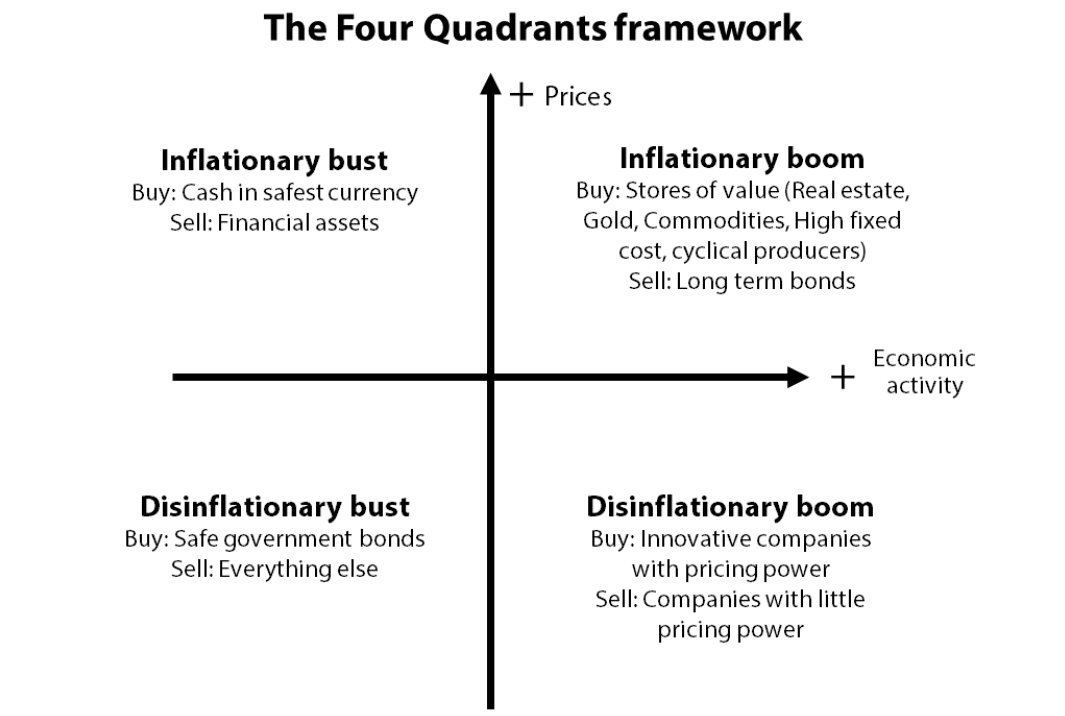

Many readers will be familiar with my four quadrants representation of macroeconomic conditions, which like most Gavekal research is backed by impeccable logic. The tricky part, as ever, is linking the conceptual insight to current market conditions. To put it simply, the questions I want answered are: where are we today and where are we likely going next?

Needless to say, I have worked on such questions since authoring the tool back in 1978. Over the years, I have come up with a few answers ranging from the straightforward to the rather complex, as expounded on in my 2016 book investigating Wicksellian analysis.

Back to MV=PQ In this paper, I want to show that using tried-and-tested tools, which have not changed since they were built, I can, indeed, pinpoint where we are, and where we are going. Longtime readers will know that I place emphasis on the old equation MV=PQ, except that I consider V to be an independent variable, and not the result of the ex-post tautology V=PQ/M.

They may even recall that around the turn of the millennium, I developed a leading indicator for Q (growth in volume), for P and for V, while M (M2) is provided to me by the Federal Reserve. Hence, a logical solution to my problem of mapping where we are in the four quadrants should be possible.

My growth indicator will tell me whether we are on the left or right side of the four quadrant representation, while my P indicator will give indications of whether we are in the top or the bottom halves. And the V indicator should tell me whether interest rates are going to rise, or fall.

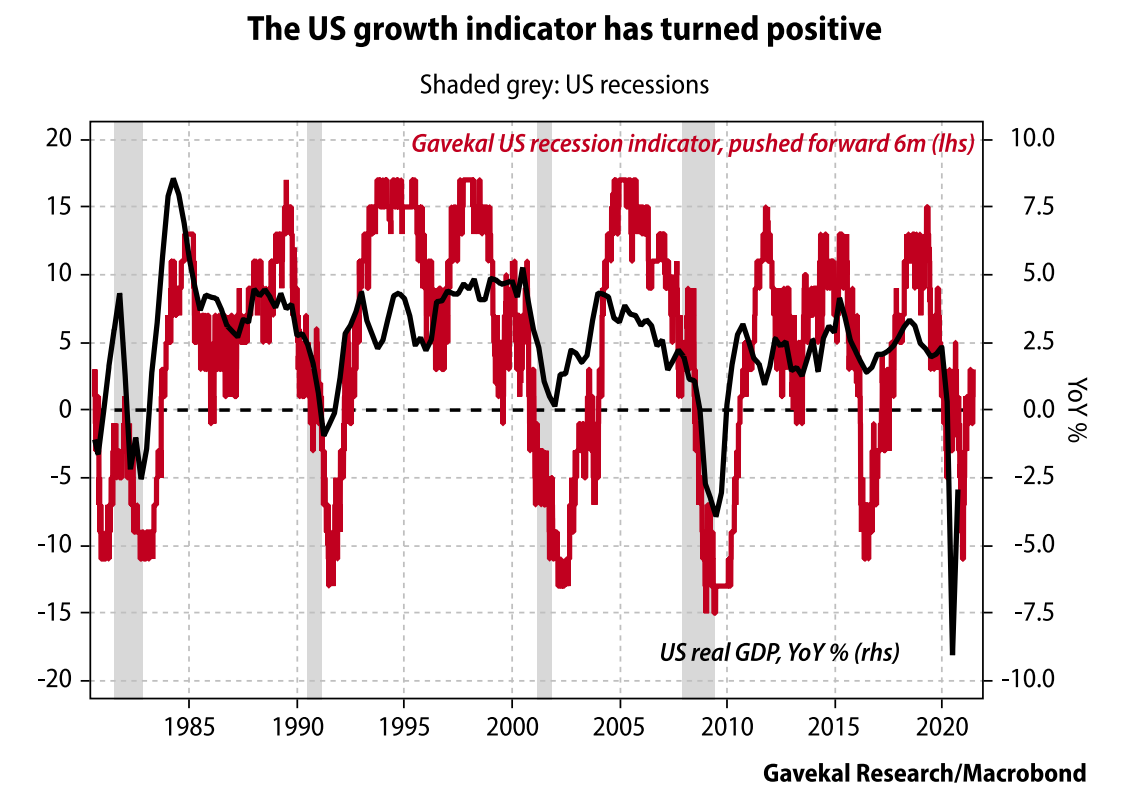

Let’s start with the US growth/recession indicator, shown below, which incorporates mostly economic data.

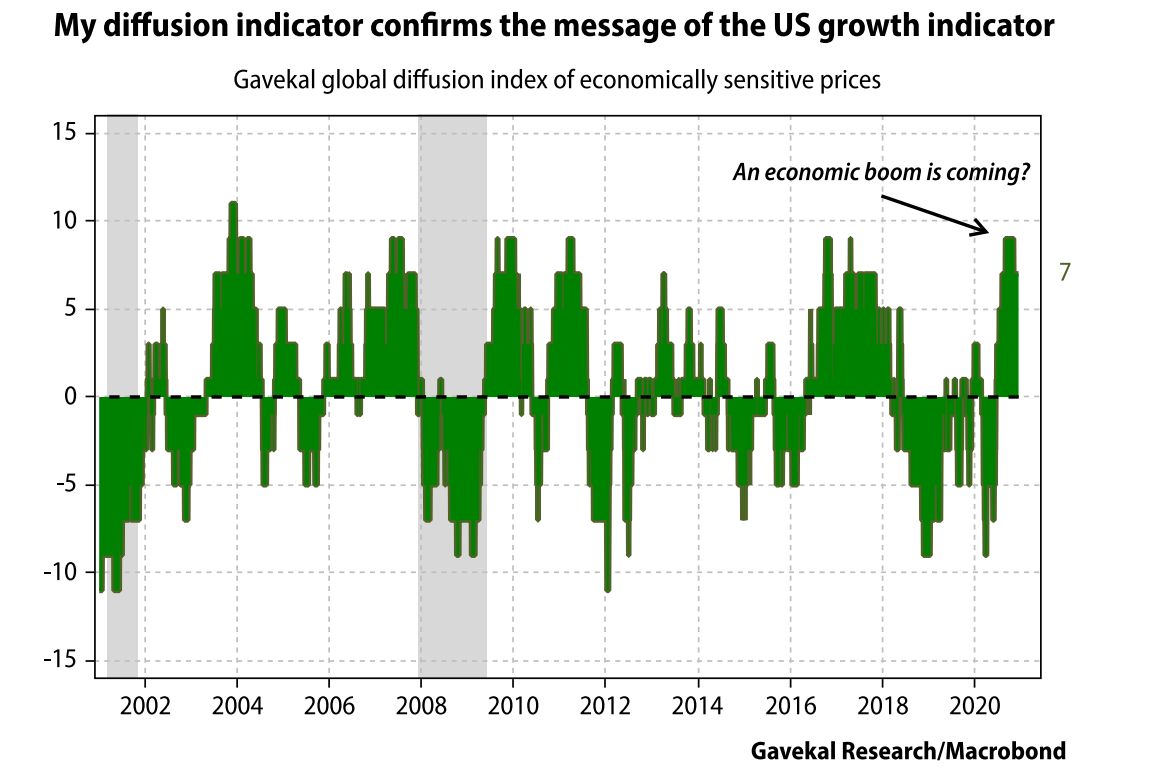

The indicator collapsed at the end of 2019 and the early part of 2020, but has now returned to positive territory. This reading suggests that the US recovery will continue, which is supported by my “control” tool— a diffusion index of economically sensitive prices—which incorporates only market prices. The diffusion indicator is telling me that a boom is coming in the US, which confirms the message of the growth/recession indicator that a US recession is highly unlikely in the near future.

