By Doug Noland

I’ve been dreading this. In the midst of all the policy responses to the collapse of the mortgage finance Bubble, I recall writing something to the effect: “I understand we can’t allow the system to collapse, but please don’t inflate another Bubble.” It was obvious early on that policymakers had every intention to reflate Bubbles.

There was a failure to grasp the most critical lessons from that terrible boom and bust episode: Aggressive monetary stimulus foments market distortions, while promoting risk-taking, leveraged speculation and latent risk intermediation dysfunction. Years of deranged finance ensured unprecedented economic imbalances and deep structural impairment. There was no predicting a global pandemic. Yet today’s acute financial and economic fragility – and the risk of financial collapse – are directly traceable to years of negligent monetary management.

I have to adjust my message for today’s post-Bubble backdrop: I understand we can’t allow the system to collapse, but Please Don’t Completely Destroy the Soundness of Central Bank Credit and Government Debt. Does anyone realize what’s at stake?

I don’t see another Bubble on the horizon. Each reflationary Bubble must be greater in scope than the last. Mortgage finance was used for post-“tech” Bubble reflation. Policymakers unleashed the “global government finance Bubble” during post-mortgage finance Bubble reflation. Massive international inflation of central bank Credit and sovereign debt went to the heart of global finance – the very foundation of “money” and Credit.

There is no greater Bubble waiting in the wings to reflate the collapsing one. We are instead left with desperate measures to expand central bank “money” and government borrowings that will surely appear absolutely reckless in hindsight.

Let’s touch upon prospects for Bubble reflation. There was an abundance of positive spin coming out of the previous bust period. “If only the Fed hadn’t incompetently failed to bail out Lehman, crisis could have – should have – been avoided.” Reckless home lending caused the crisis, and regulators will never tolerate a replay. Prudent “macro-prudential” policies and an abundantly capitalized banking sector ensure stability. From the crisis experience, central bankers learned to move early and aggressively to nip market instability in the bud.

The previous crisis was labeled “the 100-year flood.” Onward and upward, with enlightened central banking both leading the way and ensuring a smooth ride.

With assurances of central bank liquidity and market backstops, an unprecedented Bubble inflated throughout global leveraged speculation. Popular “carry trades,” foreign-exchange “swaps,” myriad derivatives (incorporating leverage) and such morphed during this cycle into a colossal self-reinforcing Credit Bubble. The resulting liquidity became a prominent fuel source for asset and economic Bubbles, reminiscent of the late-twenties.

