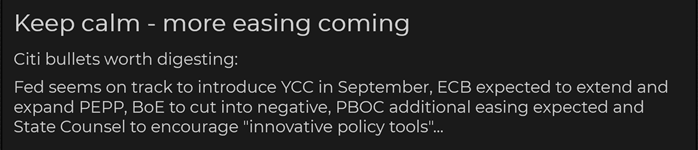

Fiat system goes critical with the dawn of the new decade, the world will become increasingly interventionist. In keeping with the motto “Once your worldly reputation is in tatters, the opinion of others hardly matters”, all the barriers to new debt are now being breached. Debt no longer plays a role, and zero interest rates and money supply expansion remain the order of the day as far as the eye can see.

What was obvious from writing this report was that, the main result of the fiscal and policy response globally to the virus, through monetary and fiscal policy and regulations, will be a structural shift to much bigger government, whatever political flag it is under. This will change the whole nature of society, perhaps best highlighted by Bloomberg which said German Chancellor Merkel’s stimulus package will result in the biggest re-engineering of the economy since post-war construction, installing the kind of state “capitalism” in Germany that borrows heavily from France or China. This is not the result of some devious plot as many assume, but rather the cost of sustaining the existing imbalances. Nevertheless, with the imbalances and costs so high, the changes to the shape of the economy and industry, both domestically and internationally, and the makeup of that industry in terms of competition and ownership etc, including passive vs active (the only game in town will be base money & fiscal spending) – will be massive.

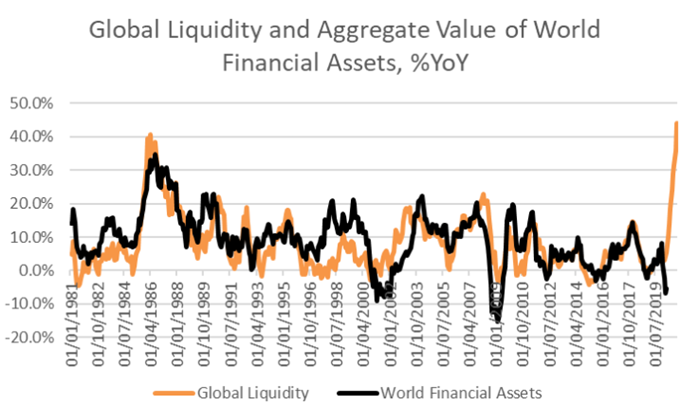

The only chart that matters

I know cash flows and valuation matters for the patient long term investors but even warren Buffett has started complaining about lack of market opportunities due to heavy intervention by central bankers and famed investor Jeremy Grantham has reduced his equity allocation in his flagship GMO fund from 35% to 25% and was quoted in FT saying stock markets are “lost in one sided optimism”. It seems that now you need to take LIQUIDITY as granted and then use your skills to find the direction in which this LIQUIDITY is flowing. This kind of LIQUIDITY just makes the system more vulnerable as poorly run companies are also able to find money to continue operations and this brings down the productivity for the entire system.

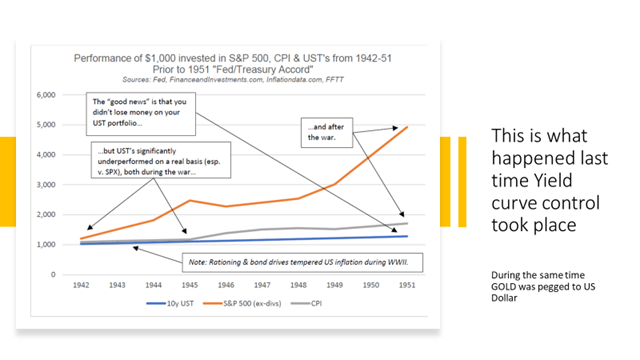

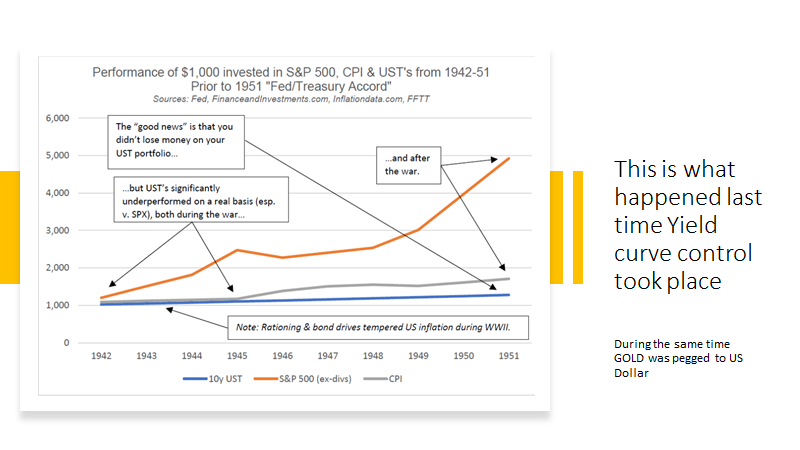

if you are worried about whether this Tsunami of LIQUIDITY is creating distortions in asset prices wait till US Fed decides to CAP the bond yields. I believe the only way US can get back to its Trend growth growth is by reducing the value of US Dollar. The best way is to Cap the bond yields and let the inflation run hot. Lat time it happened was after second world war during 1942-1951 period and US was able to get back to fast growth lane by nominally defaulting on its debt.

Goldman turns optimistic based on what Higher Prices?? Goldman turned optimistic on U.S. Stocks. Strategists rolled back a prediction that the S&P 500 will slump to 2400- 21% below Fridays 3044 Close – and now see the downside risks capped at 2750.It may even rally further to 3200.Policy support limits the downside to roughly 10%, they said.

What lays ahead for the Federal Reserve free money printing institution of the world

The United States’ Federal reserve’s balance sheet increased by USD441bn in May to USD7.06trn. Over the last 5 and 10 weeks, M2 money supply has grown at an annualised pace of 106% and 111% respectively. The growth is set to continue. The inert Treasury General Account soared to USD1.364trn, indicating that, to meet its own goal of it being down to USD800bn by the end of June and September, the Treasury must inject USD564bn into the economy, equivalent to over 3% of money supply in just over 4 weeks. Also, Boston Fed President Eric Rosengren said he expects companies to begin receiving money through the central bank’s Main Street Lending programme within 2 weeks, which the Boston Fed will be administering. The general message was of greater monetary and fiscal stimulus to come.

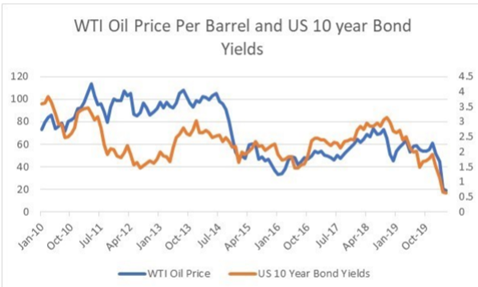

Have oil prices finally turned?

Looking into the Mirror is not helpful in investing

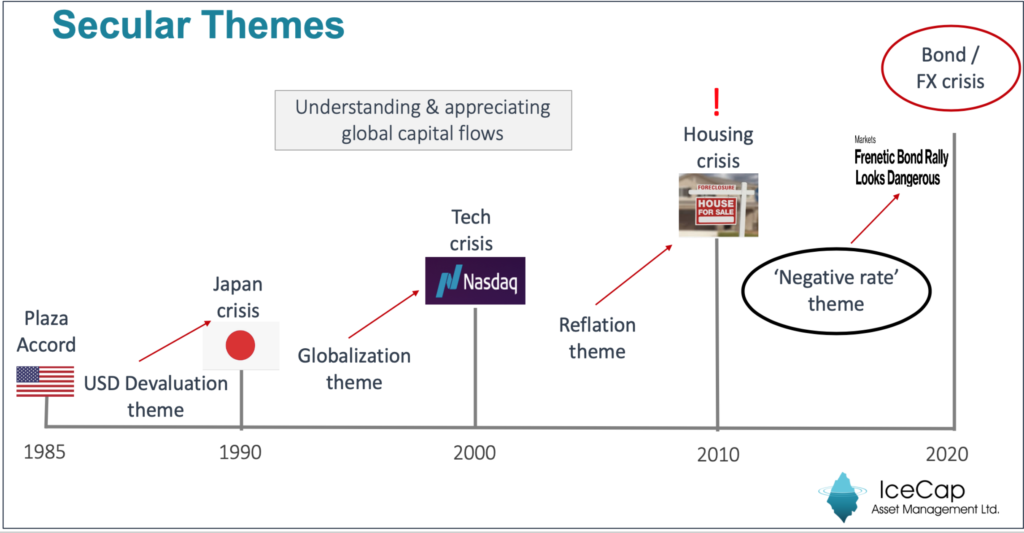

The first 20 years of the 21st century can be divided into two halves. The first half was the reflation trade, which was characterised by rising commodity prices, a weak US dollar, and strong growth. The second half has been the opposite, with falling commodity prices, weak growth and a strong dollar. Perhaps nothing shows this more clearly, that the relative performance of emerging markets, which greatly outperformed the S&P 500 in 2000s, and then gave back all that relative outperformance in 2010s.

