Executive Summary of the In Gold We Trust Chartbook

A Turn of the Tide in MonetaryPolicy • Events in Q4 clearly showed that a “monetary U-turn”is currently on its way, which means that further large-scale experiments like MMT, GDP targeting and negative interest rates might be expected in the course of the next severe downturn. • We might already be in a prerecession phase. Crisis-proof assets will probably be in greater demand again in the coming months.

A Turn of the Tide in the Global MonetaryArchitecture • Renunciation of the US-centric monetary order(“de-dollarization”) is now making headlines. • Geopolitical tensionsare increasing: Trade wars -> currencywars

Gold‘s Status Quo • 2019 ytd, gold is up in almost every major currency. In many currencies (AUD, CAD) gold trades at or close to new all-time highs! • Despite the rally that started in August of last year, sentiment is still bearish.

Gold Stocks • Mining stocks are in the beginning of a new bull market. Creative destruction has taken place, and leverage on a rising gold price is higher than ever. The mega-merger between Barrick and Randgold might have marked the bottom. • Gold & silver mining stocks are probably one of the most hated asset classes these days. We are convinced that the capitulation selling of the last couple of years now offers investors a very skewed risk/reward-profile.

The HUI/SPX ratio currently stands at a similar level as in 2001 and 12/2015, when the last bull markets in gold stocks set in

Now time for some REALTALK from the philosopher / pseudo-economist deep inside of me:

Low interest rates are (ultimately) deflationary, sustaining zombie-firms in a “liquidity-trap,” which weigh on overall economic performance while also weakening investment.

Low interest rates and QE are deflationary as you incentivize mal-investment and blow perpetual speculative-asset bubbles, which (ultimately) correct and drive deleveraging—thus the ‘balance sheet recession.’

As there is still a lot of debt-related “scar tissue,” you can’t push credit on a string. This then leads to quick “muscle memory” returns to a defensive posture: “If there is no return on capital, capital should not be deployed.”

Now we see the Fed “stuck on this hamster wheel” because neither markets nor the economy apparently can withstand a rising interest rate environment.

He concludes “ Long-term ‘inflation expectations’ will never truly be move higher without full-scale fiscal stimulus (or the future-state of outright ‘helicopter drops,’ shudder)…because debt, disruption and demographic forces are too strong. #BUYBONDS and #PASSOUT”

Emerging Market spreads are inversely proportional to the US Dollar and recession causes strong US Dollar, not the other way around. These are two basic notions in economics and these two possess the capability of creating a havoc. These notions are driven by many factors which causes skewness in the upside or downside depending on risk taking capability of the investors and this gives central banks globally a huge responsibility to make decisions not only to advance the country domestically but also to analyse how the decision may affect other economies. In today’s scenario, who holds all the cards? US? China?

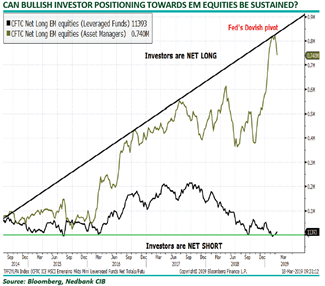

Fed was hawkish in 2018, Europe which is still weak, US Tariffs & US – China trade war sucked global dollar liquidity and already fragile economies went pale. A strong dollar causes damage to external economies, people lose their purchasing power and most affected by are emerging markets. When balance sheet reductions paused, Fed also became dovish, trade war silenced, this change in stance made room for dollar to weaken. A weak dollar saw inflows in EM economies and the stocks rallied. Investors became cautiously bullish in their net positions and have already priced in ‘no change’ decision of Fed in 19-20 March meeting leading to stability in the markets for now.

Fed has no

option but to shift from being hawkish as higher interest rates causes tight

financial conditions and global economic weakness. Hiking further would not

only bleed the world but US too. US is currently locked in with China’s economy

and inch away from the double edged sword with all the cards which they once held

shifting into Chinese hands. In rear view, China seems to be driving the

decisions of Fed. A weak dollar makes a strong Yuan, a strong Yuan makes not

only Chinese economy healthy but all the neighbouring and emerging market

economies. A world where USD and Yuan move together have never existed, the

world reap benefits from their negative correlation. Even though China is

currently witnessing a slowdown, forex is always to the rescue with Chinese

realising gains from strengthening Yuan and falling inflation, boost from

imports from its trading partners and also leading a way for Trump in 2020

election. This economic cycle would play in his favour and to extend the cycle,

a pause in rate hike, pause in balance sheet reductions is the only way in for

him.

