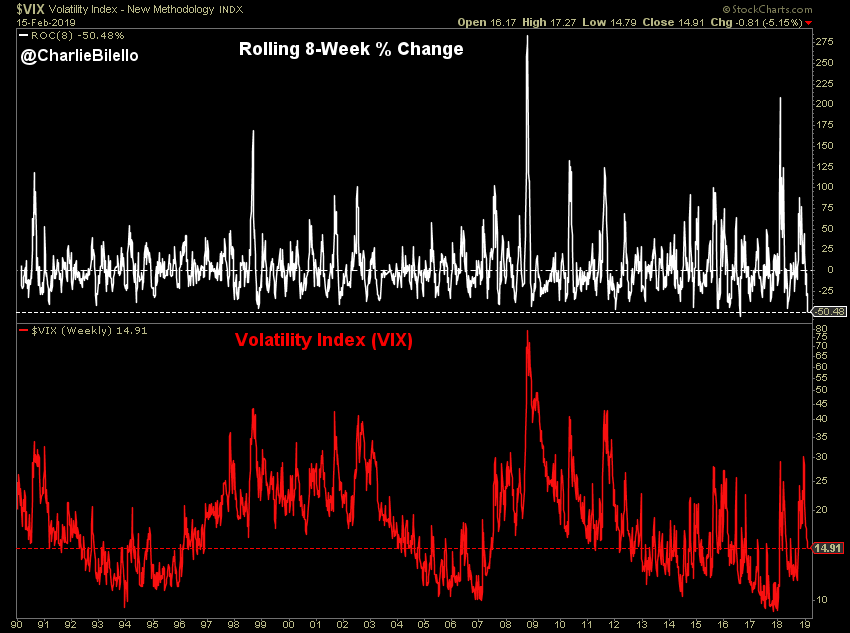

Just 9 weeks ago the Volatility Index closed at 30.11. Today it closed at 13.51. At -55%, that’s the largest 9-week decline in history.

Vol has been smashed even though Fundamentals are weaker, Political Risk higher, and Society more volatile.

One reason could be China’s total social financing (TSF) growth surged to its highest level on record last month, indicating that Beijing’s recent push for more lending to offset a slowdown is taking effect,Caixin reports.

TSF, a gauge of the economy’s credit and liquidity, rose to Rmb 4.64 trillion ($684.93 billion) in January – a big jump from December’s reading of Rmb 1.59 trillion, according to People’s Bank of China data. This mindboggling credit growth Liquified the system and allowed the volatility to be kept suppressed.

This will reverse just as violently as it was smashed.

All the major economies are over indebted with Japan being the most followed by Europe, U.K, China and the US. Japan particularly have found itself in adding debt since 1944 first when debt grew faster than income during pacific war, then the Japanese asset price bubble collapsed in late 1980s causing rapid increase in debt to GDP ratio and then Fukushima disaster of 2011 also had a negative impact on current account surplus of Japan.

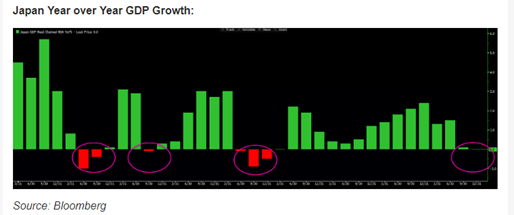

In past decade, Japan had four contractions YoY GDP growth. Each time economy is met with small spurt in growth, negative growth ensued. Raising the interest rates trims the economic growth even further proof of which lies in bubble collapse due to hike in lending rates by BoJ. Over indebtedness produces inherently weak aggregate demand which makes the economy subject to downturn without cyclical pressures.

There are four

variables that affect monetary policy: interest rates, inflation, exchange

rates and growth.

