Say what you want, but this is one of the best trading markets I can remember in ages. For those complaining the moves make no sense – I agree! But – this is way better than those quiet-no-one-is-interested sleepy sessions.

This morning’s action was just plain wild. No other way to describe it.

Take a gander at the past two day’s of trading in Game Stop:

This is a stock that a week ago was trading at $40, and the week before that $20. This morning, it ticked north of $150. A few days ago, famed short seller Andrew Left from Citron Capital, withdrew from public discussions about this company after receiving death threats against his family. The absurdity of anyone feeling strongly enough to threaten death on someone with a differing opinion of a company’s prospects says a lot about the emotional nature of this market.

You see, a group of enthusiastic of traders on a reddit sub-group called Wall Street Bets (WSB), orchestrated a squeeze on GME. I won’t bother repeating all their scheming, but there is little doubt that this was a concerted effort by a group of traders to squeeze a heavily-shorted stock.

Now, you may believe anyone foolish enough to short a stock with such a high short-interest deserves what they get. I’m not here to figure out the morality of this situation.

Instead, I want to bring to your attention an often overlooked by-product of this recent market action.

This morning’s squeeze wasn’t just relegated to GME.

There was a whole host of heavily-shorted names that got ramped.

Bed, Bath and Beyond:

iRobot:

Express Inc:

The more heavily shorted the name, the more it was a target this morning.

The problems arise due to the fact that there are a whole slew of quantitative and fundamentally based large hedge funds short these names. For example, many on WSB were supposedly specifically targeting Melvin Capital’s large short book. When the stocks that these funds were short all collectively get squeezed, this increased the volatility of their portfolio.

Look at GameStop. Two weeks ago, $1 was considered a decent-sized move.

Earlier today, we were up over $90 at one point!

That’s an obscene change in the dollar value of an expected daily move.

This morning’s WSB concerted-squeeze ended up being a massive increase in the volatility of the short book for many of these hedge funds.

When this happens, these funds are faced with two unfortunate developments – P&L losses and increases in their daily VAR (value-at-risk). These two factors combine to force a general de-risking of the fund’s portfolio.

If you were wondering why Nasdaq all-of-a-sudden plunged this morning, it was most likely from this effect:

And this lesson does not apply solely to increases in volatility to the heavily-shorted stocks portion of a hedge fund’s portfolio. Any increase in volatility will often have the same effect.

The reality is that most modern-portfolio management uses volatility-of-returns as a method of “dialing” the amount of risk they are willing to hold. Some funds use hourly volatility, some use daily, and others use monthly, but make no mistake – the more volatile, the less risk these funds are willing to take.

So, ironically, this morning’s WSB squeeze that took many of these individual stocks higher, caused a general de-risking from many of the large sophisticated hedge funds.

And the real question is whether this selling starts a negative feedback loop.

I’m not smart enough to know the answer to that question, but I wanted to take a moment to explain why even though it might seem like the stock market bulls should be cheering WSB’s squeezes, their success might end up being the trigger that brings about the general stock market correction many have been waiting for.

Remember – increases in volatility cause general de-risking from hedgies and other quantitively-modeled funds. The greater increase in volatility, the more they have to sell.

Watch the VIX closely in the coming days. If we get an increase in demand for protection, this will also cause some “vanna” related selling which could reinforce the negative feedback loop.

The danger signs are piling up. I continue to trade defensively.

Let me throw this out there; the investing game is mind-numbingly easy. You buy good businesses for less than fair value. Sure, we can all argue about fair value. There are always surprises in the future trajectory of a business. This game has some wrinkles and drama, but at the most basic level, it’s easy. In fact, done correctly, it only involves a handful of decisions each year.

If it’s so easy, why aren’t I wealthier? It’s because I’ve tried to complicate things from time to time and made some very expensive mistakes along the way. Look, I’m human. Fortunately, I learn fast and usually avoid making the same mistake twice. I like to joke that my career is nothing more than two decades of finding creative ways to lose money. That’s not to say that the markets haven’t been good to me—the markets have been amazingly rewarding to me.

When I look back on my career thus far, I don’t dwell too much on the winners—remember how I said buying something cheap is easy? Nor do I think about the ones that didn’t go anywhere, while tying up my precious capital. Instead, I repeatedly relive my most expensive mistakes. Over a decade later, I still ask myself how could I have been so foolish to keep shorting more Research in Motion (currently BB – USA) as it went parabolic? On one hand, I was right about the iPhone displacing the Blackberry. On the other hand, it didn’t matter because I was a year early. I was stubborn and it was my most expensive loss ever. (Thankfully I took the loss when I did, as it more than doubled from where I eventually covered my short).

Over the years, I have learned that it is never the boring compounder that really hurts you—it’s the leverage, the complexity and the shorting that gets you—especially the shorting. There’s a reason that I rarely ever short these days. I even penned a piece on the topic; Stop Shorting “Project Zimbabwe” as I wanted to warn my friends that the market is suddenly quite different from what we were all accustomed to. Having been run over in the past, I have a reasonably good perspective on when other situations can run people over—heck, I sometimes even join in the fun on the long side. Looking back to Tesla (TSLA – USA), it was obvious to get out when I did. I feel bad that so many friends didn’t listen. I feel even worse that I didn’t reverse long—it was that obvious.

I bring this all up while watching the drama at GameStop (GME – USA). Let me start by saying that I don’t care how confident you are that a company will go to zero, when there are more shares short than outstanding, you’re just asking for people to play games with you. When word gets out that a few large funds are individually short 8-figure positions, you know that someone will try for the kill-shot. r/WallStreetBets gets the attention, but there are killer whales out there, silently doing the real work. There’s a price where these shorts will puke it up and the market has a funny way of finding that price.

