Rick Ackerman writes…. Unfortunately, two predictable things will now happen. China will face a credit crisis and the dollar will likely strengthen. Dangerous times for all of us. it’s not hard to imagine all the new risks that come with turning off the trade taps (if that is the real agenda). We can’t know for certain of course, but Trump is certainly playing from a position of strength. He picked a fight he is going to win. The charts already say the U.S. trade deficit will start falling, so it’s baked in the cake. An added strategic benefit is that Belt & Road [China’s strategy of building infrastructure to facilitate trade growth with Europe, Asia, Latin America, Africa and the Middle East] will be set back a decade or more. We will see if the Chinese are clever enough to see what just happened and start playing ball, or if pride will be their downfall (I think pride will win out). The problem I see is that China can ill afford to monetize all the debt that has been created. We may be about to enter a critical period of Asian corporate bankruptcies.

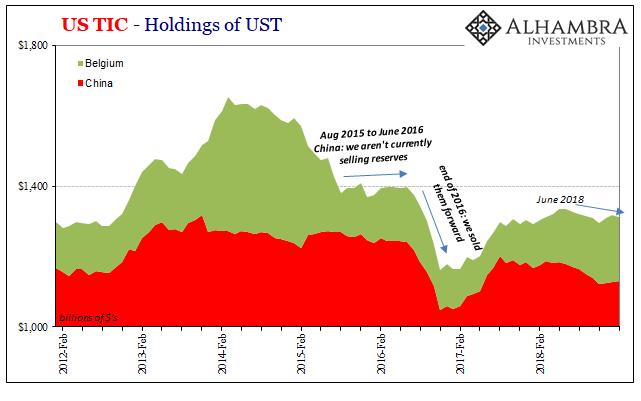

It’s a tell-tale sign of someone who doesn’t know what they are talking about. In the realm of global currency systems, anyone who brings up China’s massive stockpile of US Treasury assets inevitably they assign all the power to the Chinese. Xi could destroy Trump if he wanted, bringing down the US in a righteous fit of trade war anger.

Not only is this totally wrong, it is ignorant of history. Recent history. Toward the end of November 2013, out of nowhere a report appeared in Chinese State media which said officials were reconsidering their foreign reserve allocations.

The Year of the Pig in China is quickly becoming the Year of the Pig Disaster. African Swine Fever (ASF), which has been spreading across Eurasia since the late 2000s, has ravaged the Chinese pork industry after it fi rst appeared in the northeastern city of Shenyang last summer. As of late March, according to INTL FCStone’s in-country sources, some 40% of the pig feeding capacity had been destroyed, and insiders on the ground worry there may be no stopping the disease before it decimates the industry. Although ASF poses no threat to human health, it represents a twofold challenge to the global economy. First, pork is far and away the dominant meat source in China. It makes up 3% of the country’s consumer price index and is the number one driver of food infl ation. As the industry declines, it will have farreaching eff ects on the world’s second-largest economy. Second, China’s preference for pork makes it the world’s largest hog consumer, with a market share of 49%. The country is also the largest importer of soybeans, a primary protein source for hog farming. Consequently, the faltering of the Chinese pork industry will reshape global trade in both meat and feed grains.

On October 8th 2018 The Solid Ground commented upon Vice-President Mike Pence’s October 5th speech on US China relations – Desolation Row: Which Side Are You On? While a bit of sabre rattling ahead of mid-term elections is to be expected, this speech, in the opinion of your analyst, changes the world. It changes not just the world of finance and money but, very probably the world of geopolitics…… In the context of this speech trade sanctions are a lever for change in many areas well beyond the issues of trade themselves. It is incredibly difficult to see how the Chinese Communist Party genuflects, or perhaps kowtows, to such major and wide-ranging criticisms of their behavior. To bend to the will of the US administration on these multiple issues is to back away from the political control that is at the heart of the Chinese Communist Party and Xi’s Presidency. For all of us as citizens this raises the prospects of a much more confrontational relationship between Washington DC and Beijing, and for investors it means a whole new monetary order must now be developed. The development of that new monetary order will be as important for investors as the breakdown of the Bretton-Woods agreement was for their predecessors.