And thus, I can safely assume that we are on the right side of the four quadrants; either in an inflationary growth period (top right) or in a disinflationary boom time (bottom right).

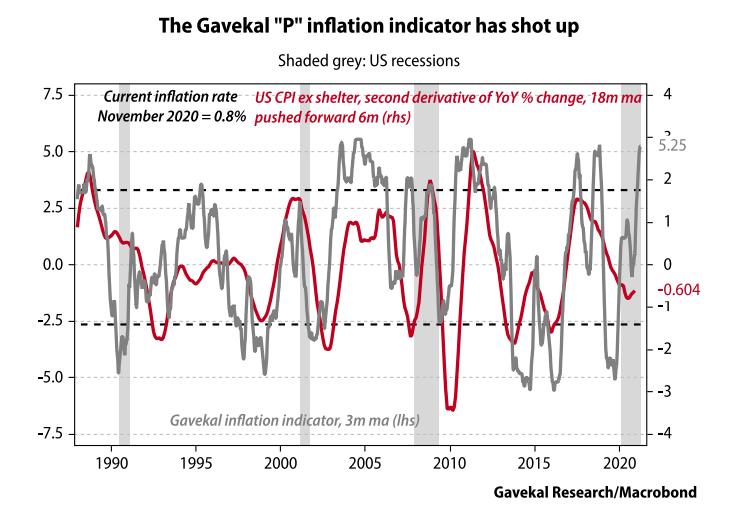

Having established that the US economy sits in the right side of the quadrant, I feel fairly sure that its precise position is in the upper (inflationary) quadrant as my “P indicator” of inflation has shot up.

In the chart above, the P indicator is compared to the second derivative of the US CPI (ex-Shelter). Why the second derivative? Because what matters for financial markets is not the actual inflation rate but the “surprising” changes in this rate, either up or down. And surprises may be coming. The P indicator seems to expect, one year down the road, a rise of at least 200bp in US CPI, which would take it close to 3%, versus 0.8% today.

In summary, my indicators tell me that US growth will be strong and we are on the right side of the four quadrants framework. As prices seem set to accelerate, we are moving into the upper half, which means that 2021 should see an inflationary boom in the US.

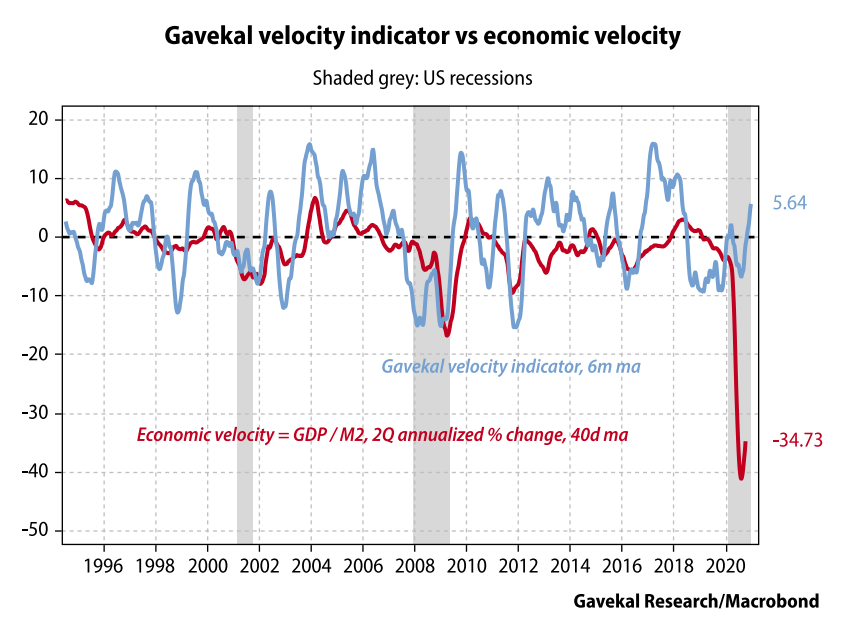

The velocity of money turns up This brings me to the velocity of money, V, and to the reaction of the central bank to the US entering an inflationary phase. The amount of money injected into the US economy in the last 12 months has been stupendous. As a result, V has collapsed as never before. But most of this money is still in the accounts of economic agents (the Treasury, individuals, and companies) and is apparently starting to be used. As a result, velocity is starting to rise again, but I will know for sure by how much only with a considerable lag, due to the time needed for GDP data to be compiled.

So, I need a tool to give me some “lead” on the likely direction of economic velocity. This is why I built the Gavekal Velocity Indicator using market-based data that gives a heads-up as to whether what I call economic velocity (PQ/M) is about to turn up, or turn down. The chart is shown below.

The GVI—which is supposed to lead actual velocity by six months—“turned” up at the beginning of September 2020 and is now positive. This implies that cash balances held by economic agents are starting to move into the real economy. It confirms that activity is accelerating.

I have argued before that if the velocity of money is rising, demand for money must be growing faster than the supply of money. This implies that the price of money—the interest rate—will rise. What could upset this logic would be the Fed continuing to print, so that M keeps rising. If this happens, it goes without saying that the US dollar exchange rate will fall big time.

Conclusion

Economic activity is going to be strong, to very strong, in the near future.

Inflation is going to accelerate significantly in the next 12 months.

Yields on 10-year treasuries will rise from an abnormally low level to a more normal level, implying a gain of about 200bp.

If the Fed tries to stop rates rising, the US dollar may collapse, which will be inflationary for the US and deflationary in Europe.

In short, the US is moving from a deflationary boom to an inflationary boom. A wrinkle could be a big rise in the oil price, which would make the situation difficult for the Fed, as it was in 1973. In past inflationary booms, non-US markets, especially in Asia, tended to outperform the US, while the dollar usually fell. Hence, investors needed to own gold and long-dated bonds in currencies which were due to revalue strongly (deutschmark and Swiss franc in the 1970s) but large cash positions also had to be held in those currencies.

My advice today is to replace bunds with Chinese government bonds and hold cash in Asian currencies, which are tracking the renminbi. As an aside, Brazilian bonds and cash tend to offer exceptional returns and could be put in the aggressive part of the portfolio as a replacement for equities.

With Central Banks keeping interest rates near or below zero, …

European bank deposit rates are still above zero, although close to zero which harm savers. A negative deposit rate is intended to encourage lenders to do something more useful with their money than park it with the ECB. But European banks are adding fees to already beleaguered savers.

(Bloomberg) In normal times, bankers who oversee assets exceeding $1 trillion wouldn’t be groping for loose change under the sofa.

But in the banking equivalent of hunting for pennies, European financial giants like Banco Santander SA and ING Groep NV are looking to squeeze more revenue from depositors. Wealth For YouHelp us deliver more relevant content for you by telling us about yourself. Answer 3 questions to tailor your experience.

Introducing charges and increasing fees show how a future of sub-zero interest rates is forcing euro-area banks to transfer more costs to clients. While the tactics could backfire by accelerating a shift of depositors into low-cost neobanks, they may help traditional lenders sell more lucrative products.

For a banker, “if you only have a current account with me, I lose money,” said Angel Corcostegui, former Santander CEO and founder of private equity firm Magnum Capital Industrial Partners. “Banks need to be a clearer about the costs that they assume.”

The move toward more fees will most likely have more impact on those who don’t have a steady paycheck or the means to buy financial products, said Patricia Suarez, president of financial consumer watchdog Asufin. “They’re separating more profitable clients from the less profitable ones,” she says.

In Spain, Santander will introduce a monthly charge in the new year of as much as 20 euros on current accounts for customers who don’t meet certain criteria, which include paying in salary and buying at least one other financial product. Banco Bilbao Vizcaya Argentaria SA is starting to charge customers over 29 years old who don’t pay in their salaries and use the account to pay bills. It will also begin charging 2 euros for using cashier services and 0.4% on transfers.

