Hello, This is a short weekly email that covers a few things I’ve found interesting during the week.

Article Horizon Kinetics is one of the websites I periodically check to see if they have posted anything new. Their quarterly commentaries are must-reads.

Podcast Louis Vincent Gave is one of my favourite thinkers and in this podcast or youtube clip he outlines a very clear framework for how he views the world. “There are three prices that matter more than any other and what everything else is priced off.-The 10-year Treasury yield.-The US dollar.-The oil price.If you get these right everything else falls into place.”Quote “You can measure everything about a bubble except the most important part: When investors will stop believing in it.

The end of the bubble is just the end of enthusiasm.

And enthusiasm isn’t a tameable statistic.

It’s a hormone that owes nothing to the logic of your data.” -Morgan Housel My favourite tweet ChartTechnical analysis isn’t my strong point but when I see a trading range compressing like this, the result is usually explosive.

Books Nassim Taleb’s has done a lot to shape my thinking with his work over the years.

I’ve started working my way through Antifragile for the second time. If you don’t have time to read the book these points from this article summarise it well.Stick to simple rulesBuild-in redundancy and layers (no single point of failure)Resist the urge to suppress randomnessMake sure that you have your soul in the gameExperiment and tinker — take lots of small risksAvoid risks that, if lost, would wipe you out completelyDon’t get consumed by dataKeep your options openFocus more on avoiding things that don’t work than trying to find out what does workRespect the old — look for habits and rules that have been around for a long time Something I’m pondering

I’m still fascinated by Raoul Pal’s bold announcement and changes to his macro views, which I’m trying to wrap my head around.I watched his recent video on Real Vision where he poses two questions that have got me thinking. “Question why you hate it?”This question was posed in relation to Cathie Woods Ark; “You are doing it because of jealousy of her performance and her outrageous price targets and they have been right.” I object to this as my big gripe with Cathie is the shallow and flawed analyses she presents. Tesla didn’t achieve its valuation as a result of it meeting any of her assumptions.

Yet when it hits her price target she puts out an even crazier price target for which the assumptions make no sense (Ark see that by 2025, Tesla will achieve 80%-120% of non-hybrid global EV to insurance business margins never seen before in the insurance industry) and outright errors and does not consider CAPEX or capital raising in the methodology (if you’d like a deeper dive this is a great thread). It reminds me of Annie Duke’s book ‘Thinking in Bets’“We have a tendency to equate the quality of a decision with the quality of its outcome.Poker players have a word for this: “resulting.” When I started playing poker, more experienced players warned me about the dangers of resulting, cautioning me to resist the temptation to change my strategy just because a few hands didn’t turn out well in the short run.A great decision is the result of a good process – not that it has a great outcome.”Second question“That is mean reversionist thinking, why are you apologising for the euphoric thinking?2000 wasn’t a bubble it was a minor blip on an exponential chart of the internet.” Now, this really annoys me as it ignores the whole behavioural side of investing.

Following an 80% drawdown in the Nasdaq by 2002.

Then the index largely going nowhere through to 2011.

I bet most investors didn’t feel they were riding an exponential trend of the internet and had likely thrown in the towel along the way. It’s a similar idea to saying; “I wish I’d just bought Amazon in 1997.” The truth is that there is near- zero chance you would have hung on through the brutal volatility.

Amazon Share Price1997: $11998: $71999: $1102000: $142001: $52006: $362007: $1102008: $502010: $135 $10k to $1.1m and back to $50k would really screw with you mentally! I hope you all have a great week. Cheers, Ferg

It’s the end of the Age of Reagan, but it’s much more than that

“If the formula doesn’t work, you change the formula.” — Arin Hanson

“The era of ‘big government is over’ is over.” — James Medlock

I know this post has a very Vox-like title, but in fact I’m not going to go through Biden’s new infrastructure plan point by point and tell you what’s in it. if you want that, you can check out the actual Vox explainer, or the always-excellent writeup by the WaPo’s Jeff Stein et al. You can also check out Brad DeLong’s thoughts and David Roberts’ deep dive into the climate aspects. I’m sure there will be more in the days to come, and I’ll have plenty of thoughts on the specific provisions as well.

What I want to do in this post, however, is try to figure out what it all means. By now I think everyone has realized that something is changing in American economic policy. The tenor, pace, and scope of Biden’s economic programs proposals, and the muted nature of the ideological opposition, suggest that we’ve entered a new policy paradigm — much as when FDR took office in 1933 or Ronald Reagan in 1981. Every President comes in with a laundry list of initiatives, but once every few decades a President comes in with a new philosophy for what policy should look like. And that is happening now. The fact that a $1.9 trillion COVID relief bill was passed with relatively little fuss, and was really just the warm-up to an even bigger infrastructure bill, and that other “big” policies like student debt cancellation are being pursued on the side as an afterthought, should make it clear that Biden is blitzing.

But what’s the unifying philosophy here? What is Bidenomics? I have some thoughts. First, we need to talk a bit about why the old paradigm wasn’t working.

Why we needed a new paradigm

The last economic policy paradigm, bequeathed to us by Ronald Reagan (and Paul Volcker), was based around tax cuts, deregulation, welfare cuts, and tight monetary policy. These were intended as remedies for the two main economic problems of the 1970s — slow growth and inflation, together known as “stagflation”. The idea that tax cuts boost growth comes from basic economic theory; in almost any model, taxes distort the economy (except for things like carbon taxes), so if you cut taxes it should make the economy more efficient, thus increasing growth at least temporarily. The idea that deregulation boosts growth was more of an article of faith — since “regulation” means a ton of different things, there’s no economic model that can capture it in a general sense (actually deregulation really started under Carter, who arguably did more than Reagan). Welfare cuts were partly based on economic theory — means-tested welfare programs are a form of implicit taxation, which theoretically discourages people from working — and part dogma about a “culture of dependence”. As for tight monetary policy — or more accurately, an anti-inflationary bias at the Fed — that was obviously just a response to inflation.

We can argue back and forth about whether the Reagan paradigm ever boosted growth; in fact, I don’t know the answer. The late 80s and 90s were good years for American incomes and the 90s and early 00s were good years for productivity. How much tax cuts and deregulation had to do with that is up for debate, and how much the country benefitted from reduced inflation is also arguable.

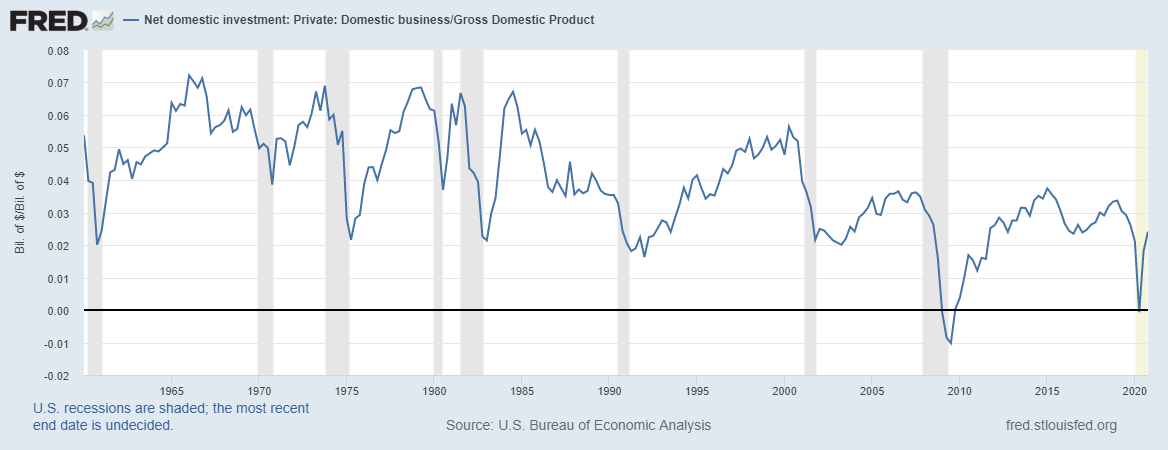

But it’s clear that by the 2000s and 2010s, the Reaganite paradigm wasn’t doing what it was supposed to do. Bush cut taxes for investors, but as Danny Yagan — who is not working in the Biden administration — showed, this didn’t boost business investment at all. In fact, tax cuts in general failed to stem the overall drop in private business investment during 1980-2020:

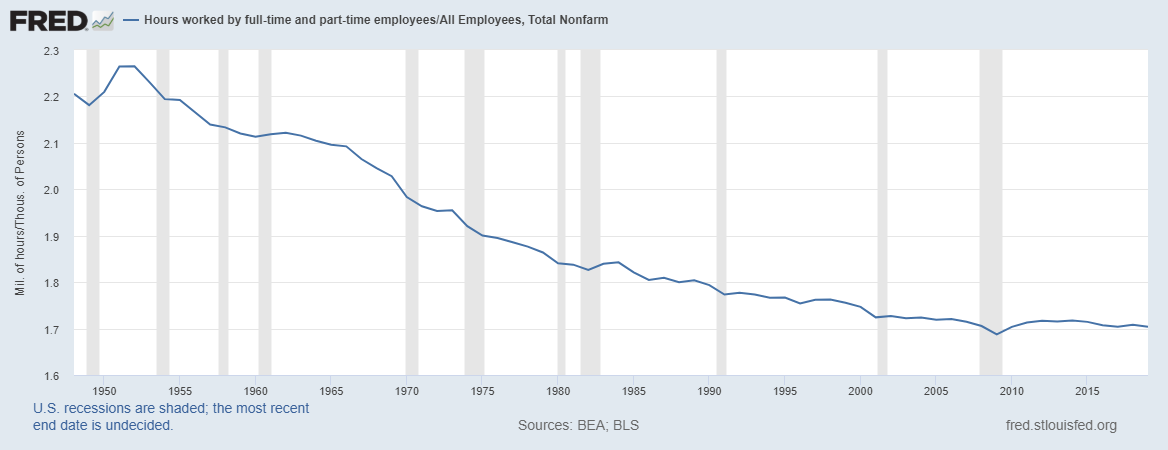

And if income tax cuts made people work more, it certainly isn’t apparent in the aggregate data:

As for productivity, by 2005 the computer boom was over and we were back to slow growth. That came coupled with weak competitiveness, as industrial activity fled to China.