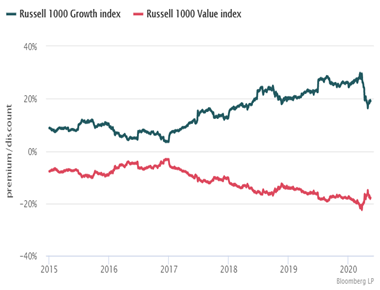

Collapsing yields and commodities have forced investors into a variety of “safety trades”. Growth stocks over value stocks, gold over silver, and long dated bonds. All have remarkably similar performance, particularly in recent years.

( chart courtesy: Horseman Capital)

The tale of two halves

2000-2010: Capital moves from Developed Markets TO Emerging Markets

2010-2020: Capital moves back from Emerging Markets TO Developed Markets

( chart courtesy: Horseman Capital)

Macro Outlook

2020-?

Changing underlying trends in oil, government spending and Chinese exports suggest that the macro trend of the 2010s will not be the same as the 2020s.

If the experience of changing macro trends from 2000s to 2010s are repeated, then the winners of last decade, will under perform the losers of last decade

COVID-19 has acted as a ‘Great Accelerator’ to many pre-existing socioeconomic and technological trajectories.

Trends in monetary and fiscal policy have also been accelerated. Not only in the amount of stimulus but also in merging the two forms of policy.

In many ways, merging the two is necessary, given that the historic reliance on monetary tools has left the real economy struggling while asset prices have rebounded.

A powerful narrative has emerged in the wake of COVID-19. ‘The Great Acceleration’ is the concept that previously existing socioeconomic developments have been pushed into overdrive. Tele-commuting, the dominance of big-tech, and the shift to online learning have all taken multi-year jumps forward in the space of just months. For instance, NYU Stern Professor Scott Galloway explains that post-secondary education models are permanently shifting here.

The economic fallout from COVID-19 has also provided new fuel for the prevailing trends in monetary and fiscal policy. The Fed has expanded its balance sheet by around $3 trillion in around 90 days.

Even before COVID-19 appeared, monetary easing was already ongoing. The Federal Reserve cut overnight rates three times before the global pandemic shocked the world (July, September and October of 2019). The ferociousness of the Fed’s response to the virus indicates that policymakers believed that liquidity conditions were tight, despite a 1.5% Fed Fund rate pre-virus.

Policy, Currencies, And Credit

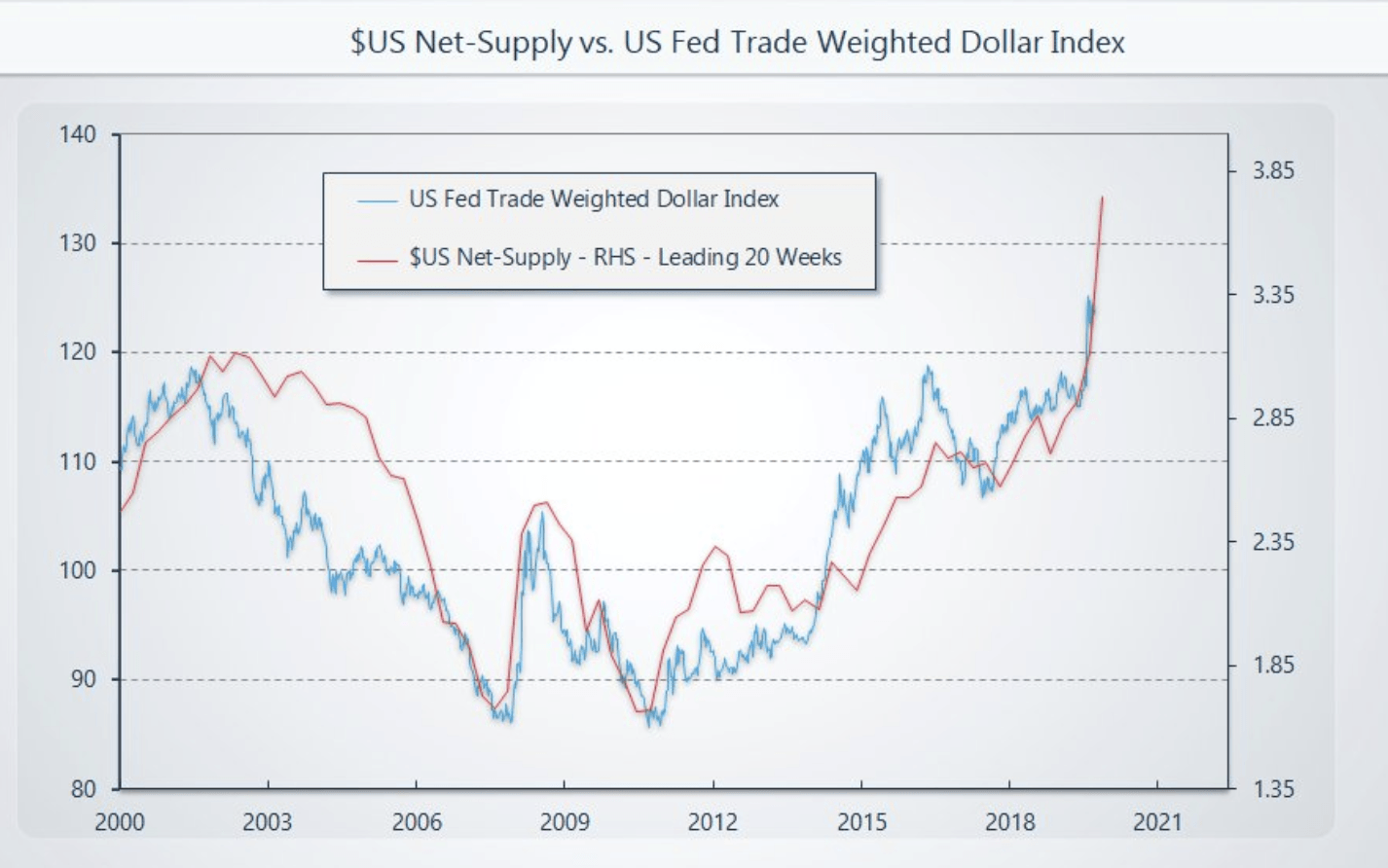

A strengthening USD amidst a growing Fed Balance Sheet has been a hallmark of the post-GFC period. This is somewhat counterintuitive to traditional economic doctrine. The rapid balance sheet expansion in March accelerated the post GFC trend. Below is a chart of net USD supply (M2 – Total US Denominated Debt) compared to the Trade Weighted Dollar Index.

Source: GMI

One explanation for this relationship is that through Quantitative Easing (QE), the money supply sits as excess reserves at institutions, while borrowing demand remains weak. Smaller entities that need dollars have a hard time getting them from banks. Larger, formerly highly-indebted companies focus on de-leveraging. This was a hallmark of Japan’s ‘lost decade’ through the 1990s.

Source: Bank of Japan

As monetary policy becomes easier, the velocity of money decreases. Central bank balance sheet expansion through QE and asset purchases increases asset prices but does not stimulate corporate capital expenditures. Below is a graph of U.S. money velocity as compared to commercial and industrial (C&I) loans outstanding.

Source: St. Louis Fed, BIS

The Japanese experience through the 1990s was somewhat different in the sense that the Yen did not carry the same global reserve currency status that the USD maintains. The offshore dollar borrowing market (Eurodollar market) has exploded in size over the past decade. This is the classic currency carry trade – the USD as a funding market for offshore recipient markets.