ING, which for many years advertised the appeal of no-fee current accounts in Spain, sent out an email to its customers there telling them it would begin charging 10 euros a month on holdings over 30,000 euros ($37,000) if the customer doesn’t use ING for their salary deposits or receive at least 700 euros a month in income.

A statement from ING cited “the unusual economic moment in which interest rates (which set the price of money) have been going down endlessly.” A Santander statement emphasized that “loyal” customers will avoid new fees.

At the other end of the spectrum, euro-area banks have also imposed new costs. Deutsche Bank AG and Commerzbank AG last year lowered the threshold to 100,000 euros for charging new retail depositors.

While Asian and American banks cans still count on positive rates, Europe’s half-a-decade experiment with negative interest rates has put pressure on lending revenue and burdened banks with billions of euros in penalties for parking cash with the central bank. In Denmark, where benchmark rates have been negative since 2012, most banks now charge clients on deposits exceeding a set amount.

Michael Soffe, a British expat who owns wedding and catering companies in Malaga, Spain, says he’s noticed a steady increase in fees on credit cards, debit cards and transfers. As an owner of a business account at Banco Unicaja SA, he was able to get some of those removed, although the charges he does pay have risen about fourfold in recent years. He’s also noticed a push to sell other products, such as house insurance.

“Bank charges have risen quite substantially,” Soffe said. “And they all want you to have insurance with the banks.”

The increase in fees and charges may represent an opportunity for digital-only banks such as Monzo Bank Ltd., Revolut Ltd. and N26 Bank GmbH, which thanks to lower cost structures may be able to lure new customers with the promise of no charges on services. Starling Bank Ltd., which also recently began lending, could prove an appealing alternative for consumers fleeing charges.

“Whenever there is a negative customer experience in a traditional bank, it opens the door for someone to come along and do it better,” said Joe Fielding, head of banking and payment practice for the Americas at Bain & Co. in New York. “’Better in today’s terms is inevitably digital.”

But with interest rates at record lows, a move to charging for those services makes sense, said Magnum Capital’s Corcostegui.

“What we’re going to see now is an unbundling of costs per service. We’ll move toward a pay-per-use system,” Corcostegui said in an interview. “Having a current account is a service that needs to be paid for, just like when you pay to catch a bus.”

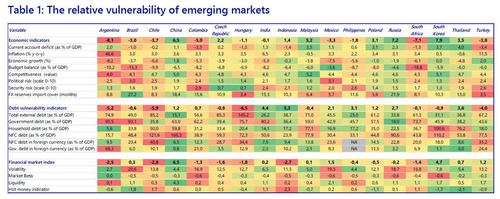

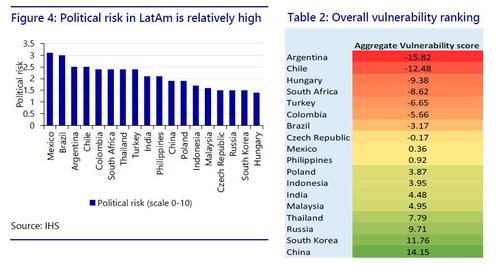

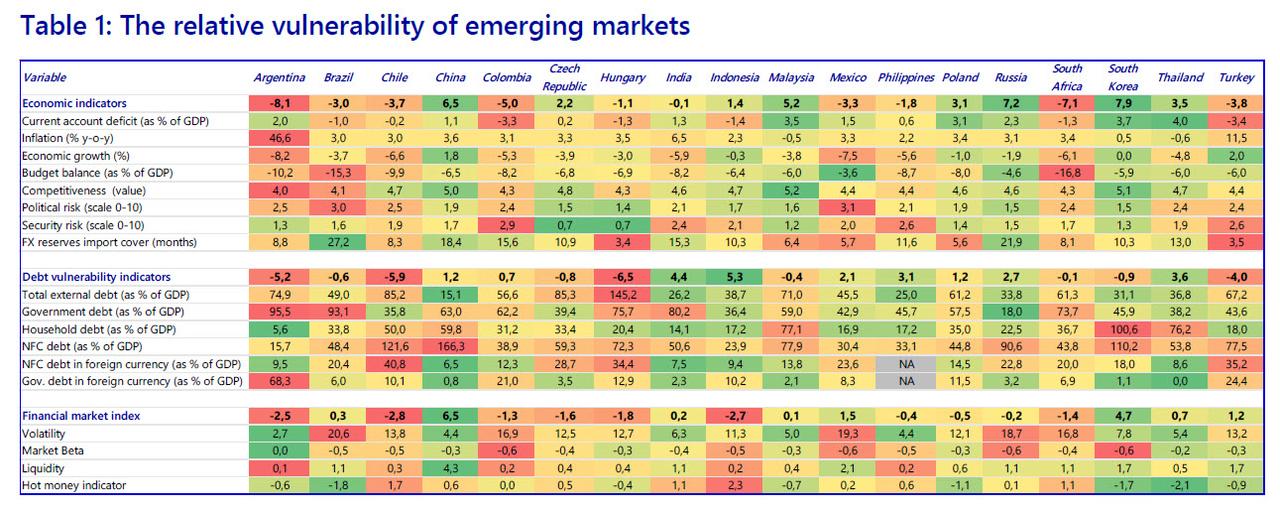

We have updated our emerging markets heatmap which provides a comprehensive overview of the relative vulnerability of 18 emerging markets

Asian countries are in relatively good shape, while Latin American countries are most vulnerable, with Argentina ‘topping’ the ranking

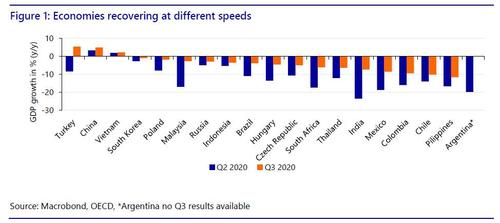

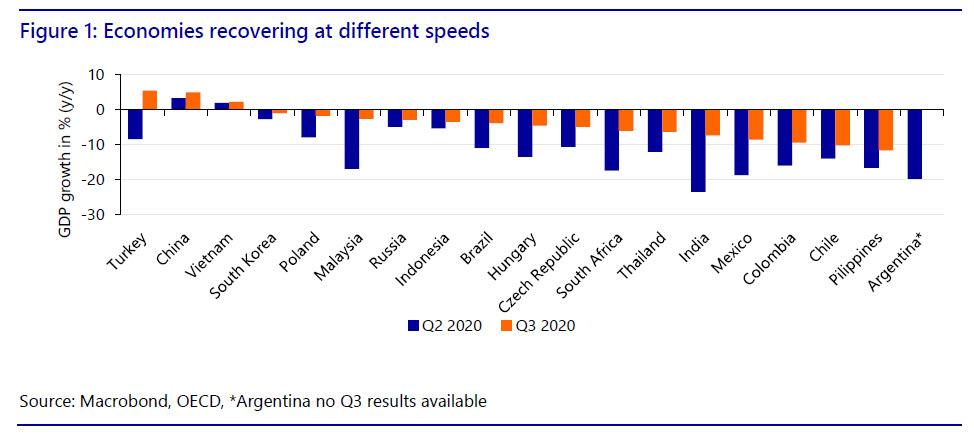

Emerging markets are recovering at different speeds, ranging from single digit growth (China, Vietnam) to double digit contractions (Chile, the Philippines) in Q3

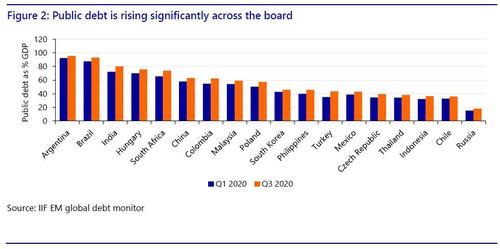

Public debt levels are surging in all economies, limiting future fiscal space

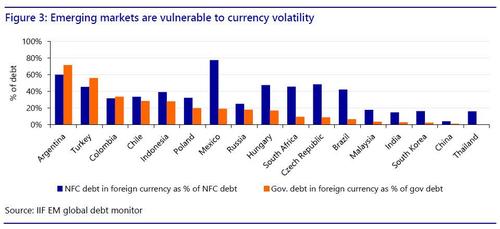

In terms of currencies, Philippine Peso, Hungarian Forint and Chilean Peso are outperforming while the Russian Rouble and Indian Rupee are underperforming relative to their vulnerability

Going forward we expect EM currencies to be relatively strong on the back of a weak dollar and global economic recovery

But if downside risks materialize, the local currencies of countries that are vulnerable according to our heatmap will be most heavily impacted

The vulnerability of EMs after rollercoaster 2020

Concluding that 2020 was a turbulent year would be an understatement. In light of all recent developments we have updated our emerging market vulnerability heatmap (Table 1) to provide guidance on a range of economic indicators and present the relative performance of emerging markets in an intuitive manner.