The chart below is the Global manufacturing PMI of major economies over last one year. As most of you know, a reading above 50 is expansion and below 50 is contraction. We are seeing clear signs of weakness in Germany which derives most of its GDP through manufacturing exports. China is hovering around 50 inspite of huge credit creation this year, staring in early February, showing signs of slowdown in global demand and lack of domestic demand. US is by far the strongest and in my view the reason is inventory building to beat tariffs and a relatively stronger manufacturing sector as compared to rest of the world.But I think the best of US Manufacturing PMI is behind us as inventory needs to be drawn down before it can be rebuilt again. This is against the backdrop of less than 4% unemployment in US. India is facing its own election and the recent data from consumer discretionary and Industrial production is not positive.

All these major countries are already getting some helping hand from either monetary or fiscal policy with US running a trillion dollar deficit, Germany getting extreme monetary support from ECB, China throwing fiscal kitchen sink to get some growth and even lending money through MLF facilities to its bank so that it flows into real economy. India is having a compliant central bank governor who is helping on the monetary side and on fiscal side a shortfall in tax collection to the tune of almost USD 15 billion acts like a fiscal stimulus.

Even after all this the Global manufacturing activity refuses to pick up. The reason is, we have reached a point where any addition in debt does not lead to increase in productivity or generation of economic activity. This is when the world economy reaches a tipping point known as secular stagnation.

Martin Armstrong writes “ We are switching from QE to a new reality of budget management. If interest rates rise on government bonds, the budget blows out. At this stage, the Fed is toying with the idea of setting benchmark rates for 2 to 10-year instruments. This will be different than QE. It will be the collapse of government bond markets on a global scale.”

WSJ writes…The new hard line taken by China in trade talks—surprising the White House and threatening to derail negotiations—came after Beijing interpreted recent statements and actions by President Trump as a sign the U.S. was ready to make concessions, said people familiar with the thinking of the Chinese side.

High-level negotiations are scheduled

to resume Thursday in Washington, but the expectations and the stakes have

changed significantly. A week ago, the assumption was that negotiators would be

closing the deal.

Now, they are trying to keep it from collapsing.

Adding to the pressure, the U.S.

formally filed paperwork Wednesday to raise tariffs on $200

billion of Chinese goods to 25% from the current 10% at 12:01 a.m.

Friday. Beijing’s Commerce Ministry responded by threatening to take unspecified

countermeasures. At a campaign rally in Florida Wednesday night, Mr. Trump said

Chinese leaders “broke the deal” in trade talks with the U.S.

Share

Your Thoughts

Is President Trump’s plan to raise tariffs on China worth the economic

pain it may cause U.S. consumers and businesses? Join the conversation below.

In the current negotiations, the U.S. thought China agreed to detail the laws it would change to implement the trade deal under negotiation. Beijing said it had no intention of doing so, triggering Mr. Trump’s threat Sunday to escalate tariffs and bringing the dispute into the open.

Risk

appetite of investors is a major driver of returns that financial markets

provide. Thinking about US, the rate hikes of which big beneficiaries were

Emerging Market Countries, might be taking a toll on US itself with equities

crashing relatively and a weaker USD. For Fed, waiting time is coming to an end

and they have only one way to go, get dovish. If they hike rates further, it

would be a disaster for US as $62T GDP is on the outside and $18T on the

inside.

