Here’s a quick list of Things We Should Have Learned by Now:

Potential growth in developed economies is lower than it was before the GFC. And policy can’t do as much about it—whatever your policy inclinations—as we’d like to think.

The interest rate sensitivity of economic activity is far less than was believed to be the case.

The economic channel of monetary policy and financial channel of monetary policy have to be thought through jointly and separately, and often have very different requirements and equilibrating dynamics.

Oil matters less. It didn’t help the consumer as much as forecast when it fell, and didn’t hurt GDP as much as others suggested, either. Oil intensity of GDP or share of consumption basket is far lower than the levels most observers—consciously or unconsciously—had anchored on.

The overall commodity intensity of output has declined significantly and will continue to do so. It is in some sense the very definition of technological advancement.

Commodity markets (IDK about softs) are driven in the first instance by speculation, which regularly overwhelms fundamentals.

Inflation/wage impulse per increment of GDP has been systematically lower than thought. And transitory shocks are often, well, transitory.

Government intervention is a necessary evil in a financial crisis. What’s desirable isn’t always feasible. Path dependency is dominant. And circuit-breaking the self-reinforcing downward spiral of panic is essential.

The bond market—in both shape and level—has been telling us very little about US economic prospects/activity. However, short-term changes do inform us as to the prevailing narrative.

Economics should be used for diagnostic purposes, not predictive ones.

Very few investors/traders can disentangle their political preferences from their economic analyses. Systematic traders, disciplined risk managers, and passive investors have a big advantage in this regard.

Salil writes….Fast forward a decade and we will have a whole generation of people who’ve come to realise they don’t need to own an asset to use or enjoy it. And even if they were to think of buying an asset, is there room for another monthly instalment in their budgets, after having spent on an exotic vacation and for the latest iPhone? Buying a large ticket asset such as real estate then seems to be an impossible task, especially in the metro cities where property prices are unaffordable for most white-collar workers even today. A generation conditioned by the conveniences of a sharing economy, and the ubiquity of cheap credit that spurs consumption, will have a detached attitude towards home buying, a purchase/investment which once upon a time was seen as a milestone for Indian families. Millennials and Generation Z will see lesser merit in buying a home and greater sense in renting one, especially given the huge differential (4-5x) between rents and an EMI for a loan on the same house. They would rather spend the difference on consumer durables or holidays or even invest it. Other demographic changes, such as higher mobility (for jobs across cities) and late marriages will also increasingly shape the demand for residential property – owned or rented. Some of these trends, in varying degrees, have been seen in the US and China too,

That does not imply that the younger generations will forever stay in rented homes. Just that they will feel no pressing need to make that a priority i.e. they will postpone their home buying. And it doesn’t take long for such behavioural changes to impact share prices – we are seeing the effect that just 6 years of Uber’s operations in India have had on demand for cars in India.

We all hope that our tax dollar will be use productively for creating capital asset than instant gratification through revenue deficit which only increase the burden for future generations but Martin Armstrong is very categorical when asked on this subject. He writes in his blog

“That proposition assumes the government can actually do anything correctly. There is absolutely no evidence of that whatsoever in the historical records going back thousands of years. I do not care how much they raise taxes. The pension crisis alone will wipe out government as we know it. For every person that retires, they must replace them and the cost of government doubles. A child with a pocket calculator can give you a better forecast. It is absolutely impossible for this to ever end nicely. The system is not sustainable.“

I agree with this view and I believe a tax hike is coming across most of the world as govt deficits increase and they falls short on pension and health liabilities. This will be in addition to the lost revenue on account of cooling off of real estate markets.

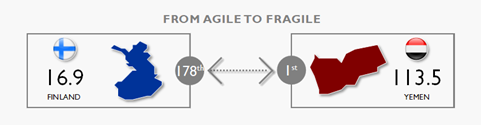

“This year,

Yemen claimed the top position for the first time as a result of its civil war

and humanitarian catastrophe. Although Yemen’s top ranking may provide cause

for idle chatter, really the most attention should be given to its rapid

worsening over the past decade, and the regional instability and power plays

for which its population are unspeakably suffering.

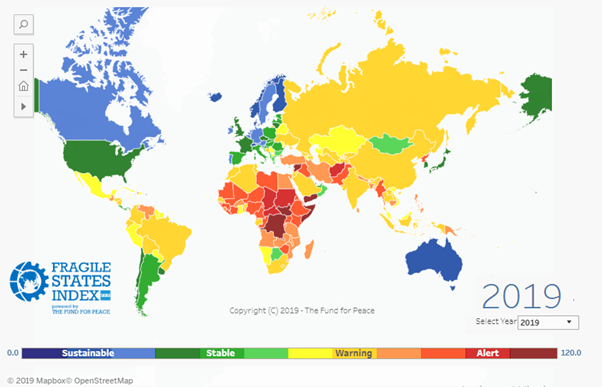

In 2019, an African nation has, for the first time, ranked in the “Very Stable” category, with Mauritius ascending to join the likes of the United Kingdom and United States. Just as Mauritius this year became the first African country to break through to the Very Stable category, it is also important to recognize that Singapore became the first Asian nation to move into the Sustainable category.”

“There

is still widespread fragility and vulnerability, plenty of poverty and

inequality, and conflict and illiberalism. But broadly speaking, over the long-term,

the world is becoming steadily less fragile. It often takes cold, hard data —

like that produced by the FSI — to demonstrate that for all the negative press,

there is significant progress occurring in the background.”

J.J. Messner, Executive Director

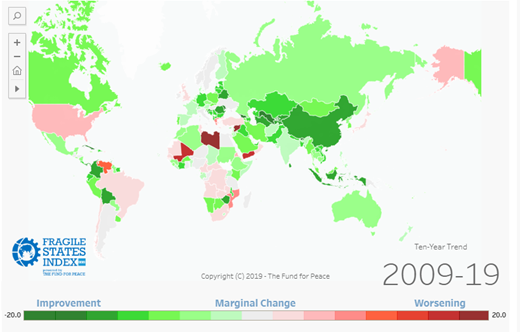

“Two countries tied for most-worsened over the past 12 months. Venezuela has been beset by enormous turmoil, and in the wake of a contested and deeply flawed election in 2018, now finds itself with two leaders. Brazil’s internal challenges remain significant, with tumultuous politics and a new president who came to power through a campaign fuelled by harsh right-wing rhetoric.”