Diverging economic recovery

Amid the reverberations of the global pandemic we observe different speeds of recovery among emerging markets. Countries like China and Vietnam showed positive growth figures while countries like the Philippines and Chile are still showing a double digit contraction y/y. Figure 1 presents the fastest growing economy in Q3 on the left and the slowest on the right. The difference in speed of recovery can be attributed to a number of factors. First and foremost, the level of containment of the virus, which, for example, explains why China is doing well (it has been relatively successful in containing the virus). But other factors also play into these developments. For example, countries like the Philippines and Thailand are very dependent on tourism and are hit hard by closed borders. Other countries like Malaysia and China are exporting medical or electronic equipment and could benefit from a rise in demand for these products rose as a result of the pandemic and lockdowns. On the flipside, this implies that countries suffering from closed borders in recent months can expect to rebound quickly whenever vaccines are widely available and international travel returns to pre-pandemic levels.

Rising debt levels

In order to limit the impact of the pandemic, governments reacted with large stimulus packages. In an earlier publication we elaborated in depth on COVID-19 monetary and fiscal stimulus packages among developed and developing countries. The additional fiscal stimulus has resulted in large increases of public debt. In Figure 2 we see the countries with the largest public debt as a % of GDP, ordered from left to right. Countries that stand out are Argentina, Brazil and India. These countries have increased their public debt as a result of large fiscal deficits in order to finance COVID-19 support packages: Argentina 6% of GDP, Brazil 8.4% of GDP and India 8.5% of GDP. Going forward, limiting large budget deficits helps governments to keep the public debt level sustainable and retain fiscal headroom to stimulate the economy if needed. High debt levels are a constraint to future economic growth. They limit future fiscal spending for a number of reasons: i) A higher share of the government budget needs to be allocated towards debt repayments and cannot be used to stimulate the economy ii) higher debts lead to higher default risks and iii) higher debt levels could increase interest rates on future government bond issuance.

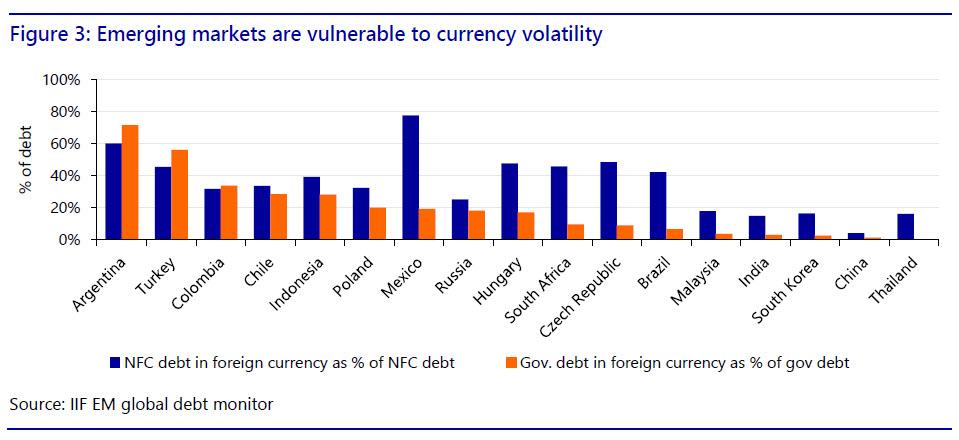

Another important measure is how much of the debt is denominated in a foreign currency. Large shares of foreign-currency denominated debt increase the vulnerability to currency volatility. In Figure 3 we observe that Argentina, Turkey and Indonesia have the largest share of their debt denominated in foreign currency, which makes them the most sensitive to currency movements within their region. This dependence on foreign capital constrains the set of monetary or fiscal mechanisms that can be used to stimulate the economy. For example, cutting central bank interest rates depreciates the local currency, indirectly increasing government debt levels in terms of the local currency. On the other side of the spectrum we see that mainly Asian countries (Thailand, China, South Korea) are in good shape with regard to foreign currency-denominated debt.

Overall rankings

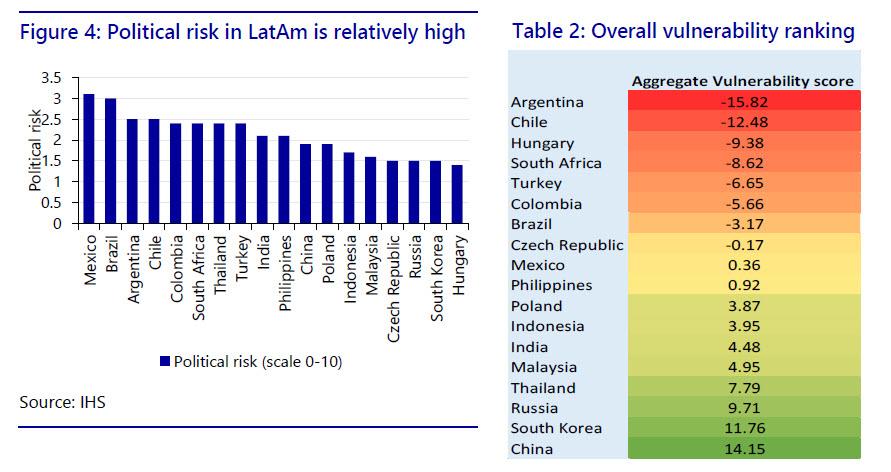

In Table 2 we show the aggregated rankings. The countries shown at the top are the most vulnerable according to our framework while countries at the bottom are least vulnerable. In general, we observe that Asian countries are performing quite well, while countries in Latin America are showing a higher degree of vulnerability. We already showed (Figures 2 & 3) that countries like Argentina, Turkey and Chile are relatively vulnerable with regard to their debt levels. At the same time, the Philippines, Chile, Colombia and Mexico are struggling to rebound from the economic dip caused by the pandemic. Alongside economic performance, institutional quality is another driver.

Zooming in on institutional indicators like political risk we note that Latin American countries are more vulnerable than countries in, for example, Asia (Figure 4). However, these are all relatively low with the highest score being around 3 on a 0-10 scale.

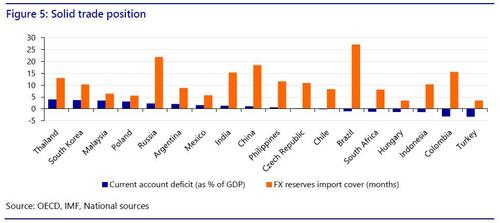

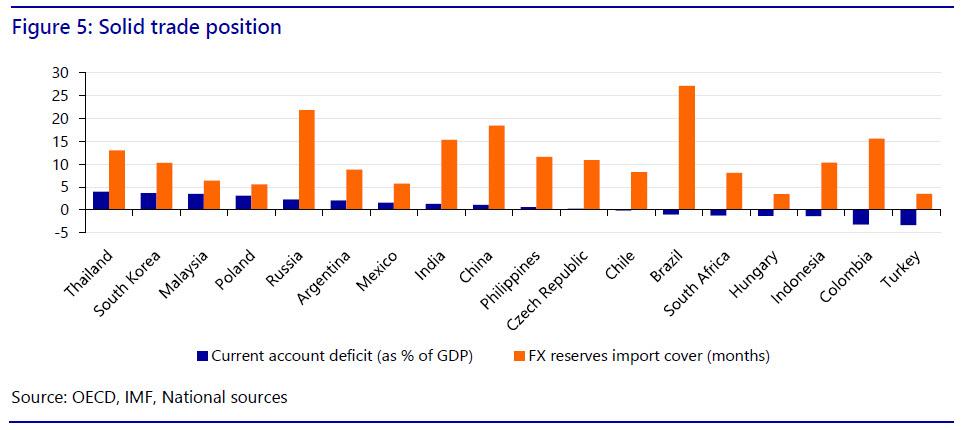

Finally, trade figures provide another important economic indicator. Figure 5 shows which countries have the largest trade surplus left to right and the vulnerability with regard to FX export cover, which indicates how many months of imports can be covered by current foreign reserves. The figures point out that a relatively solid trade position supports to a country’s relatively good position in the overall rankings, especially in the case of Thailand, South Korea and Russia.