The market liquidity event through March caused massive stress in offshore dollar funding markets. As U.S. policymakers announced an unprecedented $7 trillion in monetary and fiscal stimulus through March and April, the trade-weighted dollar was unchanged over that period. This indicates how short of dollars global markets have been for years, punctuated by a liquidity event that exacerbated the prevailing trend.

The Next Chapter

So long as the U.S. dollar maintains strength, it’s likely that policymakers continue with massive fiscal and monetary initiatives to address the economic fallout from COVID-19. Policymakers would prefer a lower dollar, but the past ten years have shown the disconnect between dovish policy and the dollar.

The disconnect between market prices and the real economy is historic. The importance of fiscal policy to restore employment and consumer spending cannot be understated. The distinction between monetary and fiscal policy has effectively shrunk. As the U.S. Treasury issues stimulus cheques to individuals funded by Treasury bond issuances and the Fed purchases these securities through open market operations, we’ve crossed a bridge into MMT.

Difficulties in walking back balance sheet expansion were illustrated by the Q4/18 rejection of Powell’s quantitative tightening (QT) program. Given massive headwinds in employment, it will be incredibly challenging for policymakers to consider reductions in fiscal stimulus. If anything, policymakers will likely err on the side of more, rather than less.

The most prominent effect of stimulus is not CPI inflation, dollar weakness, or material increases in economic growth. Instead, it’s an appreciation in asset prices. The Fed is incentivized to continue to stimulate asset prices further.

Unfortunately, a major consequence of asset price inflation is the exacerbation of wealth inequality. This was traditionally due to ownership of assets being increasingly concentrated in the hands of the wealthy. Now we face another source of income equality: the benefactors of new economic stimulus being disproportionally large businesses while Main Street does not have the same access to capital. This was observed in Japan in the 1990s, and already there are signs of the same trend in the U.S.

In Conclusion

The reliance on monetary policy as a stimulus tool has accelerated through the coronavirus epidemic, just like many other trends across society. The emergent phenomena of combining fiscal and monetary policy is also making a surge forward.

This combination is necessary given the disconnect between asset prices and the state of the real economy. History suggests that businesses prefer to de-lever rather than borrow after facing insolvency scares. Policymakers have much more experience in monetary expansion compared to directly injecting capital into individuals’ bank accounts. The transmission mechanisms for the former are tried and tested, whereas the implementation of policies resembling MMT is embryonic.

The widening gap between the well-being of the average American and the level of asset prices adds to the palpable state of societal unease, particularly among low-income earners. Policymakers understand this, and I would expect a massive fiscal response. However, these tools are new and less battle-tested than monetary policy, which will also continue to be used heavily. The implications for further monetary expansion are easier to see (higher asset prices) than an acceleration in monetization of fiscal deficits. But it’s hard to imagine that the usage of both sets of tools will not continue to accelerate at breakneck speed.

High debt levels have been a significant contributor to the fragility of global economies in response to the pandemic shutdown.

These high debt levels can be “fixed” by reducing debt (numerator) or increasing the money supply (denominator). The latter is more often the case, historically.

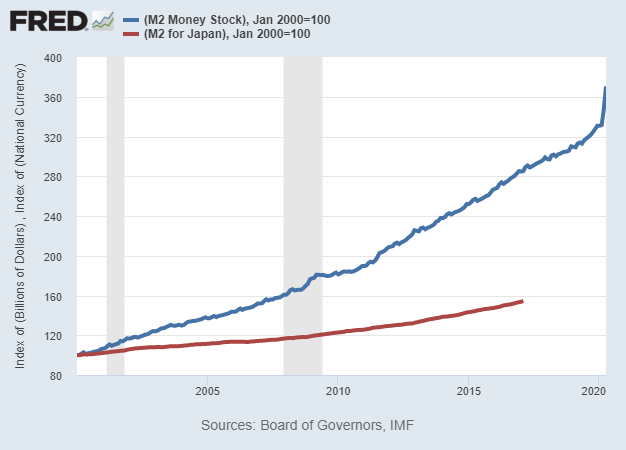

The U.S. money supply is expanding more rapidly than that of Japan and the Eurozone, and is likely to continue doing so.

The world has a debt problem.

Specifically, debt as a percentage of GDP has climbed to very high levels throughout the world. Developed markets on average have much higher debt than emerging markets, but emerging markets often owe debt in currencies they don’t control (like dollars), so it’s a very large problem all around the globe, albeit with different magnitudes and different styles in different places.

A 2019 report by the International Monetary Fund found that, using 2018 figures, total global debt was $188 trillion, or over 220% of global GDP. When private and public debts are added together, the United States, China, and the Euro Area have similar levels of total debt as a percentage of GDP, while Japan stands atop at the highest ratio of total debt to GDP.

The Bank for International Settlements keeps track of government and non-financial sector private debt as a percentage of GDP for many nations. Here are their debt figures for some of the largest countries and economic regions:

This article helps put some potential outcomes for these high debt levels in perspective as it pertains to financial asset class performance in the 2020’s.

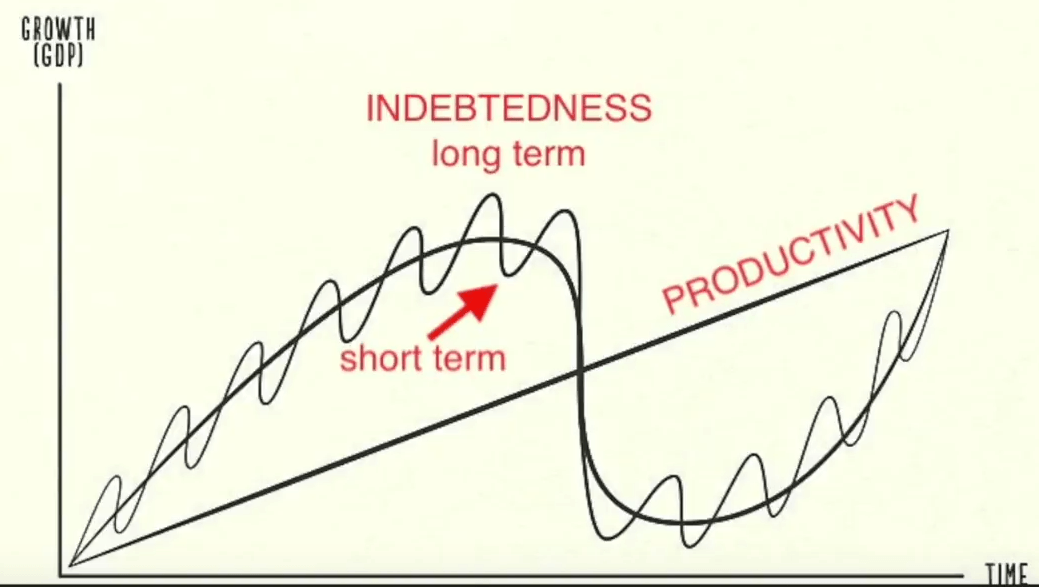

The Long-Term Debt Cycle

Leverage has a tendency to gather in large super-cycles, in addition to typical business cycles.

Ray Dalio, founder of Bridgewater Associates, has a good visual that shows his conception of the relationship between the long-term debt cycle and the short-term business credit cycle:

Chart Source: Ray Dalio

Over time, technology leads to productivity growth at what tends to be a pretty smooth rate. However, rapid debt accumulation can pull forward some of that growth to create a period of more rapid GDP growth (a “boom”), and then subsequent periods of deleveraging can give back some of that extra growth that was previously pulled forward (a “bust”).

During a typical 3-10 year business cycle, debt accumulates until a recession occurs, which forces a period of deleveraging to happen, and then upon recovery, debt starts to accumulate again. However, deleveraging rarely brings the debt as a percentage of GDP down to where it was in the beginning of the cycle, so each subsequent business credit cycle tends to finish and restart with a higher level of debt than the prior cycle.

Another key variable is interest rates. As interest rates decline during a long period of disinflation, governments, households, and companies can support higher absolute debt levels relative to GDP or income, while still being able to pay the interest on that debt. However, that excessive debt level makes businesses and other entities with debt fragile to economic shocks.

This debt accumulation over multiple cycles (lasting 50-100 years in total) is the long-term debt cycle. It eventually hits unsustainable levels and triggers a much larger deleveraging event that typically involves a currency devaluation to smooth out such a big, systemic adjustment.