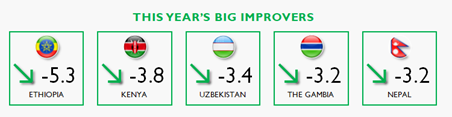

“After having ranked as the most-worsened country in the 2017 FSI, Ethiopia has staged a remarkable turn-around this year, ranking as the most-improved country in the wake of the ambitious reform agenda that has led to more political and social inclusiveness, breaking down the previous ethno-centric system that the country endured for decades.”

As per World

Economic Forum, “Any UK citizens alarmed at seeing their nation ranked as the

fourth most-worsened will find that three of the 12 indicators used to compile

the index were largely behind the low score: the behaviour of ruling elites,

social divisions and state legitimacy.

The authors point to

the influence of Brexit as a factor. But they say that long-term worsening of

the UK’s score predates the country’s referendum on membership of the European

Union. Even before 2016, the authors say the UK had the seventh worst trend for

the same three indicators, and suggest the country’s problems are deep-rooted

and unlikely to be solved by leaving the EU.

The US made it into the Most Worsened category thanks to poor scores in the same categories as the UK plus a sliding score on human rights and respect for the law, in part reflecting political divisions, legal controversies and the issue of immigration.”

As per World

Economic forum, “We need more investors who are willing to take chances in

countries that need us most. These are places where we can all make the

greatest difference in ending extreme poverty and boosting shared prosperity.

These are the places where economic and social progress would ensure peace and

stability.”

Let me give you the Cliffs Notes version of how I think the next decade will play out, more or less, kinda sorta.

We already see the major developed economies beginning to slow and likely enter a global recession before the end of the year. That will drag the US into a recession soon after, unless the Federal Reserve quickly loosens policy enough to prolong the current growth cycle.

Other central banks will respond with lower rates and ever-larger rounds of quantitative easing. Let’s look again at a chart (courtesy of my friend Jim Bianco) that I showed three weeks ago, showing roughly $20 trillion of cumulative central bank balance sheets as of today. If I had told you back in 2006 this would happen by 2019 you would have first questioned my sanity, and then said “no way.” And even if it did happen, you would expect the economic world would be coming to an end. Well, it happened and the world is still here.

Before 2008, no one expected zero rates in the US, negative rates for $11 trillion worth of government bonds globally, negative rates out of the ECB and the Swiss National Bank, etc. Things like TARP, QE, and ZIRP were nowhere on the radar just months before they happened. Numerous times, markets closed on Friday only to open in a whole new world on Monday.

In the next crisis, central banks and governments, in an effort to be seen to be doing something, will again resort to heretofore unprecedented balance sheet expansions. And it will have less effect than they want. Those reserves will simply pile up on the balance sheets of commercial banks which will put them right back into reserves at their respective central banks.

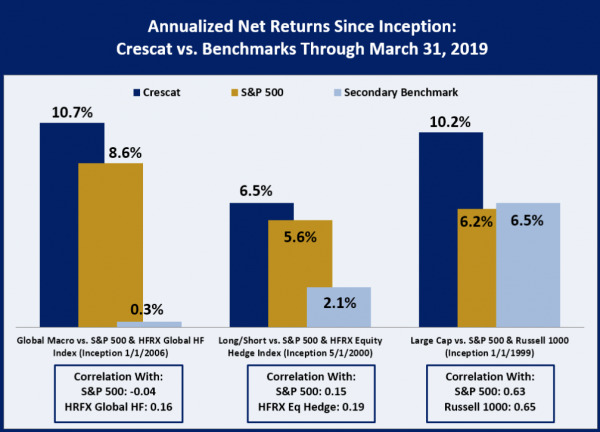

Crescat was one of the best performing hedge fund of 2018 and although this year has started on a negative note , they clearly lay down their views and strategies for this tough market .

They write……The year-to-date rally in global risk assets after the Fed flip appears to us to be a last gasp of speculative mania for the current economic cycle.

In our view, three flawed narratives are driving late-cycle euphoria in financial markets today:

“Central banks can always prevent a downturn in financial markets and the business cycle”;

“US stocks valuations remain attractive”; and

“Chinese stimulus and a US-China trade deal will reignite growth in the second half of 2019.”

We believe that the first two storylines are simply wrong. We show why herein. Regarding the third, in our view, China is much more likely to tank the world economy over the next several quarters than rescue it given the historic credit imbalances there.

Central Banks Do Not Have Your Back

There has been a huge misconception that global central bank liquidity is what is driving stock prices up today. Our work shows that both global M2 money supply and central bank assets have been contracting on a year-over-year basis so far in 2019. That tells us liquidity has not been the driver of the market-top retest rally; hope has been.

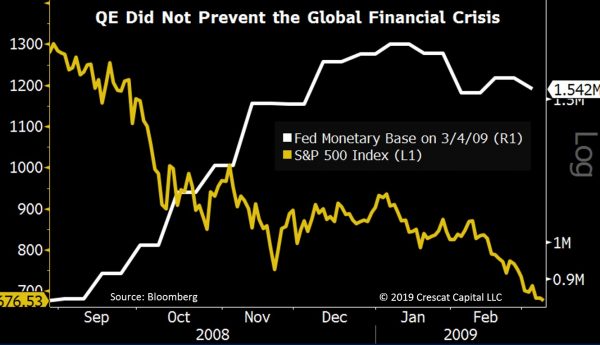

But even when global QE returns, it is likely to be no saving grace. As shown above, starting in September 2006 led by China, global central banks increased their balance sheets by $3.9 trillion or more than 50% through March of 2009. This unprecedented level of money printing did not prevent the Global Financial Crisis. Rather it preceded and accompanied it.