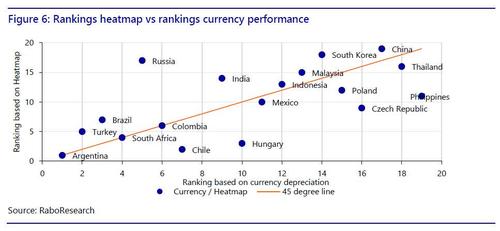

Vulnerability heatmap vs. performance of local currencies

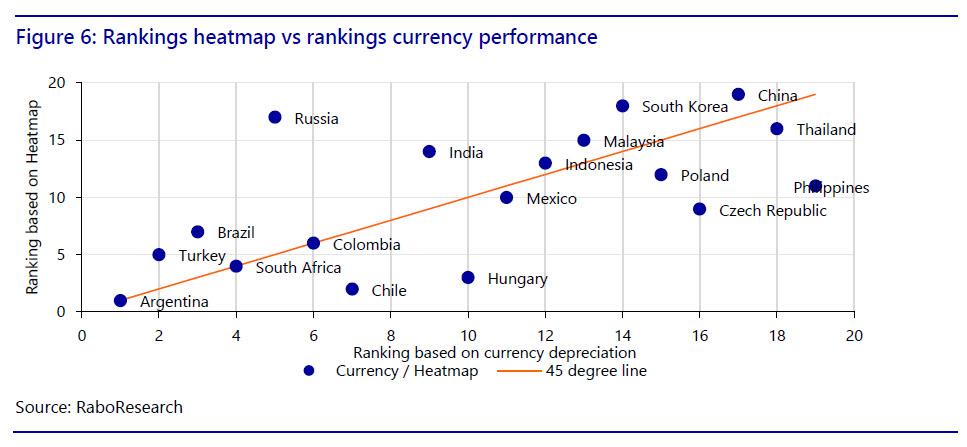

In figure 6 we compare the vulnerability rankings to the performance ranking of the local currencies since the start of 2020. Overall, we observe that the vulnerability is a good gauge of the relative performance of the local currencies. There is a decent fit between the vulnerability and depreciation of currencies. Currencies above the 45 degree line are relatively underperforming based on the relative vulnerability ranking, while currencies under the 45 degree line are relatively outperforming their relative vulnerability ranking. Although these indicators provide a comparison based on fundamentals, other very important factors must be considered when evaluating the value of these currencies, for instance current local economic circumstances, global events and global investor sentiment. In this way, the Philippine Peso’s strength can be attributed to the increase in remittances and collapsed imports during the pandemic and recovery from strong typhoons in November. The Rouble’s weakness could be attributed to foreign policy risks and associated risks for investors, constraining them from investing in Rouble-denominated assets.

The year ahead

The vulnerability heatmap provides an intuitive framework to assess the fundamental performance of emerging markets and their relative performance on a range of indicators. But we should not look at these in isolation. Next year the individual performance will be driven by economic recovery, virus containment, political stability, budget prudence and central bank policy as well as global investor sentiment.

In general, emerging market currencies have the opportunity to appreciate on the back of a weak dollar, as a result of ample liquidity provided by the FED and ECB. In turn, this provides governments and central banks of EMs to loosen their policy in order to stimulate their economies. The divergence in monetary and fiscal policies will be one of the main drivers in relative performance of the EM local currencies.

The economic recovery, spurred by the implementation of vaccines is another important factor. EMs will benefit from developed markets opening up, increasing the global demand for products and commodities, which will benefit production countries like China and Malaysia and commodity exporters like Indonesia and Brazil. Likewise, opening borders to tourism will benefit countries like the Philippines and Thailand.

On the flipside, downside risks like new outbreaks or a shift towards risk-averse investor sentiment will have a more severe impact on currencies of countries that are most vulnerable according to our vulnerability heatmap. Countries that are least vulnerable according to the heatmap will be less impacted by negative events and a risk-averse investor environment.

Moving closer than ever to nationwide launch, China’s DCEP e-RMB will soon circulate in the heartland city of Suzhou in the biggest test yet of the nation’s new central bank digital currency (CBDC).

About 100,000 residents of Suzhou, a manufacturing hub in eastern China, will receive free digital red packets containing a collective 20 million digital yuan — or about US$3 million — starting tomorrow. China’s latest digital currency giveaway, the largest to date, is scheduled to happen the day before the nation’s “double twelve” festival of shopping this Saturday, Dec.12.

Aside from designated brick-and-mortar retail stores and restaurants, Suzhou residents will also be allowed to spend their DCEP cash at online stores in JD.com, the first time that the digital yuan will be available for online shopping.

A select group of users will also be able to experiment with the CBDC’s offline wallet function — which will allow users to make a direct payment without having to go through the internet, according to People’s Daily.

Suzhou will be the second city in China to test out the new digital yuan on a large scale with ordinary people, following a test in October involving 50,000 users in Shenzhen. Aside from the Suzhou DCEP test being twice as large, the location’s symbolism also stands out.

Unlike the high-tech hub of Shenzhen, which became a city only in 1979 and is full of young professionals, Suzhou is among the cultural centers of China, famous for its 2,500-year history and classical gardens.

“When ready, there’s no doubt that China will introduce CBDC to the RCEP (Regional Comprehensive Economic Partnership) and the Belt and Road countries, with the ultimate goal to make the RMB an alternative to the almighty U.S. dollar,” said Stanley Chao, managing director of All In Consulting, a culture change consulting firm based in Los Angeles. “In short, the CBDC is front and center in this new cold war, and reducing its [reliance] on the U.S.”

DCEP DIGITAL YUAN AS PART OF CHINA’S NEW “SILK ROAD”

In November, Chinese President Xi Jinping announced that Beijing would further promote its “digital Silk Road,” part of Chinese ambitious Belt and Road Initiative aimed at expanding Chinese trade and economic influence to Asian, European and African countries. Compared to other large-scale traditional infrastructure construction projects, the digital Silk Road would focus on playing a similar role for China to develop its leadership and global influence in emerging technology, like blockchain, 5G and cloud computing.

Aside from reducing China’s own reliance on the U.S. dollar, the DCEP digital yuan could see China’s trading partners using e-RMB as their future currency of settlement rather than the U.S. dollar.

China’s new CBDC may come even sooner to the nation’s own backyard. The Hong Kong Monetary Authority recently began discussions with the Digital Currency Institute of the People’s Bank of China on pilot-testing the DCEP digital yuan for making cross-border payments between the mainland and its territory. Hong Kong has its own currency, the Hong Kong dollar — has been pegged to the U.S. dollar since 1983.

“The writing is on the wall,” Chao said. “China and the U.S. are heading towards bifurcation, and China doesn’t want any reliance on the U.S. from an economic, finance, high-tech and geopolitical standpoint.”

Multiple sources told Forkast.News that the Suzhou test would include trialling the digital yuan’s offline payment and contactless payment function based on NFC (“Near Field Communication”) — a contactless communication technology based on radio frequency. In preparation, stores in the Xiangcheng district of Suzhou are now installing NFC-based point-of-sales (POS) terminals, according to local media.

Testing the offline payment function of e-RMB wallet is important to realizing China’s globalization ambitions, said Nir Kshetri, a professor in the Department of Management at the University of North Carolina-Greensboro and author of the book, “Blockchain and Supply Chain Management.”

“China also hopes that subsequently the cryptocurrency will be made available in foreign countries. Many developing countries have lower proportions of population connected to the internet,” Kshetri said. “If CBDC is to be adopted by these populations, the NFC trial holds special significance.”

Since China began planning and building its DCEP digital yuan six years ago, it has already gone through pilot tests involving four large state-owned commercial banks — ICBC (Industrial and Commercial Bank of China), Agricultural Bank of China, Bank of China, and China Commercial Bank.

Shenzhen’s DCEP testing in October brought the CBDC for the first time, en masse, to ordinary people — which many China experts note may be part of the final push to troubleshoot as well as create favorable publicity before the digital currency’s official launch.

Suzhou announced today that it would use a lottery system similar to the one in Shenzhen to pick the lucky digital yuan winners. The giveaway also likely will underscore the CBDC’s nature as programmable money with government strings attached.

In Shenzhen, where over 1.9 million people who learned about the DCEP digital yuan giveaway registered for the lottery, the 50,000 winners had only seven days to use it or lose it. Though the digital money was legal tender, the holders were not allowed to put their CBDC in a bank, regift it to another person, or stash it under the mattress longer than a week, under the rules set by and programmed into the digital currency by China’s central bank.

The CBDC money used in Suzhou’s testing will be good for 15 days. If the digital yuan isn’t spent by then, the e-money will expire, just as some did at the conclusion of Shenzhen’s test.