I don’t want to focus too much on GameStop. I had an Event-Driven long position because July 4th is always more fun when you buy your own fireworks. I tossed it at $92.50 premarket for a nice score. I’ve also written a pile of puts as implied volatility has experienced a supernova event, but this is still boring GameStop after all. However, this article isn’t about what will happen at GME; my guess is as good as yours. Rather, I want to point out that you have to be a special sort of stupid to stay short when there are more shares short than outstanding. Hubris is dangerous in the investing game. Shorts are extra dangerous. There are landmines everywhere. I don’t care how small the position is, when a short position goes up 25-fold in six months, it’s going to hurt badly. If you didn’t realize that was a risk, you really weren’t paying attention.

Remember how easy this game is? Buy cheap stocks and go to the beach. I’d be a whole lot wealthier today if I had done more of that when I was younger. Instead, we all like to add complexity because we think we’re smarter than the market. We like to add leverage because 50% more of a good thing tends to make it better. We often forget that one big mistake on the short side can bankrupt you. The first rule of investing is to never put yourself in a position where you can lose it all. Having been burnt in the past, I focus inordinate attention today on how I can get hurt; not on where I can make the most money—that part is easy. I like to think that the shift in my focus means that I have matured as an investor. Trust me, I know how frustrating it is to dig out of a self-created hole. As a result, I’m amazed that so many people blindly dismiss the risks out there. That is just asking for trouble.

“Project Zimbabwe” is a brave new world for everyone. Please stop, review your portfolio, stress test everything, think through the implications of 100-sigma events happening each day. No one is ready for what’s about to happen, as it’s mostly right-tail risk—except if you have a financialized book, in which case a move in interest rates may detonate your left tail first. As others blow up their books, your version of complexity may end up as collateral damage. Stop. Think it through. Be extra careful. No one expected GameStop to become a momentum stock. What else does no one expect? What else can happen? Be careful out there. Stop being stupid. A large fund with a great track record, is not immune to these rules—if anything, their position sizing makes them more vulnerable. A lot of rules that we’ve all taken for granted are about to be re-written. NEVER put yourself in a position where you can lose it all.

The shorts at GameStop are probably thinking that Friday was the blow-off top. Instead, they should be asking themselves, “was Friday a base-camp on the way to the real blow-off top?” Remember, in today’s world, any asset can trade at any price. The price of oil went negative. No one thought that was possible, yet trillions of bonds at negative yields should have been a warning that the old rules no longer applied. I want to repeat again for the third time; NEVER put yourself in a position where you can lose it all. The rules for “Project Zimbabwe” are being re-written and they will be full of surprises. In particular, be careful on the short side. GameStop isn’t the first supernova squeeze of this decade and it surely won’t be the last.

Disclosure: Funds that I control are short GME puts of various strikes and maturities.

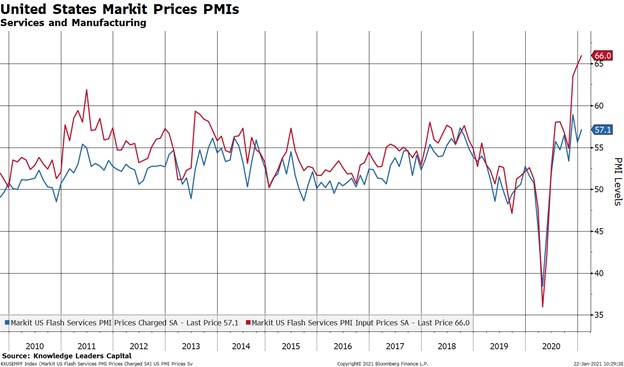

We’re going to keep this post short and sweet because the charts speak for themselves. Today, preliminary Markit PMIs were released for January. Headline numbers ticked up, which is great and shows a continued expansion into the new year. The release also showed that input prices for services exploded higher again, to another all-time high by a wide margin. However, those input prices have not yet fully fed through to prices charged for services. Given the tight relationship between input prices and prices charged, we would expect prices charged to accelerate higher over the coming months. This makes since since service providers will naturally seek to protect their margins.

Moreover, core personal consumption expenditure prices, which is the Fed’s preferred inflation indicator, also appears set to move considerably higher in order to catch up to input prices. This has obvious implications for Fed policy. Does the taper discussion continue? Do expectations for rate hikes get moved forward? Or, does the Fed sit back and watch as prices move to and through their inflation target? They have told us they will do the latter, and we may soon see how strong their commitment is.

The market implications here are pretty straightforward. Tapering is tightening. Bringing rate hike expectations forward is tightening. Allowing inflation to run hot while doing nothing could be seen as de facto easing, which could give even more fuel to the cyclical trade and make those inflation hedges even more attractive.