The one really enduring economic success of the Reagan age was that inflation stayed low, but there’s a good argument to be made that in the aftermath of the Great Recession it was too low; if the Fed had allowed inflation to rise more, it might have helped speed the recovery of the 2010s (not just through macroeconomic effects, but by hastening deleveraging).

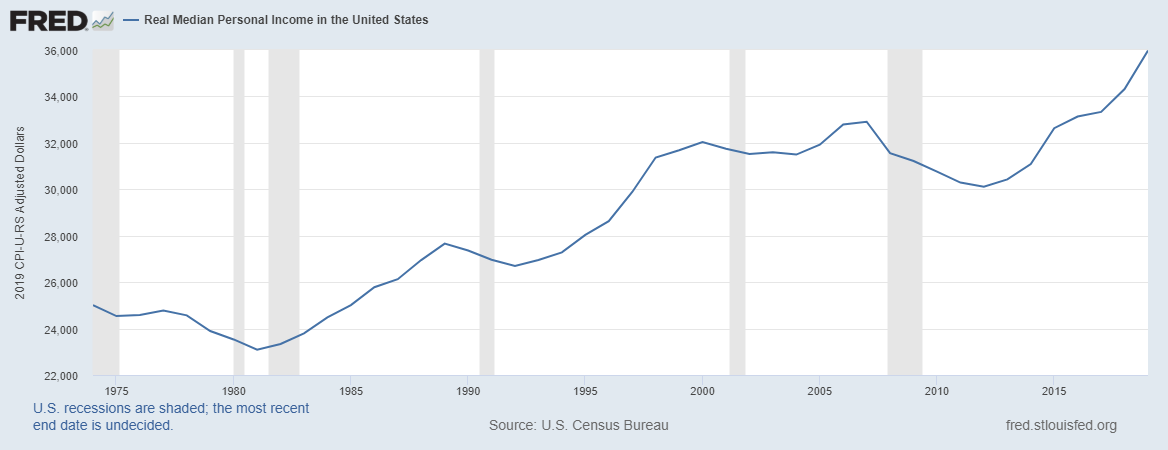

So growth slowed and investment slowed; the Reagan program wasn’t fixing those problems. Meanwhile inequality soared during the years after 1980. Slowing growth and soaring inequality combined to produce a stagnation in median incomes after 2000.

There was an encouraging rise in the late 2010s, but not enough to shake the perception that progress for the average American had stalled. Americans were no longer doing better than their parents. Meanwhile, increased risk from the country’s broken health care system, a rise in evictions, the unemployment and house price declines of the Great Recession, and the vicissitudes of 401(k) programs meant that true standards of living performed even worse than the above graph suggests.

Thus it was clear that the Reagan policy program of tax cuts, deregulation, and welfare cuts wasn’t working. So we needed to come up with a new paradigm. We should have come up with one in the Great Recession, but we didn’t. Instead, it took COVID and the insanity of the Trump administration to push us over the edge and make us realize big changes were needed.

Well, we finally woke up, and here we are. The big changes are Bidenomics.

Cash benefits, care jobs, and investment

The Biden program is multifaceted — it includes things like support for unions, environmental protection, student debt cancellation, immigration, and a bunch of other stuff. But it would be wrong to characterize his program as merely a grab bag of long-time Democratic policy priorities. Three approaches stand out above the maelstrom:

Cash benefits

Care jobs

Investment

Cash benefits were at the center of the COVID relief bill that already passed. In addition to the standard COVID relief items (quasi-universal $1400 checks, special unemployment benefits, housing and medical assistance, etc.) there was a very big program that is officially temporary but which will probably be made permanent: A child allowance. It’s very big in size — $3000 to $3600 per child. There’s no time limit and no work requirement. It’s basically a pilot universal basic income program for families.

The second pillar of Bidenomics is care jobs. The new “infrastructure” bill includes tens of billions of dollars a year for long-term in-home care for disabled and elderly people. Biden has made it explicit since early on that he intends to make caregiving jobs a pillar of his strategy for mass employment.

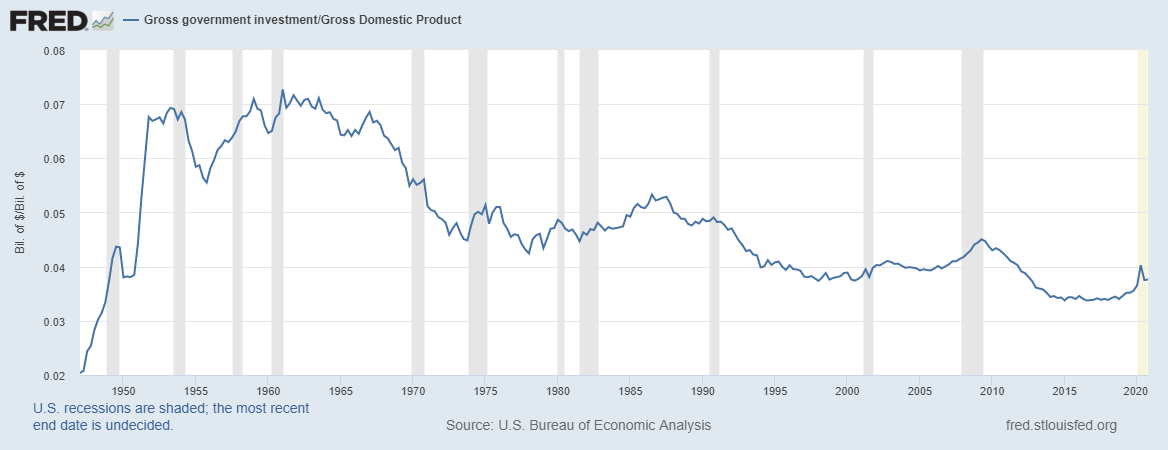

The third pillar of Bidenomics is investment — government investment, and measures to encourage private investment. The former includes tens of billions a year in new research spending, massive construction of new green energy infrastructure like electrical grids and charging stations, retrofits of existing infrastructure (e.g. lead removal from pipes), and repair of existing infrastructure like roads and bridges. This will help restore government investment as a fraction of GDP, which has been drifting downward for decades:

In other words, if private businesses aren’t investing enough, have government plug the hole. But in fact it’s not just about plugging the hole, since things like a modernized electrical grid, a network of charging stations, and lead removal are not things the private sector is likely to do (or do enough of) on its own.

But the administration isn’t relying entirely on direct government action to lift investment — not by a long shot. First of all, infrastructure is a complement to private investment; repair roads, and private businesses will buy vehicles to take advantage of those roads. Government research is also complementary to private investment — there’s a clear pipeline from government-funded labs to privately-funded product innovation and the investment that goes with it. And finally, Biden’s clean electricity standard for the power sector, which will force all U.S. electricity to be carbon-free by 2035, will require huge private investment — in solar, wind, storage, hydro, and nuclear.

Note how little of this investment program relies on indirect investment incentives like capital gains tax cuts or depreciation allowances. Bidenomics doesn’t just turn the knobs and hope that useful investment comes out — it actively directs investment into particular sectors (green energy) and particular activities (science).

Together, these three things — cash benefits, care jobs, and investment — are the pillars of the new approach that’s going to replace Reaganomics. It’s not a direct one-for-one substitute, any more than Reaganomics was a direct repudiation of the New Deal. Instead, while there are some reversals, much of it is orthogonal to the old paradigm, because it’s focused on addressing the problems of today.

Bidenomics: Creating a two-track economy

Before I go on to discuss the justification for this new paradigm, I’d like to sum up all these “pillars” into one more-or-less cohesive vision of where I think Bidenomics is taking us. I think it’s aiming to create a two-track economy — a dynamic, internationally competitive innovation sector, and a domestically focused engine of mass employment and distributed prosperity.

I basically get this notion from Japan. In the 1970s and 1980s, Japan cultivated a world-beating export sector, based around all the companies you’ve heard of (Toyota, Panasonic, etc.). But this was only perhaps 20% of its economy, and the rest was a domestic-focused sector. Although some domestic-focused industries were highly productive (health care!), much of the domestic-focused sector — retail, finance, agriculture, utilities, and a few non-competitive manufacturing industries — was not very productive compared to the U.S. But those sectors did manage to employ a huge number of people; Japan has traditionally had very low unemployment, and that has not changed with the mass entry of women into the workforce since 2012. Japan in many ways built the most effective corporate welfare state in the world.

Biden and his people, I’m sure, do not want the domestic-focused sectors of the economy to be unproductive. But they want those sectors to do the heavy lifting in terms of giving most Americans a job, as they did in Japan. Those domestic sectors include the care economy, where Biden’s team believes much of future employment will come from.