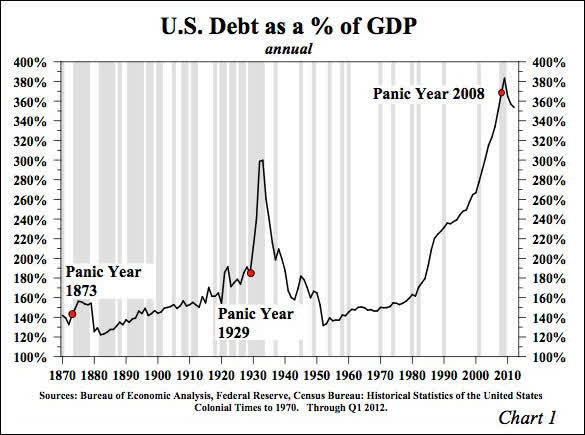

In the United States, the Great Depression in the 1930’s was the culmination of the long-term debt cycle, and a period of massive deleveraging and currency devaluation occurred. We then spent the better part of a century accumulating debt as a percentage of GDP since then, and in recent decades we have built up an even larger debt relative to GDP than we had in the 1930’s.

The United States has the global reserve currency, so this article will focus on the United States as the key example, but I’ll provide an interesting comparison to Japan as well.

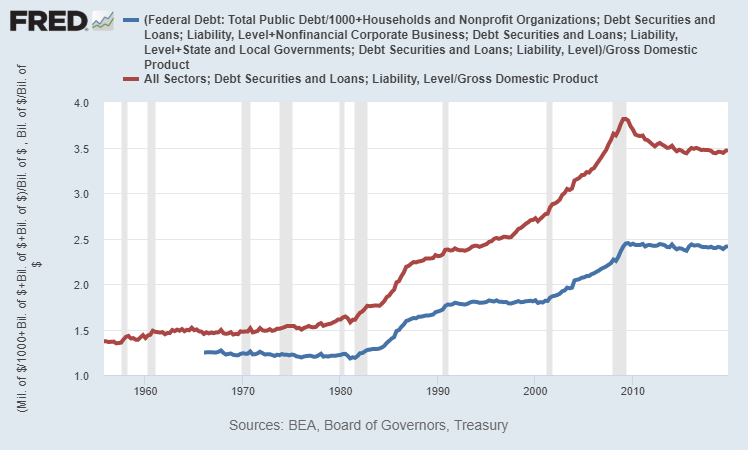

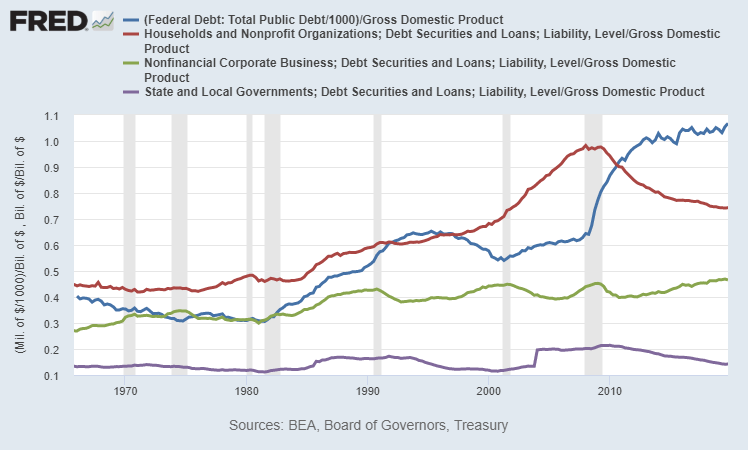

As of the end of 2019, U.S. total debt of all types according to the Federal Reserve (meaning, it includes more than the BIS debt chart above) was equal to about 350% of U.S. GDP (red line below). If we just focus on debt in the non-financial sectors (federal government, state and local governments, households, and non-financial corporations), the ratio is just under 250% (blue line below), which roughly corresponds to the 250% BIS estimate.

Chart Source: St. Louis Fed

We can break down the four major sub-components of non-financial sector debt (the blue line in the chart above) and see that after the 2008 crisis, a significant amount of the leverage moved from the private sector to the federal level, and yet overall private balance sheets are still quite leveraged:

Chart Source: St. Louis Fed

This large amount of debt is a key reason for why so many consumers and businesses became insolvent in a two-month economic shutdown in response to a virus, and why trillions of dollars of bipartisan stimulus and money-printing happened within weeks of the shutdown. High debt levels create systemic economic fragility, to the point where mass-insolvency becomes a national security issue.

In recent years, people often said that the historically high debt levels don’t matter much because, thanks to low interest rates, debt servicing costs are low. This did allow households and businesses to hold elevated levels of debt. However, that argument only applies when everything works smoothly, in a non-inflationary and non-disrupted economic environment. A pandemic (and particularly the economic shutdown in response to that pandemic) came along and showed how fragile that situation was. The low interest rate and its effect on debt servicing costs don’t matter much for either households or businesses if they lose their income while they still have a ton of debt on the balance sheet.

As a measure of system resiliency/fragility, absolute debt levels relative to metrics like GDP and income levels matter, even in low interest rate environments. Debt levels are also a measure of how much financial asset value we’ve extracted and multiplied, relative to the base economic reality.

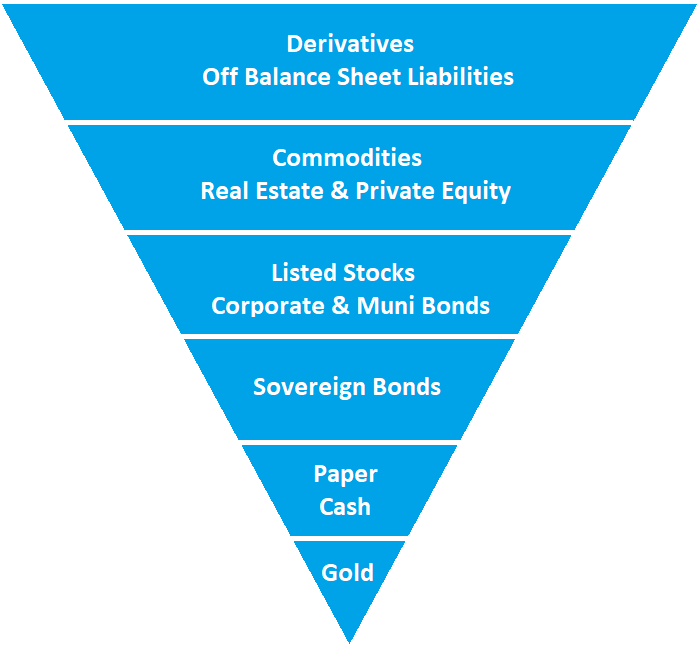

Exter’s Pyramid

The 20th century economist John Exter has a well-known visual conception of the financial system called Exter’s Pyramid, and here’s a simple version of it:

The pyramid is inverted because each layer of the pyramid is much larger than the one beneath it. The foundation assets like gold and cash are dwarfed in market size by the riskier sections of debt, equity, and derivatives.

At the bottom of Exter’s pyramid is gold, the small foundation, because dollars and other currencies were still backed by gold in Exter’s career. In some forms of the visual representation, the gold section is separate from the rest of the pyramid. The United States officially has about $400-$500 billion worth of gold as reserves, depending on price levels in recent months.

The next layer up is paper cash or in today’s more common form, digital money. At the core of this is the monetary base, and from there it expands into narrow and broad measures of total money supply in the fractional reserve banking system.

Then up from there is the layer of sovereign bills, notes, and bonds. These are promises to pay cash in the future, and are considered to have near-zero nominal default risk, but do have interest rate risk and purchasing-power risk.

Up from there is a couple layers that include the universe of private and local government assets, ranging from stocks to corporate bonds to municipal bonds to private equity and real estate. These securities and other assets have default risk, in addition to interest rate risk and purchasing-power risk.

At the top of the inverse pyramid is the derivatives market, e.g. options and futures. This layer of the pyramid is also sometimes thought to include unfunded liabilities.

The “wider” the upside-down pyramid is, the more top-heavy and unstable it is, with lots of debt and expensive equity markets. The “narrower” the upside-down pyramid is, the more stable it is. This is unlike a normal pyramid that would be more stable as it gets wider.