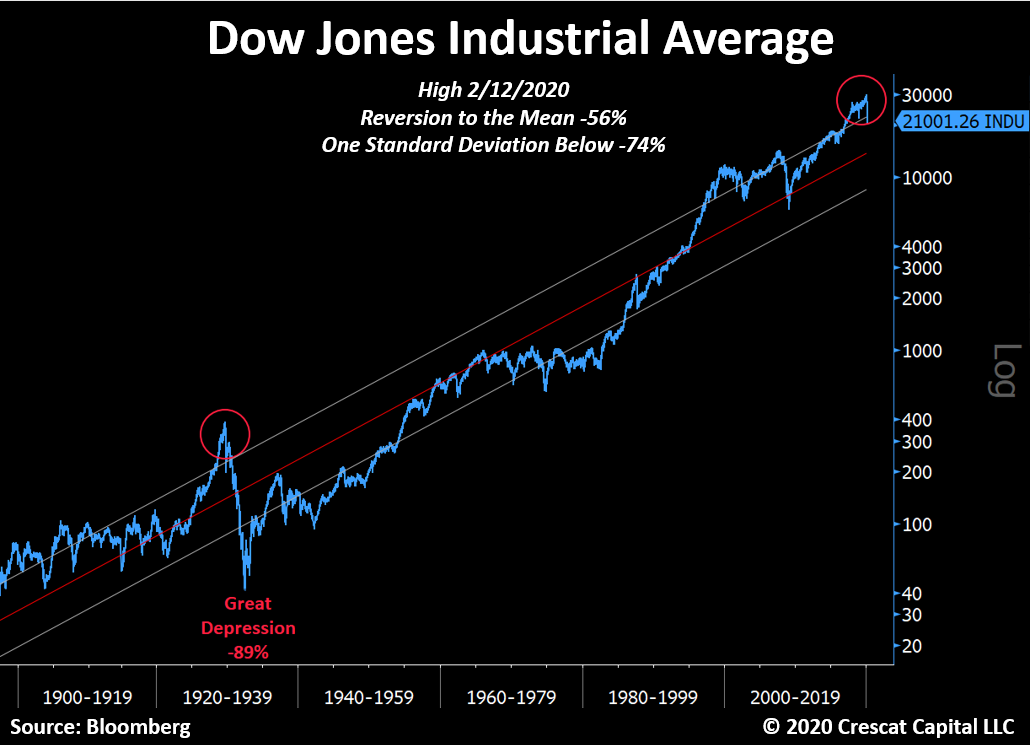

Can’t a massive expansion of central bank Credit (securities purchases, lending facilities, swap lines, etc.) now reflate the Bubble? I seriously doubt it. Risks associated with various strategies have been revealed. Leverage in its many forms has been, once again, shown to be a serious problem. Rather than the proverbial “100-year flood,” for the second time in less than 12 years the world is facing the worst financial crisis since the Great Depression. Burn me once, shame on you. Fool me twice…

It’s not hyperbole today to use “depression” to describe the unfolding deep global economic downturn. Coronavirus uncertainty makes it impossible to forecast the length and severity of the economic collapse. In the best case, the rapidly expanding outbreak in Europe and the U.S. subsides over the coming weeks. Even so, economies around the world will take huge hits. And prospects for the coronavirus to reemerge next winter (and emerge more powerfully during the southern hemisphere’s approaching winter season) will keep risk-taking well-contained for many months to come.

Coming out of the previous crisis, the global economy had the benefit of a powerful “locomotive” of accelerating expansions in China and the emerging markets more generally. Importantly, post-Bubble reflationary measures came as those fledgling Bubbles were attaining powerful momentum. Beijing pushed through an unprecedented $600 billion stimulus package, while aggressive monetary policy stoked EM booms generally. Keep in mind that total Chinese banking system assets inflated from about $7 TN to $40 TN since the crisis.

Looking ahead, the global economy is without “locomotives.” It evolved into one massive global financial Bubble financing a precarious synchronized global economic expansion. And I believe speculative finance became a prevailing source of Global Bubble Finance.

Here’s where I could be wrong. I seriously doubt this Bubble is revivable. The unwind will likely unfold over weeks and months. Extraordinary central bank measures will spur rallies and hopes for recovery. At times, it will appear that liquidity is returning. Yet the Bubble will not be reflated.

Confidence has been shattered. Faith that central banks have everything well under control has been broken. Myriad fallacies have been exposed. Central banks can’t guarantee liquid markets, especially in a Bubble-induced highly levered speculative environment. The entire derivatives universe has been operating on the specious assumption of liquid and continuous markets. History is unambiguous: markets experience bouts of illiquidity, dislocation and panicked crashes. The fantasy that contemporary central bank monetary management abrogates illiquidity and market discontinuity risks is being debunked. The mania in finance has, finally, run its course.

Leverage has to come down – and I believe it will stay down for years to come. A month ago risk could be disregarded – had to be disregarded. Market, financial, economic, social and geopolitical risks matter tremendously now, and they will matter going forward. In the best-case scenario, the coronavirus peaks over the coming weeks. I don’t want to ponder the worst-case.