This is partly a story about technology — automation, the end of mass manufacturing employment, etc. With even retail jobs commonly believed to be at risk from new technologies, many people look to care work as the last thing we know we want humans to do. But it’s also a story about globalization, and the shift of global economic activity from the U.S. to Asia. With Asia becoming the workshop of the world, the U.S., with its low population density and relatively remote location, has been forced to become something else — the world’s research park.

The U.S. still has the world’s best research universities, and an enormous concentration of talent from around the world. If we can sustain both those things, we’re well-positioned to continue to be the world’s idea factory; innovation is our comparative advantage. And as long as we do that, we will maintain highly competitive knowledge industries whose specialty is continuous innovation that’s downstream from government science — software, high-tech manufacturing, and pharma/biotech. That’s an assembly line even China may never be able to match.

But while this sector will generate a lot of productivity and a lot of export revenue, it is not going to employ most Americans. Instead, most Americans will work in less competitive, domestically focused sectors — selling houses to each other, pulling each other’s wisdom teeth, preparing each other’s food, bagging each other’s groceries, taking care of each other in their old age. That vast domestic sector will distribute the income generated by the highly competitive knowledge sectors (in fact, this is exactly how an agglomeration model of the economy works, as you can read in Paul Krugman’s book with Masahisa Fujita and Anthony Venables).

And that distribution of income via domestic industries is supplemented by active government redistribution of income — taking a bit of money from the Elon Musks of the world and using it to make sure the mass of people have a claim to food and houses and schools and medical care.

So I think Bidenomics, with its dual focus on research/investment/immigration and care jobs + cash benefits, is an attempt to boost both sectors of the economy at once — to make the export sector more productive while making the domestic sector better at spreading the wealth around. If there’s one unified characterization of the vision Bidenomics is creating for our future, I think that’s it.

Bidenomics and economics research

As with Reaganomics, Bidenomics is based on multiple sources of inspiration — economics research, political imperatives, gut instinct, wishful thinking, and so on. I’ll talk here about the economics part, since that’s the part I know the most about.

The idea that the U.S. needs more research spending probably comes from the work of Paul Romer. Romer was a pioneer of endogenous growth models, which said that the generation of new ideas is key to growth (he won a Nobel for this in 2018). That theory implies that if you spend more on research you get faster growth, and Romer has been vocal in promoting this idea. Also important is the recent research of Bloom et al. and especially of Charles Jones; these researchers suggest that we need to pour more resources into science to keep innovation going. John Van Reenen has done a lot of important work in this area as well; see his call for “innovation policy to restore American prosperity”. See also the work of Daniel Gross and Bhaven Sampat, as well as that of Jonathan Gruber and Simon Johnson, who show how the “spend more money on research” approach worked for us before.

The idea of cash benefits — without work requirements or time cutoffs — owes much to the work of Hilary Hoynes, who keeps a low profile but is incredibly influential. The child allowance is directly from a 2018 paper by Hoynes and Diane Schanzenbach. Heather Boushey, who works in the Biden administration, has been deeply influenced by this literature. Meanwhile, an increasing amount of empirical research is showing that unconditional benefits usually don’t stop people from working. See the famous paper on the Alaska Permanent Fund payouts, by Damon Jones and Ioana Marinescu. And see Marinescu’s 2018 literature review on unconditional benefits, showing that they don’t have much of a deleterious effect on work output, if any. That research basically debunks the “culture of dependency” argument, at least as far as unconditional cash benefits are concerned. Then see Henrik Kleven’s research on the EITC, showing that it was probably the cash benefit aspect, rather than the work incentive, that accomplished most of that program’s much-lauded poverty reduction.

As for Biden’s environmental focus, much of it comes from research outside the field of economics, but Martin Weitzman’s research on the risks of climate change deserves a mention.

This is an impressive body of research. It doesn’t constitute a slam-dunk case — nothing ever will — but it’s a heck of a lot better than a graph on a cocktail napkin.

Bold, persistent experimentation

There are some elements of the Biden plan I didn’t mention, because numerically they’re not very big. One of these is the industrial policy part of the infrastructure bill, which would create a new office in the Commerce department that would actively try to relocate certain industries and their supply chains in the U.S. This aspect of the bill is certain to cause the greatest howls of rage from various people who have decided that industrial policy is bad bad scary-bad.

There is little solid reason to believe that industrial policy is bad bad scary-bad. The case against it has always been far more based in dogma than in evidence; like regulation, industrial policies are so multifarious and complex that it’s not really possible to conclude that it “works” or “doesn’t work”. There is some research suggesting that it’s important — Ricardo Hausmann’s work on economic complexity, various research by Dani Rodrik, a few exploratory papers by the IMF, scattered studies on export subsidies, and so on. This literature is nowhere near conclusive; it doesn’t even agree on what constitutes industrial policy.

But that’s how policy actually works, in real life. There are things that experts think won’t work, based on theoretical grounds; until some bold policy entrepreneur or wild-eyed nutcase actually goes and tries these things, we won’t really know if they work or not.

A great example is the minimum wage. Back in the 1970s, economists almost all believed that minimum wages hurt employment a lot. But they had been getting too high on their own textbook models — when the evidence started rolling in, it turned out that minimum wage was a lot less harmful to employment than Econ 101 had suggested. That prompted people to dust off old theories like monopsony power to explain the newly realized facts. The pipeline here was 1) policy entrepreneurship —> 2) empirical studies —> better theory. Not the other way around.

I expect Bidenomics to contain a lot of stuff like that. Union policy. Subsidies for care jobs. Various new types of infrastructure. Industrial policies. Competitiveness policies vis-a-vis China. And so on. The three basic pillars I described above are the starting point, but they won’t be the whole thing.

That’s going to make a lot of people at the Cato Institute and the Heritage Foundation and the Manhattan Institute and other think tanks that still believe in the old Reagan orthodoxy pull their hair out. It’s going to ruffle the feathers of some economists who still think theory comes first. It’s going to worry older Democratic policy advisors who came up during the Age of Reagan and who still instinctively believe in technocratic knob-turning rather than in directly mucking about in the bowels of the economy.

And that’s OK. It’s good to have a “loyal opposition” that watches and critiques the new paradigm. Sometimes that opposition will be right; like every policy paradigm before it, Bidenomics is going to make some mistakes. That is the price of progress.

The key will be making sure the mistakes don’t get too big.

How Bidenomics could go wrong

Obviously I’m pretty excited about Bidenomics — I don’t agree with everything Biden is doing, but overall this has the general contours of the change I’ve long thought needed to happen. Still, there are some ways the program could fail, and I think it’s important to keep an eye on these as we push ahead. The main ones I can think of are:

1) Debt constraints. Biden has shown a much greater willingness than previous Democratic Presidents to borrow and spend, and the exigencies of COVID caused a big bump in government debt. Some people (mostly online meme warriors) believe there’s no constraint on government borrowing, and others believe there are constraints but we’re nowhere near them. I tend to think it’s not much of a problem right now, but I also recognize that the effects of government debt are not well-understood. If bond investors get nervous and long-term interest rates spike, the Fed will have to decide whether to push those rates down. If it does (perhaps concerned that failing to do so would cause government interest costs to spiral out of control), the result could be accelerating inflation. Or not. I don’t know, since I don’t understand the relationship between monetary policy, fiscal policy, and inflation, and I don’t think anyone yet does. But it bears keeping an eye on.

2) Ruinous costs. The U.S. has an excess cost problem in two big industries — health care (plus child care), and construction. Care work and construction are exactly the two biggest sectors that Biden wants to pump money into. Remember how when we poured all that money into California’s high-speed rail program and it became a giant boondoggle and lots of it got wasted and we didn’t actually get high-speed rail? If that happens with Biden’s new electrical grid etc., we’re in trouble. And if pumping money into long-term care just makes the cost spiral out of control, it will waste labor and add to our overall health cost problem. Either of those outcomes would depress productivity and growth, leaving a smaller pie to be distributed to the nation’s masses. Thus, in order to make sure we actually get bang for our buck, Biden and his team should focus on identifying and mitigating the sources of excess costs in construction and care, rather than just assuming that throwing more money at these things is enough.

There are other dangers, such as higher consumer prices from some of Biden’s less-well-thought-out industrial policies, but I think they’re really second-order compared to these big two. Of the two, I’m much more worried about the second one; excess costs are the big millstone around the neck of the U.S. economy, a looming problem that so far I haven’t seen either Biden or his Republican opposition talk or think much about.

But anyway, I don’t want to end on a negative note. Always remember that America needed a new paradigm. Our old one wasn’t working, and economic research and basic data analysis both suggested clear directions for change. There will be missteps and mistakes on the way to change. Many people will resist the changes, some for better reasons than others. But when it comes time to turn the ship, you must turn the ship, and that is what Biden is doing. Let’s see where it goes.

Whether it occurs in everyday life or while investing, there’s nothing like finding a free dollar. I enjoy it so much, BOGO (buy one get one free) shopping has become one my favorite hobbies.

A few weeks ago, I was “BOGO-ing” at our local grocery store and noticed a BOGO on one of my favorite desserts—chipwiches! For those less familiar with the wide variety of ice cream offerings, a chipwich is made by rolling vanilla ice cream in chocolate chips and placing it between two chocolate chip cookies. Whoever invented the chipwich wasn’t messing around! Considering it’s one of the most delicious and irresistible ice cream treats on the planet, promotions are very rare. My taste buds and wallet were ecstatic!