For example, a wider upside-down Exter’s Pyramid would typically have a higher ratio of debt-to-cash within the system (which is less stable), and a narrower pyramid would typically have a lower ratio of debt-to-cash within the system (which is more stable). Most or all modern economies have more debt than cash, but it’s a matter of ratios.

Long-term debt cycles often run into deleveraging events when the pyramid becomes very wide, with an incredible amount of debt relative to cash in the financial system. There becomes a shortage of cash from which to support existing debts, and this gets exposed during an otherwise normal economic downturn.

In other words, one of the typical recessions turns into something bigger when a short-term business cycle deleveraging event crashes into an extremely wide Exter’s pyramid that doesn’t have much flexibility, and it results in a bigger long-term deleveraging period, as we saw starting in the 1929 and 2007 timeframes, and lasting for many years from those peaks.

“Fixing” the Debt: Narrowing the Pyramid

The government and central bank can’t directly control the GDP, which is a measure of economic output. They can, however, significantly control the money supply.

Some people think that commercial banks alone control the money supply based on how much they lend and how much demand there is for lending, but it’s important to realize that the government and central bank can also directly send money to people in the form of helicopter checks, extra unemployment benefits, social security, housing support, healthcare support, tax cuts/credits, federal student loan forgiveness, or indirectly through major infrastructure programs.

In other words, the federal government can run massive fiscal deficits that are funded by QE debt monetization (when the Federal Reserves creates new dollars to buy newly-issued Treasury securities to fund government spending), and those deficit dollars get injected into the economy in various ways and find their way into the broad money supply, outside of the fractional reserve commercial bank lending channel.

So, when it comes to “fixing” the debt at the end of a long-term debt cycle, it’s important to keep in mind that the financial system can either reduce debt, or increase GDP and/or money supply to come up and more closely match the debt. The goal from the perspective of policymakers is to decrease the debt relative to GDP and/or the money supply, and to do that, either the nominal debt can go down or nominal GDP or money supply can go up.

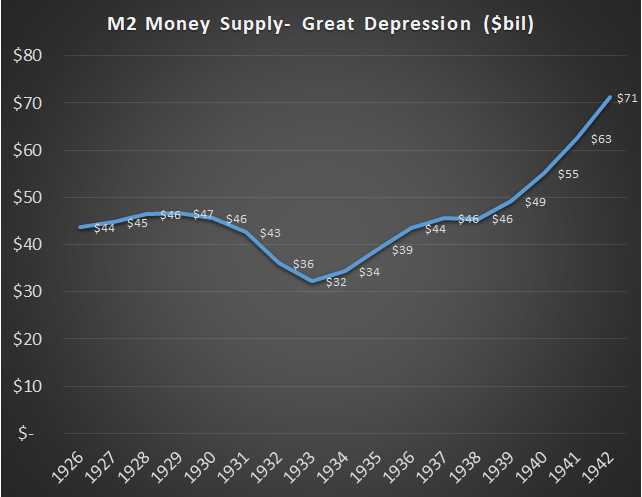

The Great Depression Example

If we look at that Great Depression debt/GDP chart again, we can see how rapid the deleveraging was in 1933:

So what happened? Did everyone just default or suddenly pay off debts? No.

A significant amount of defaults and deleveraging occurred through the whole period from 1930 through 1933, and that in part led to GDP contracting, so debt as a percentage of GDP kept going up. In 1934, the dollar was devalued over 40% relative to its gold peg (from roughly 1/20th of an ounce to 1/35th of an ounce), and the government greatly expanded the monetary base (i.e. “printed money”) to fund all sorts of programs.

A big “deleveraging” occurred because all existing debts were essentially devalued relative to a much larger money supply and relative to the gold peg.

This policy naturally favored debtors over creditors, and turned a deflationary cycle (1930-1933) into a reflationary cycle (1934-onward). It also happened to boost the velocity of money, so nominal GDP went up as well. It was not without major drawbacks, especially for folks who were holding dollars or were creditors that were owed dollars, since the purchasing power of those dollars was diminished.

Total M2 money supply, after having collapsed during the default/deleveraging/deflation period from 1930-1933, quickly doubled over the next several years during the post-devaluation reflationary period:

We can look back into thousands of years of history, through American history, into longer European history, and then deep into ancient Roman and Greek and Mesopotamian history, to see that widespread long-term debt structural problems are often resolved with major currency devaluations and/or outright debt jubilees. Like it or not, that’s just how it goes.

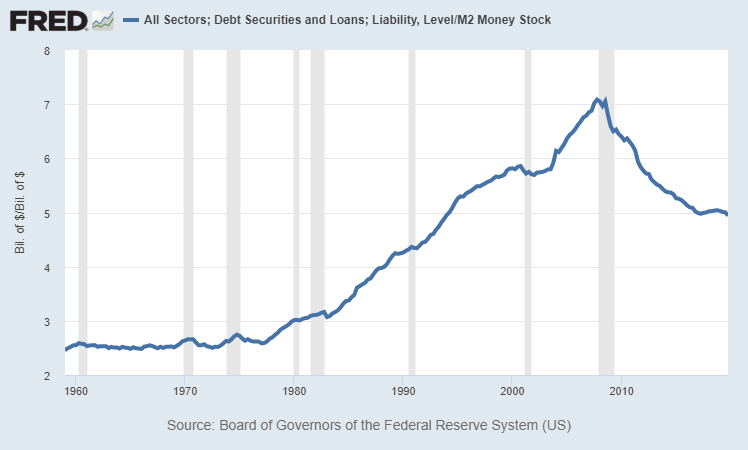

Because the government can control money supply more directly than GDP, a useful ratio to be aware of is the total debt in the system divided by the broad money supply. In other words, how many dollars are promised to be paid in the future (i.e. debt) relative to how many dollars exist now? The higher that ratio, the wider Exter’s inverted pyramid is, at least in terms of that particular measure, which makes it more unsustainable and fragile.

I’ve been tinkering with that Bridgewater/Dalio chart above recently because I wanted a version with post-pandemic May 2020 numbers. Here’s my update and annotation:

Chart Source: Bridgewater Associates, Ray Dalio, Updated/Annotated by Lyn Alden

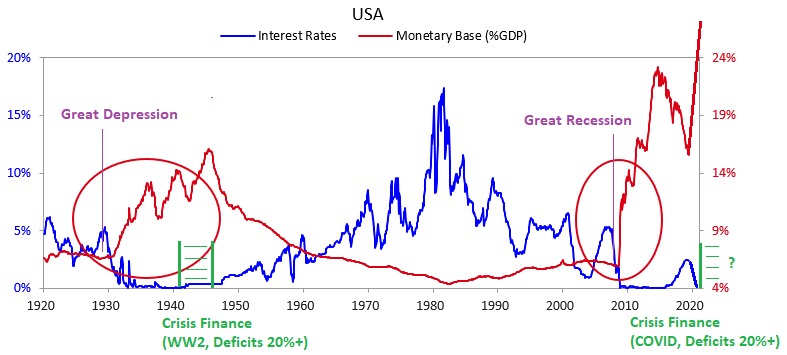

In many ways, the 2010’s were eerily similar to the 1930’s, and the 2020’s are shaping up to be eerily similar to the 1940’s, in terms of fiscal and monetary policy.

Modern Situation

Here’s the recent ratio of total debt to broad money supply over time, as of the end of 2019:

Chart Source: St. Louis Fed

The 1960’s and 1970’s were the low point on the long-term debt cycle, meaning that debt as a percentage of GDP (and as a percentage of money supply) were low. Specifically, the ratio of debt to broad money supply averaged about 2.5x for quite a while.

Starting from the late 1970’s, debt as a percentage of GDP and money supply began accumulating (which not coincidentally, also involved a secular bull market in equities). Debt as a percentage of money supply peaked in 2007 at a ratio of over 7x.