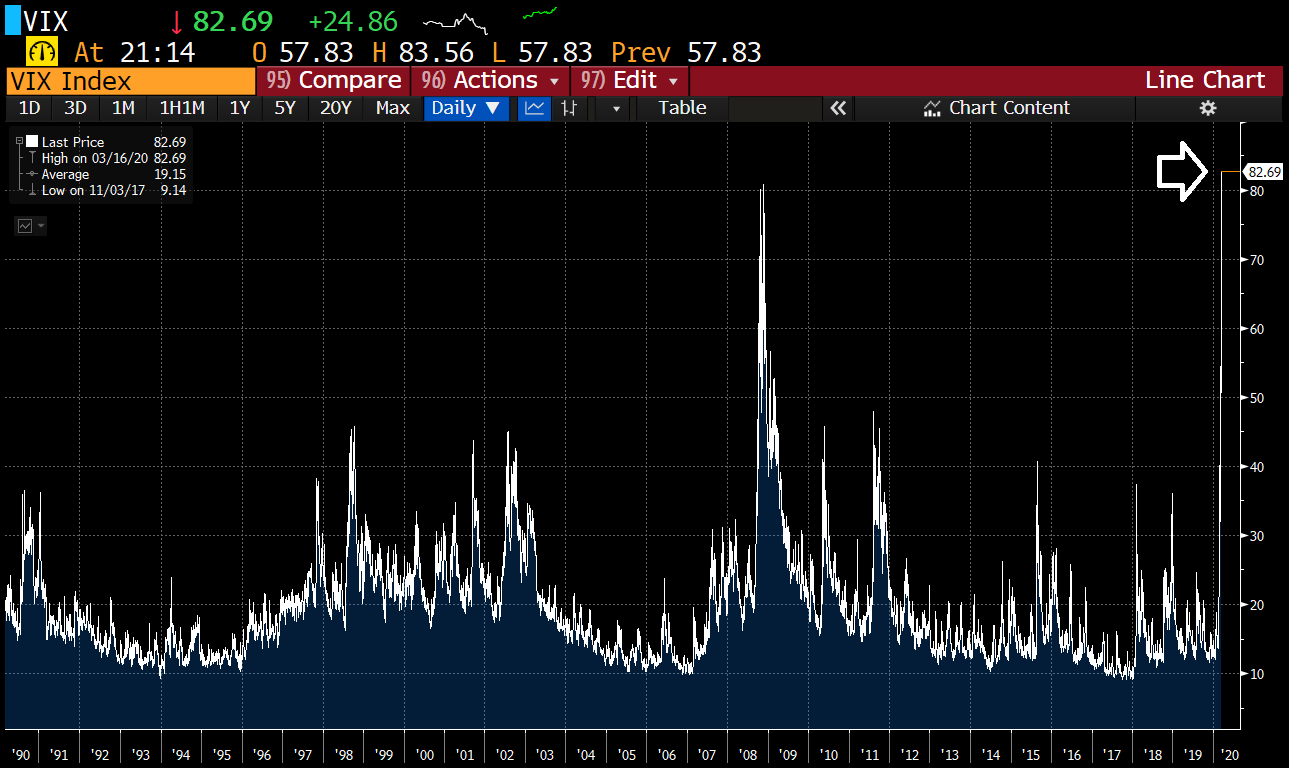

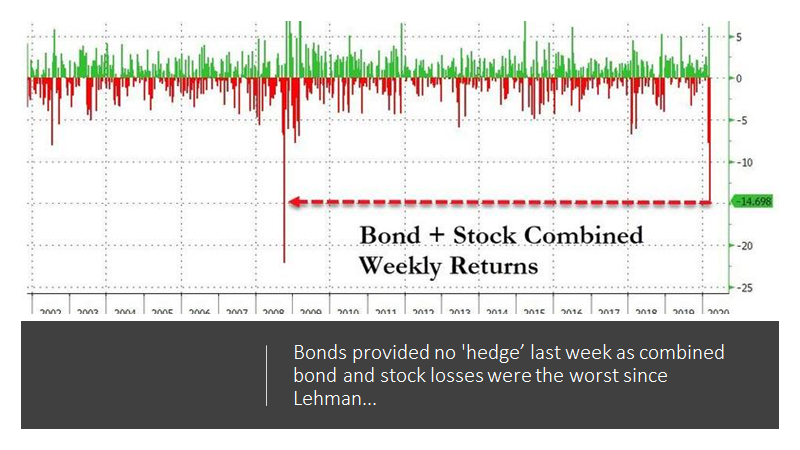

A Friday-evening Zerohedge headline says it all: “Stocks Suffer Worst Week Since Lehman Despite Biggest Fed Bailout Ever.” In last week’s CBB, I wrote that we “saw more than a glimpse of what the beginning of financial collapse looks like”. This week’s sequel was how global financial collapse gains momentum – especially Wednesday. I watched the ’87 stock market crash on a Quotron machine. I’ve witnessed scores of bursting Bubbles and collapses – including bonds in ’94, Mexico ’95, SE Asia ‘97, Russia/LTCM in ’98, “tech” in 2000, 9/11, the spectacular 2008 collapse and 2012’s near melt-down. None of those previous crises were as alarming as current market dynamics.