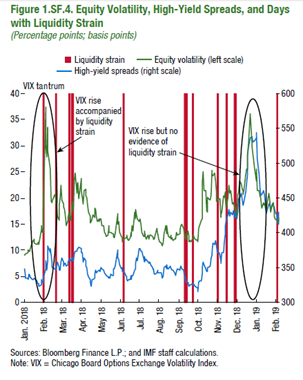

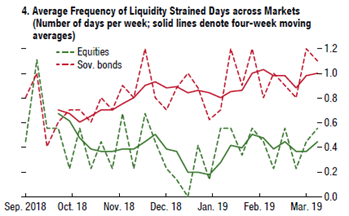

In a liquid

market, an adjustment in prices in response to a news shock would happen

rapidly. However, if the market is not very liquid, the jumps are sluggish. Big

Price movements in bond markets tends to be more reflective of liquidity

strain. Recent events like flash rally in US Treasuries in 2018, Sharp drop of

S&P500 futures in December 2018 or yen spike in January 2019 have raised

concerns about fragility of market liquidity.

‘Global USD liquidity is vulnerable to the downside’, says Nedbank’s Global Macro Insight. In our history, investor sentiments have played a crucial role whenever crisis occurred.

‘All of the

elements of our theory of animal spirits are essential to understanding the

depression of 1890s: a crash of confidence associated with remembered stories

of economic failure, including stories of growth of corruption in years that

preceded the depression; a heightened sense of unfairness of economic policy;

and money illusion in the failure to comprehend the consequences of the drop in

consumer prices’, said Akerlof and Shiller in Animal Spirits.

Alfred

Noyes, a then financial editor of New York Times pointed out, “…the first act of frightened bank depositors

was to withdraw these very legal tenders from their banks. Experience has

taught these depositors that in a general collapse of credit the banks would

probably be the first mark of disaster.”

When Fed was founded in 1913 and subsequently FDIC was the answer to liquidity problems then. In 1998 with LTCM, 2008 Bear Sterns rescue (to name a few), Fed was the banker of last resort to prevent liquidity crisis. The powers of central banks and their actions decide the impact on the economy and investors hope that they always proceed with best interests.

The most recent spike could be attributed to investors readjusting to monetary policy normalization and change in outlook of growth. The effects of structural change in the provision of liquidity is more pronounced in sovereign bond markets than equity or cash segments.

An escalation in US – China trade war or Fed’s no cut stand has left liquidity of in particular, USD vulnerable. Trading volumes has clearly decreased post financial crisis which is a function of investor sentiment ,may not the only factor affecting market liquidity but has always been the key factor which cannot be ignored.

“Recent years there has been a shift in how various assets classes are trading. There is emerging a high degree of positive correlation among various financial asset classes that have many concerned since it is not conforming with the perceived historic norms. Many are reading into this as a warning of what is to come. When different asset classes move in the same direction simultaneously, this obviously eliminates the theory of diversification is asset allocation.

Asset allocation over the years has been the way portfolios are arranged because they lack the ability to forecast the major trends. The belief has been that the possible benefits of diversification across classes reduces risk and offers a management tool knowing that you will lose on one side but win on another class.

When there is a high correlation between classes, these asset allocation models fail. The concerns become that this injects a negative development because they fear if one asset class falls, it will take all of the others with it.

Conclusion

What is being overlooked here is the fact that there is a major shift underway which is not understood and this creates the risk of a LIQUIDITY CONTAGION whereby a loss in one asset class causes liquidation in all others to raise cash to cover the losses in one particular asset class. Welcome to the new age of international contagion which is far more serious and cannot be reduced by simply diversification.”

Some perspective from a prior post on President Trump’s predisposition toward free trade.

We hope for a good trade deal and China caves on everything. We also hope for the end of poverty, world peace, and everyone to self actualize this year but will it happen?

Come on, man, let’s be realistic. China’s not about to give up it’s sovereignty to Trump. See our post from yesterday.

In my experience in participating in and negotiating several multibillion sovereign debt restructurings, a good and doable deal is one where both sides win more than they give up yet at the same time both sides are not entirely jubilant with the final outcome.

…in a long-term relationship with the other party, drive for a win-win. Exercise caution driving for a win-lose. People [and Countries] have long memories, and you might encounter them again, perhaps when they are in a position of relative strength. — BizJournals

Trump is notorious for driving for a win-lose outcome. Xi will having nothing to do with it.