Even the Fed’s QE1 which started in 2008 did not stop stocks from plunging; it only coincided with it as shown below.

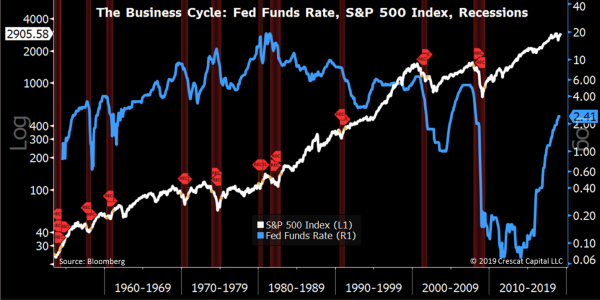

The same goes for the Fed’s past changes in interest rate regimes from hiking to easing which are much more often bearish than bullish for stocks. As we show in the chart below, there were twelve times since 1954 (the history of the Fed Funds) that the US central bank paused its interest rate hiking cycle and then reversed it. Only three of those reversals ended in soft landings (1966, 1984, and 1995). In contrast, nine were associated with stock market downturns that led to recessions. We believe the three soft landings were possible because they occurred early in the business cycle, an average of only three years into the expansion. The Fed’s December 2018 hike followed by a pause, on the other hand, occurred a record 9 1/2 years into the economic expansion, beating the pause at the peak of the tech bubble by one quarter! Of the nine pauses associated with market downturns and recessions, the economic contraction began an average of just five months from the date of the last rate hike. That would be next month if this is the average delay! But we likely won’t know officially when the next recession begins, as typical, until months after it has started when prior-reported economic data gets revised downward.

It is also important to note that the stock market peak associated with the nine recessions occurred an average of two months before the last Fed rate hike. The September 2018 market peak, therefore which we are re-testing though still shy of, could still be relevant; it was three months before the Fed’s last hike. Even if the market pushes marginally higher here, it will still be very likely that we are near a top based on Crescat’s work.

It is also important to note that none of the historical corrections and bear markets that surrounded late-cycle Fed rate reversals bottomed until after the economy entered the recession. It seems highly prudent therefore to wait until the next inevitable recession which could be right around the corner before buying stocks today.

Another good macro timing signal for the peak of the stock market and business cycle is when the credit markets start pricing in Fed rate-cuts late in the expansion. That has never been a bullish sign. As shown in the chart below, every prior time the 2-year yield started to fall after re-testing a multi-decade resistance line going back to 1980, a major bear market and recession followed. Will this time be any different?

Precious Metals

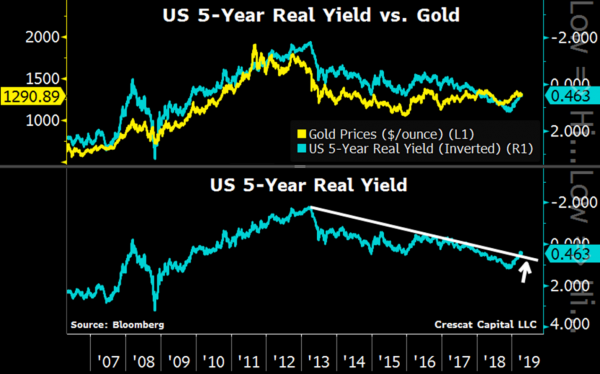

The recent drop in nominal rates is also causing a drop in real yields. Below we show a multi-year breakout of the 5-year TIPS, inverted, which reflects the real interest rate. Real rates have followed gold prices remarkably closely for years. If this pattern holds, even if inflation expectations remain muted, the decline in nominal rates should be positive for gold, especially at today’s historically low valuation relative to the global fiat monetary base.

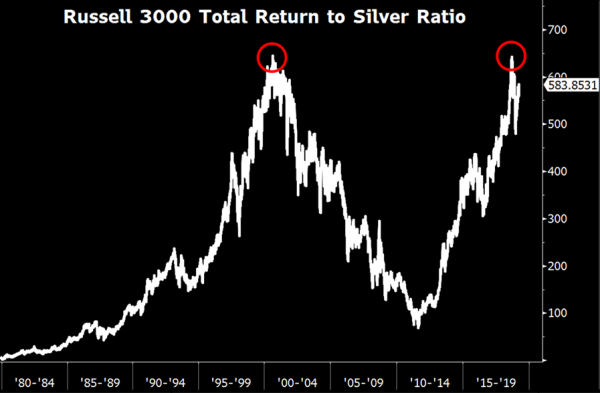

It’s stunning to us how historically depressed the valuation for gold’s high-beta, safe-haven cousin, silver, is this late in the cycle. One interesting way to see this is by comparing silver’s performance relative to a broad US stock index. Below, we show Russell 3000-to-silver ratio near record levels. It formed what appears to be a double top after retesting tech-bubble-peak levels last year.

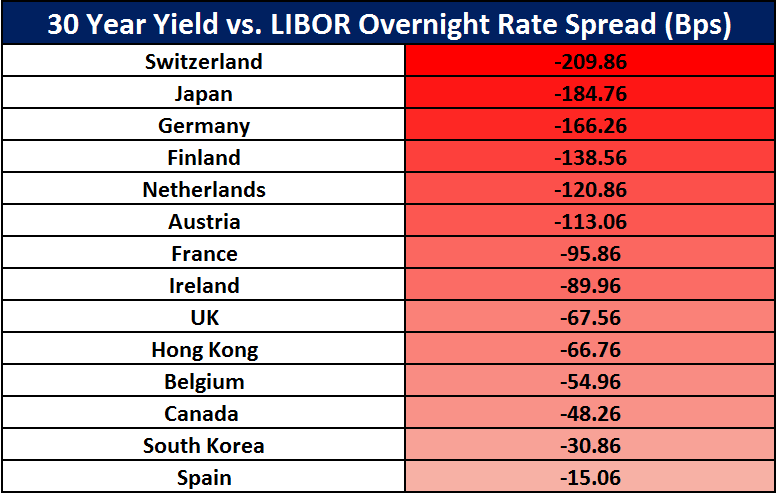

Global Yield Curve Inversion

As we noted before, today we have an unprecedented amount of economies with 30-year yields lower than LIBOR overnight rates. Spain just joined the pack recently and we now have fourteen economies showing this negative spread. For us, it reiterates Crescat’s global yield curve inversion thesis, which is negative for global stocks and positive for future inflows into US dollars, and US Treasuries by extension as haven assets in a global financial crisis. The fact is, US yields across the entire curve today are attractively high compared to many global developed market alternatives.