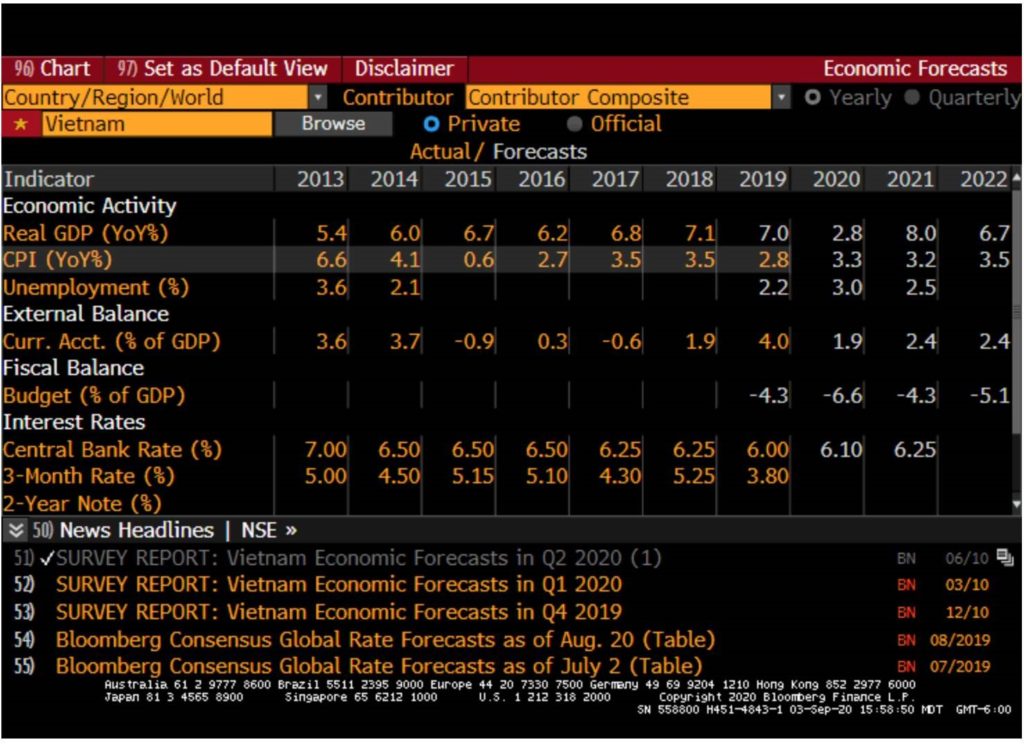

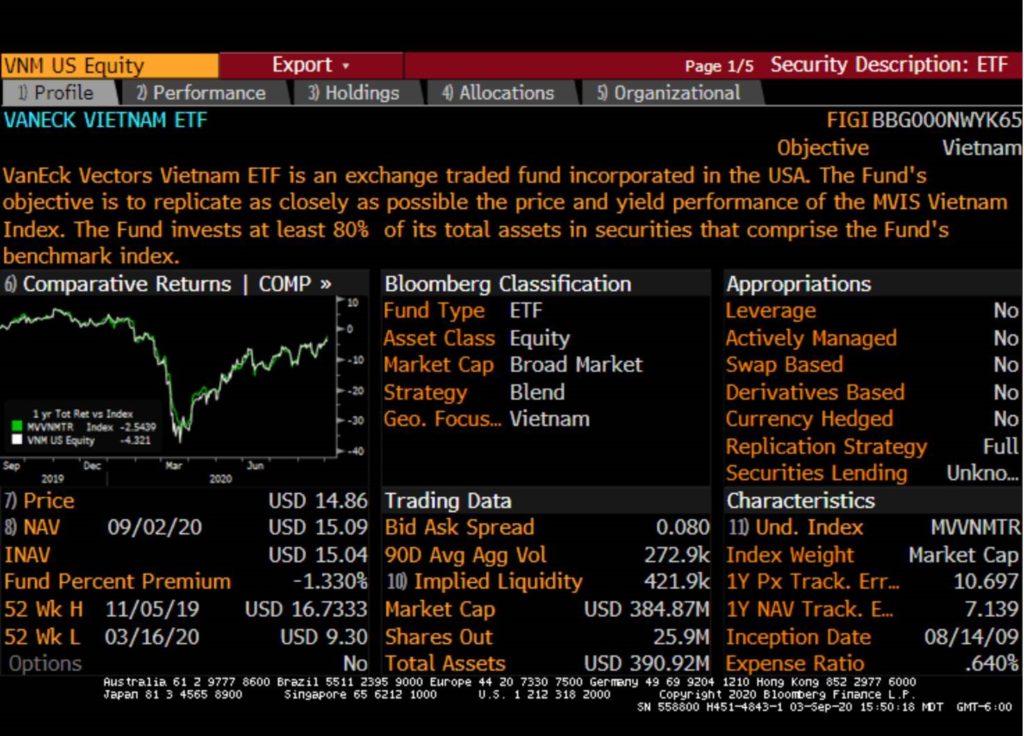

Vietnam is one of the few countries left in the world which will still boast a double digit nominal GDP growth rate. They have 200-300 BP of real rates and a low fiscal deficit which is rarity in today’s world. Positive real rates, low and stable inflation, low unemployment and Positive current account balance is a characteristics of a strong economy. India was exhibiting all these characteristics ( except positive CA balance) in 2002-2003 just before a domestic consumption boom was born.