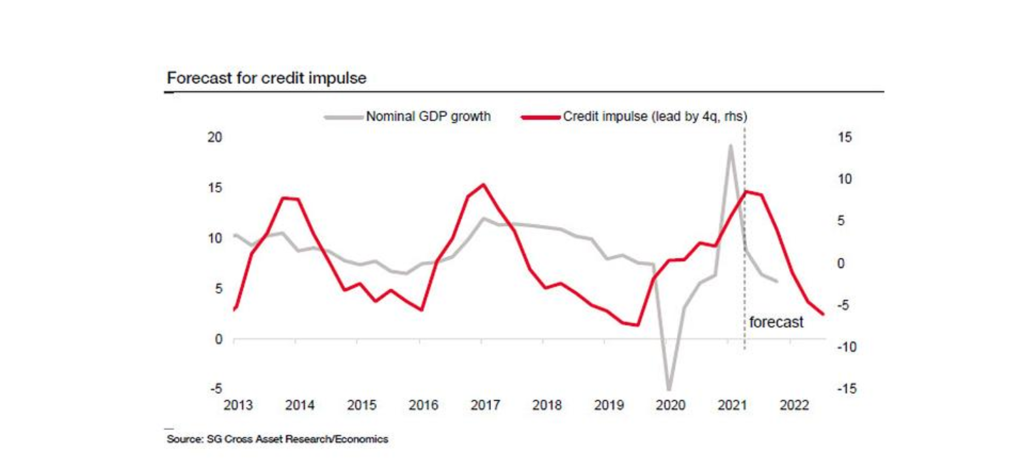

Soc Gen says that China’s credit, and indeed fiscal impulse, is peaking and about to turn down. Even if the PBoC does not embark on an aggressive tightening cycle, “the combination of a smaller fiscal deficit, these targeted deleveraging programmes and potentially more credit events will likely already be enough to exert material downward pressure on credit growth in 2021”. Given all the factors above, SocGen expects the credit impulse to start moving dramatically lower at the turn of the year, from over +8% to around -7% end-2021, about as low as that seen in late 2018 when global stock markets suffered a major wobble. his projection assumes that credit growth will decelerate slightly slower than during the 2017-18 deleveraging campaign, from 13.5% y/y currently to barely above 10% y/y end-2021. Then, as nominal GDP growth is expected to rebound strongly in yoy terms, partly thanks to base effects, the credit impulse will likely see a steeper decline than credit growth next year. According to Macro strategy …In the year through Q2, China only managed to get 9.2 cents of growth for each additional yuan of debt, and in the year through December 2019,before the crisis, 27.6 cents. This meant that 72.4 cents of the credit was just going into servicing and sustaining imbalances, and therefore, with only 27.6 cents of that credit going into growth, any slowdown in credit growth would have a much more material impact on economic growth – (the residual that is not going into servicing imbalances) – than historically.

and Promptly after this data, JP Morgan just closed its bullish position on Base Metals

As per CNBC

JPMorgan has turned “neutral” on base metals, which include copper, aluminum, nickel and zinc, and now forecasts that copper will deteriorate from an average of $7,700 per ton in the first quarter of 2021 down to around a $6,500 per ton average in the fourth quarter.

“Our analysis shows that a slowing in Chinese credit over the course of 2021 will turn into a drag on base metals prices that will likely outweigh continued recovery in the rest of the world,” JPMorgan commodities analysts said in a quarterly outlook report.

Conclusion

Chinese credit impulse, historically has been positively correlated with Base metal prices and any slowdown in that data will negatively effect the Base metals and support the general slowdown in Chinese Economy.

James Aitken makes a very welcome return to The End Game to take a look back at 2020 and a look forward to 2021.

Where did he get things wrong and why? What went according to his forecasts, and, most importantly, what has this turbulent year taught him that will help him in the future?

From the dangers of ‘Big Dicking it’ to Robert Shiller’s nasty case of FOMO to the curious birth of the Equity Vigilantes, James shows precisely why his thoughts are so indispensable to his clients.

Summary of the main points

Liquidity is here to stay will continue beyond 2021. What will differentiate various asset class in 2021 is the companies which used this year to restructure their business. The companies who will be winner in 2021 also need to have considerable earning momentum. FOMO is very powerful for investors. academicians and economist. If discount remain very low, then stock prices can go very high.

Liquidity not going anywhere even if inflation picks up a little bit in second quarter. We had state contingent monetary policy for many many years but there is a wrinkle. Previously you had central bank guidance based on central bank forecast but now you will have central bank guidance based on outcomes and Fed in particular is very clear on that saying that we will keep on pushing till we get what we want. In addition to that some countries are deploying state contingent Fiscal guidance and Australia is the leader in that, Australia will keep fiscal support in place till unemployment heads below 6%.

When you have outcomes based monetary policy working hand in hand with outcomes based fiscal policy it is a powerful combination. This is what we were supposed to do in 09/10/11 but we did not because of Tea party and smash up in Europe. So this is the man story, Liquidity is actually a back story.

For right or wrong

CB are telling us that short term interest rates are not doing anything for long time to come.

For better or worse credit risk premia has been squashed and if we take CB at face value then they will not tolerate rise in credit risk premia

And if we assume that long term interest rates remain well behaved then only risk premia for allocators to harvest over the year would be equity risk premia.

Somethings looks extraordinarily rich versus reality and investors put in mathematical term for example if you assume equity risk premia in US at 4% and a SWF or endowment fund taking a 15-20 year view then they can generate 60-80% over next 15 years but they have to unlearn about asset allocation. Oh gosh I shouldn’t be doing this, but I have to…. You keep looking at thing’s things on bloomberg which makes no sense and we keep on comparing current valuation to early 2000 and we should but there is one key rider. In start of Jan 2000 10 year TIPS in US were about 410 BP and now they are -100 BP.

There is a conundrum and if we think the things are crazy today then you got this back story that real and nominal discount rate which is forcing people to play and who knows how silly it can get.

Lets think about in accounting term MTM, if we collectively have a billion dollar to allocate and we have no redemption risk and we meet as investment committee with our bosses. Everything is overvalued what should we do. We collectively decide to invest in instruments which are not Mark to Market and that is Private equity. The big problem in subprime crisis was that too little was invested in MTM assets. if I am as asset allocator and I have 25% in FANG and some antitrust happens then I lose face but I want to continue investing in these booming markets without embarrassing myself so its no wonder that institutional investors are taking this Non MTM assets.

10-year TIPS +400 BP in 2000 Now -100 BP.

You have to take risk at these levels of TIPS

Imagining what I will do if I have a mandate as central Bank. For 20 years CB have not been able to meet their inflation mandates. Along comes 2020 and you are CB you think oh gosh we have such a big carnage, job losses, credit defaults we will have undershoot of inflation and the conclusion is there is not much different then it is for past decade plus. If you are in service dominated world where there is perpetual excess labor supply and its cheap then the only way you are going to meet your inflation targets is via financial markets keeping financial conditions loose as possible for as long as possible. So from CB point of view what else can they do. There are occasional lips to financial stability, but it is a placeholder.

It is tempting to draw 2000 analogy. What is so different for this cycle is that if inflation shows up for any period of time then CB around the world is going to cheer and throw a party as opposed to stop it.

The great reset is about Fiscal policy is going to be here for a long-long time.

Great reset in fiscal policy is available in scale and happily monetary policy is not the only game in town. The big problem come out of 2009 was that fiscal policy was turned off way too soon and monetary policy became the only game in town and then was forced to do things which monetary policy is not supposed to do. The fact that Europe has arrived at joint and several liability and for a euro skeptic like me its here and its real and cut the left tail off lot of euro denominated assets. Thank goodness fiscal policy is allowed, thank goodness they are committing to fiscal policy

So few of warning signals which used to work till 15 years don’t work or not allowed to work. The game for last 25 years is to avoid liquidation of assets. If you are Fed telling the world over and over that you think the only route to higher inflation is via Maximum employment, then quite frankly Fed will have very little tolerance for any sustained tightening in financial conditions. If this ability is constrained then Fed will act, it is as simple as that

Because we have started to eliminate enormous labor market slack and if we are making far great progress in next 6-12 months then you have to assume that people are getting higher wages than they anticipate, or economy is doing far better they imagine which are two high class problem to have.

If we are imagining global rates higher than we are anticipating that global growth coming white hot in 2nd and 3 q of 2021 and that’s a good problem to have. Long term bonds can only go up if fed is happy with the progress of the economy and in this scenario some of these high flying companies which include high ROIC companies including tech will get smacked and investors will not get worried and they will rotate.

But on the other hand, if rates are moving up because of indigestion in bond markets then that is a big problem. We are going to get inevitable inflation scare in second quarter of 2020 because of base effect and maybe there is also pressure on rates but unless we simultaneously believe that we are making rapid progress on unemployment it is difficult to assume that is more than a speed bump.

The simplest index of inflation for me for many-many years is CRB raw industrial index and for some reason it turned around this June like a hockey stick. This index is a function of pure demand and supply and this index is telling me that reflation trends are very powerful. We don’t know yet if these reflation tailwind will turn into inflation headwinds but we will find that in q2 2021

The biggest mistake of 2020 was OVERTHINKING.

The extra ordinary feature of QE2 was that average duration of treasury which Fed bought was 12 years whereas the average duration of purchases was 6 years in 2020 which is quite short and which helped ease liquidity conditions.

The Fed meeting this week is green light for investors who are light on risk to load onto risk in the run up to the end of the year.

Some of the obvious speculative excess in QQQ and calls have come off dramatically so I am wondering if there is one last surprise in the crazy year for the stock market into year end. We might get a blow off top into the year end.