A box of four chipwiches cost $4.79. Therefore, for every box I bought on BOGO, I was practically picking up a free $5 bill. As much as I wanted to purchase every box, there are some unwritten rules related to BOGO shopping. For instance, it’s considered rude, or poor “BOGO-manship,” to leave an empty shelf for other shoppers. With that in mind, I placed 10 boxes of chipwiches in my shopping cart, leaving plenty of inventory behind. Even though I wanted to buy more, I was very satisfied with my purchase and return on investment!

As soon as I got home, I opened the freezer to deposit my winnings. I couldn’t believe it! To my surprise there were already 10 boxes of chipwiches stacked in the freezer. Earlier in the day, my wife also took advantage of this special BOGO! What an amazing turn of events. Our family went from owning zero chipwiches to holding a full position (20 boxes). Combined we saved $48—an incredible day of BOGO shopping!

My BOGO experience didn’t end there. After spending the next three weeks consuming chipwiches, I returned to the grocery store to hunt from more BOGOs. On my way in, I weighed myself on the store’s scale and was shocked to learn I gained 10 pounds! Apparently, BOGO shopping is not risk-free 😊.

As a BOGO enthusiast, I’m very attuned to changes in the promotional environment. Based on numerous trips to the grocery store and other retail outlets, I’ve noticed a sharp drop in promotions over the past several months. Recent quarterly results and commentary of the businesses on our 300-name possible buy list support my anecdotal observations. With declining inventories and rising costs, companies have been reducing promotions to protect gross margins and receive full price on their limited supply.

Examples of declining promotions are numerous and broad-based. For instance, on their last conference call, Dick’s Sporting Goods (DKS) discussed declining promotions, stating, “The merchandise margin rate expansion was primarily driven by fewer promotions and lower clearance activity [our emphasis].” Lower inventory and supply constraints have also become a common theme. Management explained, “During Q4, we again remain very disciplined in our promotional strategy and cadence as certain categories in the marketplace continue to be supply constrained.” Management also noted inventories were lower than they prefer (down 11%) and stated certain categories of merchandise were not being manufactured sufficiently.

Carter’s (CRI) had similar comments related to inventory and promotions. Management said, “With leaner inventories, we focused our marketing less on promotions and more on the beauty of our product offerings.” With declining inventory, Carter’s has been less promotional in their retail and wholesale channels. Management’s comments related to their wholesale channel were particularly interesting, stating, “Everybody we sell to actually wants more inventory right now, so I think folks are doing a good job managing their business, getting price realization, higher margins, as we’ve all played it tight and conservative given the uncertainties.”

Another business we follow, Big Lots (BIG), also reported fewer promotions, stating, “As our inventory levels were sold through, we were able to navigate through the holiday period with fewer promotions than last year. This reduction in markdowns significantly mitigated the pressure felt from increased spot freight rates and higher supply chain charges we incurred.” Big Lots’ comments were similar to other companies attempting to pass on rising costs.

Other categories in retail, such as branded apparel, also reported lower inventories and higher average prices. In fact, we’re noticing more companies discussing their efforts to receive “full-price.” During Ralph Lauren’s (RL) recent conference call, management said, “Third quarter AUR [average until retail] growth of 19% was above our expectations, with North America and Europe up double-digits and Asia up high single-digits.” Management pointed to significantly lower promotions, targeted price increases, and improved full-price penetration.

Under Armour (AU) is also focusing on selling full-price inventory, saying, “We are working to evolve concepts to drive more profitable formats, particularly for our full-price brand house locations. Our factory house business is about driving greater productivity in store and reducing our promotional levels…”

Skechers (SKX) commented that they too were seeing more full-priced sales, stating, “Gross margin increased over 100 basis points, primarily driven by a favorable mix of international and online sales and an increase in domestic wholesale average selling price, with higher full-price sell through of several of our innovative platforms.”

Nike (NKE) discussed how supply chain shortages are negatively impacting sales, saying, “Starting in late December, container shortages and West Coast port congestion began to increase the transit times of inventory supply by more than three weeks. The result was a lack of available supply, delayed shipments to wholesale partners and lower-than-expected quarterly revenue growth.” Management also commented on its improved gross margins, partially contributing them to “higher full-price product margins.”

Sticking with the footwear theme, Shoe Carnival (SCVL) commented they were also generating higher gross margins, had less inventory, and were providing fewer promotions. Management explained, “Many investors were surprised by the third quarter upside across the space, which was primarily driven by tight inventory management and, from what we’ve heard, of just a broadly less promotional environment.” Regarding future promotions, management said, “I think that’s going to actually pay dividends as we go forward because as you eliminate those promotional time periods, there’s no reason to reinstate them next year.” They even commented on their version of a BOGO, stating, “We ran a promotion that everybody knows as BOGO. Buy one get one half off, that we eliminated many, many weeks of that and we’re continuing to do just that…there’s just no reason to discount that product to the customer as long as they’re willing to pay full-price.” There’s that “full-price” reference again!

We noticed larger retailers are also reporting fewer promotions. In their most recent conference call, Target (TGT) commented on their improving gross margins, saying, “In 2020…a significant tailwind [to gross margins] of about 150 basis points was driven primarily by the favorability of markdowns. A portion of this favorability was related to promotions, but the biggest single factor was a significant decline in clearance markdown rates as demand in seasonal and other clearance sensitive categories far outpaced our expectations.”

Kohl’s (KSS) reported similar trends, stating, “We discussed on our Q3 call the early success we had in optimizing our price and promotional strategies, and we built on this success in Q4. We continue to reduce the number of general promotional offers and stackable offers…” Kohl’s also noted how fewer promotions, pricing, and inventory management have helped offset higher shipping costs.

Macy’s (M) provided commentary on promotions and full-price sales as well, saying, “We’re also going after pricing and promotions. We’re trying to minimize the unnecessary promotions and markdowns and discounts to achieve a higher full-price sell-through, which will help our merchandise margins and ultimately help our gross margins.”

Tempur Sealy International (TPX) discussed pricing and rising input costs on their last conference call, stating, “We have a history of taking price on products to offset industry inflation. Most recently, we have implemented pricing actions during the fourth quarter that have fully mitigated the anticipated input cost headwinds at that time. However, as we’ve entered 2021, input costs have continued to increase beyond our initial expectations. We continue to monitor these costs and expect to take additional pricing actions as needed.”

And finally, Walmart (WMT) had interesting comments related to inflation and how they work with suppliers. Management explains, “We work with suppliers—if we’re getting cost inflation in a product, how do we potentially change the product? How do we make it less expensive? How do we — can you do that and still keep the quality of the product?” In effect, the price may not change, but the product may. As my dad often said about his tools and yard equipment, “They don’t make them like they used to.” I believe he was right! Many products have been altered over the years to offset rising costs.

Rising costs, reduced promotions, and an emphasis on full-price sales are all inflationary. As such, we are curious how the Consumer Price Index (CPI) has been factoring in these trends. Based on the most recent CPI report, apparently it is not! Specifically, the February CPI less food and energy came in at blistering (sarcasm intended) 0.1% with the core rate up 1.3% year over year. While we don’t spend much time analyzing government economic data, we believe the CPI has some catching up to do!

The current operating environment reminds us of 2018 when businesses were also reporting rising costs and pricing power. Ultimately, the CPI caught up with what we were observing in the real world, rising to 2.9% by June 2018.

Unlike today, in 2018, the Federal Reserve was raising the fed funds rate. Interest rates across the yield curve responded, with the 2-Year Treasury yield increasing from 1.92% on January 2, 2018 to 2.98% on November 8, 2018. Rising interest rates were eventually too much for the stock market to withstand. Small cap stocks fell approximately 25% from their 2018 highs to their lows in December.

Without the tailwind of a rising stock market, the economy stalled, commodity prices declined, and the December 2018 CPI fell back below 2%.

Similar to 2018, we expect the inflationary pressures being reported by businesses to eventually find their way into the government data. Also similar to 2018, we expect rising inflation will place upward pressure on interest rates. Now here is where it gets tricky. Do rising interest rates cause the stock market, economic growth, and inflation to decline like the end of 2018? Or do rising rates cause the Federal Reserve to increase quantitative easing (QE) in an effort to manage the yield curve and keep asset prices inflated? Based on how the Fed responded in 2018 to falling stock prices, we believe they’ll attempt to maintain inflated asset prices.

Assuming we are correct, we do not believe the Fed’s efforts to protect asset prices will necessarily succeed. By artificially suppressing interest rates along the entire yield curve, we believe current inflationary trends are less likely to self-correct and could possibly worsen. In effect, the more money the Fed creates to suppress interest rates and maintain asset inflation, the greater the risk of losing control of real-world inflation and its perceived control of asset prices. Put simply, we believe a policy of endless quantitative easing and a dismissive attitude towards inflation are incompatible.

While we’re fascinated by the box the Federal Reserve has placed itself in, we feel no sense of urgency to act or speculate on how the Fed will respond. As portfolio managers with an objective of generating attractive absolute returns over a full market cycle, we are in the fortunate position to not have to “play the game” and remain fully invested. In our opinion, small cap valuations have never been more expensive and risks never so underappreciated. Getting aggressive here makes absolutely no sense to us. However, waiting for the return of volatility and opportunity does.