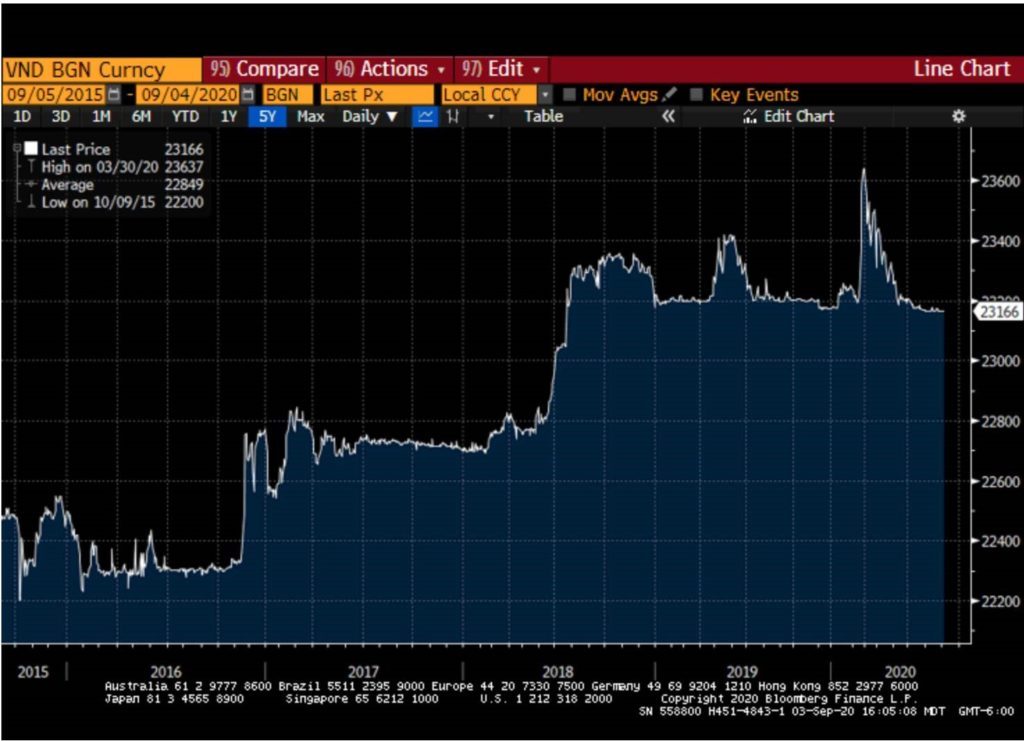

Vietnamese dong has been stable even in the year when Dollar was strong ( between 2015-2019). This is because Vietnam was the beneficiary of huge FDI during those years. In spite of stable currency Vietnam outperformed its ASEAN neighbors which saw depreciating currencies but still couldn’t compete with Vietnam on exports.

Summary of my discussion on Vietnam with an industry insider

Country is communist divided into two camps Pro-China which is in power Pro US which is gaining power

Irrespective of who is in power the work goes on and only the favorites shift but bribes and competition among provinces to attract foreign capital does not hamper the work There are three countries which are becoming favorite of South Korean and Japanese companies looking to “reshore” out of china and Vietnam is the favorite for Low end tech followed by Philippines and then Bangladesh ( for garments and textiles) Low end tech assembly can be easily taught to the Vietnamese because they have high level of basic education. Electronics is the biggest industry in Vietnam and average salary is $300 USD per month Like any other developing economy consumption is the best way to play Vietnam He told me a story about Indian Conglomerate which wanted to set up a steel plant in Vietnam and they were able to easily source iron ore and coal but were not willing to grease any palms . The steel plant went to Korean company Vietnamese military owns a bank and is a big asset owner but they don’t interfere in the economy There have been a bank failure in the past but Vietnam central bank did not allow the bank to go bust and have gradually tightened prudential norms over a period of time He believe that Vietnam has a great future and like any other Emerging economy will have its share of setbacks but in spite of communist characteristics Vietnam is very pro-business

Below is the geographical holdings of VNM Vietnam ETF). You will see some south Korean and Taiwan companies over here. The reason is that as per mandate VNM invests in companies which derive at least 50% of their revenues from Vietnam.

The portfolio is a healthy mix of exports and domestic growth companies. There is also some details about the average valuation. The average daily traded volume are close to 200000 shares

( This is not an investment recommendation. Please do your own due diligence before investing)

As we head deeper into a new decade, and after a memorably turbulent 2020, financial markets seem remarkably optimistic. They look forward to friendlier fundamentals, improved global economic growth, and the much-awaited mass vaccinations which are to improve consumer confidence and lead us back to a “normal life”. This all happens, of course, under the benevolent and sage guidance of governments and central banks that will competently lead us all to a robust recovery. Yet, I wonder: might this outlook be a little too optimistic?

I am not a big fan of economic and financial forecasts. The pretense of being able to foresee what will happen during the next year – or even decade – in a complex system such as the global economy should always be taken with a healthy dose of skepticism. Therefore, I’m sharing my own outlook for 2021 as food for thought, to be considered and added to, or weighed against, the reader’s own expectations and analyses.

While I do have my doubts about future predictions themselves, I am in fact a great fan of the PROCESS of forecasting – all the reading, learning and analysis involved, the discourse, and the estimation of what might lie ahead. That is fun and stimulating. It is one of the reasons I love what we do at BFI. And it is a necessary exercise for investment success. Smart investing is based on recognizing and understanding the driving forces, relevant trends, and global dynamics. That understanding lays the foundation for your strategic allocation. And, while nobody can model (at least for now) and foresee the future, an educated and informed guess is still better than throwing darts at the board without any knowledge at all – well, at least in my experience. So, here we go.

The Great Rebound – or The Great Awakening?

At some point, in school or some other type of Economics 101 class, we all learned that stock markets reflect the aggregate of effective and expected successes and/or failures of companies in an economy, which again reflect the overall strength or weakness of an economy. Therefore, with stock markets ending the nightmare year of 2020 at new record highs, that would leave us to believe the global economy is amazingly strong and robust. Right?

Well, unfortunately, it is not that simple. The world we live in has very little to do with the rules and theories that traditional economics were based on. When I graduated from university, I would not have been able to envision a world where interest rates are at zero, inflation is nowhere in sight, debt levels – both public and private – are at record highs, money supply is at record highs, money velocity and productivity are at record lows and, yet, the S&P 500 has just reached a new, all-time record after one of the worst recessions in modern history.

However, we have all been taught, sometimes painfully, that “markets are always right”. And they have priced in a great deal of positivity. Much of that optimism for 2021 is based on the belief that things can only get better after 2020. Once the coronavirus pandemic is in check with mass vaccinations underway, and once all that pent up demand comes back to life, how can things not get better from there?