When financial crises have unfolded in the past, US rates have tended to converge with global rates. Therefore, we expect many of these yield spreads to narrow significantly as the global economic cycle turns down.

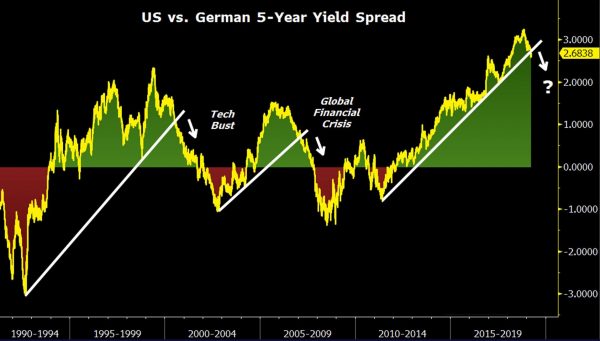

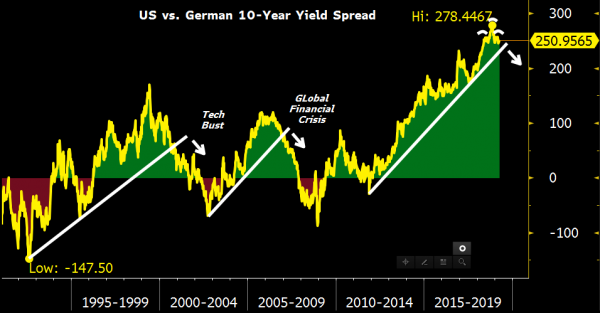

US Treasury vs. German Bund Spread

US vs. German 5-year yield spread just broke down from a multi-year support line! Previous breakdowns timed the market top in 2000 & 2007. It’s another critical macro timing indicator.

The US-German 5-year yield spread breakdown is possibly leading a big move that is likely to happen on 10-year spread. In our global macro hedge fund, we are long US 10-year Treasuries and short 10-year German Bunds to play the likely breakdown and narrowing of that spread as shown in the chart below. The legendary former bond king, Bill Gross, was too early in this trade. It got away from him, but it was still a good idea. The trade is now lining up with so many of our other macro timing indicators that we believe the spread is finally getting ready to converge. A classic head-and-shoulders pattern meanwhile appears to have formed over the last year, a bearish technical set up.

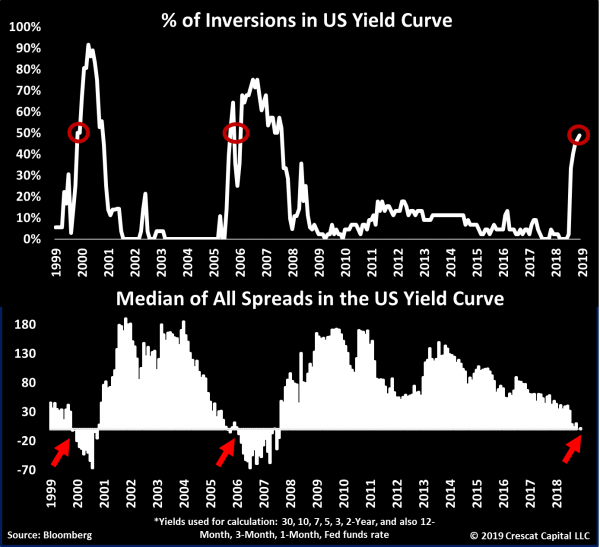

US Yield Curve Inversions

Below is our comprehensive way of measuring inversions in the US yield curve. This model calculates all possible 44 spreads across US rates, and the percentage is now close to 50%, just as high as it was at the peak of the tech and housing bubbles. Historically, these elevated levels of inversions tend to be great times to own precious metals and sell US stocks.

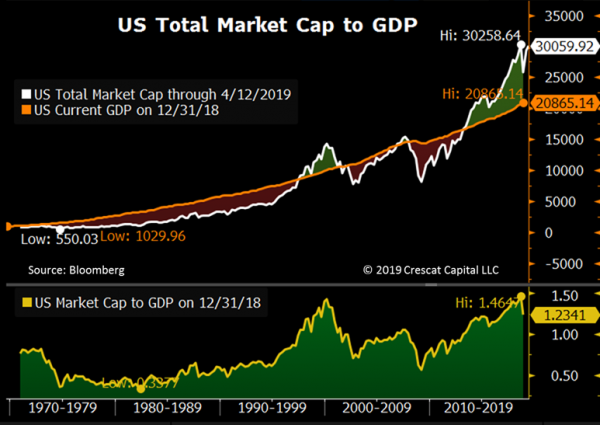

US Equity Valuations Near Record Highs

The recent surge in stocks has pushed valuations back near all-time highs. Below, we show that the total US market cap-to-GDP ratio reached its highest ever last September at almost 150% prior to the 4th quarter market meltdown. This measure is close to re-testing its highs again today! The first panel of the chart below illustrates how the total US equity market capitalization tends to fluctuate above and below GDP across economic cycles. A multiple of one time GDP tends to be the median valuation over time. But valuations rarely stop at the median during bull and bear market cycles. They have become more stretched than ever relative to GDP in the current business cycle. In the second panel, we can clearly see that valuations in this cycle went even higher than in the tech bubble.