There is a downside to this analysis which could cause some investors to remain net short. The point of difference between 2016 rate hike and 2018 rate hike is that in 2016 global central banks were not in tightening mode like Fed but in 2018, Fed when turned dovish, global central banks were also softening. This tandem movement of Fed and central banks have kept emerging markets in a fragile state if not crumbling and the yields provided by short term US treasuries are still more attractive and stable. This fear is keeping some investors from take a long position and they rather prefer holding on to existing portfolio.

Technical analysis shows us that a golden cross is emerging and higher growth is expected if the economic situation remains unchanged. Equities and commodities like copper and oil are pricing in the positive effect of China stimulus and pressure on commodities caused by rate hikes is lifting. Copper which is seen as an indicator of global growth is moving opposite to 10 year treasury yield.

In late 2018, under pressure from Trump administration and to prevent further domestic slowdown, China implemented tax cuts to increase consumption, reduced the rate of required reserves for lenders to encourage borrowing and stimulated fiscal multiplier to boost demand which along with weaker USD led to strengthening of Yuan and rally in demand dependent commodities. China in effect is navigating this ‘reflation trade’. A weak Yuan hurts US manufacturing sector so to stretch out economic cycle for 2020 election in US, Trump would not mind a weak USD for stronger Yuan out of China which will recover global growth and reverse inflation expectations. China’s (almost) healthy economy keeps all the neighbouring economies in shape and any poking in China destabilize other Asian and EM economies. So, who holds all the cards? Xi Jinping?

Thus will end the central banks’ bombastic hubris and the public’s faith in

central banks’ godlike powers.

Having fixed the liquidity crisis of 2008-09 and kept a perversely unequal

“recovery” staggering forward for a decade, central banks now believe there is no crisis

they can’t defeat: Liquidity crisis? Flood the global financial system with liquidity.

Interest rates above zero? Create trillions out of thin air and use the “free money” to buy bonds.

Mortgage and housing markets shaky? Create another trillion and use it buy up mortgages.

And so on. Every economic-financial crisis can be fixed by creating trillions of out thin air,

except the one we’re entering–the exhaustion of credit. Central banks, like generals,

always prepare to fight the last war and believe their preparation insures their victory.

China’s central bank created over $1 trillion in January alone to flood China’s faltering credit system with new credit-currency. Pouring new trillions into the financial system has always restarted the credit system, triggering renewed borrowing and lending that then powered yet another cycle of heedless consumption and mal-investment–oops, I meant development.

It seems as if investors are no longer willing to finance the U.S. Shale Oil Industry Black Hole. And why should they? One of the largest shale players in the Permian, Pioneer Resources, suffered its eighth consecutive year of negative free cash flow. In 2018, Pioneer spent $541 million more on capital expenditures than it made from cash from operations and if we add up all the eight years, it’s a grand total of $6.8 billion in negative free cash flow

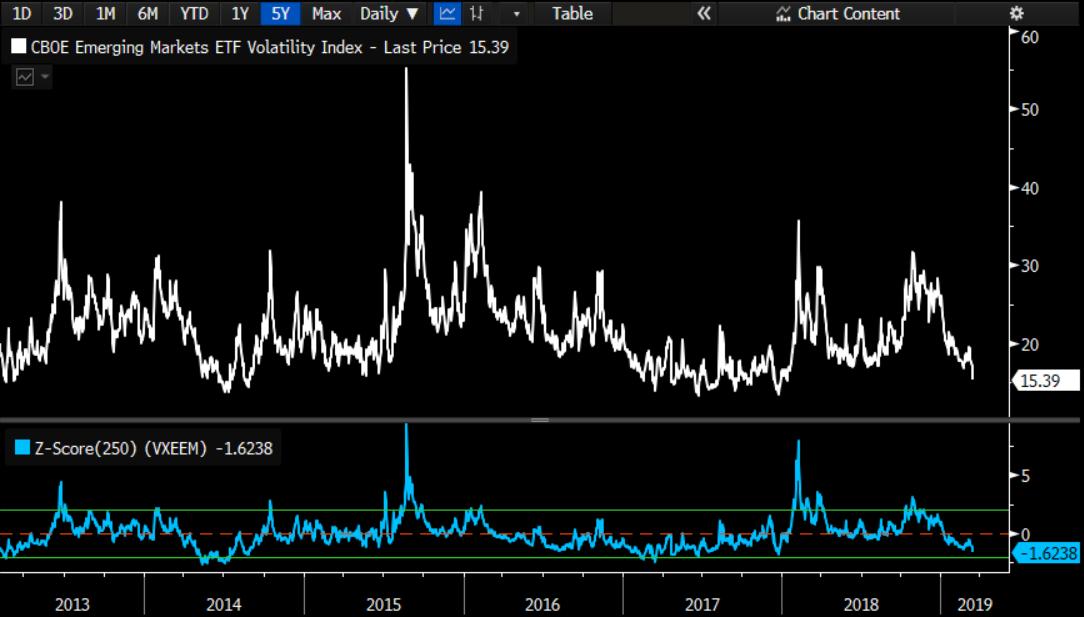

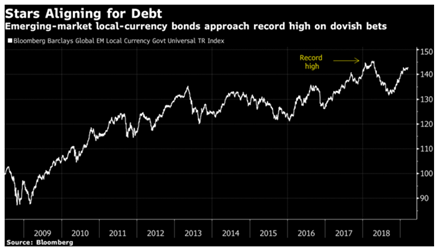

Volatility collapses in Emerging Markets. Suggest euphoria which is seen in EM currencies also along with Chinese Yuan.