So, the question is whether 2021 will provide us with a global economy that goes down in history as The Great 2021 Rebound, or whether we will instead encounter The Great 2021 Awakening. Personally, I think both scenarios have convincing arguments that would support each of them. And at BFI, we will be investing accordingly…; let me explain:

Key factors and considerations

Here’s a summary of some of the core factors and considerations for investing in 2021:

1) The hope of ending COVID. Vaccinations are being rolled out globally. Expectations are high that this will allow us to leave the pandemic behind and return to some form of normalcy in the coming months. In China and other parts of Asia, this already appears to be a reality. However, we should also expect logistical setbacks and delays. Moreover, this coronavirus, as so many in the past, will continue to evolve and mutate, while new viruses may also emerge. Therefore, based on the lessons we learn from this round of “pandemic management” and the future measures employed, we may expect to see more lockdowns and heavy-handed government interventions.

2) Split-world economy. The world economy remains somewhat decoupled. China, along with some other Asian economies, have normalized and are much less impacted by the pandemic and the respective government measures. On the other hand, America and Europe remain hard hit. Therefore, 2021 starts with weak and slowing economies in the Western world, while Asia is enjoying solid growth. Assuming we don’t experience any major pandemic setbacks, an economic rebound may occur in Europe and the US as well. However, this would go against the secular declining growth potential stemming from negative demographics, excessive debt, increasing regulation, and misguided policies.

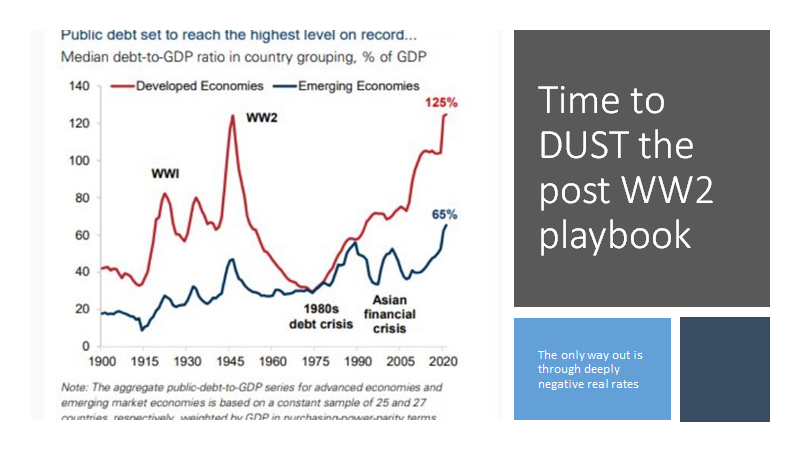

3) Monetary and fiscal excess. Few things are certain in life beyond death and taxes, but it appears we may add a third item to the list: debt. The arrival of this new decade is paired with record peaks and growth rates of debt and deficits, both public and private, and pretty much everywhere. In response to COVID-19, and “thanks to it”, governments have been given the magic-money wand. And they are making ample use of it. As shown in the chart that follows, the fiscal response in 2020 alone dwarfs the response over the period of 2008-2010 during the last financial crisis. A similar picture, by the way, can be seen in monetary policy.

Fiscal Deficits 2020 as % of GDP

Source: Clocktower

This unprecedented expansion of monetary and fiscal support is being justified as a measure to help those who have lost their jobs and businesses. It is presented as relief and support spending. However, as can be seen particularly in Europe and the US, the pandemic has been highly politicized. And the so-called “relief packages” include numerous and large items that have little or nothing to do with relief and support in the context of the pandemic.

4) Big Government. With the unlimited power of “creating” money and debt, the share of government spending in most economies has reached levels that are highly concerning. Empirically, we know that government dollars spent are less productive – in other words they add less to growth – than dollars spent in the private economy.

Sheep spend their lifetimes afraid of a wolf and end up getting eaten by the shepherd.~ Unknown

According to IMF estimates, published in October 2020, government spending as a share of GDP now accounts for more than half, at 50.5%. The Euro area is at 55.7%, while the United States is at 47.2%. The increased share of government influence on the economy (planned economics) is in the process of crowding out the more efficient, innovative and propulsive private sector. It is in essence killing off the benefits of a free-market economy.

Government Debt as % of GDP

Source: Refinitiv Datastream, ECR Research

A necessary condition for sustainable economic growth in the future is a reduction of debt levels. However, reducing the current debt levels would require politically unpopular measures (austerity, debt restructuring, defaults…). The way out that governments are currently working toward instead will involve a mix of inflation and financial repression (higher taxes), and the hope for growth.

5) Negative Real Interest Rates. Financial prudence and thriftiness have been largely thrown overboard, at least in the public sphere. Financing this kind of squander and profligacy, of course, is only possible in the context of rock-bottom interest rates. In fact, as depicted in the following diagram, financing costs (net government interest payments as a percentage of GDP) have been relatively flat, and in some cases, as in Italy or Germany, they have been decreasing over the past 20 years.

Cheap Financing – Net Government Interest Payments as % of GDP

Source: Refinitiv Datastream, ECR Research

This reduction in financing costs is counterintuitive. But it is a reflection of the past four decades – and particularly the last decade – of increasingly low interest rates. As we’ll touch on shortly, two primary deflationary forces (globalization and technology) have contributed to a very unique scenario: they have allowed (and continue to allow) governments and central banks to expand the monetary base beyond comprehension without inflation (in terms of CPI) rising and counterbalancing.

To be clear, we are coming to the end of a secular credit cycle. Sovereign bond yields around the world are in a secular bottoming process that may stretch out for a few more years, but we are, in effect, at the brink of transitioning into a new era.