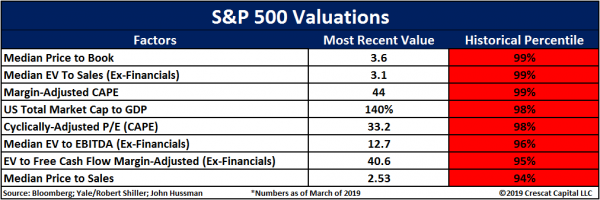

Total market cap to GDP is just one example of US stock market valuations at historic extremes. Crescat’s models show that record valuations were hit on September 2018 across most valuation measures. We are just shy of re-testing them today:

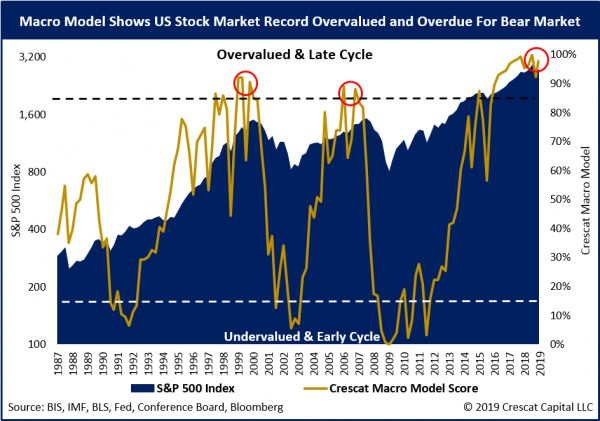

Crescat Macro Model

Crescat’s macro model combines sixteen factors across key fundamental, economic, and technical indicators to time the stock market and business cycle. After the year-to-date rally, the model is just two percentage points from record overvalued and record late-cycle levels! The yellow line below shows a back test of our model score going back to 1987. The model did extremely well at timing the tops and bottoms of the last two US stock market and business cycles. This time, the S&P 500 briefly entered overvalued/late-cycle levels in September of 2015 and was followed by a meltdown in China and emerging markets that Crescat capitalized on in 2015. A pause in 2016 in Fed interest rate hikes gave emerging and developed markets a new lease to extend the global business cycle. As hikes resumed in 2017, the market and our macro model score only surged to new highs. In September 2018, we reached what we believe were and still are truly mania levels.

We strongly believe US stocks are overdue for a bear market and the time of reckoning is near. The bear market started to unfold in the fourth quarter of last year in our view. But now we are close to retesting the September highs. Based on Crescat’s macro model score, and a myriad of other indicators, there is a strong probability that this rally will fail and that the bear market will resume.

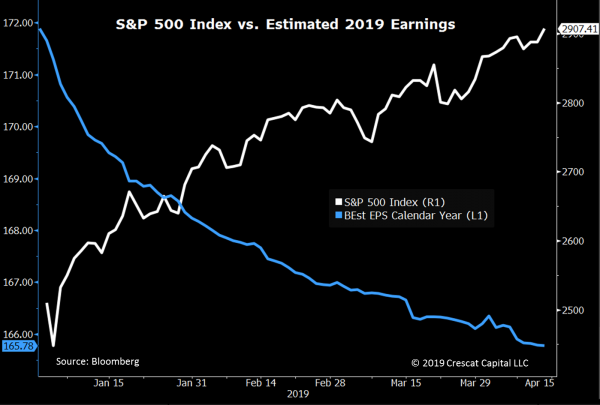

It’s interesting to us how surging US stocks are in complete disconnect with the deteriorating fundamental outlook. Earnings estimates for 2019 in fact have been plunging all year while diverging significantly from sharply rising equity prices. This is not a positive set-up for stocks as we start the Q1 earnings season.

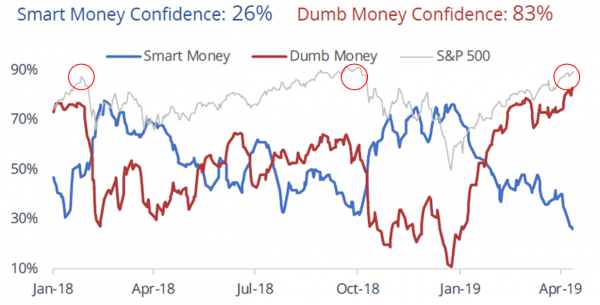

Sentiment Indicators

The recent stock market rally has remarkably similar fingerprints to the January 2018 and September 2018 speculative tops as shown by the two charts below courtesy of Jason Goepfert at sentimenTrader.com.

Jason’s smart versus dumb money indicators incorporate OEX put/call and open interest ratios, commercial hedger positions in equity index futures, and the current relationship between stocks and bonds. The smart-money indicator is currently near its lows while the dumb money one is near its highs. A similar wide spread between these two indicators preceded the market’s two steep selloffs last year.

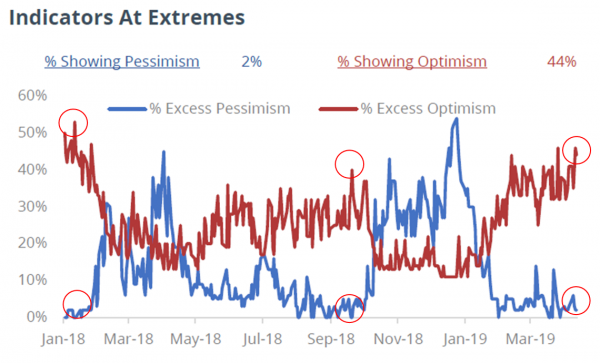

SentimenTrader also tracks 60+ market indicators and tallies the percentage of them showing extreme optimism versus extreme pessimism. As shown in the chart below, 44% of these indicators are registering extreme optimism levels in equity markets today. Conversely, only 2% of these indicators are showing significant levels of pessimism. Similar to the smart vs. dumb money spread, such divergences performed extremely well at identifying the last two interim market tops.

Record bullishness sentiment rarely ends well for longs. Neither does extreme divergences between speculative longs and professional hedgers who are short.

Certainly, indicators like these in hindsight could have helped us see how temporarily oversold the markets were in late December to better manage the recent counter attack from the bulls. While we have stayed grounded primarily in our macro and fundamental research, and that will not change, sentiment indicators can help on the margin. We hope they will help others to can see why timing for many of our tactically bearish macro views could be ripe.