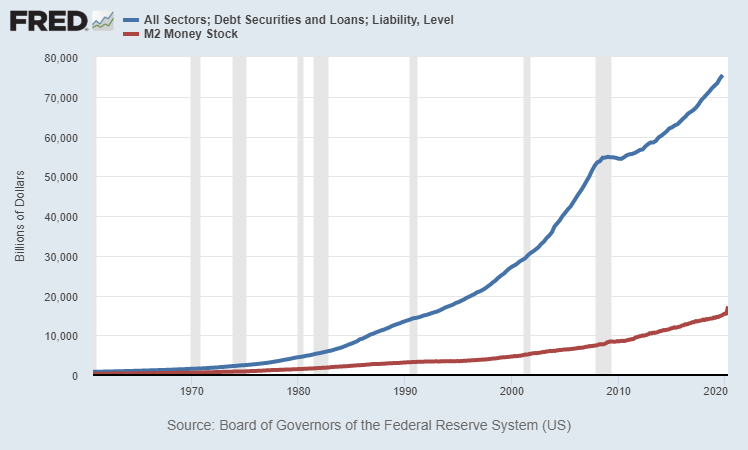

During the crisis of 2008, absolute debt was over $54 trillion and never went down from that point; it trended sideways for a couple years as the private sector deleveraged a bit and the federal government took on a lot more debt, and then total debt started accumulating again. However, money supply grew faster than debt from 2008 and onward, so the debt-to-money-supply ratio went from as high as 7x in 2007 down to only 5x at the end of 2019. This chart shows total debt (blue line) and broad money supply (red line) separately in nominal terms:

Chart Source: St. Louis Fed

In the coming several years, we should expect the ratio of total debt as a percentage of money supply to continue to move closer to 3x or below, and this pandemic recession will accelerate another leg lower. This is in part due to debt monetization; a significant portion of new debt, especially federal debt, is funded by new dollar creation from the Federal Reserve (QE), rather than extracted from actual lenders in the economy as it was prior to 2008. In other words, money supply will likely continue growing faster than total debt in percent terms.

For reference purposes, at the current amount of $75 trillion in total U.S. debt, a 3x ratio or below would be $25 trillion or more in broad money supply. If total debt goes up to $90 trillion in several years, a 3x ratio or less would mean $30 trillion or more in money supply. The current money supply in May 2020 is a little over $18 trillion.

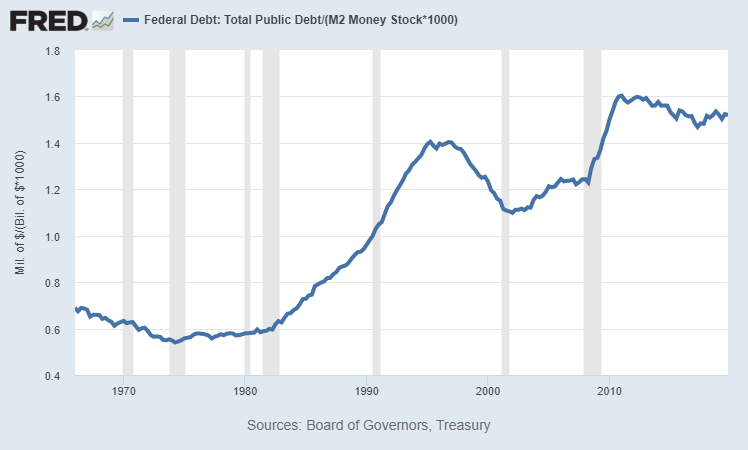

If we specifically look at the ratio of U.S. federal debt to the broad money supply (rather than total debt to the broad money supply), it looks like this:

This ratio was under 0.75 for much of the 1960’s, 1970’s, and 1980’s, but for a while now has been over 1.50, or about twice as high. Because debt moves up to the sovereign level as crises unfold, this ratio is harder to get down without a combination of higher inflation and yield curve control, which are both currently Federal Reserve targets to accomplish according to FOMC meeting minutes and Federal Reserve official inflation targets.

Post-Virus

In response to the economic shutdown that occurred due to COVID-19, fiscal and monetary authorities in the United States and much of the rest of the world spent and printed a lot of money to offset the big deflationary shock and GDP contraction that is occurring. The total U.S. response (fiscal spending plus central bank money-printing) was larger relative to GDP than most other countries so far.

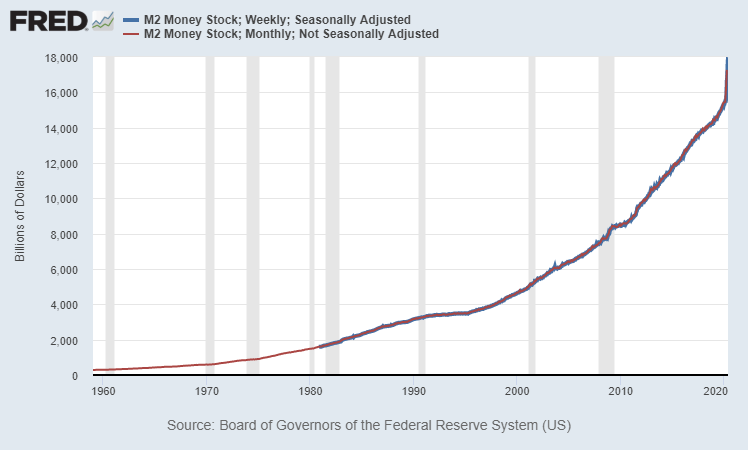

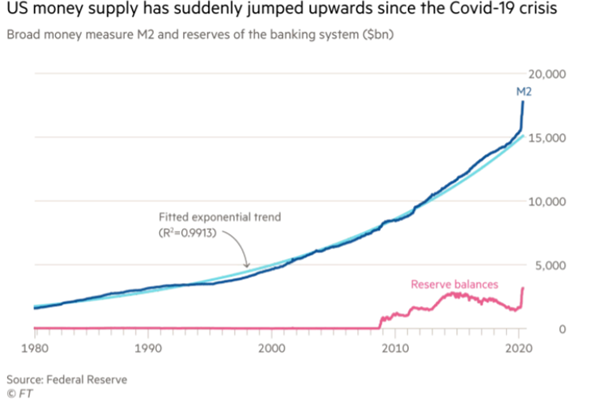

As GDP went down, the U.S. money supply went vertically upward. Money supply started this year at $15.3 trillion and went to over $18 trillion by late May.

Chart Source: St. Louis Fed

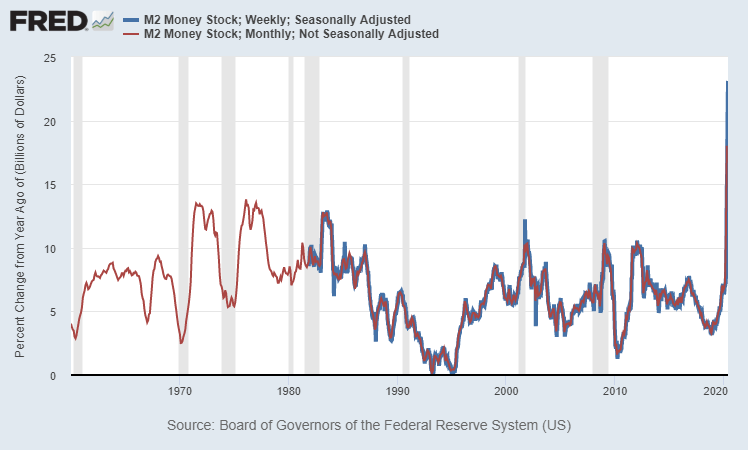

In year-over-year percent change terms, the growth in broad money supply is growing at the fastest rate in modern history:

Chart Source: St. Louis Fed

So, we’re already seeing a narrowing of the pyramid in terms of debt-to-cash, with broad money supply most likely rising as fast as total debt added to the system, which drives the ratio lower.

For example, if total debt has jumped from $75 trillion at the end of 2019 to $79 trillion in mid-2020 (mostly from federal debt increases), and we know that money supply is now over $18 trillion, then the ratio has already narrowed to about 4.4x as of May 2020, from 5.0x at the start of the year.

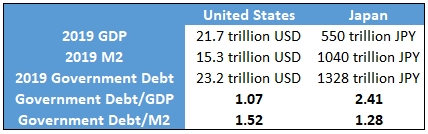

United States vs Japan

Japan often gets singled out as having the most debt relative to the size of its economy. However, although Japan has the highest total debt-to-GDP ratio in the world, the United States has a higher total debt-to-money-supply ratio.

As of the end of 2019, the U.S. broad money supply was only about 0.7x of U.S. GDP ($15.3 trillion in broad money supply vs $21.7 trillion in GDP). For Japan, that ratio was more like 1.9x (just over 1 quadrillion yen in broad money supply and 550 trillion yen in GDP). In Japan, the money supply is far larger and money velocity is far lower.