At this point, with interest rates at rock-bottom, the trillion-dollar questions on the minds of economists and investors are: when will yields start rising? And how? Central banks will try to keep interest rates low, but how and for how long will they be able to resist market forces that will force yields up, particularly once inflation starts to rise?

6) CPI Inflation. Currently, CPI inflation is depressed in most economies, with outright deflationary situations in several European and Asian countries. Central banks have been communicating their intentions to raise inflation to around 2% for several years without much success. The deflationary forces were too strong. Fed Chairman Powell even expressed the intention to let inflation “run hot” (run higher, maybe 4%?).

It is impossible to say if and when inflation will rise in earnest, and how high it will go. The estimates of reputable economists are running all over the map. I personally don’t expect inflation to be a problem in 2021 (a ‘problem’ in a sense that it could trigger turbulence on the yields front). However, we do know from history that inflation can be quite unpredictable, with sudden spurts and eruptions that do have the potential of moving markets rapidly.

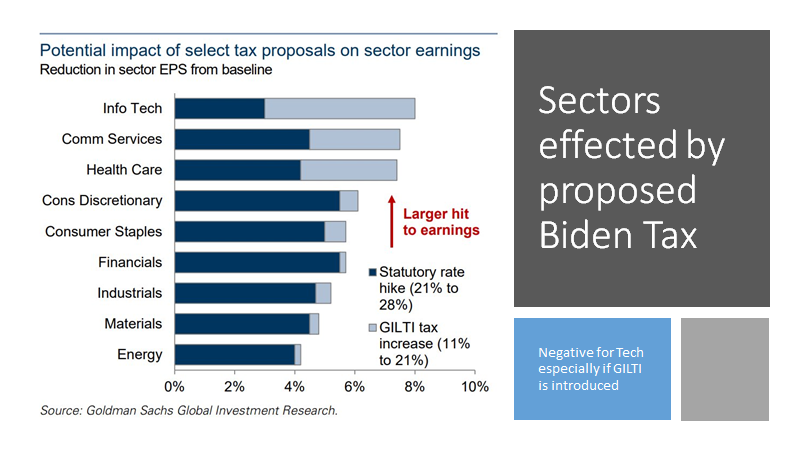

7) Equity Bubbles. There are some sectors in the equity market that look overvalued and (very) toppish. Equity markets have been the main beneficiaries of cheap money. The liquidity induced has lifted the prices of stocks higher and higher.

At BFI, we increasingly see the potential for a short-term correction in stock markets. However, based on an almost 100% certainty of continued monetary and fiscal stimulus, stock markets will continue to benefit. Therefore, we give 2021 the probability of another year with very attractive profits in stocks. The expected setbacks need to be considered and managed actively, however.

Major stock market bubbles since 1960; the FAANG stocks look, and smell, like another one

Source: BCA Research

8) Social Tensions. Wealth inequality in western economies is rising. To a large part, this is due to the monetary and fiscal policies discussed earlier: wealthy investors are able to reap profits on the back of rising financial markets, while the general economy does not allow for equal financial progress for the majority of society. This has led to growing dissatisfaction and growing potential for stark social unrest, as seen in the US last year. In my opinion, the polarization and social tensions in America will not go away under a Biden-Harris presidency.

And it is hardly surprising that the corona crisis has increased this inequality. A recent IMF study on inequality during and after five major pandemics this century found that inequality increased considerably in all cases in the five years following the outbreak, (both when focusing on the Gini coefficient and on the proportion of the total pie taken up by the 20% of households with the highest incomes). More social unrest is in the offing and studies suggest that inequality slows down economic growth.

Inequality on the Rise: Mean Household Income in the US

Source: Refinitiv Datastream / ECR Research

9) The Future is Faster than You Think. This is a title I am borrowing from another interesting book written by Peter H. Diamandis. It discusses how converging technologies are rapidly transforming business, industries, and our lives. I recommend reading this book to get a good overview of the manifold technological advances and the impact they have (and increasingly will have) on literally everything. A constellation of disruptive technologies – the internet of things, cloud computing, big data, 5G communication and, of course, artificial intelligence – is paving the way for a new form of global economy.

Unless you take good note of the (in some cases exponential) acceleration in technological progress as a result of the confluence of several different innovations, you will have a hard time understanding the power of de-monetization and deflation that the so-called Fourth Industrial Revolution (4IR) has. It is a force to be reckoned with in our economic and investment analysis. At this point, unfortunately, it is hard to determine whether the net impact will be positive or negative in the decade ahead. These technological advances are arriving at lightning speed and our current societal systems – and most of all, our governments – are not ready to cope efficiently and effectively with them. Therefore, while much good can come from all of this, we are also facing some formidable challenges.

Investment Strategy

Based on the current circumstances and trends, we all need to reevaluate and carefully consider our individual investment strategies. In the current context, I strongly recommend an investment approach that is PRUDENT, ACTIVE, AND SYSTEMATIC. I do NOT consider the current markets to be in a do-it-yourself environment and I think investors that are not financially sophisticated and experienced enough, with the necessary analytical tools and skills, should either mandate a professional investment firm or radically adjust and simplify their exposure to financial markets.

At BFI, and for our clients interested in a globally diversified portfolio structured to withstand the test of times, the strategic approach for 2021 in summary looks something like this:

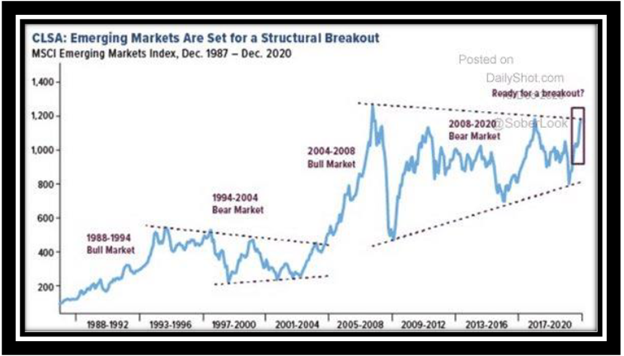

Equity: Stay invested with a strong exposure to selective sectors in equity markets, globally diversified, with increased weighting in emerging markets.