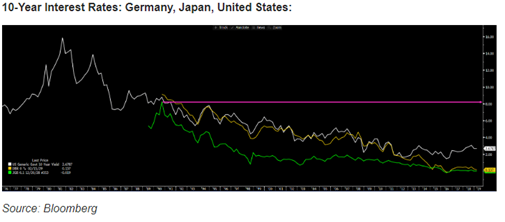

In Japan, while both net and gross debt increased over time, level of net debt is far lower than level of gross debt because Japanese government owns large amount of domestic and foreign financial assets in form of loans, bonds etc. Majority of Japanese bonds are purchased by BoJ which insulates it from changes in global bond market. Remainder of debt is financed by domestic creditors.

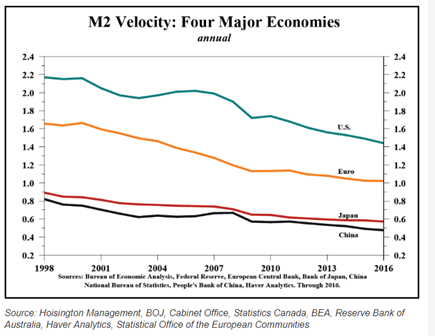

Central banks can control short term interest rates and size of their balance sheet but they cannot control money supply. As velocity of money declines, monetary policy is increasingly ineffective. As debt burden grows and productivity growth declines, velocity of money crashes.

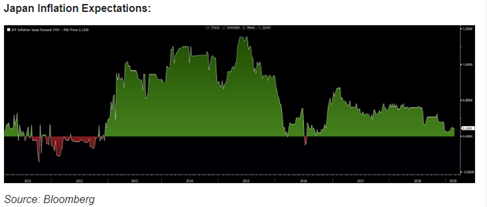

In Japan, long term rates are at 0%. Long term interest rates are built around the expectations of future inflation. Japan’s inflation expectations is also at 0% .

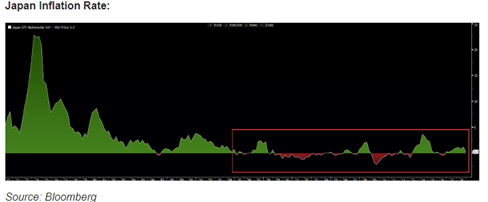

Economy that is over indebted can be seen in persistent disinflation or outright deflation. In Japan, deflation has arrived as the headline CPI rate has remained negative for many years. Yen is a great barometer of this deflation and I would be watching Yen weakness carefully to see any incipient signs of impending inflation.