If we look at government debt, which is the easiest to calculate and display, although Japan has a higher amount of government debt as a percentage of GDP, they actually have a lower percentage of government debt relative to money supply than the United States:

The same holds true for a total public+private debt calculation as well. Japan has more total debt relative to GDP than the United States, while the United States has more total debt relative to the money supply than Japan.

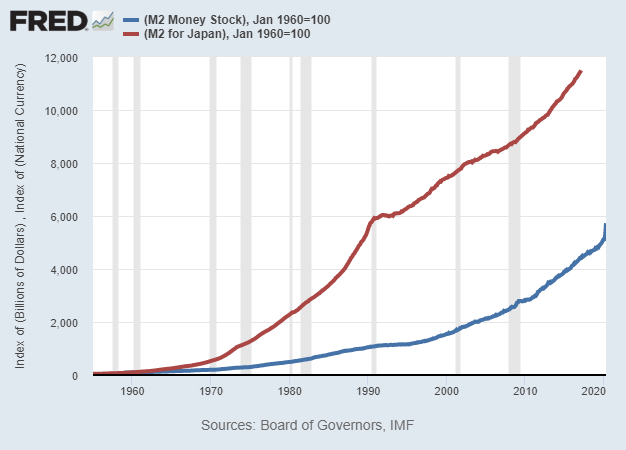

If we chart the money supply of Japan and the United States from the beginning of the data set from 1960 and onward, normalized to 100 in 1960, we can see that Japan’s money supply grew far faster than the money supply of the United States over the long run.

Chart Source: St. Louis Fed

However, if we normalize it to 100 in the year 2000 and chart from there, the United States’ money supply has been growing much more quickly than Japan’s money supply in recent decades:

Chart Source: St. Louis Fed

The same is true if your normalize it to 1990 or 2010, and even if you adjust it for differences in population growth as well. In these more recent decades, US money supply has been growing much faster in percentage terms than Japanese money supply from its existing level. This particular data set charted by the St. Louis Fed ends in 2017 but more recent data from other sources shows that this remains the case into the 2018-2020 period. The United States has been “catching up” to Japan in terms of increasing the total money supply and reducing the velocity of that money supply.

Over the past decade, this is true for the U.S. money supply vs the Eurozone money supply as well, meaning that U.S. money supply has been growing more rapidly from the starting baseline.

In my view, when it comes to currency analysis, too many analysts focus heavily on past monetary expansion (e.g. “Japan has printed a lot more money than the U.S.”), and don’t focus enough on the rate of change of current and future monetary expansion (e.g. “the U.S. is now printing money at a more rapid pace than Japan, and has been for a while”).

Final Thoughts

The ending of the previous long-term cycle and major economic depression in the United States had two phases: one for the 1930’s and one for the 1940’s.

After the 1929 peak, a recession and major asset price collapse began. In the 1930’s, total debt as a percentage of GDP peaked, but it was primarily a private debt bubble. Federal debt as a percentage of GDP was pretty low, while private debt was extremely high. This massive crisis and deleveraging event resulted in a bank crisis and the biggest economic contraction in U.S. history. Money was printed and currency was devalued, but due to the major destruction in other net worth, it was not a very inflationary event. The first few years were outright deflationary, and then the money-printing turned it into a mildly reflationary environment, but the overall decade saw low inflation or disinflation.

1940’s: Federal Debt Bubble, Wartime Finance, Inflation

In the 1940’s, private debt had gone down considerably as a percentage of GDP due to all of this deleveraging and expansion of the money supply, but due to World War II, federal debt as a percentage of GDP skyrocketed. This era of wartime finance was inflationary due to massive spending and industrialization, with peak federal deficits exceeding 30% of GDP. However, the Federal Reserve used yield curve control (which was basically quantitative easing; creating dollars to buy Treasuries as needed) to peg Treasury bond yields to 2.5% or below despite higher inflation. Therefore, Treasuries significantly under-performed inflation for the decade and the government effectively inflated away its excess debt.

So far, we have an echo happening in the 2010’s and 2020’s.

After the 2007 peak, a recession and major asset price collapse began. Total debt as a percentage of GDP peaked in 2008, but it was primarily a private debt bubble. Federal debt as a percentage of GDP was moderate (about 65%) at the start of the crisis, but quickly grew to over 100% in the subsequent years as the private debt bubble was mainly pushed up to the sovereign level. The massive deleveraging resulted in a bank crisis and the biggest economic contraction since the Great Depression. Money was printed via quantitative easing, but due to the major destruction in other net worth and several deflationary forces, it was still a disinflationary environment rather than inflationary environment, outside of certain key areas such as healthcare.

2020’s: Federal Debt Bubble, Pandemic Finance, Inflation?

In the 2020’s, private debt has gone flat for a while as a percentage of GDP (household debt is down while corporate debt is up), but federal debt began skyrocketing from an already high 106% of GDP baseline level in early 2020 due to the pandemic and subsequent economic shutdown. Federal deficits of 20-30% of GDP in 2020 have approached World War II levels for the first time in modern history, resulting in federal debt levels rapidly moving to 120-130% of GDP and likely higher in the years ahead. The Federal Reserve began discussing yield curve control in 2019, bought a massive amount of Treasuries in mid-March when foreigners sold over $250 billion in Treasuries and yields briefly spiked, and in recent FOMC meeting minutes they discussed yield curve control via ongoing Treasury purchases.

In line with a reflationary or stagflationary outlook combined with yield curve control from the Federal Reserve, I continue to be long-term bullish on precious metals in this environment, with a particular emphasis on silver at the current time. For this decade I also like certain cheap value/cyclical/foreign sectors over expensive growth/defensive/tech sectors broadly (when carefully-selected, with strong balance sheets and high returns on capital).

Louise Gave was interviewed by Tyler Hay of Evergreen Gavekal on above topics.

Summary

On Supply Chains

I think the question around global supply chains is already a big focus of the US presidential campaign. The arrow in President Trump’s quiver is to say that this all happened because China is an untrustworthy partner. There’s going to be tremendous pressure on industries coming out of this to reduce their exposure to the international supply chain.

I wrote a piece at the beginning of this crisis called “Exponential Optimization.” I think that if you look at the past decade, we’ve lived in a world where everything has been optimized as much as possible. That includes optimizing balance sheets, share buybacks, and portfolios; but it also meant optimizing the supply chain. If that meant businesses could find a producer in the middle of Wuhan, China that would produce goods cheaper than alternatives, then they would do business there. Of course, the idea of producing things in Wuhan might no longer seem like the best idea.

One of the first things to look at when constructing a portfolio is how much government pressure will be placed on a business to produce at home rather than in China, which will undoubtably impact margins. Take healthcare as an example. We live in a world where 90% of antibiotics are produced in China. Is that something that the government will feel comfortable with going forward? My guess is that drug companies around the world will be told that if they want to sell their drugs somewhere, they have to be produced at home without regard to cost. We can’t live in a world where all of our drugs are produced somewhere else.

We had a 30-year stretch of globalization in the supply chain, but it turns out that finding the cheapest producer actually has an embedded cost that we weren’t recognizing. Now that we’re recognizing this cost, we’re finding out that it’s actually really, really high. I think there will be big disruptions to the global supply chain and people will probably want to invest in companies that aren’t going to be massively dislocated from needing to relocate their supply chains.

On Inflation vs Deflation

As a firm, Gavekal has been firmly in the deflationary camp for years and years. The reason for this is that every shock to the system was a fundamentally deflationary shock in that it didn’t really reduce supply – in fact, it often increased supply – but it did destroy demand. If you take the 2008 crisis as an example, we saw Quantitative Easing (QE) 1, 2, and 3, and a lot of people made the case that this was going to lead to a massive inflationary problem. But what people missed is China’s response to the crisis. It went on a capital and infrastructure spending boom such as the world has never seen. Up until 2008, if you were producing in China that meant you were either producing in Shenzhen or Shanghai. The production base for China was actually relatively small at that point. After the huge infrastructure spending boom China went through in 2008, you could produce in many other cities in China. The 2008 crisis resulted in nearly 500 million Chinese workers joining the global economy, which was a fundamentally deflationary shock. At the same time, oil prices were at $150/barrel and companies were pouring into new production all around the world. As money poured into energy infrastructure, oil prices came down over the next several years and today we’re much, much lower. Of course, the current economic hit means a destruction in demand, but the big question today is what happens to supply. What I see in the energy space is capital spending being slashed, so if I’m projecting three years down the road, I don’t think there will be an increase in supply of energy but a deterioration in the supply of energy.

