield rose to 2.46%, near the top of its recent range, and near the upper end of the Fed’s target range for the federal funds rate (2.5%).

In the middle, the 3-year and 5-year yields both dipped to 2.18%, respectively the lowest since Jan. 2018 and Dec. 2017

At the long end, the 10-year yield dipped to 2.41%, lowest since Dec 29, 2017, below the 1-year yield and shorter maturities; but it remained above the sag in the middle, including the 2-year yield, which also dropped.

At the far end, the 30-year yield dipped to 2.86%, the lowest since Jan 2018, but remained above all the rest.

This produces a beautiful middle-age sag, so to speak, that started forming late last year and has been deepening in recent weeks. The chart below shows the yield curves on six dates. Each line represents the yields on that date, from the 1-month yield on the left to the 30-year yield on the right. The steeply ascending green line represents the yields on December 14, 2016, when the Fed got serious about rate hikes. The deeply sagging red line represents the yields on Tuesday, March 26:

Yields on top-rated German companies like Allianz now negative out to 4yrs. No top-rated borrower will pay a bank positive interest rate on loan when it can borrow the cash it needs from capital markets and get paid for taking money. (Holger via HFE)

Bid-to-Cover On Treasuries Is Falling… Despite U-turn in monetary policy relatively strong dollar and falling bond yields. … And some still believe governments can issue all the debt they want without risk. Daniel Lacalle

The other side of the story which patriotic Indians don’t want to hear. Nytimes writes “It was an inauspicious moment for a military the United States is banking on to help keep an expanding China in check. An Indian Air Force pilot found himself in a dogfight last week with a warplane from the Pakistani Air Force, and ended up a prisoner behind enemy lines for a brief time.The pilot made it home in one piece, however bruised and shaken, but the plane, an aging Soviet-era MiG-21, was less lucky.”