We believe our patience will pay regardless of how the Federal Reserve responds to rising inflation. If the Fed acts to fight inflation, we’d expect interest rates to rise, putting pressure on sky-high equity valuations. If the Fed dismisses inflation, its credibility will suffer, risking a revolt in the bond and currency markets. Either way, we expect the Fed’s inflation dilemma will likely lead to an increase in volatility, and in our opinion, opportunity. Given the current backdrop, we like our patient positioning, appreciate our objective more than ever, and believe we are well prepared for future investment BOGOs!

I am not a gunslinger when it comes to investment because I have have learned risk management hard way (loosing my first year salary in the 200 Tech boom). Bill blain has painted a kind of doomsday picture below and I think it is worth reading as we are dealing with a very complacent market.

By Bill plain via morning porridge

The supreme art of war is to subdue the enemy without fighting.”

You could not make this up; an unimaginably complex WW3 Techno-thriller unfolding as markets stumble and global supply chains hover on the edge of anarchy. On the other hand, maybe that’s just the way it was planned.

I am not one for conspiracy theories. But… this morning… If I was a writer of trashy global-techno-World War 3 pulp fiction, and proposed the following scenario where the global economy lurches into an unprecedented period of instability – nobody would believe me:

1) Global Supply Chains, weakened and struggling after a year of global pandemic, plus a growing shortage of microchips holding back multiple industrial sectors, are plunged into new crisis by a puff of wind causing a box-ship to skite sideways and block the Suez Canal, trapping East-West Trade.

2) Unstable and over-priced Global Markets are spooked into a frenzy late on a quiet Friday night by the largest margin calls ever ($20 bln plus) as an Asian “family office” dumps billions of dollars of stock into the market. Collateral damage spreads, as other financial firms, (inevitably including Credit Suisse (Switzerland’s very own Deutsche Bank), and Nomura), announce material losses.

3) As global central banks struggle to restore real growth, while trying to hold interest rates low and support commerce, and acutely conscious of how a market crash could crush global confidence – things suddenly get more difficult as confidence in equity valuations takes a massive knock.

4) Geopolitical stability wobbles after China lashes back at US criticism in Alaska, and then surprises Europe with sanctions and push back on trade deal – when many has expected China to attempt to reach out to Europe – even as it reaches out to pariah states including Iran, Myanmar and Turkey.

5) Rumours abound of imminent China action to seize Taiwan – and the potential impotence of US fleets from the Gulf to the Pacific are targeted by long range Chinese carrier-killer missiles – further destabilising markets.

6) Cyber-attacks across western economies, first uncovered at Solar Wind, but possibly undiscovered elsewhere, raise questions as to how much the West’s digital and financial infrastructure has been compromised.

What happens next?

On the basis I am an optimist, and things are never as bad as we fear, I think it all settles. Who knows? But I suspect one thing is going to become very apparent. China has crossed the Rubicon and will now longer be a rule taker. The rules have changed. China has demands.

What’s different in the above scenario is that it doesn’t necessarily lead to a hot-war. The Beijing leadership see benefit in trade, engagement and the global economy to deliver its pact of prosperity to the Chinese population. They may conclude China’s done enough to achieve its’ strategic economic objectives; parity with the west, and economic primacy across Asia. Whether the mood turns hot or cold rather depends on how the West responds to the apparent nullification of the USA’s military hegemony achieved by China’s new missile technologies.

These new missiles are a known unknown. The latest versions of the D-26 Carrier-Killer are apparently based on the Tibetan Plateau and can take out US Carriers from the Gult to New Zealand – making any defence of Taiwan look an extremely risky call. Sending the UK’s carrier strike group into the region later this year looks… challenging.

And suddenly you are wide awake and wondering just how crazy this suddenly got…..

* * *

On Sunday I spoke with one of my old racing yacht crew who is now doing extremely well in Global Shipping. I asked if there was anything we were not being told, or what the real story of the ship blocking the Suez was. He was cagey but told me.. “If you need Garden Furniture, buy it today.”

This morning it looks like the Suez has been uncorked – the boat has been shifted – but I was asking because I reckon slowing global trade by sending it the long way round Africa isn’t just about miles and time – it’s finding the ships capable and seaworthy for the longer trip, and bunkering them accordingly. It’s not just a matter of a longer voyage. Suddenly everyone wants Air Freighters.

The key-thing is what happened on the Suez demonstrates is just how easy it would be to block the bottlenecks of global trade. Everything from consumer tat to chips would be stressed.

After Archegos Capital, the family office of tiger-cub and convicted insider Bill Hwang was forced to sell more than $20 bln of stocks in a series of block trades on Friday, this morning – its looking likely to be a risk-off day. Block equity-trades stemming from the margin-calls on Archegos will have sent the market’s spidey senses a’tingle. Who is next?

There will be flows back into the relative safety and comfort of bonds – even if they do yield nothing. In bonds there is truth, and I suspect today will confirm it’s all about fear. Over the past 10-years artificially low rates have eroded the relationship – telling investors low rates are a reason to take risk. Its low rates that have supported today’s frankly insane stock market valuations. Risk is very real again.

While Gold might be on the agenda, I’m not so sure about Bitcoin. The Chinese have made it quite clear they will digitise the Yuan.

Today’s moves will likely also reflect a Q1 rebalancing of bonds vs equities holdings– which have been distorted by the relative yields on asset classes. But I suspect it will just be the start of a trend. Just how big has unregulated leverage in the shadow banking system of investment firms become? How could it unravel impact markets? Or maybe it will be illiquidity as the next duck tumbles and no one is prepared to buy?

Today won’t be much fun for anxious central bankers.

It’s not going to be much fun for the politicians either as they look realise just how vulnerable the West is to a new economic shock, even as we’re still being floored by the self-inflicted economic harm of the Pandemic.

Western Economies are dependent on long exterior global supply chains to fuel demand for more and more consumer goods. We’ve become comfortable to click and deliver being satisfied from China. Stuck in lockdown we’ve heard disembodied voices warning of economic catastrophe, but we’ve been cocooned from the economic reality, relying on governments assurances they can prop up the Covid ravaged economy with subsidy and furloughs. Destabilise our supply lines, and the threat is a run on everything – potentially making last year’s pandemic panic look tame.

Meanwhile, dissent is all the rage across the west, whether it’s the right-wing complaining about their civil liberties, smaller nations demanding independence, or gender and race issues coming to the fore and exposing the inequality and division of society. All of these divisions are fed on a rich oxygen-mix of social media, and targeted with fake news aiming to deepen division. Everyone has a cause, and everyone believes what they want to, but nobody listens. Western society has never been this unstable, polarised and disunited.

Chalk up another win to China.

China’s leaders are satisfied. Their position is secure. China’s economy is exposed to supply chains, but is based on interior lines (and pretty much brand new infrastructure) – better able to weather and internalise a global trade-storm. Its’ society is homogenous and willing to buy the greater prosperity/state control trade off. National pride hasn’t been compromised by the pernicious effects of Wokery.

The economy of the West is bought into the promises of technological change and addressing the environment. Markets are soaring on the back of expectations of increased technological adoption, with a few successes spurring thousands of highly speculative copycats – witness the insane boom in SPACs. But the reality is economies have become increasingly bureaucratic, stultified by regulation, and held back by political gridlock and polarisation. Infrastructure is old and tired. Key skills and capacities have been lost.

Let me present a tiny example – speciality steels. Without speciality steels for the fine work of tech, the economy will ultimately wither and die. We are now entirely beholden to external steel. The UK government put plans to restore mining the key element of steel in the UK on hold. Without metallurgical coal – you can’t make steel. Fact. The UK prefers its steel to be made in China with Australian met. coal so it can say it’s tough on cutting carbon. The facts are simple – make the steel here, less carbon miles and more high quality jobs.. Or…

But, the risks are not just in terms of physical supply chains. The digital economy is even more important and potentially even less protected. We’ve largely remained unaware of just how vulnerable we are. The cyber-attacks on SolarWinds last year may reveal the Trojan Horse is already in the city.

The degree of interconnectedness in the global economy is extraordinary. All the major financial institutions used SolarWinds’ Orion platform. The hackers got into SolarWinds and were able to install malicious code into software updates, accessing thousands of clients’ confidential information. We still have no idea how deep the hack goes. Increasingly companies release its not a matter of understanding their own vulnerability, but the vulnerability of all their suppliers, and hence, the whole digital supply chain.

So… what happens next?

Do the Chinese explode a couple of massive nuclear missiles in space to take down global positioning, communications and spy satellites with an EMP pulse, alongside a simultaneous cyber-attack to crash the Western Financial System, plunging us into limbo? How would Central Banks cope with the resultant market meltdown? What would happen if even a small part of the global payments system crashed?

Sometimes it easier to not over think it.. and just hope it was just coincidence… hope is never a strategy.

For the past few years, I have been critical of the Ponzi Sector. To me, these are businesses that sell a dollar for 80 cents and hope to make it up in volume. Just because Amazon (AMZN – USA) ran at a loss early on, doesn’t mean that all businesses will inflect at scale. In fact, many of the Ponzi Sector companies seem to have declining economics at scale—largely the result of intense competition with other Ponzi companies who also have negligible costs of capital.

I recently wrote about how interest rates are on the rise. If capital will have a cost to it, I suspect that the funding shuts off to the Ponzi Sector—buying unprofitable revenue growth becomes less attractive if you have other options. Besides, when you can no longer use presumed negative interest rates in your DCF, these businesses have no value. I believe the top is now finally in for the Ponzi Sector and a multi-year sector rotation is starting. However, interest rates are only a small piece of the puzzle.