The chart below shows a third sentiment indicator we found that looks incredibly frothy today, VIX speculation at an extreme. Speculative futures traders are more net short stock market volatility than they were at the September market peak.

China More Likely to Tank than Rescue the Global Economy

We think those looking for China growth resurgence or trade deal to materially extend the stock market and business cycle are sorely mistaken. We have written extensively about China’s 400% growth in banking assets since 2008, likely creating the largest credit bubble and overvalued currency in modern financial history. Based on this unsustainable rate of credit expansion, China was responsible for over 60% of global GDP growth since the global financial crisis. The country’s massive investment in non-productive infrastructure assets was financed on credit and created high GDP growth but failed to add to the wealth or debt-servicing capacity of the country. As a result, China appears to us to be a financial crisis waiting to unfold.

State-directed misallocation of capital has compromised the savings of Chinese citizens. In other words, there is an enormous non-performing loan problem that we believe renders China’s banks insolvent. The country’s citizens, the banks’ creditors, are the ones holding the bag. When the Chinese economy inevitably implodes under its bad debt, the government will be forced to print money to recapitalize its banks and bail out its citizens to avoid social unrest. This massive money printing will almost certainly lead to a currency crisis.

The Trump administration’s hardball on trade is just one of many catalysts for the bursting of the China credit bubble. Whether there is a trade agreement or an ongoing trade war, either one would lead to a continued decline in China’s current account balance which should exert downward pressure on its currency. We think China’s increasing fiscal deficit due to the recent stimulus will also exert new downward pressure on the currency.

While the US administration may continue to hype an impending trade deal as hope for financial markets, we believe trade talks have dragged on for too long already to not have wreaked havoc on global supply chains and economic growth for the rest of the year. As the light continues to get shined on China, it should become clear that nothing beyond a token trade deal is likely to ever be reached. It is much more likely that the ongoing trade negotiations will only continue to serve to awaken the US government and its citizen voters to the egregious extent of China’s malfeasance.

China’s cyber hacking, intellectual property theft, and forced technology transfer are likely to be impossible roadblocks to arriving at any meaningful and enforceable trade deal. The U.S. Trade Representative reports make it clear that China has failed to live up to its commitments to open its markets to fair trade ever since it was permitted to join the WTO in 2001. China’s state-directed economic policies are simply incompatible with an international trade system based on open, market-oriented policies and rooted in the principles of nondiscrimination, market access, reciprocity, fairness and transparency.

With election season upon us in the US, the nature of our country’s engagement with China should once again become a major campaign issue. Taking a strong stance against China’s trade and human rights transgressions would likely have broad, bi-partisan voter support. Democracy, liberty, and justice are the foundation that has made the US a true world economic superpower. Contrast that with China’s authoritarianism, suppression, and corruption. Sure, there may be some corruption in democratic, advanced economies too. But we believe it pales compared to China.

In our view, the trade talks are closer to morphing into a new cold war than to being resolved by a substantial trade pact. Meanwhile, much like downfall of other totalitarian communist economies, we believe both internal and foreign capital is likely to continue fleeing the country, exerting downward pressure on its currency, economy, and banks. We continue to have a negative view on both the Chinese yuan and Hong Kong dollar that we are expressing in our global macro fund through put options on these currencies. We also are short richly-valued, US-listed “China-hustle” stocks in both hedge funds.

Crescat Remains Steadfast in our Views and Positioning

Today, with historic US equity valuations, record credit bubbles globally, and longest US economic expansion cycle ever likely to soon come to an end based on our models, we remain steadfast in our net short US and global equities position in our hedge funds. We are also short subprime credit in our global macro fund. We remain long precious metals and precious metals mining stocks across all our strategies.

There is indeed a US business cycle as well as a global economic cycle. We believe both are ripe for a downturn. We intend to capitalize on it like we did in the fourth quarter of last year which should be only the beginning. Like last year, we are having what we think is only a temporary pullback as the US stock market retests its all-time highs. Like last year, we believe global financial markets are poised for a major downturn. Staying grounded in our models, themes, and positioning was key to our strong year in 2018. Such grounding we believe will be key to generating strong performance again in the coming months and quarters.

We will continue to follow our model signals and risk controls, but we aim to stay net short global equities and subprime credit until the next global economic downturn has been widely acknowledged and stock values are once again cheap before we get significantly net long again.

As macro managers with a strong value bias, we remain confident that the underlying intrinsic value of Crescat’s portfolios at any time are worth substantially more than the market is quoting them (longs worth more and shorts worth less) or we would not be in those positions. This grounding gives us the fortitude to withstand a moderate amount of market volatility and persevere for long-term high absolute and risk-adjusted returns compared to our benchmarks as we have been able to deliver historically and expect to in the future. We think the financial markets are presenting an incredible setup for Crescat’s strategies today

Can we bank upon the banking sector and other financial institutions today? The U.S. Chamber released a Financing Main Street report in which they surveyed more than 300 corporate finance professionals to understand the ongoing impact that financial regulation has on broader economy.

Quoting

from the special report by Better Markets

published on 9th April, 2019, “To save the hardworking Main

Street Americans from economic catastrophe that would have resulted from the

collapse of financial system and economy in 2008, policymakers claim that

without bailing out the gigantic financial institutions, another Great

Depression was inevitable, which would have been worse than the Great Recession

those financial institutions did cause – a recession that will cost the U.S.

more than $20 trillion just lost in GDP.”

“At least

$29 trillion was lent, spent, pledged, committed, loaned, guaranteed and

otherwise used or made available to bailout the financial system during the

2008 crisis.”

As per Executive Summary of report from U.S. Chamber,

“American businesses are reporting that their ability to access capital is

steadily improving and generally they are optimistic about their expected

performance over next 12 months. In order to promote sustainable economic

growth, our financial system must be as vibrant and diverse as the businesses

it serves. U.S. capital markets play a critical role in providing debt and

equity financing to American businesses. A

key component of a strong financial system is a regulatory structure that

promotes economic growth.”