The dollar index surged 4.1% this week, in a perilous market dislocation. The Mexican peso sank 10.2%, and the Russian ruble fell 9.2%. The South African rand dropped 7.6%, the Czech koruna 7.5%, the Indonesian rupiah 7.4%, the Hungarian forint 7.0% and the Brazilian real 4.5%. Massive “carry trade” losses (i.e. borrow in dollars to lever in higher-yielding EM bonds) were compounded by collapsing EM bond prices (surging yields). Even with Friday’s bond rally (yield decline), yields this week surged 96 bps in Peru, 82 bps in South Africa, 70 bps in Turkey, 44 bps in Indonesia, and 39 bps in Thailand.

Ominously, the rout was even more pronounced in dollar-denominated EM bonds. This market rallied sharply Friday after the announcement of enhanced central bank swap facilities. Mexican yields sank 44 bps Friday but were still up 72 bps for the week. Brazilian yields surged 68 bps this week, even after Friday’s 34 bps decline. For the week, dollar-denominated yields were up 152 bps in Ukraine, 131 bps in Qatar, 97 bps in Chile, 92 bps in Philippines, 92 bps in Turkey, and 74 bps in Indonesia. This type of dislocation in highly levered markets signals global markets are “seizing up.”

Market dislocation went much beyond the emerging markets. Crude oil’s 29% collapse was behind the Norwegian krone’s stunning 13.9% decline. The Australian dollar fell 6.7%, the Swedish krona 6.6%, the New Zealand dollar 5.9%, the British pound 5.3%, the Canadian dollar 3.9%, the euro 3.8%, the Swiss franc 3.6%, and the Japanese yen 3.0%. Mayhem.

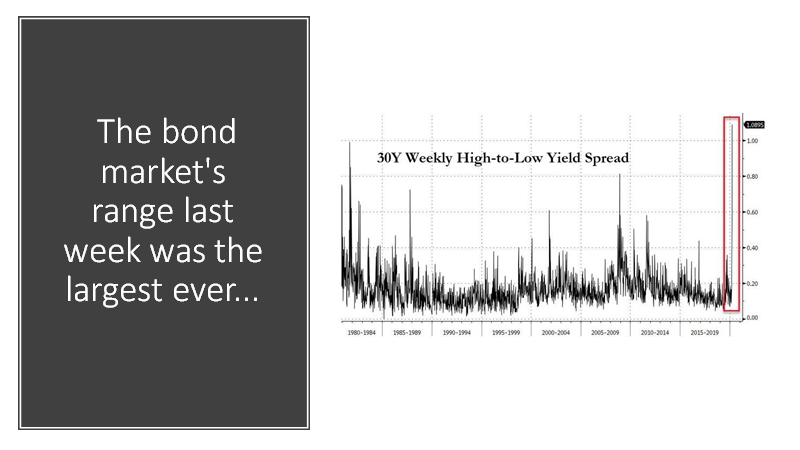

Pointing to acute systemic risk, “developed” nation bond markets also dislocated. After beginning the week at 1.85%, Italian yields spiked to 2.99% in panicked Wednesday trading. Greek yield began the week at 2.10% (up from 0.96% on Feb. 21) and traded as high as 4.09% Wednesday. Portuguese yields were at 0.86% in early-Monday trading before spiking to 1.61% by mid-week. Spanish yields surged from 0.66% to 1.38%. Even German 10-year bund yields rose from Monday’s negative 0.59% to Wednesday’s negative 0.24%.

Wednesday’s meltdown spurred the ECB into emergency action, announcing a new $800 billion QE plan. ECB buying was surely behind the big end-of-week rallies in euro zone periphery bonds.

March 15 – Financial Times (Martin Arnold): “Christine Lagarde has apologised to other members of the European Central Bank’s governing council for her botched communication about its new monetary policy strategy which triggered a bond market sell-off last week. Speaking to the ECB’s top decision-making body in a call on Friday, the central bank’s president said she was sorry for comments that led to the biggest single-day fall in Italian government bonds in a decade… In Thursday’s press conference Ms Lagarde said it was not the ECB’s role to ‘close the spread’ in sovereign debt markets…”

Lagarde’s “gaff” was ridiculed by market pundits, with comparisons to communication blunders early in Powell’s chairmanship. Yet it should never have become the ECB’s role to narrow borrowing spreads, or for the Fed and global central bankers to kowtow and backstop the securities markets. Years of central bank cultivation of risk-taking and leveraged speculation are coming home to roost in the a very bad way.