Conventional wisdom says that the internet bubble blew up due to increasing interest rates. This may partly be true, but bubbles are irrational—rates shouldn’t matter—it is the psychology that matters. I believe two primary forces were at play that finally broke the internet bubble; equity supply and taxes. Look at a deal calendar from the second half of 1999. The number of speculative IPOs went exponential. Most IPOs unlock and allow restricted shareholders to sell roughly 180 days from the IPO. Is it any surprise that things got wobbly in March of 2020 and then collapsed in the months after that? Line up the un-lock window with the IPOs. It was a crescendo of supply—even excluding stock option exercises and secondary offerings. The supply simply overwhelmed the number of crazed retail investors buying worthless internet schemes. Back in 2000, I used to joke that in a scenario where a company wanted to raise equity capital, but insiders wanted to sell, they’d both dump shares on the market—but the insiders would get out first. What do you think that did to share prices as both parties fought for the few available bids?

However, the proximate cause of the internet bubble’s collapse was when people got their tax bills in March and had to sell stocks to pay their taxes in April. What’s the scariest thing in finance? It’s when you owe a fixed tax bill from the prior year, yet your portfolio starts declining. You start selling fast to stop the mismatch. Trust me, I’ve been there. Tax time is pushed back a bit this year, but it is coming.

Admittedly, All 3 Are Full Of Shit…

I bring this all up, because the SPAC market is in the process of detonating and it will take the Ponzi Sector with it. Let’s look back at the internet bubble. A VC firm would IPO 4 million shares at $20, the stock would open at $50 and end the day at $100. Everyone chased it to get in. Then the brokers would upgrade it and the CEO would go on TV. With a 4 million share float, it was easy to manipulate the shares higher. Often, the newly IPO’d company would level out well north of $100 a few weeks later. It was a virtuous cycle and everyone played the game. What was left unsaid was that there were another 46 million shares held by management and VCs and these shares would hit the market 180 days later. At first, the market absorbed the new supply so no one showed concern—then the market choked. I wrote about this when talking about the QS unlock. This process is about to repeat, but now with the odd nuances of SPACs.

A typical SPAC deal involves a few hundred million dollars raised for the SPAC trust—this is the only real float. Then a few hundred million more is raised for the PIPE—these guys are buying at $10 because they plan to flip for a gain as soon as the registration statement becomes effective—which is often a few weeks after the deal closes. When a company merges with a SPAC, billions in newly printed shares are given to the former owners—those shares start to unlock a few months later in various tranches. Finally, the promoters behind the SPAC get to sell. When you look at a pre-merger deal trading at a big premium to the $10 trust value, you’re looking at an iceberg. There might be ten or twenty restricted shares for every free trading share—all of these guys desperately want out. It’s a game theory exercise—how do you find enough bag-holders without destroying the price? Hence, part of why the current price is determined by an artificially restricted float and the unlocks come in tranches. As restricted shares come unlocked, the promoters lose control of the float and the house of cards collapses.

Part of the hilarity of SPACs is that the promoters claim to be aligned with shareholders because they exit last in terms of unlock tranches. What’s left unsaid is that their shares have almost a zero-cost basis—hence when they sell out at well under $10, it’s still all profit. Meanwhile the acquired company insiders often have an even lower cost basis because they founded the company at a negligible cost, there were bidding wars by various SPACs which drove the valuations to nosebleed levels and the acquisition targets are often mostly fake anyway.

When there were only a few high-profile SPACs, this supply could be absorbed—very much like 1999 with internet IPOs. This made people unconcerned about the supply deluge. Now we’re starting to enter the teeth of the unlock window from 2020 vintage SPACs. There are literally tens of billions a week in stock flooding the market—except there’s no natural shareholder base for these things. There are only so many retail punters who wake up and want to buy a fake “green” company with no revenue and no path to revenue—much less profits. When everyone is making money in ESG themed frauds, it draws fresh capital into the bubble and helps inflate things. When the losses start stacking up, capital leaves—yet there are still hundreds of billions of dollars in SPAC shares waiting to be unlocked and dumped. Remember how their cost basis is effectively zero? The insiders and promoters literally do not care what price they sell at. It is the internet bubble all over again.

You may wonder how the SPAC bubble will infest the rest of the Ponzi Sector. It comes down to collateral and shareholder bases. On the collateral side, much of the Ponzi Sector bubble is built on leverage. That could be margin debt or YOLO call options, but it’s all leverage. As asset values decline, brokers will force punters to de-lever. This will lead to waves of selling, leading to more forced selling. As for YOLO call options? They’re not exactly firm bedrock when it comes to a bubble. The SPACs and the Ponzi Sector are all tied together, because they all have the same shareholder base. As these owners take losses, they’ll be forced to sell “best in class” Ponzis like Tesla (TSLAQ – USA).

Back in 1999, there were various firms that enabled the internet bubble. They had handshake agreements that they’d be given IPO allocations, on the understanding that they wouldn’t sell—in fact, they frequently bought more in the open market, often at many times the IPO price. This allowed VC firms to tighten up already tight floats and manipulate shares higher. As these firms outperformed, they had inflows, allowing them to continue buying the same companies and pushing shares higher—leading to more inflows. It was a virtuous cycle and many firms worked together as wolf-packs in the same names. When redemptions came, these firms were forced to sell and the process unwound—except it was unusually speedy to the downside as the share prices were artificially propped up.

I have my sights on a certain ETF for this cycle. Go through ARK Innovation ETF’s (ARKK – USA) position list, go through all the quasi-affiliated firms that have copied this position list. All these firms have surprising concentrations in the same names. When it comes tumbling down, you don’t want to own any of these positions—especially the ones where ARKK owns more than 10% of the shares. You won’t want to own positions that are owned by people who own ARKK type positions as they’ll be forced sellers too. You want to be as far away from the Ponzi Sector ecosystem as possible.

I don’t know when it’s going to blow, but if I’m right that the top is in, the deluge isn’t too far off. Bubbles are highly unstable—if they’re not inflating, they’re usually bursting—there isn’t really a middle option. I think the past few weeks are more than a simple pullback—the losses from the SPAC bubble are going to dent the Ponzi Sector psychology. With this in mind, I took my long book way down over the past few weeks (including my GameStop (GME – USA) straddle for a nice score). That said, I don’t have shorts because this is still “Project Zimbabwe.” If I’m wrong, so be it. I’ll do just fine on my Event-Driven book. Besides, 2021 has already been a pretty spectacular year for me.

Turning to Grayscale Bitcoin Trust (GBTC – USA), it now trades at a surprising discount to NAV—partly due to the shareholder base’s cross-ownership of other Ponzis. I had told myself that I’d hold GBTC through the sort of shake-outs that Bitcoin is famous for. However, this week when I went through my position sheets, I asked myself if I really needed this much exposure to a Ponzi Scheme, after repeatedly reminding myself that the Ponzi Sector is detonating. As a result, I booked a bit more than half of my GBTC exposure—taking all of my cost basis out and then some. I’m not going to say that my dismount in the mid-$40s was graceful—I wish I had sold it with a $5 handle, but I’m up 4-fold in 8 months and it still feels like quite the victory. For now, I intend to keep the rest of the position, though I’m moving my stop up once again. Will Bitcoin get caught in the downdraft? Who knows; I don’t need a position limit while I find out.

But Kuppy, what about “Project Zimbabwe?” Won’t the Ponzi Sector go up with everything else? My good friend, Kevin Muir, over at The MacroTourist (if you aren’t subscribed, you are missing out), likes to say that we’re “experiencing a period of rolling bubbles.” History says that once a bubble pops it rarely re-inflates. I believe that the Ponzi Sector bubble is now past the apex. With losses stacking up, the bubble psychology will break and people will start looking at things rationally again. How does this square with my “Project Zimbabwe” paradigm? It squares perfectly. We will have a rotation and some other asset class will bubble up next. I suspect it is one where increased cost of capital and massive government interference shuts off supply growth. Could inflation beneficiaries be next? I want exposure where the puck is going, not where it’s overstayed its welcome for far too long. On this pullback, that is where my focus will be.

Today, we will be exploring the fundamentals of Uranium investing. Just like many other commodities, Uranium has been left for dead in the past 10 years. It is about to come back on the mainstream investment shows and portfolios and soon be the town’s talk. Therefore, here is my top reasons to invests in Uranium:

Supply & Demand imbalance

Consistent lack of Capex investment

Price of uranium

As you can see, I am a simple man. I like an investment thesis that is easy to understand.Subscribe

Supply Depletion

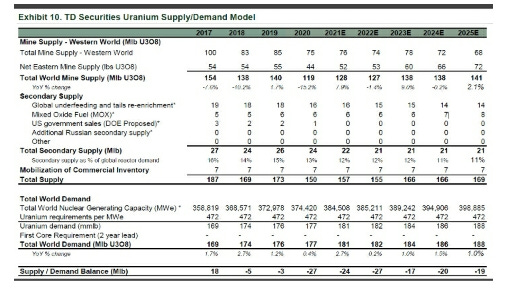

This is not your typical “peak oil” supply depletion. This is a factual, quantifiable, and auditable fact. The below table, provided by TD securities, shows us all the current and future uranium supply by their sources. The interesting fact is the total western mine supply keeps declining year after year. I like the below table because it goes into a lot of detail about the different sources of supply.