What is the risk of over doing monetary or fiscal policy? It is very low

The speed of arrival and delivery of vaccine is the best stimulus you could have hoped for. Getting a vaccine can take years and we got within months and if it works then we got 3 forms of stimulus

Monetary

Fiscal

Vaccine

When will these excesses matter?

Heroic valuations can get more heroic

As Paul James put it in marvelous video of 1987

You never ever short upward sloping parabola but boy if it breaks…. we do not know when it breaks.

We have got vaccine which is a major stimulus but there are companies which should benefit from it have barely rerated.

In science knowledge is cumulative and in finance knowledge is cyclical.

I think one of the outstanding reflation trades out there is OIL.

There are bargains out there

Sam Zell is available at book value. If I can take away some of my capital from these high-flying companies and invest with the people who have seen cycles, I can sleep good at night.

At a minimum core and headline inflation 2.25-2.50 for better part of the year before Fed gets concerned. So, focus only on labor market slack for taking a call on inflation.

We are coming out of an economic catastrophe to begin with very rapidly, we are going bit sideways here lot of uncertainty, lockdown difficult new year. It probably means that the data for first quarter of 2021 is not going to be great. You probably not going to see inflation pick up too much for a while then as you move through second quarter, the things start to pick up and that is why I keep using reflation i.e. recovery as opposed to deflation, disinflation. I am going to take it by degrees and as to my earlier point there are investments available today where you can hedge against some of these outcomes down the road and whether it is miners who have restructured the business, paying dividend including commodities. Things are available today which will serve in both reflation and inflation environment and it is so interesting that so many commodities and other markets breaking out and this is so far a reflation cycle. May be things are doing better than we thought

More dollars were liberated in 2020 and before and that you can see in commodities.

One CB is far more dovish than all central banks and that is the reason dollar is weak.

As the year draws to a close, most financial market players like to project themselves forward and attempt to figure out what challenges, or surprises, the upcoming year may have in store. The aim of this piece is to do precisely the opposite: instead of looking forward, I propose to look backwards at the important changes of the past year. Some changes (especially the first couple) may seem obvious. Yet they are important enough to warrant a mention. Other important shifts in 2020 may have gone unnoticed (even if highlighted in our research!) and could end up casting a long shadow.

A dramatic shift in Western economies’ fiscal policies

In 2020, Western governments spent money like never before and promised to continue doing the same through 2021. Thus, for Keynesians, these are exciting times. And more broadly, too, for as my friend Jawad Mian recently wrote in his Stray Reflections piece:

“America’s response to the coronavirus pandemic revealed something true, says Astra Taylor, co-founder of Debt Collective, a debtors’ union fighting to cancel debts. “So many policies that our elected officials have long told us were impossible and impractical were eminently possible and practical all along.” Evictions are avoidable; there’s shelter for the homeless in government buildings; water and electricity need not be cut off for late payments; paid sick leave can be statutory for everyone; missing a mortgage payment shouldn’t result in foreclosure; and debtors can be granted relief. Political action is possible; it needs will. Multi-trillion-dollar programs were mobilized quickly in this emergency, and it will be near-impossible to put that spending genie back in the bottle…”.

The fiscal spending genie is indeed out of the bottle and there is no political will in the West to stop it from “working its magic”. Governments will thus keep spending other people’s money until they run out of it. With the “other people” being the central banks. Now importantly, in a recent must-read piece, my colleague Tan Kai Xian showed how, for all intents and purposes, US store shelves, along with procurement centers, are empty (which, on anecdotal evidence, feels broadly right as stores seem to be missing many items). And half-way across the world, my other colleague Dan Wang basically confirmed the same thing when talking to Chinese manufacturers. The Covid-linked disruption to supply chains has meant that in many industries, Chinese manufacturers are struggling to keep up with orders from Western clients. This may help explain China’s soaring export numbers, despite the renminbi having been strong.

Needless to say, empty shelves and stretched supply chains are not the typical backdrop for a recession. But even if we lack the “typical backdrop”, it seems pretty clear that policymakers can be relied upon to deliver the “typical recession answer”—namely print more money and expand budget deficits.

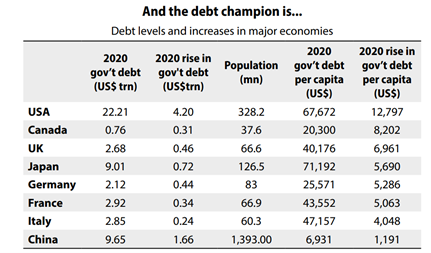

So what next? Runaway fiscal spending will keep most Western currencies under pressure, especially the US dollar since the US economy has seen the biggest rise in debt.

Initially, the weaker dollar will be reflationary for the rest of the world and generally welcomed with glee. At some point (given dislocated supply chains, maybe sooner than later), the weaker currencies will start to trigger higher inflation. Central banks with falling currencies will then face the choice of either letting their domestic currencies continue to bear the brunt of the above spending (and gradually sink into irrelevance), or choose to defend their currencies and trigger a bond market and broader asset price meltdown.

Interestingly, US inflation expectations are already rebounding (see left-hand chart below). So will the Federal Reserve be forced to reveal its hand earlier than most expect?

Embracing MMT (the magic money tree)

As the world ground to a halt in March, the Fed injected more than US$3trn into the US treasury market in a few weeks. For the first time, it also started directly buying US corporate bonds. Confronting these unprecedented actions, the obvious questions for investors is whether the Fed was aiming to (i) stop US growth from collapsing, (ii) stop the US equity market from collapsing, or (iii) stop the US bond market from collapsing.

Now granted, the answer is likely to be yes to all of the above. But if so, this marks a key difference from past cycles when, in a crisis, the government bond market would be strong and could be counted on to reduce portfolio volatility. In fact, for 40 years treasuries were the “anti-fragile” asset of choice. Then in mid-March they stopped doing the job that was expected of them (see right-hand chart below). In response, the Fed stepped in with unprecedented firepower.

All of which brings me to this interesting quote from Randal Quarles, the Fed Vice Chair for financial supervision:

“It may be that there is a simple macro fact that the treasury market being so much larger than it was even a few years ago… that the sheer volume there may have outpaced the ability of the private market infrastructure to support stress of any sort there… There is thus an open question about whether there will be an indefinite need for the Fed to participate as a purchaser to support market functioning.”

Of course, one could launch an interesting philosophical debate on whether a market that needs constant government intervention to function is really a market. I will spare readers that detour and instead conclude that current monetary policy means that the US bond market (along with its European and Japanese equivalents) survives due to the good grace and generosity of central banks. Which brings me to a fairly obvious conclusion: either central banks decide to remain generous, and bond returns should broadly flatline (as since early April 2020). Or alternatively, one day, central banks will decide that they now need to support their currencies instead of supporting their bond markets. In this scenario, bond markets will implode. In short, following the massive intervention of central banks, government bonds all across the Western world have now become “return-free” risks.

China blasts its own policy path

As the rest of the world becomes more Chinese (stay-at-home orders, smartphone tracking of individuals, church services closed and commercial banks forced to lend to firms on noncommercial terms), China’s response to the Covid crisis has been far less expansionary than its reaction to either the 2003 Sars outbreak, the 2008 global crisis and its own 2015 equity bubble burst. China’s response to the Covid crisis not only goes against the current of its own recent history, but also against the trend of all major Western countries.

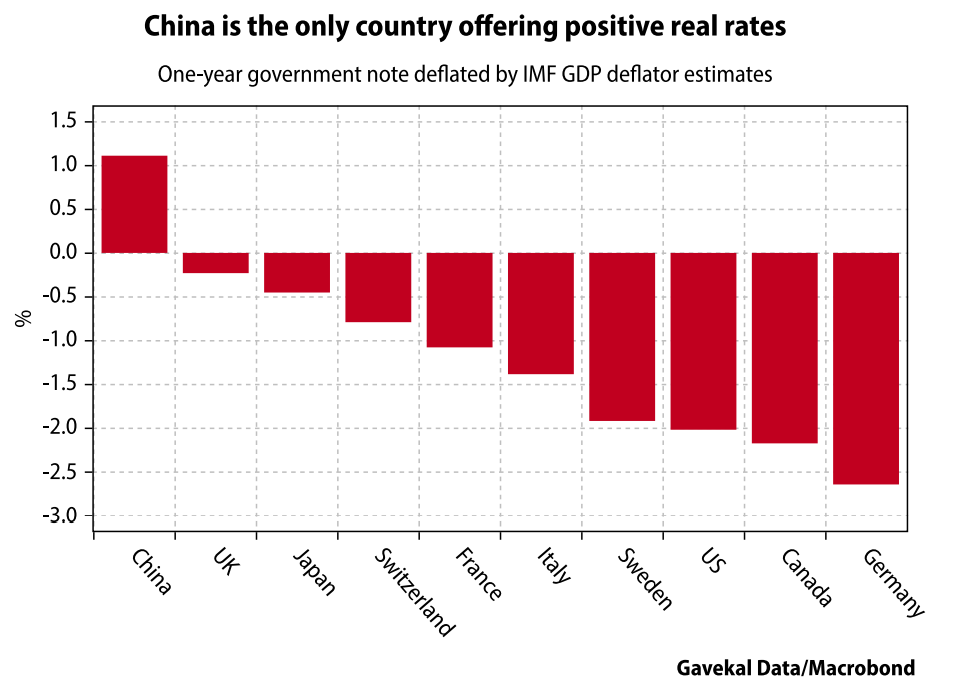

Throughout the year, we have updated readers on the reasons behind this important policy paradigm shift, whose obvious immediate consequence is that China is now alone among major economies in offering global investors positive real interest rates.