Evidence of acute financial instability made it to U.S. shores this week. “Short-Term Bond Market Roiled by Panic Selling;” “Government Bonds Buckle as Investors Dump Haven Assets for Cash;” and “How a Little Known Trade Upended the U.S. Treasury Market.” It was the nightmare scenario for highly levered contemporary finance: Illiquidity and rising safe haven yields, rapidly widening Credit spreads, surging CDS prices, de-risking/deleveraging, general market illiquidity and dislocation. The definitive recipe for devastating outcomes. Even more alarming, systemic dislocation unfolded not long after the Fed announced a new $700bn QE program.

March 15 – Wall Street Journal (Nick Timiraos): “The Federal Reserve slashed its benchmark interest rate to near zero Sunday and said it would buy $700 billion in Treasury and mortgage-backed securities in an urgent response to the new coronavirus pandemic. The Fed’s rate-setting committee, which delivered an unprecedented second emergency rate cut in as many weeks, said it would hold rates at the new, low level ‘until it is confident that the economy has weathered recent events and is on track’ to achieve its goals of stable prices and strong employment. ‘We have responded very strongly not just with interest rates but also with liquidity measures today,’ Fed Chairman Jerome Powell said during a press conference Sunday evening…”

As the week unfolded, it was full-fledged financial crisis. It was difficult to keep track of the various emergency measures.

March 17 – Bloomberg (Christopher Condon, Craig Torres, and Matthew Boesler): “The Federal Reserve unleashed two emergency lending programs on Tuesday to help keep credit flowing to the U.S. economy amid strain in financial markets… The central bank is using emergency authorities to establish a Commercial Paper Funding Facility with the approval of the Treasury secretary… The Treasury will provide $10 billion of credit protection from its Exchange Stabilization Fund. Later in the day it announced a Primary Dealer Credit Facility, also with backing from Treasury. The moves follow mounting pressure to act after the Fed’s Sunday evening emergency interest-rate cut to nearly zero and other measures failed to stem market stress as investors reacted to the risk that the virus will tip the U.S. and global economy into a recession.”

March 18 – Reuters (Howard Schneider and Megan Davies): “The U.S. Federal Reserve rolled out its third emergency credit program in two days to battle the fallout from the virus crisis, this one aimed at keeping the $3.8 trillion money market mutual fund industry functioning if investors make rapid withdrawals. The Money Market Mutual Fund Liquidity Facility unveiled on Wednesday will make up to 1-year loans to financial institutions that pledge as collateral high quality assets like U.S. Treasury bonds that they have purchased from money market mutual funds. The Fed is in effect encouraging banks to buy assets from those mutual funds, insulating the funds from having to sell assets at a discount if they come under pressure from households or firms wanting to withdraw money.”