They

further add, “Unfortunately, the post 2008 financial crisis regulatory response

imposed enormous costs on the economy while doing little to fundamentally

reform the U.S. financial regulatory system.

As a result, Main Street businesses found it more difficult to access

the capital they needed to innovate, grow and hire new employees.”

For years

big financial institutions engaged in high risk transactions, manipulated

regulations, committed crime and settled it all against fine. Their deeds led

to the crash of 2008 yet they sang their songs of innocence and were bailed out

by transferring huge wealth from Main Street to Wall Street and as Better Markets puts, “The banks showed

no gratitude, no remorse and no willingness to reform their activities. They

didn’t bother to end their systemic, widespread and brazen illegal conduct.”

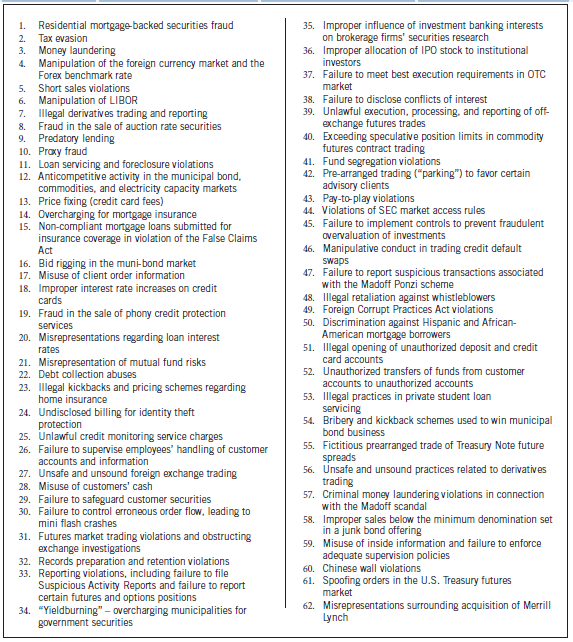

The chart shown is from Better Markets and it is not still an account of the entire list of actions. These are only a few classic ones.

We have

contrasting view by Brett Milano who wrote on Harvard Gazette about the seminar

conducted by Niall Ferguson and quoted him, “Of the common theory that the

crisis happened because of deregulation, ‘You

should dismiss that as a cartoon.’”

Ferguson

carried on, “That’s a fantastic example. Bernanke had studied Great Depression,

so as the crisis intensified he was in the position to identify and recognize

the symptoms of something much bigger than anyone in the room had experienced

in their lifetimes. You could have anticipated the choices Bernanke made

(addressing to Harvard students who were his students) and would have known

that the Fed (in 2008) would do exactly the opposite of what the Fed did during

the Great Depression, because they did everything wrong the first time.”

As per

Ferguson, “One of the main reasons another depression was avoided was a global

component, the stimulus money U.S. received from China. The relationship

survived the crisis despite some pretty nasty rhetoric; we called them currency

manipulators. But China didn’t sell their great accumulation of U.S. bonds. China

may well be next source of global crisis and the decline of China – U.S. Relations may prove the tipping point. The

best case scenario is that China’s growth rate steadily declines. In worst

case, there is a crisis. Either way, the outlook is bleak one.”

Milano

concluding the seminar writes, “During

the audience questions afterwards, one student asked Ferguson if he’d neglected

to mention the role of fraud and other white collar crime in triggering the

2008 crisis. Ferguson replied that almost no bankers ever went to jail.”

Ferguson

added, “Is that because we decided to

turn a blind eye to white collar crime, or is it because they committed no

crimes, they only bent the rules? I think it’s the latter. It is really hard to

get convictions when people were essentially complying with the regulations. As

long as they were compliant, nobody felt any compunction about doing things

that were morally wrong, if not technically criminal.”

Report from

U.S. Chamber deduced, “Overall, businesses report that while there have been

improvements in accessing short term credit, their ability to raise long term

debt as well as equity has become more difficult. Companies are also more

pessimistic about the overall economy than about their own performance: More

than one – third expect the economy to worsen over the next 12 months, with

interest rates and trade related issues cited as the top two concerns.”

“Businesses

have long relied on financial system for traditional banking and lending

products, but they increasingly rely on financial institutions to manage

currency fluctuations, hedge risk through derivatives and raise large amount of

equity or debt. Unlike in other countries – where traditional bank lending

remains the primary source of corporate finance – the U.S. capital markets play

a critical role in helping companies meet both short term and long term

obligations.”

A huge

amount of taxpayer money has gone in ongoing bailout of financial system. As

per ProPublica, their database accounts for both broader $700 billion bill and

separate bailout of Fannie Mae and Freddie Mac.

As per

ProPublica, a few companies failed to repay the government and all other

investments either returned a profit to the government or might still be

repaid. Recipients of aid through TARP’s housing programs (such as mortgage

servicers and state housing orgs) received subsidies that were never intended

to be repaid. There have been 980 recipients with $632B in total disbursement, with

$390B total returned and total revenues from dividends, interest and other fees

account for $349B.

“The eight

large U.S. banks received Treasury Department’s initial round of capital

investments – money described by Treasury officials not as a bailout but rather

as funds to help ‘bolster heathy banks’. “

Out of these 8 large banks in U.S. Better Markets focussed on six megabanks, Bank of America, Citigroup, Goldman Sachs, JP Morgan Chase & Co., Morgan Stanley and Wells Fargo, they committed several illegal acts and were subject to more than 350 major legal actions which resulted in almost $200 billion in fines and settlements. They received more than $8.2trillion in bailouts!

Better Markets noted, “Some eye – catching cases are like the infamous LIBOR manipulation. Among others, Citibank and JP Morgan Chase were also involved in this scandal with Citigroup paying a whopping $175 million civil penalty to CFTC.

In May

2015, the DOJ announced that Citigroup, JP Morgan Chase, Barclays and Royal

Bank of Scotland pled guilty to charges of conspiring to manipulate the price

of U.S. Dollars and euros exchanged in foreign currency exchange spot market.