Similarly, I don’t think that there will be an increase in the supply of workers. I think that the world will turn their backs on the Chinese workforce. Instead of bringing a supply of 500 million workers to the global economy, we’re going to be pushing them back. So even though I see a destruction in demand, for the first time in quite a while, I also see a destruction in supply. In fact, this entire crisis is really about a destruction in supply. We’re now seeing it in industry after industry.

My big fear is that if you look at the TIPS market (Treasury Inflation-Protected Securities), it’s now projecting inflation of 1.1% every year in the US for the next ten years. Aside for 2008, the US hasn’t had an inflation rate of 1.1% in the modern era. Now we’re supposed to have 10 years in a row?

Right now, the rate of inflation is 1.5%. What happens over the next six months if, instead of going to 1.1% as the market anticipates, inflation goes to 2.0% or 2.5% as the result of supply chain disruptions? I think that would create a whiff of panic in the markets. I’m much more afraid of inflation that’s not priced in, than deflation that’s fully priced into markets.

From a purely macro perspective, the emerging market and reflation story of the 2000s was a reflection of the exciting macro story of that period, the rapid growth of Chinese exports

The macro story of 2010s has been the tremendous growth in US oil and gas production, to make the US the world’s largest energy producer, and to turn the US from an energy importer to exporter.

The tune – Core periphery model– Let me explain the components of this model

Core = US Dollar

Periphery = Rest of the world

1st half money moves away from core fueling rally in Periphery (emerging markets)

2nd half …The combination of slower Chinese growth, rapid oil production growth led to a collapse in oil prices, contributing to suppressed inflationary pressures, and this has precipitated a collapse in bond yields as central banks have desperately tried to reignite growth.

Rise in oil supply by shale + existing suppliers

Led to Deflation

Which led to

which further led to

Safety trades comprising of high tilt towards growth stocks + gold + long dated bonds

So what do we see happening

Many of these trends will reverse

Well the US shale boom seems to be ending which means us will be a net importer again and restart dollar weakening cycle.

With an uptrend of regulation moving towards the growth sector comprising highly of tech sector and a wave of regulatory green shoots regarding free riding of media platforms on free content we see entry of regulation as a reversal of the growth stock trend. The other parallel is like the dotcom bubble we live in the offload risk on to others platforms and a bubble based on Machine learning.

All this money from growth stocks will mean revert to Value stocks which have underperformed growth for better part of the last decade

Silver might start outperforming GOLD…..

and yield curve might start to re steepen again with help from short term yield capped by central banks.

Most investors are not ready for the change in this narrative and by the time they start repositioning their portfolio to reflect the new realities… major gains would have already been made.

I am talking about my favourite asset i.e Silver .

Gold/Silver ratio hit an all time high ratio of 1:120 in march this year and since then silver is silently outperforming GOLD with this ratio breaking down below 1:100 ( silver outperforming GOLD).

according to Midas Touch consulting

At this moment of time it takes about 97 units of Silver to purchase one unit of Gold. The monthly Gold/Silver-Ratio chart above illustrates that nine years ago it took only 31 units to accomplish the same purchase. Relationships like these rarely stay long in extreme measurements like the two mentioned. Consequently, it is quite reasonable to assume that we will at some point find ourselves near the 200 moving average, a value between those two extremes more likely in the future. Once Silver which is always late and lags, catches up with Gold’s extension, this medium Gold/Silver-Ratio zone will be reached. This means there is a force in place driving Silver prices still higher.

Julian Bridgen of M12 Partners write

After hitting our initial target around $100, the market chopped sideways for a week. But now, the Gold/Silver ratio appears to be starting the next leg. My target is the mid-80’s … a lower gold/silver ratio is historically inflationary!

The best way to capture Silver upside is through Silver Miners.

Keith Dicker has taken us to the uncomfortable corners of the investment world in this month’s newsletter.

The link to newsletter is attached below but I thought of sharing this chart from his newsletter which clearly depicts the outcome of massive money printing across the globe

Federal reserve Bank dusted an old trick to kill two birds with one stone.

Federal Reserve Bank of New York President John Williams said policy makers are “thinking very hard” about targeting specific yields on Treasury securities as a way of ensuring borrowing costs stay at rock-bottom levels beyond keeping the benchmark interest rate near zero.

“Yield-curve control, which has now been used in a few other countries, is I think a tool that can complement -– potentially complement –- forward guidance and our other policy actions,” he said in an interview Wednesday on Bloomberg Television with Michael McKee and Jonathan Ferro. “So this is something that obviously we’re thinking very hard about. We’re analyzing not only what’s happened in other countries but also how that may work in the United States.”

This will not only ensure a lower value of USD and increase the inflation expectation but also lower the DEBT/GDP by inflating away the debt.

The same remedy was applied by US in aftermath of WW2 nation building.

The default on bond obligation was more nominal than real. With cap on bond yields and increase in spending, the real interest were negative for better part of decade. The smart money went in search of returns and that decade was one of the best period for US equity markets as higher inflation and lower bond yields coupled with war spending led to higher corporate earnings and reduced the over all Debt/GDP of the US economy.

Conclusion

Fed is increasing floating trail balloons about yield control and I believe we might see the post WW2 playbook again which will lead to -3% to -5% real rates in US in next few years. This will be the decade when real assets makes a come back.

3.Tail end consequences of a phenomenon occurring.

As this crisis and almost every decade we find our financial system being dominated by players who concentrate on the first two aspects of risk and not the last one. These funds like a few quant funds had risk party executed using low vol strategies which blew up even in the face of fed backstops.

These tail risk events don’t matter until they suddenly are the only thing matters as the market swings from purchasing power risk to principal risk. Now is there a class , textbook or special coaching that can allow you to think about tail risk. And the answer seems to be no because such a calculation is not rationally possible by the brain nor is it possibly computable in the fundamentally uncertain universe, we live in.

It is over here that experience or trauma matters because these memories can fundamentally reshape your risk aversion and perception through its effect on the hippocampus and Amygdala of the brain.

The author recounts his own experience where he and two of his other friends would go out skiing sometime in places that they weren’t allowed to as they were prone to avalanches. This one time he actually faces an avalanche that does not turn out to be life threatening but buries his feet in the snow , all the friends laugh it off but he was clearly shaken. The next time he went skiing again with his friends on being asked to ski the dangerous parts again , he unconsciously said no. The author makes the point that these unconscious decisions can affect our lives for better or worse , much more than the conscious decisions which fall into the first two categories of risk.

In investing, the average consequences of risk make up most of the daily news headlines. But the tail-end consequences of risk – like pandemics, and depressions – are what make the pages of history books. They’re all that matter. They’re all you should focus on. We spent the last decade debating whether economic risk meant the Federal Reserve set interest rates at 0.25% or 0.5%. Then 36 million people lost their jobs in two months because of a virus. It’s absurd.

Tail-end events are all that matter.

Once you experience it, you’ll never think otherwise

As the Long-term debt cycle dynamics become more important as the day passes. This crisis has been one where we have had demand and supply side contraction at the same time. The current scenario signals deflation and may also render previous inflation indices meaningless.

While previous money printing by central bankers had to led to hyper inflation , Current US M2 shows large jumps in growth , so a combination of constrained output along with rapid monetary growth may signal inflation , if velocity of money follows an uptrend. However , just like the last bout of inflation in the 1970s an unexpected surge in inflation might come about as supply chains fray. The supply chains are concentrated and more fragile than ever before, for example the shutting down of one Tyson food plant had affected 4 to 5% of pork supply in the US.

The probability of highly fragile structures failing and leading to inflation cannot be downplayed and deserves a much important role in portfolios. As a trader remarked on CNBC that the bond market almost universally expects deflation which means there will be inflation.

The problem is if we see the worst possible outcome i.e STAGFLATION. The supply chains are going to be reshored, inventory buildup is no more going to be Just In Time but more long term and this will increase the use of working capital. I agree, the demand will take time to recover, but for STAGFLATION, you don’t require high demand but a reduction in supply.

I believe the outcome of COVID will be a STAGFLATION and don’t count on bond markets to tell you that because any signs of INFLATION/STAGFLATION will lead to capping of yield by central bankers.

In the chart above of US 10 year treasuries you can see that yields are now confined to a range. whether by design or market forces will determine the future performance of different assets.