Panic over? It is according to the derivative markets: Even Wall Street’s fear gauge VIX drops to over 5mth low.

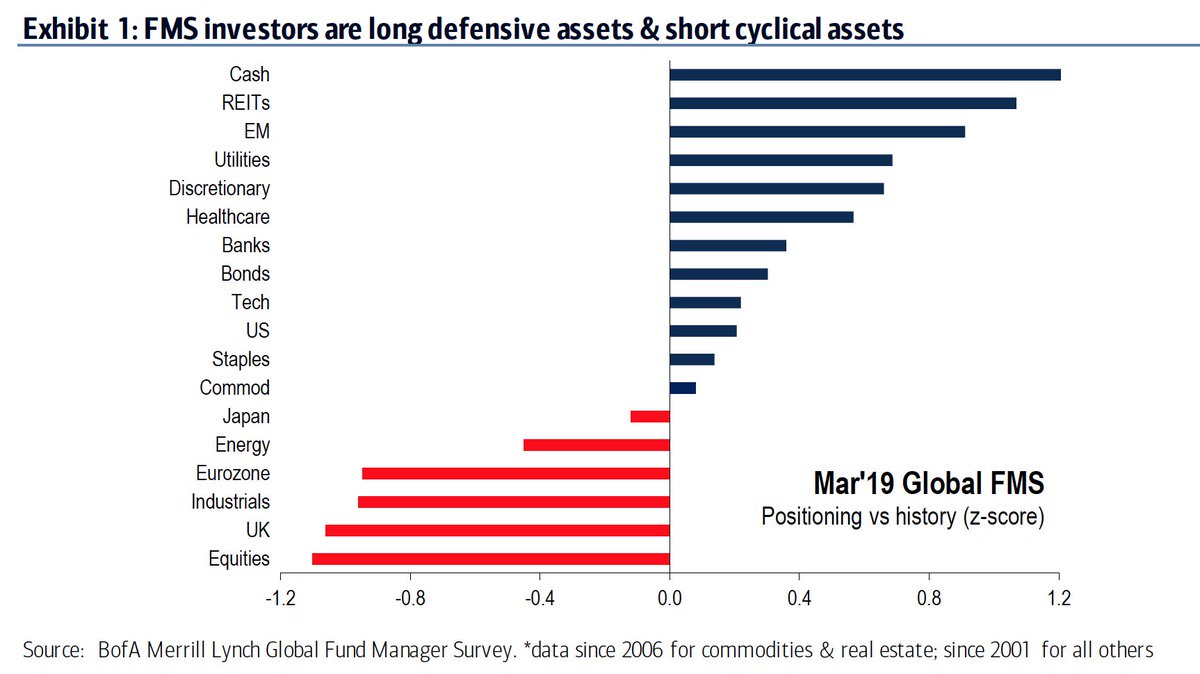

“Pain trade” for stocks is still up: In BofAML March Global Fund Manager Survey (FMS) profit expectations rose, rate expectations fell BUT allocations to stocks dropped to their lowest level since Sep ’16.

Below is a look at the broadest measure of advance-decline line breadth, the NYSE stock only Advance-Decline line. A simple failure to hold new highs in breadth marked the top in the NYSE in the fall. Now, breadth is notably diverging from price after a massive rip while it has stopped right at that old September high area. Aaron writes…We have evidence of both a longer term bullish sign with a shorter term caution sign. Thus, it seems prudent to be aware of downside risks now while keeping in mind the longer term framework, supporting an eventual move to new highs.

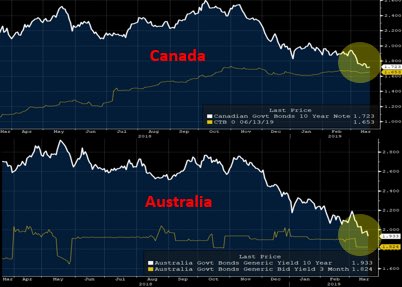

Bond markets are sniffing out a global recession… Canada & Australia just a bps away from full inversion

Swerving around

from two year long recession which ended in 2016 to one of the best performers

in emerging markets, Brazil under the newly elected right wing populist

President Jair Bolsonaro is refreshed and optimistic about its future which is

also evident from the rally in the Brazilian markets.