Together, they paid more than $2.5 billion criminal fine. This scam impacted

every consumer in US as FX markets are used by virtually every company

producing goods that are purchased in US and also used by those in connection

with anyone traveling overseas.

In December

2015, SEC imposed $267 million in penalties against JP Morgan Chase for fraud,

failure to disclose conflicts of interest and breach of fiduciary duty by its

wealth management institutes. The misconduct extended from 2008 to 2013.

In

September 2018, a federal judge approved a class action settlement to resolve

claims that Bank of America improperly charged overdraft fees amounting to

interest which when annualized far exceeded the limits on maximum interest

rates set by National Bank Act. They paid $66 million in reimbursements and

debt relief.

In Wells

Fargo, a federal judge in May 2018 and in September 2018 approved a $142

million in settlement and $480 million in settlement respectively for customers

and shareholders who were harmed by fake account scandals.”

The number

of cases increased in post-crash compared to pre-crash. U.S. taxpayers didn’t

provide their money to bail out the banks and save them from bankruptcy so they

can continue their illegal conduct. In fact, it appears that these fines and

settlements are speed bumps in their business and not a mistake to them.

Admiral Yamamoto on the Pearl harbour attack “I can run wild for six months … after that, I have no expectation of success”.

Nirmal Bang writes…ICICI Bank – Mr Anup Bagchi and AXIS Bank- Mr Amitabh Chaturvedi have guided that they are looking to grow in high teens in the Auto loan category. As a matter of fact there are products which are launched by them to promote disbursements which sound like “Sirf 2mins”. Reminds me of Maggi. ICICI Bank calls its “Insta Auto loan”

Last 5 years has been glorious for HDFC Bank, Kotak Mahindra Bank & everyone who did not suffer from NPA attack as

ICICI Bank and Axis Bank were busy cleaning the mess around their own house-(mess is a small word, it was Nagasaki)

40% of their book grew without they making any effort given 3large Credit segments grew from 2014 1.Auto loans 2.Loan Against Property and NBFC lending

The total Auto Loan market in India (excluding CVs, Tractors, Large Vehicles) is Rs 1.5Lcrs/Rs 1.7Lcrs Pa. along with the Realty+ Lap+ NBFC= ~ 6/7Lcrs … that book will now see at least ten entities trying to grab the pie – whatever they get with all Banks trying convert short-term liabilities (deposits) to long-term assets (loans). Some banks also used reserve to create Assets. The business from 2013-18 was relatively simple given most of other competitors were busy clearing their book after the NPA attack they suffered from (Very similar to USA- They prospered more versus the other countries more because no war was fought on their Land, baring One –Pearl harbour)

However come

2019..things are going to be tough as

Giants have not only cleaned their Bomb attacks , but they are ready with their Bazookas to hit their neighbors-(why?, just because they are jealous & want to grow too)

2) The 2/3 key growth areas have slowed down considerably 1) Best Case Auto growth for FY20/21 is 5% CAGR, 2) NBFC growth is expected @ 10/12%. 3)LAP/Realty may grow ( >15%) , however it can be the sole driver of the book growth. Personal loans is another category which will see all ten large liabilities franchises attacking at the same time (there is an ad of Allahabad bank offering personal loans from 8.5%)

Conclusion

India Banking for next 2/3 years will be like a Dog eat Dog world …to make matters worst for HDFC Bank, KMB.. The PSU banks will also be there on ground -given that their Asset side has been corrected to a large extent and liability will see growth at the same rate as GDP, which is sufficient for them to get that 12/13% growth rate.

On Trailing

P/B Dep(Rs bn)

HDFC Bank

5.91 9050

KMB

5.24 2058

ICICI

2.44 8151

AXIS Bank

3.07 6114

IIB

4.66 1800

BOB

1.03 6538

CBK

0.73 5247

Syndicate

0.83x 270

J&K

0.63x 860

f

Its going to a Harbor attack by All Gordon Pranges and it’s run run run to value ones

Sucheta Dalal writes Jet Airways, once India’s biggest airline, has been grounded, leaving the lives of nearly 20,000 employees and lakhs of customers in disarray. Employees haven’t been paid since December-January. Customers find their holidays in chaos; funds blocked in refunds; while they are forced to book again at steep rates, to salvage hotel bookings. All the while, the civil aviation ministry has fiddled. Well, it apparently held meetings and issued ineffectual advisories asking other airlines not to hike https://www.moneylife.in/article/jet-airways-bungling-employees-shareholders-customers-and-taxpayers-will-pay-the-price/56925.html

Wolf richter writes for his global audience in wolf street…

Today, another major airline collapsed. Jet Airways, India’s largest private airline, announced “with immediate effect” that it was “compelled to cancel all its international and domestic flights.” It suspended operations on a “temporary” basis. It said: “Since no emergency funding from the lenders or any other source is forthcoming, the airline will not be able to pay for fuel or other critical services to keep the operations going.”

Last year, Jet Airways “suddenly” discovered serious financial issues, which led to a highly dramatic rescue effort by the main creditors (chiefly state-owned State Bank of India and private-sector ICICI Bank) and minority shareholder Etihad under the new Sashakt legislation introduced by the Indian government to deal with the chronic “sudden liquidity problems” of the giant Indian economy.https://wolfstreet.com/2019/04/17/more-airlines-collapse-jet-airways-india-alitalia-wow/

My two cents

Crony capitalism keeps on taking its toll in India and the promoters are never at receiving end. Sector after sector competitive intensity is coming down as companies only cared about market share over profitability. The misallocation of capital had to come out somewhere and the people who will pay for it are the common people.

Is it different this time? Has innovation and winners take all triumphed over the lack of cash flows. In fact companies like Lyft and UBER are brazen enough to tell you that they might never make profit. Think from a point of view of poor fund managers with fiduciary responsibility to manage your money and is struggling to beat the market or from a private equity guy who is not finding enough unicorns to invest his overflowing coffers.

This is what leads to groupthink aided by free money created out of asset inflation and it will continue till we see first sign of real price inflation in real economy.