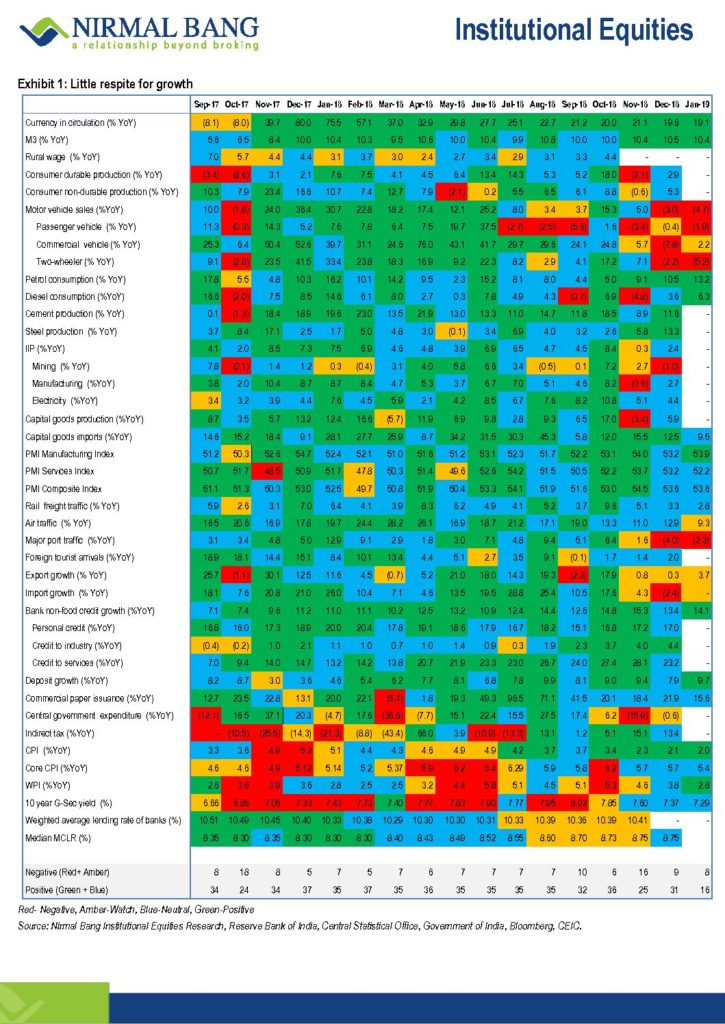

India Macro Economic Real indicators have been slowing down- as of Jan 19- Only 66.7% of indicators in positive territory in January down from 77% in December 2018.The govt is too indebted to do any meaning full capex. Corporate India is shying away from investing due to regulatory, political and technological uncertainity. Household were holding the forte till last year by going on a borrowing binge but that has also come to a halt.

Financial markets now believe that RBI will come out to rescue the economy by adding LIQUIDITY and cuting rates. I think they will try to experiment with easy money policies but the economy might not react so positively because India’s aggregate levels have been increasing faster than nominal GDP growth making it difficult for lower rates to provide meaning filip to the growth.

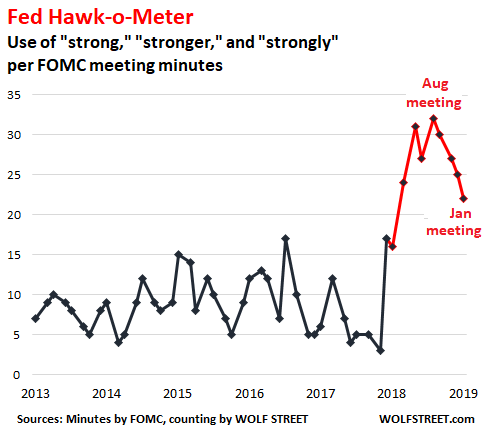

In the minutes of the January 29-30 meeting, released this afternoon, the mentions of “strong,” “strongly,” and “stronger” edged down for the fourth meeting in a row, this time by three points, to 22. The Hawk-o-Meter has now backed off quite a bit since the August 2018 high – when the Fed was rubbing it in that it would raise rates four times in the year – but it is still in outlier territory and redlining.

The G7 GDP volatility continues to trend lower.

A UBS tracker puts global growth at the weakest in a decade, with Germany & Japan seeing the biggest slumps in manufacturing

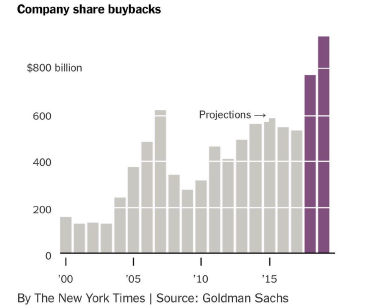

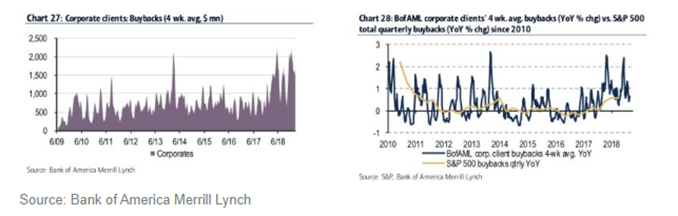

Nice chart showing the money companies spent during last 10 years on CapEx ($6.4T), buybacks ($4.9T) and dividends ($3.4T)

Recall the time

when David Einhorn came up with a devious idea of iPrefs to distribute the

massive cash that Apple was chewing among its shareholders in 2013. Instead of Apple

bowing to this idea, announced one of the biggest share buyback program and

planned to increase their dividend multifold to pacify investors demanding return

of their invested cash. Lesser known fact is that Apple had more than $130

billion in cash not in US but in Ireland and deploying a buyback would have required

them to bring that cash back in the States and pay huge taxes. Quick – witted Apple

did not disturb its cash sitting overseas but instead funded the buyback

through debt issuance and repaid the shareholders dividends through that loan.