Many investors are investing in emerging markets which is currently led by Brazil in order to gain from potentially weaker US Dollar. EM countries are witnessing global liquidity turning into favour and countries tied to China’s shifting buying preferences are gaining most from this mix.

Gordon Fraser of BlackRock Inc. says, “Emerging market equities are highly correlated with currencies and bonds so domestic players will benefit from weaker dollar. When a currency weakens or bond yields increase, typically equities go down. So if we have become positive on a currency, firstly a perfect way to express it is through an equity. The key things riding the dollar last year are now out.” Bloomberg cited

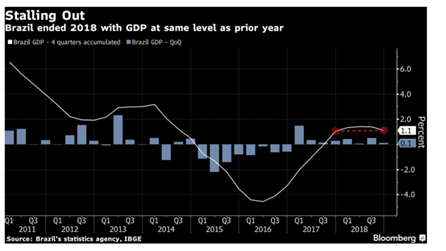

Long term bulls on Brazil and buying on dips have been giving them profits until now and they expect the rally to continue for quite some time. However there is a flip side to Brazil. The growth is expected to stay sluggish and people’s confidence depend on how the reform challenges are dealt with. Bloomberg cites that the Gross Domestic Product expanded 0.1 percent in the fourth quarter, down from a revised 0.5 percent in three months through September, the national statistics agency said Thursday. The result was the slowest quarterly pace since the third quarter of 2017 and was in line with the median estimate from economists surveyed by Bloomberg. In the full year of 2018, GDP rose 1.1 percent, same as prior year.

With slow growth

and inflation below target, markets do not see a tightening cycle in Brazil

before mid-2019. The foreign reserves dipped from nearly $383 billion in May

2018 to $374.7 billion in December. That is the lowest since December 2017 but

still covers nearly 15 months of imports and is equivalent to nearly 9 times

short – term external debt.

Brazil today

still outperforms other emerging markets and its currency, the real, rose since

the second round of voting on October 29, 2018. The MSCI Brazil index, which

fell 8 percent in 2018 while MSCI EM as a whole dropped 17.5%, is up 16.5% in

2019 versus a 4.5% gain for MSCI EM. The optimism was boosted when the pension

reform plan was announced. Current retirement age is 55 and pension reform

retirement ages is expected to be 62 for women and 65 for men. This is going to

amount up as 1 trillion real in savings.

The two right wing populist leaders, Trump and Bolsonaro meeting is considered crucial for both the countries and ways to enhance of bilateral ties will be on the agenda. US is Brazil’s second biggest trade partner after China. Matias Spektor, professor of international relations at Sao Paulo’s FGV business school said in a seminar, “Knowing that Bolsonaro has Trump on his side will be important for investors, especially if Brazil has a bumpy financial year.” Win Thin, global head of emerging market strategy with Brown Brothers Harriman said, “To someone who has been following Brazil for three decades, the huge rightward shift is simply amazing.” He added, “With inflation likely to remain low and central bank on hold for much of this year, we think Brazil will continue to outperform.” Brazil has played its card well in the recent US china dispute by staying under the radar and still a beneficiary of a this trade dispute as china shifted some of its agri buying from US to Brazil.

Tyler Kling writes….. Credit spreads have narrowed significantly since the beginning of the year. Check out the graph below via Citi Bank.

Credit spreads and stocks move together because all market moves are governed by liquidity conditions. When liquidity conditions tighten (credit spreads widen) the cost of capital goes up, and therefore the returns investors receive in equities relative to other assets looks less attractive.

It’s important to stay in tune with liquidity conditions because that’s how you give yourself a chance to actually time the market. Stanley Druckenmiller earned his breathtaking track record by paying close attention to liquidity in the financial system. (Quote below)

I never use valuation to time the market. I use liquidity considerations and technical analysis for timing. Valuation only tells me how far the market can go once a catalyst enters the picture to change the market direction.

Sir John Templeton used to quip that “People are always asking me where the outlook is good, but that’s the wrong question… The right question is: Where is the outlook the most miserable? Invest at the point of maximum pessimism.”

If you want deep value and a wide margin of safety then you have to be willing to venture where others won’t. Maximum pessimism is what creates the asymmetric bets where the risk then becomes time and not price, as Richard Chandler puts it.

Looking across global markets today there is perhaps only one industry that fits this bill. Where the outlook is beyond miserable and the stocks within it have either been dismissed by investors or just outright forgotten all-together.

I’m of course talking about marijuana stocks…

Just kidding. No. I’m talking about the shipping sector.

Take a look at the following charts showing the prolonged grinding drop in shipping rates.

The Harpex Shipping Index has been in a steep rolling bear market for nearly a decade and a half.