Bonds: Strongly reduced exposure to bonds. Short-term government paper may serve for liquidity purposes. Very selective corporate exposure. Replacement of typical traditional allocation to bonds with alternatives, including gold, silver, and low-volatility hedge funds.

Gold and silver: We have significant allocations to gold and silver, and we have started to add mining. Many of our wealthy clients hold physically allocated precious metals in segregated storage in Switzerland with Global Gold, in addition to their discretionarily managed portfolios with BFI Infinity.

Alternatives: We have significant exposure to real estate, hedge funds and precious metals (physical and mining). We are also looking to increase our exposure to commodities, which are starting to come out of an extended bear market, and which might also profit from potentially increasing inflation expectations.

Downside Protection: We actively employ downside protection tools, primarily put options, on the stock markets. This allows us to stay fully invested without the danger of stark losses in the expected corrections.

Crypto Currencies: We invest in Bitcoin in small allocations via specialized strategies that also protect on the downside. For increased exposure to Crypto, we cooperate with business partners specialized in this field.

Conclusion

Effective vaccines, declining political risks, ongoing fiscal and monetary stimulus, and pent-up demand have created a jubilant mood among investors and analysts and a very bullish outlook for 2021. However, markets are ignoring several risks and rising long-term rates that could throw a wrench into the works in the course of this year.

Stoics like Epictetus, Seneca or Diogenes recognized the value of not allowing your emotions and passion to run out of control. In victory and success, as in defeat and pain, their objective was to prioritize reason, virtue and the discipline of Eudaimonia (striving to be the best version of yourself at all times) over emotional excess based in pleasure, fear or greed.

I believe that the principles of stoicism can provide a valuable compass for life. And, as we find closure with 2020, I think we are well advised to practice some stoicism as we continue our journey into the new decade. In other words, let us not be too pessimistic or too optimistic. Let us take a calm and reasoned look at what this new year might have to offer; and then, why don’t we settle for some cautious optimism.

Samuel Rines has written a timely article on tapering and what does it mean for the markets.

Tapering Paradox

“Either the well was very deep, or she fell very slowly, for she had plenty of time as she went down to look about her and to wonder what was going to happen next.” ―Lewis Carroll,Alice’s Adventures in Wonderland / Through the Looking-GlassOver the past week or so, a few Federal Reserve officials have begun to say that “tapering” its quantitative easing program could occur in late 2021.While on many levels this seems to be a bit of wishful thinking, it is worth exploring what that actually means.In the summer of 2013, Ben Bernanke signaled tapering would occur in the fall. That became known as the “taper tantrum” as yields moved higher and the dollar strengthened.But – as it turns out – the actual tapering in January 2014 did not see a rise in long rates. Instead, long rates were pressured for the next couple years.As it turns out, rhetoric of a taper is far more powerful than the act of a taper. Currently, it is the rhetoric phase. That should not be forgotten.

Quantitative easing – the Federal Reserve’s purchases on U.S. Treasuries and Mortgages and other securities – is a powerful tool. And – long with the traditional fed funds rate – “QE” has become one of the Fed’s favorite tools to combat crises.Recently, there have been rumblings from Fed officials that QE could be “tapered” (reducing the dollar amount purchased month to month). While somewhat odd (the U.S. unemployment rate stalling at 6.7% and elevated levels of non-participants in the labor market), understanding the likely consequences of this rhetoric and an actual tapering of QE is useful.

The “taper tantrum” of 2013 provides a bit of perspective. In testimony before congress, then Fed Chair Ben Bernanke stated QE was likely to be tapered in the fall. Yields rapidly moved higher higher (as did the U.S. dollar). This shock to the system caused the Fed to back away from its plan to taper bond purchases in September 2013 to January 2014.As it turns out, yields peaked as the taper began and continued to fall for the better part of two years as the Fed halted purchases.

This seems paradoxical. The Fed slowly stopped buying billions in bonds, and bond prices rose and yields fell. But on a deeper level it makes sense. QE is a powerful tool, because it boosts confidence in positive economic outcomes. This boosts “term premium” or the compensation investors demand for holding bonds over time due to the risk of higher rates. Positive economic outcomes tend to increase interest rates. Not to be overlooked, liquidity being added to the system boosts the outlook for inflation too.When the Fed stopped doing so in 2013, these measures began a persistent decline. The likelihood of better than expected economic data faded, and inflation was no longer expected to move higher in a meaningful way. Hence, longer-term interest rates (most sensitive to economic outcomes) declined.

Importantly, the majority of 2014 saw fairly robust growth that continued into 2015. In other words, yields were falling back before economic growth sputtered. The move lower was accentuated – but not started – by slowing economic growth. Simply, the Fed changed the outlook for yields by removing a critical support for yields, not prices.

All the talk around a taper is strange. One of the tools the Fed has been trying to exploit is “forward guidance” – the ability to succinctly and clearly communicate its monetary policy well into the future. It is a “cheap” policy tool as long as market participants believe what you say. All the rhetoric of a tapering risks pulling forward expectations for a rate hike as well. That is not something the Fed is keen to do.The critical part of the taper rhetoric is that it matters more than the actual taper. Meaning, interest rates are likely to move higher during the rhetoric phase, not during the implementation of a taper. A paradox worth considering.