It also committed itself to distribute over $100 billion to shareholders by the

end of 2015.

Since then,

Apple have being repurchasing shares frequently which has increased its share

price and ROE and kept their investors elated. The new normal for young

companies and big technological companies is to keep huge amount of cash in

their war chest and argue its necessity in future technological advancements

projects or acquisitions or a million other reasons. Yet, these companies have

kept their shareholders content by distributing dividends or repurchasing

shares and made their EPS look good.

Flushed with

savings from lower tax rates and profits from a growing economy, big US

companies collectively spent a record amount of $1 trillion buying back their

own stock in 2018. Many argued that this led to further income inequality and

these companies should have invested the excess cash internally on projects or

by paying more wages to workers than distributing it to public. Some countered

by standing strong on theory that buybacks indicate a positive turn in a

company where these companies believe they are being undervalued by the market and

wish improve their valuation. Ed Yardeni of Yardeni Research points different

motivation for share repurchases and says, “S&P data suggest the aim of

buyback is to reduce dilution from stock compensation rather than to boost

EPS.”

However, JPM estimates $400B of cash was repatriated between Q1 and Q3 while $190B was used for buybacks, $90B for corporate bond withdrawals and only $75B for Capex.

Buybacks funded

by debt issuance rose from 8% in 2010 to 32% in 2016 and the opulent brands

like Apple, Oracle, Microsoft, Cisco and many others announced big buyback

programs in 2018. Few argue that these

companies have exposed themselves to risk where if Fed goes in complete QT mode,

it would threaten these equity stocks.

Right now, major

shareholders like Mark Zuckerberg who owns stock in companies that use

repurchases exclusively can defer their own tax and their heirs can avoid taxes

altogether thanks to a loophole in tax code known as step – up in basis. Sen.

Marco Rubio proposed a fix for this as opposed to proposals by Sen. Bernie

Sanders and Sen. Chuck Schumer who suggested blocking the buybacks altogether.

When tax cuts

increased budget deficit, Republicans believed that tax cuts would boost

business investments. That didn’t happen and Rubio’s proposal tries to solve

this mystery.

Essentially, Rubio proposed that buybacks should be subject to same tax code as dividends i.e. would get taxed immediately instead of waiting for shareholders to sell the stock and also allowing these companies to immediately and fully deduct the cost of new investments, thereby making it more attractive.

The debate between two mind-sets in which one supports huge buybacks of 2018 emphasizing that it kept the money in circulation in the economy and boosted consumer confidence, other set effectively are of belief that excess buybacks could lead to stagnation of wages, increased inequality by enriching shareholders and executives. Corporations funded the buybacks from tax cuts instead of investing cash in internal growth. Rubio’s proposal implicitly aimed at making corporates think twice before repurchasing the shares and explore other value propositions rather than solely focusing on boosting EPS and be always in pursuit of higher ROE. Investing for long term and efficient use of cash could also keep fundamentals aligned as well.

WTO outlook collapsing faster than anytime since 2009.Something is not right but fear not Central Bankers will open another spigot of money.

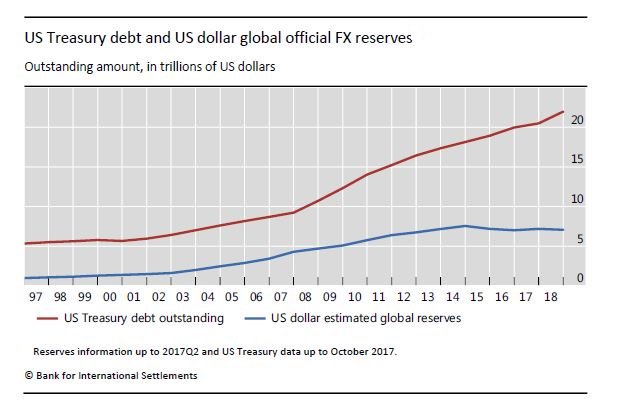

The supply of Risk free asset is rising faster than the demand from reserve managers. who will fund this?