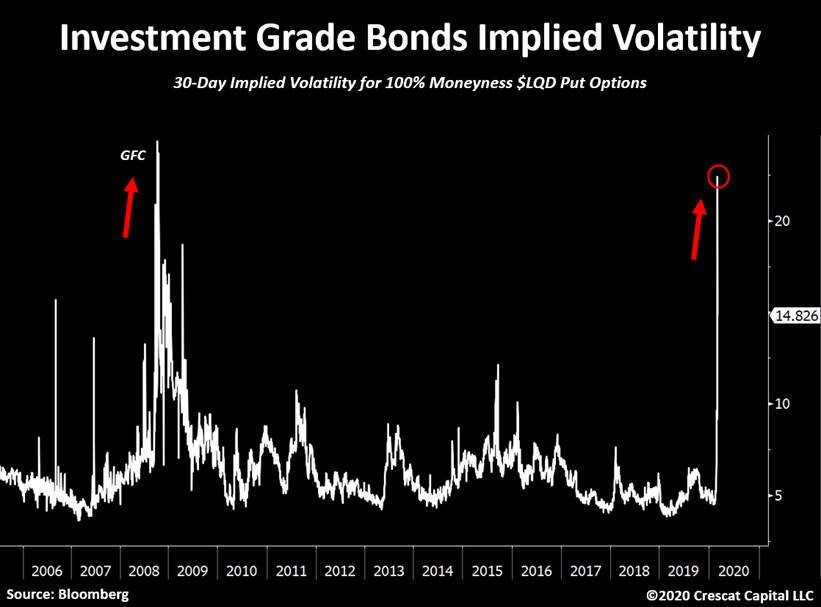

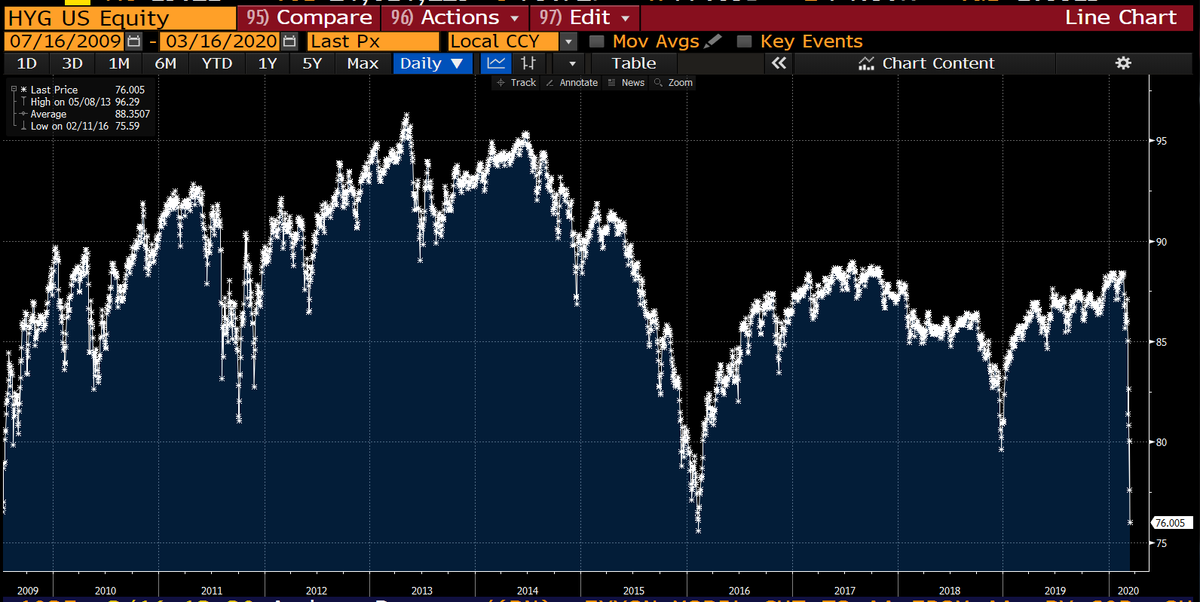

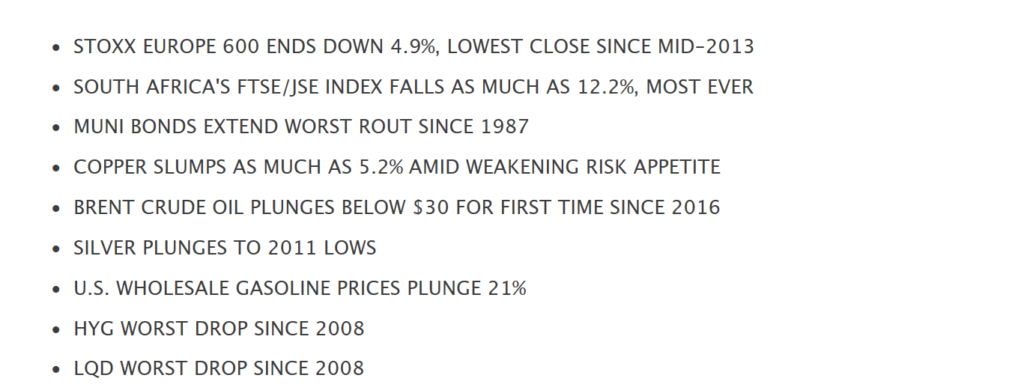

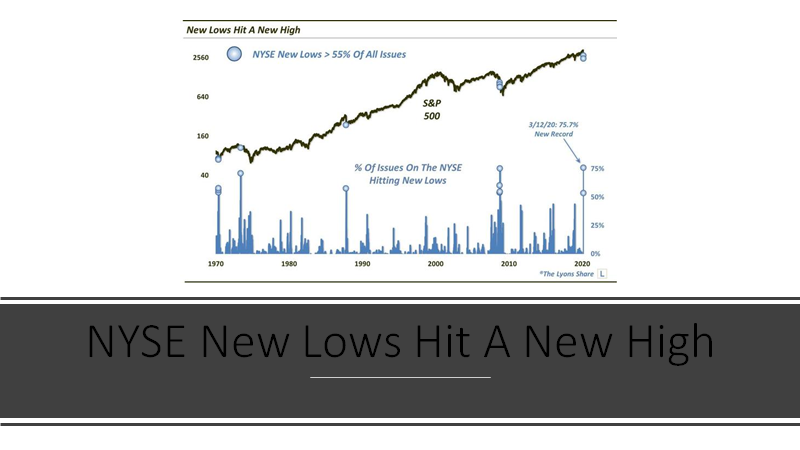

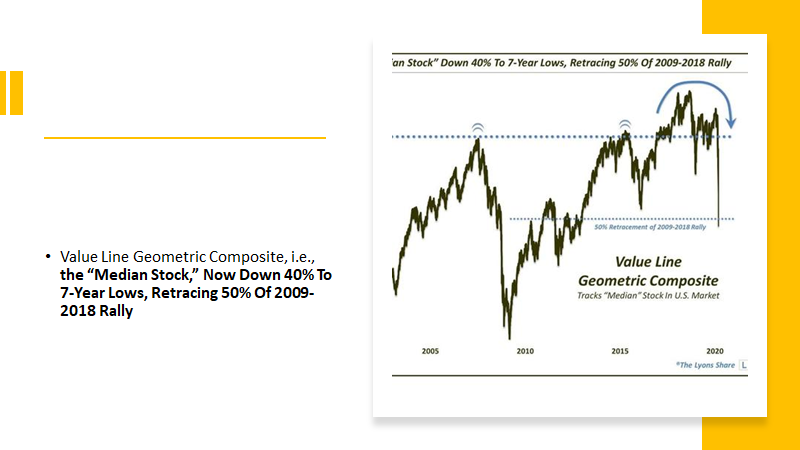

Despite it all, U.S. markets convulsed uncontrollably. U.S. equities were bludgeoned (S&P500 down 15.0% and Nasdaq falling 12.6%). Yet the more alarming developments were within the Credit market. Dislocation was deep and broad-based – Treasuries, investment-grade corporates, high-yield, municipal debt, MBS, commercial paper, CDOs and derivatives. A popular investment-grade corporate ETF (LQD) collapsed 13% in three sessions (Tuesday through Thursday). Perceived safe and liquid (“money-like”) instruments were crushed in a panic (see “Market Instability Watch” below). ETF problems turned acute, as “investors” ran for the exits.

March 19 – Financial Times (Robin Wigglesworth): “When financial markets were rattled across the board last week, some investors and analysts thought they knew where to point the finger. ‘The risk parity kraken has finally been unleashed,’ one tweeted. Risk parity is a strategy pioneered by Bridgewater’s Ray Dalio. His pioneering fund, All Weather, has been hit hard in the recent turmoil, sliding 12% this year. That is quite a fall, for a strategy designed to function well in almost any market environment, by seeking to find a perfect balance of different asset classes such as stocks and bonds. Some analysts say such funds are not just succumbing to the wider turmoil but exacerbating it — especially the freakish sight of both supposedly defensive government bonds and risky equities selling off at the same time. ‘These moves suggest a rapid unwind of leveraged strategies like risk parity,’ said Alberto Gallo, a fund manager at Algebris Investments.”

With Treasuries these days providing minimal upside, losses escalated for myriad levered strategies. The global leveraged speculating community is hemorrhaging. The derivatives complex is in chaos. Goldman Sachs Credit default swap (5-yr CDS) prices surged 66 to 223 bps, the high since the 2012 European crisis. Bank of America CDS jumped 63 to 199 bps; Citigroup 60 to 214 bps; Wells Fargo 59 to 192 bps; Morgan Stanley 57 to 211 bps; and JPMorgan 53 bps to 176 bps. Ominously, the big U.S. financial institutions were at the top of the global bank CDS leaderboard this week.