Uranium bulls were already hyped up about this thesis 3 years ago. The big unknown in the last couple of years highlighted by Mike Alkin from the hedge fund Sachem Cove, the only hedge fund focused on Uranium investing, was the secondary supply from, as an example, Japan. After the Fukushima accident, they were selling the uranium they did not need from the excess inventory they had contracted because they decommissioned nuclear reactors. This, however, is/will soon be coming to an end, and all we will be left with will be a primary supply which is even easier to forecast given that only a few mines in the world produce uranium. If you really want to get deep into the subject, I suggest the following interviews. It is 2 hours long; therefore, that is if you really want to get deep into the subject! I could spend a full article on the secondary supply dynamics. Is that something you would like to understand?

Covid 19

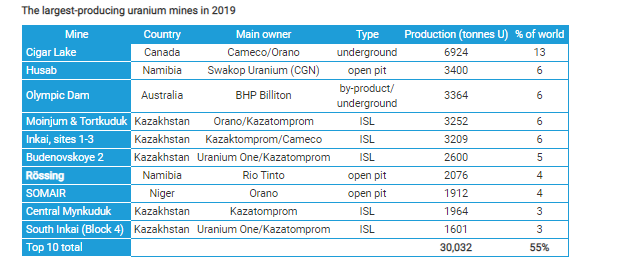

Since 2020, we have further eroded the supply of current mines. As you can see from the below table, the uranium-producing companies are very concentrated. Cameco and Kazatomprom, the biggest producers globally, have both decided to leave some of their production mines offline for the foreseeable future. Cameco, in 2018, put their McArthur River mine in care and maintenance. They said that the closure was due to Uranium’s ongoing low prices and would bring it back in production only when the price would justify it. Kazatomprom, the biggest producer in the world, in their latest earnings call, mentioned that they were most probably going to have to buy uranium on the spot market, meaning at the open market, instead of depleting their mines. In my opinion, this strategy is fantastic news to drive the price up in the future as it will deplete all the secondary supply and force future prices to increase as it squeezes the current supply even more. Looking further to the list of major uranium producers, BHP, last year, decided to stop expanding their Olympic dam mine. Not including this list is the Cominak mine from Orano that will stop its production in March this year.

Demand Imbalance

As mentioned last week, the current total number of nuclear reactors is 440. We will add another 50 reactors that are either being built or contracted by 2025. China, by 2030 will be consuming the total current production of Uranium alone. The big question will be, where will the future supply come from? Twofold, first, mines that are currently on care and maintenance. What the hell does that mean? Mines that are uneconomic at the current price of the uranium but would produce at higher prices. Paladin and Cameco have such mines. The issue of having to restart mines is that it is costly. I feel I repeat myself as we move from one commodity to another, but you cannot simply turn a switch on and off to produce more Uranium/silver/gold/copper/lithium/rhodium and so forth. The projected costs to restart the Paladin mine is 81 million dollars for their Namibian mine.

On the above graph, you can see that the returning production will cover some of the supply/demand imbalance. As we move into the latter part of the decade, however, we will need a secondary inventory source, which will be through new mines productions. John Quakes provided the above graph.

Lack of Investments

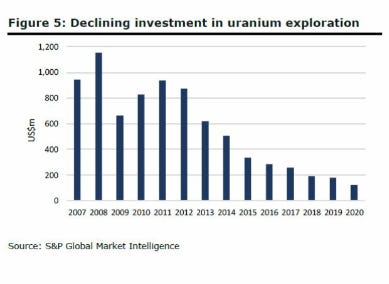

The countercyclical nature of commodities investment is usually a simple path to follow. A period of high prices leads to a lot of investment in future productions. This, in turn, will lead to higher production and, in the absence of higher consumption, will lead to lower prices of the said commodity because of the excess supply. If allowed to persist for a prolonged period of time, this situation will lead to a shortage of supply, which is exactly what has happened since Fukushima. So what is the current state of Capital investments in Uranium, you ask? In the chart below, we can see that we are between 20% to 25% of what we used to invest 10 years ago. Given the shrinking supply and the lack of investment to bring new mines to life, this will lead to higher uranium prices. In fact, I think we will see a sustained higher price of Uranium for a much longer period of time following this period of under-investment given the forecasted rising demand in the next 20 years.

The price of Uranium

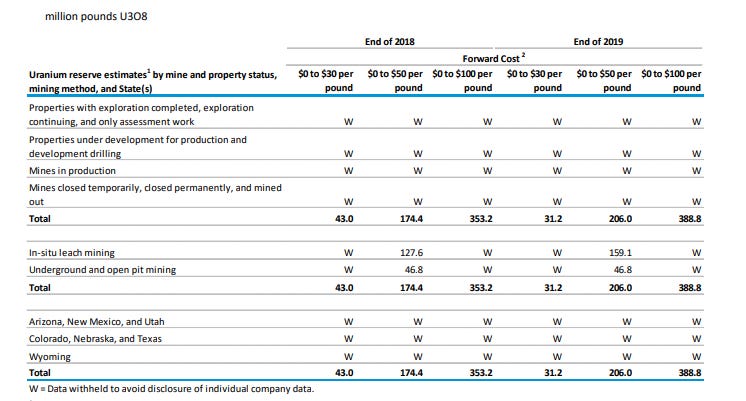

The price of uranium has been quite stable since 2015, staying below 30$/lbs. Unfortunately, only the best and most productive mines can make a profit with these prices. Looking at the below table, although this is the USA only, it gives you a great understanding of what supply can be mined by price point. Under 30/lbs, there is very little supply that can be mined profitably, as you can see.

Uranium Price chart

If you look at the new projects from future mines for companies that have confirmed resources in the ground, you find that companies will be profitable and able to operate mines with a constant and long-term minimum price of uranium 50/lbs. One of the reasons why the price needs to be significantly higher than the current 30$/lbs is that these companies will need to spend a minimum of 5 years on building a mine and potentially spending upwards of 1 billion dollars in CAPEX. Let pause here for a second. If this was your own money, would you sign contracts with builders, contractors, engage with the governments for environmental studies, knowing that you would ultimately spend 1 billion dollars if you cannot, with a reasonable level of certainty, predict that you would be making a profit? Furthermore, utilities who buy the uranium are price takers and have inelastic price demand for the fuel. Why is that? Utilities, which are usually government entities or government allowed monopolies need to keep the lights on, regardless of the price they pay for the commodity. From last week’s article, we know that nuclear reactors produce 10% of the world’s electricity, and sometimes close to 30% of a country’s total electricity is provided by nuclear.

Summary

Unless another accident like Fukushima happens in the near term, I think that Uranium equities will end up being the best-performing asset of 2020 to 2030 on a risk-adjusted basis. Before you castrate me for not mentioning Bitcoin, I still think we will see another 10x to maybe 20x from the current price. Some of the junior equities will be able to achieve 10x to 50x in the next 10 years and repeat some of the actions that we saw in the late 2000’s bull market. Of course, some start-ups could IPO and give you 10000% return over the next 10 years. A pharma could cure cancer and do the same. Uranium’s difference is that even the biggest and best in class, blue-chip companies with solid management, years of experience will experience an easy 10x increase in market cap. The smaller producers will probably experience a 20x increase in market cap. Simultaneously, the grass-root explorer and project generator might repeat the Paladin story that went from 0.04$ a share all the way up to 10$ per share for a whooping 250x times your money.

It’s no secret that money has poured into passive equity vehicles as investors seek low fees above all else. To date, that has worked out just fine since equity indexes have compounded their returns at acceptable, if not above average, rates of returns. But, the world is different now than it was 10 years ago, and the low-cost advantage of passive investing may now be outweighed by its risks.

In this quick post we’ll address three risks to passive investing that together suggest the riskiness of this strategy may well be the highest it has ever been.

Taking the S&P 500 as an example, the weighting toward tech-like stocks introduces significant concentration risk. Indeed, the weighting of the technology sector + Alphabet, Amazon, Facebook, & Tesla is a whopping 38% of the total S&P 500. In other words, 38% of passive investors’ exposure is to one risk factor. That’s a lot of chips to put on one bet.

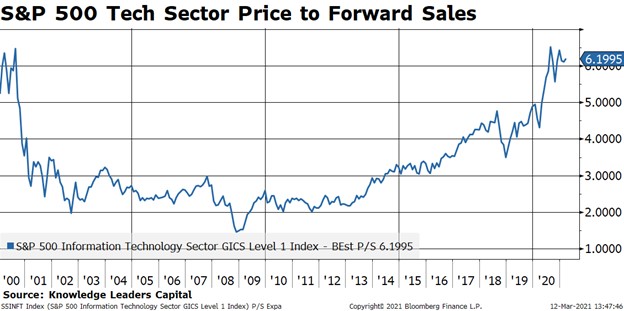

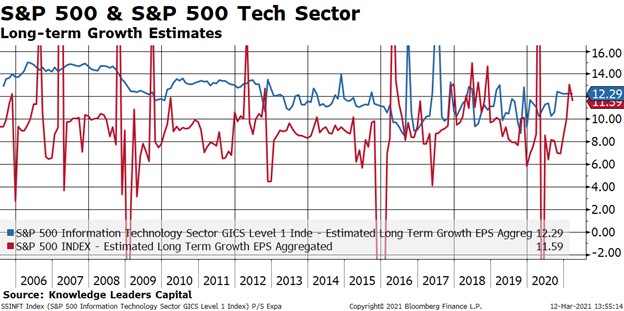

The valuation for the tech-like stocks is out of control. Taking just the tech sector as an example, it’s trading at 6.2x next year’s sales. This valuation extreme was only eclipsed (barely) in the late stages of the tech bubble. Since valuations inform prospective returns, passive investors in the S&P 500 are basically locking in a below average rate of return since 38% of their portfolio is invested in highly valued stocks. But…the growth. Yes, valuations always need to be calibrated against prospective growth rates. However, tech sector growth rates have been trending down since 2006. For the first time in a very long while, S&P 500 long-term growth is expected to be on par with tech sector growth.