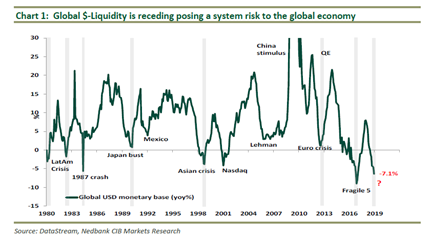

The world monetary base is shrinking, only the sixth time since 1980 – each prior episode resulted in massive losses in Asian/EM equities (1982: -31%, 1990: -14%, 1998: -28%, 2000: -32%, 2008: -54% for EMs). In all five cases, Asia was in recession.

“The correlation of EM equities with the major central banks balance sheets is 0.94 in the past three years [and] world equities have a similar correlation of 0.94 since 2009”, BOFA writes before asserting that “central bank balance sheets are the most important driver of stock prices, in our view, by lowering risk premia, and cutting off deflation risk.”

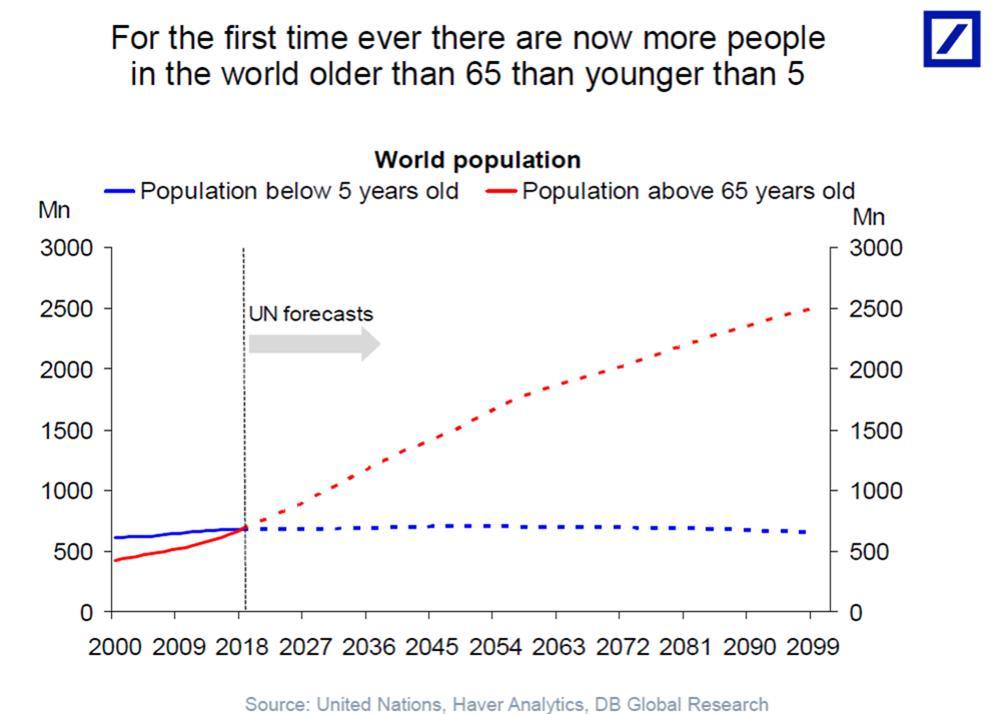

We’re running out of time, as a world, to fix our demographic problems. We’ve spent 20 yrs papering them over in debt + bubbles. It doesn’t get easier from here, and in fact it gets far worse, far faster. Many of these will be people who can sadly never retire.