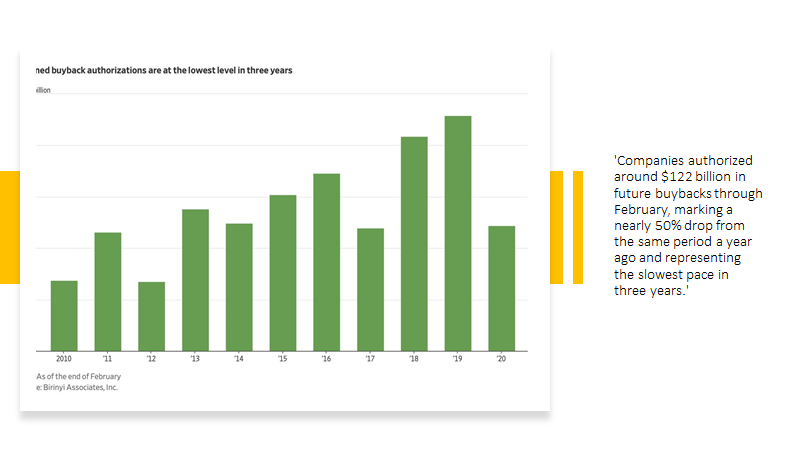

If financial collapse can be avoided, an altered financial world awaits. The old scheme doesn’t work any longer. The era of cheap money financing massive stock buybacks has ended. Leveraged speculation creating self-reinforcing liquidity abundance and asset inflation – over. Buy and hold and disregard risk has been discredited. Blindly plowing savings into perceived safe and liquid ETFs is a thing of the past. In the new financial landscape, can derivatives be trusted? How about the private equity Bubble? The age of endless cheap finance for virtually any borrower and equity issuer (irrespective of cash flow or earnings) has reached its conclusion.

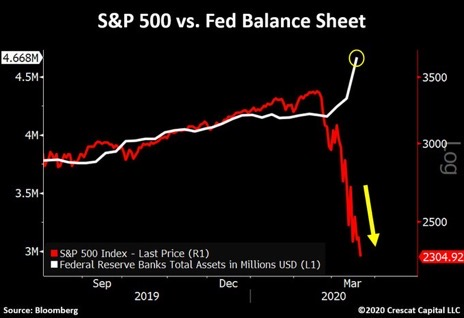

Meanwhile, “helicopter money” has arrived. Seemingly outrageous on Monday, Senator Schumer’s proposal for a $750 billion stimulus package was small potatoes compared to spending plans contemplated by week’s end. Federal Reserve Assets surged $356 billion the past week to a record $4.668 TN. Fed Assets were up $907 billion over the past 28 weeks, as it becomes clear a $10 TN balance sheet will unfold more quickly than I have anticipated.

The inexhaustible inflationists and eager MMT adherents see their opening. “Please Don’t Completely Destroy…” will haunt me – and the world. In a crisis, no one was willing to stand up to Bernanke. Today, “Helicopter Ben” looks fainthearted compared to what today’s central bankers are about to attempt. The experiment has gone terribly wrong, just as foolhardy bouts of inflationism have throughout history.

If they actually believe the massive inflation of central bank and government Credit will reflate markets and economies, they will be grievously disappointed. Government debt and central bank balance sheets have commenced what will be a frightening buildup. The inflationary consequences are today unclear. What is clear is it will be anything but confidence inspiring. The desperate inflation of perceive money-like Credit will not encourage the leverage speculating community to re-leverage. It will not entice burned investors back into perceived money-like ETFs. It will not stabilize currency markets. However, it does risk a bond market debacle.

History’s greatest Bubble is nearing the end of the line. It’s all left to central bank Credit and sovereign debt – the massive inflation of Credit at the very foundation of global finance. This experimental strategy is so fraught with peril that it is difficult to believe that risk will be disregarded – that things can somehow stabilize and return to normal. Confidence in central banks’ capacity to control global markets has been irreversibly damaged – and a long overdue market reassessment of the value of financial instruments has commenced.

Truth is stranger than fiction. The world’s weakened superpower cracks down, initiating a trade war with the aspiring superpower. Relations sour. Then, shortly after a watered-down compromise agreement is signed, a virus outbreak erupts in the aspiring country that leads to a global pandemic and major crisis in the superpower country. The aspiring nation’s dictatorial government, seeking a scapegoat to pacify its shaken populace, blames the superpower for the virus and its collapsing Bubble. The superpower government, in an election year, points blame at the aspiring nation’s government. Two strongmen leaders face off. The American Virus vs. the Chinese Virus, with consequences that are chilling to contemplate.

Two strongmen leaders face off – in the oil market. Why all the strongmen? No coincidence. A decade (or two) of booms and busts and resulting heightened global insecurity has led to this critical juncture. Strongman heads of state, uncontrollable monetary inflation, and epic bursting Bubbles make for a perilous geopolitical backdrop. Covid-19 has let the genie out of the bottle.

http://creditbubblebulletin.blogspot.com/2020/03/weekly-commentary-please-dont.html

{kind=link}