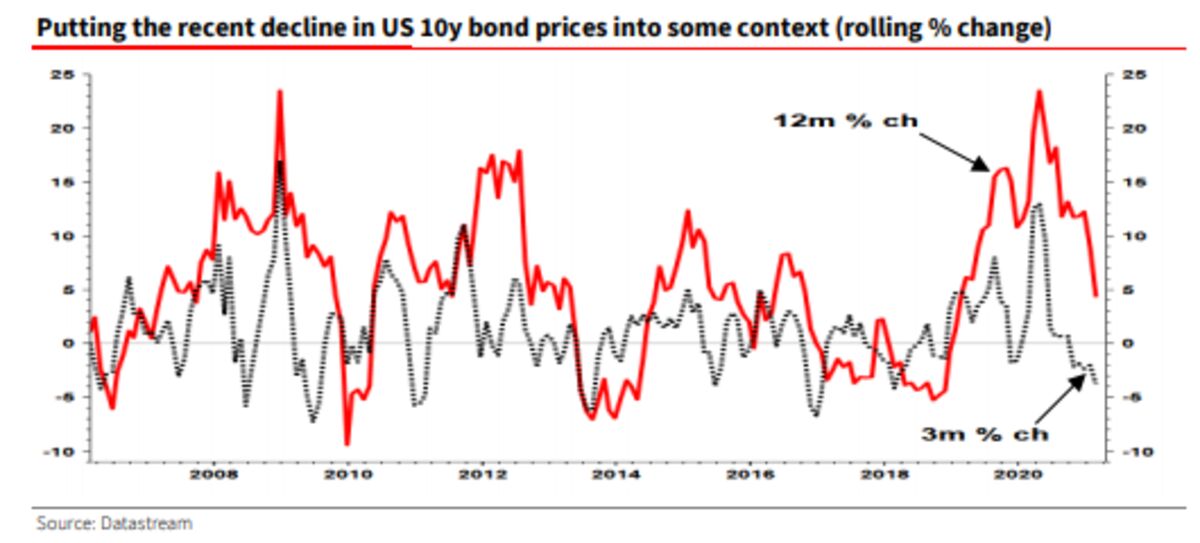

Tech valuations are highly related the level of long-term interest rates. Much of the “value” in tech stocks is the stream of cash flows that is expected many years from now, which is similar to the payoff profile of a long-term bond. When interest rates rise, the present value of those future cash flows (for bonds and high growth stocks) goes down. Since we’re in an environment in which very long-term interest rates are more likely to rise than fall, this will generally put pressure on tech valuations.

This is kind of hat trick for passive investors. Passive portfolios are highly concentrated in stocks with overlapping risk exposures, the valuation of those stocks is in the 99th percentile, and there is a catalyst for those valuations to compress. Combined, these things add up to a below average rate of return for passive portfolios, even if the average stock does just fine. But the fees are low…

As of 12/31/2021, Alphabet, Amazon and Facebook were held in a Knowledge Leaders Strategy. Tesla was not.

I have been reading Dylan Grice since his socgen days and this interview just delivered a reality check for every investor.

I have highlighted the important portions in the interview if you are short of time.

Dylan Grice, co-founder of Calderwood Capital, sees frothiness all over today’s financial markets. He thinks valuations in hot sectors like electric vehicles are insane, but he sees investment opportunities in areas like uranium and oil.

Dylan Grice is concerned. The co-founder of Calderwood Capital and former strategist at Société Générale sees smaller and larger bubbles emerging all over financial markets. «There are clear signs of excess», says the author of the monthly «Popular Delusions» report.

Still, Grice characterizes his current investment stance as reluctantly bullish: «Central banks will overcook the economy, everything is set for a few years of overstimulation in monetary and fiscal policy.» This won’t end well, he adds, but until then the equity market boom could continue.

In an in-depth conversation with The Market NZZ, Grice explains how investors could navigate the current environment and where attractive investment opportunities still exist. Grice is particularly bullish on the uranium and oil & gas sectors.

Mr. Grice, in your latest Popular Delusions report, you call yourself «reluctantly bullish». Why?

I like to feel that if I’m underwriting risk, I’m getting well paid for it. And right now I don’t think that’s the case. It doesn’t really matter which segment of the market you look at, risk premia are almost universally tight. Risk premia are back to where they were pre-Covid, in some cases even tighter, and they were already unattractive before.

So if you put on your value investor hat, you can’t see any value?

Generally not. There isn’t any broad value except for some specific pockets. Back in March of last year, we were very bullish. To be clear, that was not because we thought we could identify the bottom, but because we could see panic and dislocation. It is a core belief of mine that you have to take the other side of a market that is in panic selling mode. That’s when you have to be buying.

Many investors were surprised by the strong recovery that has taken place since. What did you make of that?

We remained bullish in the months after March, because you could see that everyone hated the rally. Twitter was full of people who were angry. Angry that the Fed had injected money into markets, angry that the Fed had created all sorts of distortions. All of these arguments, which I have quite some sympathy for, were irrelevant to the investment case. As an investor you must not blind yourself with what you think policy makers should do. You must look at what policy makers are doing, and instead of making a moral judgement on whether that’s good or bad, you have to understand what the consequences of those policy actions are. This anger clouded the judgement of many investors. So, I was happy to be bullish throughout this period.

What has changed now?

My reluctance is because I feel it’s all incredibly frothy now. There are signs of excess, and yet we are still in the middle of a pandemic, we haven’t even started the economic recovery yet.

What signs of excess?

I think that this GameStop fiasco is kind of an indication of wider problems. Also when I look at the exuberance in hot sectors like electric vehicles, which investors seem to forget is a very capital intensive business. Valuations there are crazy, this is getting demonstrably insane. I would completely avoid that. This is not the kind of market which a fundamentally value driven investor should be bullish of.

Is the boom in SPAC issues also a sign of excess to you?

I don’t have an opinion on the SPAC market, I just don’t know enough about it. I know some very smart investors who are investing in it. But I can also see that this is a market which is potentially designed to fuel excesses, given the fact that investors give SPACs money without asking any questions. It reminds me of the Initial Coin Offerings a few years ago. The SPAC sector has the potential to become an enormous bubble, even if it isn’t one at the moment.

Despite your reluctance, you say you are bullish. Why?

Because I think central banks are going to overcook the economy. Ever since Jackson Hole in August, Fed chairman Jerome Powell has made it very clear that they are going to push the economy harder than they have in the past. Powell, in several speeches, has emphasized how devastating it is for low income communities to have high unemployment. The Fed considers it its mandate to make sure that these communities have jobs. Therefore the Fed believes it is doing a good thing by running the economy harder than it has in the past.

They are willingly inflating a bubble?

The Fed sees it as its mandate to create jobs. Consumer price inflation is of no concern to them right now. I can’t imagine a clearer setup for an overheating economy and financial market bubbles. During the GameStop fiasco, Powell was asked repeatedly what he thought of this kind of froth. He said this has nothing to do with the Fed. So, in terms of monetary policy, everything is set for a few years of overstimulation.

And the same thing is happening on the fiscal side, right?

Exactly. Joe Biden is talking about $1.9 trillion worth of stimulus, after we already had $3 trillion last year, which makes it $5 trillion in total. That’s an insane number, about 25% of GDP. There already is an enormous amount of pent-up demand, money that is waiting to be spent. Normally, when you get an overcooked economy and you get inflation, the Fed would step on the brakes. But this time, the Fed has said repeatedly that they will not step on the brakes. So I think the risks here are on the right tail, not on the left tail. This is not a market to be short of.

In a nutshell, you paint a scenario of monetary and fiscal overstimulation, which means this equity market boom could run much further than it already has?

Yes. This is not a big, market wide bubble yet, but we are getting there. And to be very clear, that’s not a good thing. This actually makes me very nervous. Bubbles burst, they always do. We have all these societal cracks that became painfully visible after the Global Financial Crisis of 2008, and central banks just keep blowing up new bubbles to paper over these cracks. This is incredibly dangerous, because inevitably these bubbles burst, and the bandage on the societal cracks rips open again, with the fragmentation, polarization and distrust within our society deepening further.

This pattern, blowing up a new bubble after a previous bubble had burst, has repeated itself several times in the past three decades. What will be the end game of this?

There is no end game, there’s just a cycle. Right now people’s faith in the system is in decline. Trust in institutions – the media, politicians, the «elites» – is in decline, and it seems like distrust is just going to deepen further. What I worry about is what kind of trigger will be necessary to snap us out of this long social panic we’re in, and to start building trust again. I hope it’s not something as extreme as a war.

Do you see the risk of a bond market sell-off, with yields shooting up, which would put an end to the frenzy?

I think at some point the Fed will just step in. They can’t afford to let yields rise too high, because the likelihood of some kind of liquidity event would increase massively. They can’t afford that. So the next stage in the logic of what the Fed is doing would be that they step in and control yields, to prevent them from rising too far, too fast.