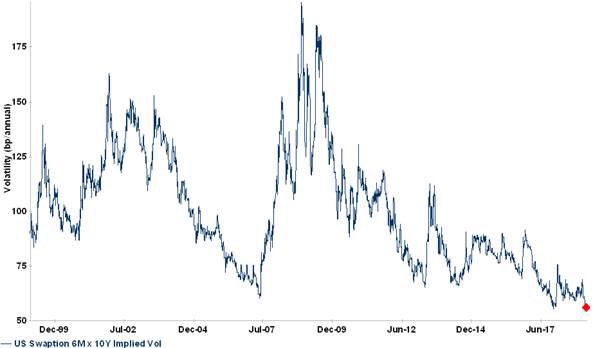

US rate vol at an all time low…..in fact the rates volatility has collapsed across the world

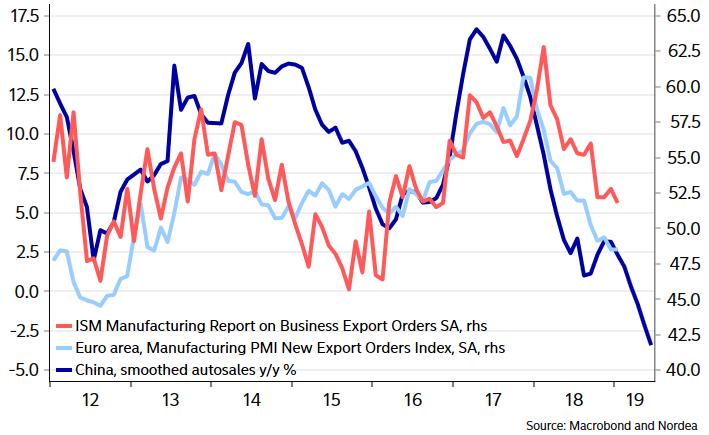

Chinese auto sales figures are plummeting ! Expect US and Euro area export orders to suffer more than already seen. China in itself is probably past the worst part, spill-over effects to US + Europe are still increasing. China currently awaits a meltdown in US manufacturing

Gold nearing the real test.

Extreme overbought and over bullish – Daily RSIs / DSIs:

Gold 73 = Highest since Sep 2017. DSI>85? Highest since Jan 2018.

US spends $8T more than trend to get 2% GDP growth it used to get organically. Businesses see the $8T + lever up; so do consumers. Asset bubble #3 fueled by that $8T. When bubble bursts, millions hurt again.

When crisis hits

you, you learn a lesson, lesson everyone makes sure you never forget. They get

written down in history and teach you forever. When it comes to financial

crisis, from Tulip Bulb craze to The Great Depression to 1987 crash to 1997

Asian crisis to 2007-08 Financial crisis, all events taught us a moral & financial

lesson and prepared us for the next crisis. With top risk management practices

in place for corporates, they diligently manage the firm and social

responsibilities. But what if the next crisis is not the result of

irrationality of mob or fraud by corporates but by the Government itself

consciously (or it seems so).

Such has happened recently when Fed hiked the rates and reduced its Balance Sheet in chorus knowing the beats would resonate and destabilize the global economy. Both actions of Federal Reserve in combination sucked up the global US Dollar liquidity.

With US – China trade war, the dollar became strong, their exports were less attractive but again did Fed’s policies had a direct impact on liquidity? China being the significant contributor to credit growth, growth in China’s economy leads to growth in global trade. With growing global trade and 90% settlement in USD, there is excess supply of USD in system, which eased financial condition globally causing weaker USD. Thus, Fed’s policies might not be the only driver of global liquidity. The global trade wars are a potential source and risk factor affecting global liquidity negatively.

Chinese bank’s foreign exchange sales have been steadily increasing showing a considerable amount of outflows from country. Despite this, strangely their currency reserves remain stable!

Emerging market equities were 20 – 30% lower from February to October, credit markets (bonds) didn’t fare much either. Along with this, the tariffs placed by US government on manufacturing turned things slow. After all, over $60T of global GDP is outside US.

The

impact on market sentiment is much larger than meets the eye. When liquidity is

being removed, investors sell assets and avoid buying risk assets during weeks

when Fed is actively reducing size.

JP Morgan Strategy Research, 17th January, 2019.

Where does this leaves us then? Are the charts which were developed to prevent crisis indicating that one is anyway near us and this time the fault isn’t of institutions and of the mass but of ‘You – Know – Who’ and this wrecking ball is hitting everyone.