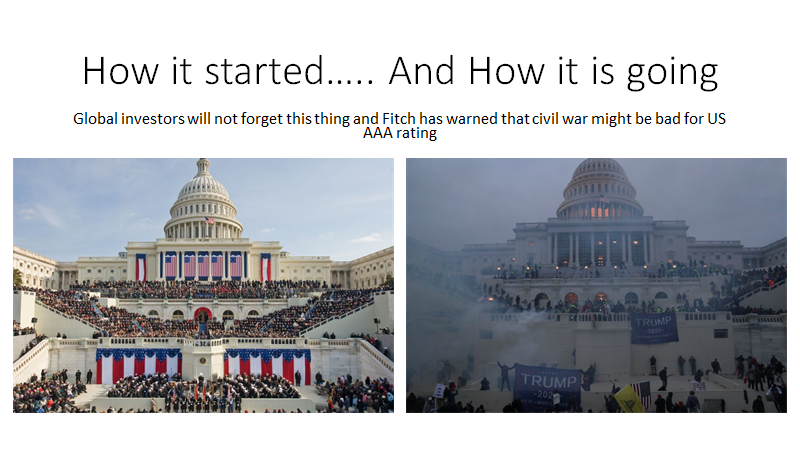

As I write this email, 10-year Treasury yields have spiked to 1.08% and stocks are at all-time highs, even though yesterday we saw a record number of Covid deaths in the United States and a mob storming the Capitol.

Why? Because our common knowledge – what everyone knows that everyone knows – is that enormous fiscal stimulus is coming soon (bullish!), and with that will come inflation (bullish?), and with that will come … something … that will impact our portfolios in a major way.

Every investor in the world is now trying to figure out that something. Every investor in the world is now trying to figure out what inflation means for their portfolio.

Here’s how it will play out in your own head.

Your first instinct will be to try to figure out on your own what inflation really and truly means for your portfolio. You will read about the history of inflation and think really hard about it. You will have some ideas and, depending on your ego, more or less confidence in those ideas. But then, on reflection, you will decide that you want to understand what everyone else thinks inflation really and truly means for your portfolio. You will do this by watching CNBC and reading Bloomberg Opinion articles and brokerage research reports and portfolio manager letters and the like. You will call this “doing your research” and “listening to smart people”. Over time you will begin to recognize a common thread running through what you hear and what you read. You will call this common thread an “investment thesis”, and you will find yourself nodding your head by the fourth or fifth time you recognize this common thread on what inflation really and truly means for your portfolio. You will begin to recognize this common thread in more and more of what you hear and read, and you will provide positive feedback in one form or another to the creators of this content. You will congratulate yourself on being smart enough to tease out this common thread from your “research” and you will begin to implement your “investment thesis” in your portfolio. Soon you will have conversations with other smart investors who have similarly identified this investment thesis from their research, and you will take great comfort in that. You will increase your position in the investment thesis.

I am not saying that your investment thesis is wrong. I am not saying that you will lose money with your investment thesis. On the contrary, if you are early with your investment thesis and that thesis evolves into common knowledge, I think you’ll do very well.

I am saying that what you call an investment thesis is, in truth, a narrative.

I am saying that the business of Wall Street and financial media is to create an investment thesis that makes you nod your head. I am saying that you will always find an investment thesis that makes you nod your head, and that this process of selling you an investment thesis that makes you nod your head is as predictable and as regular as the sun rising in the east and setting in the west.

Right now, Wall Street is trying to identify which inflation narrative will be an investment thesis that makes lots of people nod their heads.

This is what it looks like when common knowledge – what everyone knows that everyone knows – is being formed.

Recognizing THAT – and maybe even trying to get ahead of THAT – is how you play the game of markets successfully.

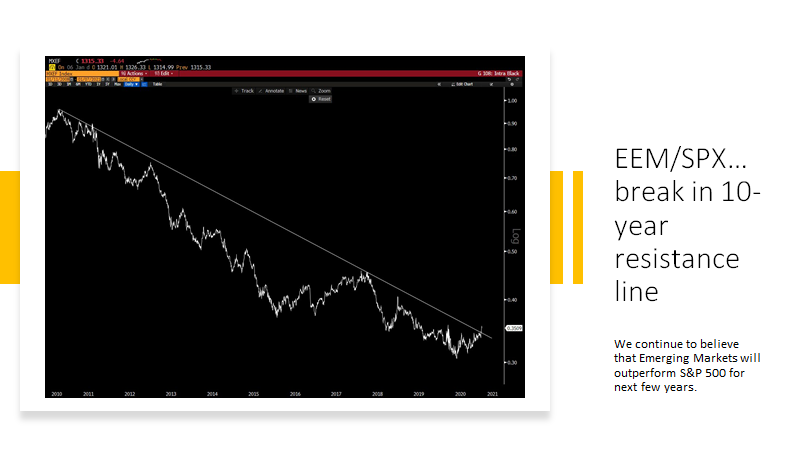

Because LIQUIDITY creates Fundamentals and not the other way round.

1987- US equity market crash led to Fed cutting rates – Dollar went down, and the capital moved into Japan and Japanese real estate.

At one-point Japanese imperial palace was valued more than the entire Manhattan. The bubble finally burst, and Japan has not seen those levels in equity markets even after 40 years

2001- Tech bubble crash led to Fed cutting the rates – Dollar went down and the capital moved into Emerging markets creating a bubble in EM

2008-9 crash led to Fed cutting the rates- Dollar did not go down and the money remained in US creating the US markets and US tech bubble (we are in late stage of this bubble)

2020- COVID-19 crash led to Fed cutting the rates- Dollar goes down and the money starts moving into Commodities and Emerging markets creating a bubble (we are in early stage of this bubble)