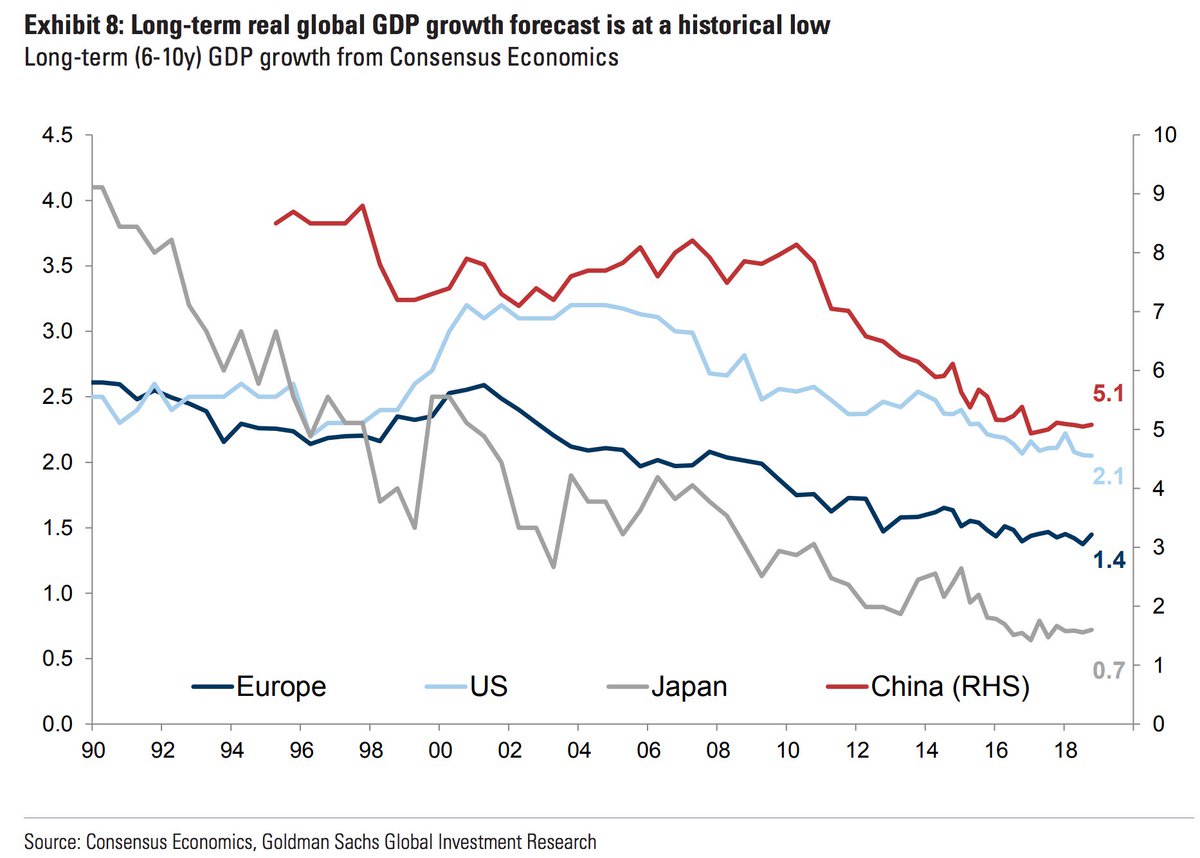

Long-term real global GDP growth forecast is at a historical low despite the move towards zero interest rates, the large expansion of central banks’ balance sheets and the substantial fiscal expansion in the US, Goldman shows. Trend growth has been slowing everywhere since GFC.

China’s biggest weakness is its dependence on semiconductor imports, primarily from US companies. China manufactures only 16% of the semiconductors it uses locally. Last year, the country spent $260 billion on chip imports, a value exceeding its oil imports. By interfering in the supply of semiconductors, America could choke China’s technological ambitions. Given that China will rely on US technology imports for the foreseeable future, Beijing may have little choice but to play by US rules in 2019. The corollary is political risks are diminishing rather than intensifying, as is widely perceived. Nearly half of economists surveyed by The Wall Street Journal said they viewed the US dispute with China as the biggest risk this year.(Stray Reflections)

The global fiscal impulse, which measures how much governments’ fiscal policy adds to or subtracts from overall economic growth, is set to turn even more positive this year. Fiscal deficits in four of the world’s biggest economies—the US, Europe, Japan and the UK—will rise to 3% of GDP in 2019, from 2.8% last year. The IMF expects the US fiscal impulse to reach almost 1% this year. Investors are making a huge mistake in their forward-looking evaluations by focusing exclusively on monetary policy. Central banks do not matter as much now that fiscal policy is taking over.

The foundations on which the shale boom was built is coming undone: cheap money, lower costs, rising productivity, and risk appetite. All-inclusive break-evens are about $51 in the Permian, $57 in the Eagle Ford and $64 in the Bakken. Oil prices at current levels will therefore start to drag on business investment in the coming year. Three aggressive independent Permian upstream operators have cut capital budgets by at least 12% to 15%. Shareholders are pushing companies to conservative capital spending plans and focus on free cash flow generation. The rig count is no longer increasing. There are signs oil productivity is also peaking as drillers have burned through their best assets. If the increase in shale oil production this year is more tepid than what many people are predicting, oil prices will move higher. Almost all other forms of oil supply have declined over the past few years. We see a drawdown in global oil inventories in 2019.(Stray Reflections)

Electronics exports from Singapore – the global hub of fabrication – plunge 15.9%, worst in 5 years. This is not just China – global trade has fallen off a cliff

Edward Gofsky write “Big Picture, this is a great chart of the bullish scenario for gold . I am personally waiting until gold gets over $1400 and silver over $21 before I get aggressive. If this does play out in the future it could be a massive 10 year {C&H}“

Eurozone slowdown. This is what the European Commission called “robust recovery”? European car sales plummet in January after five months of bad data.

India Kissing Goodbye to Demographic Dividend- CMIE

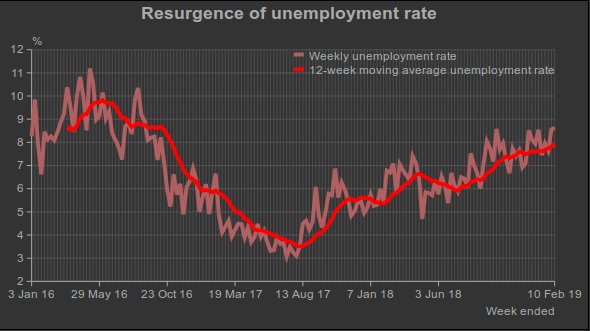

India’s unemployment rate continues to rise. It has been rising steadily since July 2017 when it had reached its recent low of 3.4 per cent. The relentless rise in unemployment led to it peaking at 7.4 per cent in December 2018. Then it fell to 7.1 per cent in January. But faster-frequency estimations such as the weekly estimates and the 30-day moving average suggest a resurgence of the unemployment rate in February.https://bit.ly/2DuBWzd

The Volatility Index has been cut in half over the past 8 weeks, the 2nd largest 8-week decline in its history.

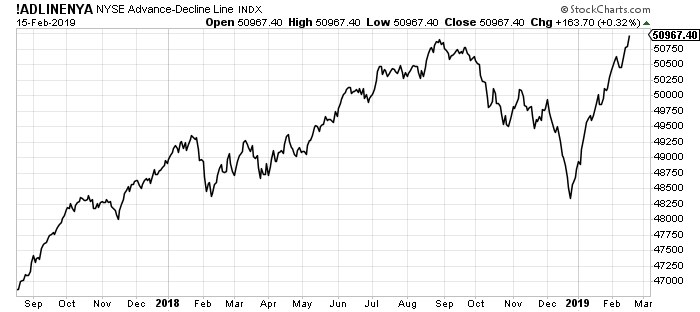

But the breadth is too strong. Probably the best breadth in Developed world market. What am I missing?