Just as water flows downhill, capital tends to flow to where it is best rewarded. Foreign investors are buying more Chinese government bonds, with their ownership share of the market doubling from 1.5% to almost 3% in the last 18 months.

These inflows have helped push the renminbi higher. For this unfolding trend to stop (lest we forget, in financial markets, all too often, the trend is a friend), one of the following will likely have to occur:

A fall in Chinese real bond yields: This could follow a big leg down in global growth, which would trigger gains in Chinese bonds, or a sharp rise in Chinese inflation (unlikely given the strength of the renminbi).

A rise in Western real yields: This seems a low-odds scenario, with real yields more likely to fall further as year-on-year inflation comparisons in the upcoming spring and summer point to rising prices.

A tightening of capital controls in China: For now, things are going the other way, with China realizing that it needs to dramatically, and rapidly, reduce the dependency of its economy on the US dollar.

Imposition of capital controls by Western economies: Facing the Sophie’s Choice of having to sacrifice either their currency or their bond market, could Western policymakers chose instead to impose capital controls on their populations? After the events of 2020, who is to say what is inconceivable, and what is not.

A change in renminbi policy?

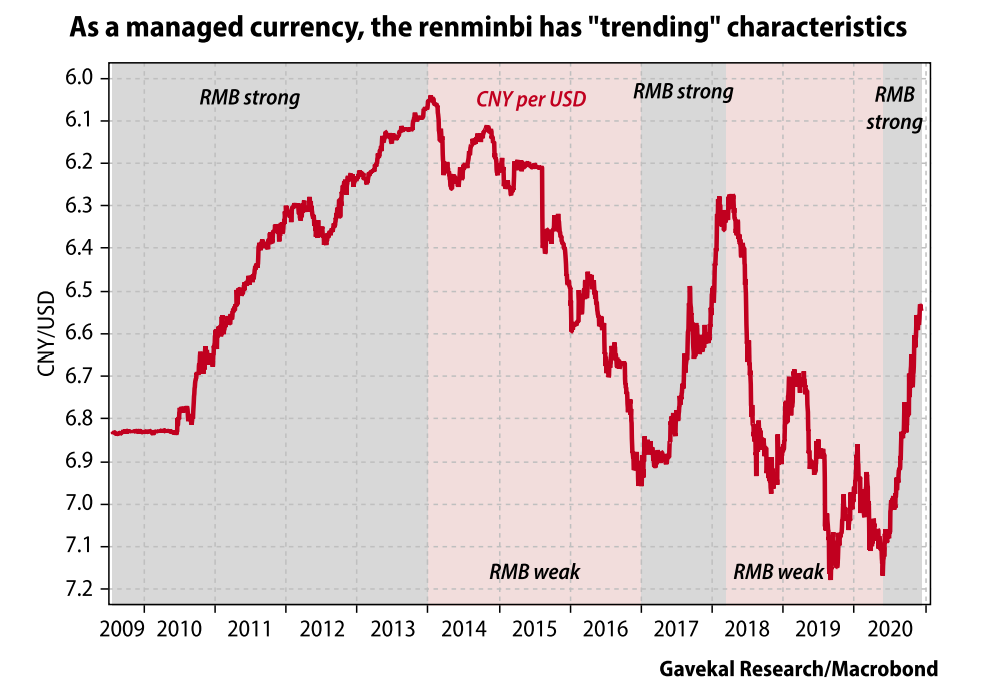

The renminbi is still a managed currency and, as such, has strong “trending” characteristics (see chart below). Another interesting feature is that it tends to “flat-line” when the outlook is uncertain. For example, after the 2008 US mortgage crisis—and until the world was clearly back on its feet by the summer of 2010—the exchange rate was fairly steady against the US dollar at around CNY6.82. A similar thing happened in the spring and summer of 2015 around the time that Shanghai’s equity market bubble burst (the renminbi flat-lined at around CNY6.2 to the US dollar). Yet, in the past six months, against an uncertain backdrop, the renminbi has registered its best six-month rebound on record.

This sharp rally raises the question: are we seeing an important change in the Chinese and global macro landscape? And if so, what are the investment implications.

A stop to Ricardian growth?

The thesis of Gavekal’s first book back in 2005 was that the ability to measure everything in real time meant successful companies would outsource all parts of their business processes in which they did not have the highest possible returns on invested capital. We used the term “platform company” to describe the firms of the future that focused mostly on design and/or sales, while outsourcing capital and labor intensive production to others. In such a world, supply chains would become ever more stretched across the globe.

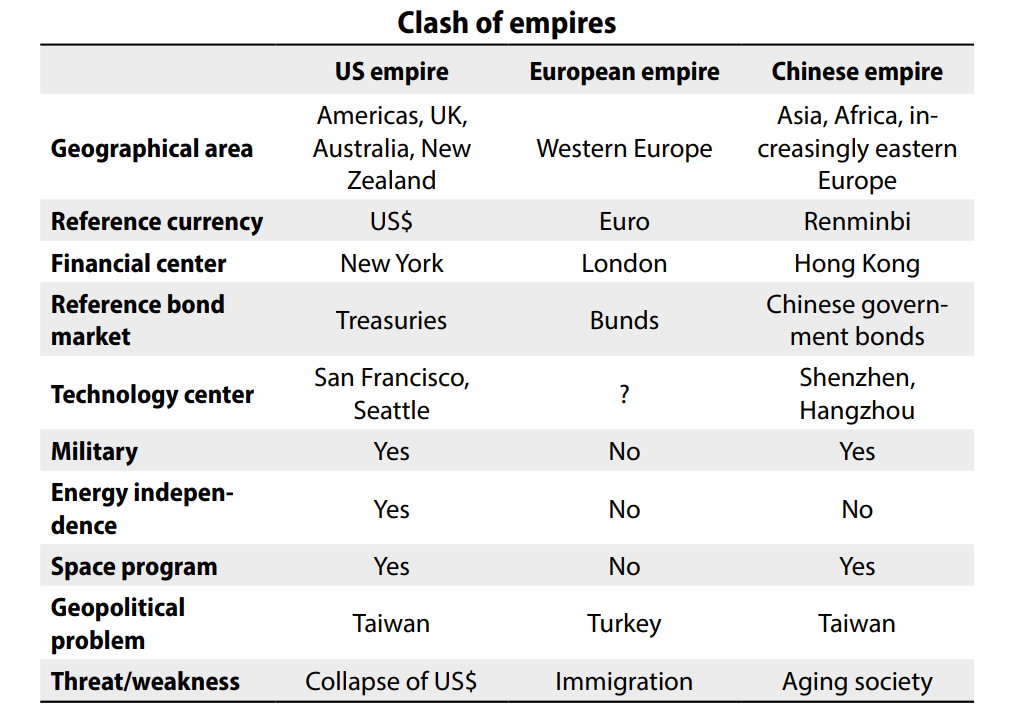

The publication of Clash of Empires at the start of last year marked a bookend to that period. No longer would supply chains be stretched across the globe. Instead, the world would break into three separate economic zones, each with their own currency of reference (US dollar, euro and renminbi), financial capital (New York, London, Hong Kong), bond market (treasuries, bunds, Chinese government bonds) and their own supply chains.

But this breakdown would present challenges.

For Europe, it is the lack of an army, space program or serious tech center. Also, after Brexit, its financial center will be outside its immediate borders.

For the globally-integrated tech world, the problem is that the US has identified this as a key battlefield for confronting China.

But this tech war is now having broader consequences. In one of the best pieces we published this past year, Dan Wang makes the following point.

“Chinese companies shudder at the thought of suffering the same fate as Huawei, which at a stroke found that it could not procure many of the components it needed to make its products. That has shown Chinese companies in all industries that reliance on US supply is a potential risk… Because the US government has introduced the possibility that supplies might be cut off at any time, Chinese firms are starting to look more at US competitors, in China as well as the rest of Asia. One sales manager at a US chemicals company confessed anxiety about this trend, as the high quality of its products is no longer a guarantee that customers won’t switch to another vendor.”

To put this another way, for 20 years, every company’s procurement process was driven by the price-to-quality ratio: could a potential supplier produce an adequate product at a low enough price point. That was then. Today, after actions against Huawei, ZTE, Semiconductor Manufacturing International Corporation, the equation, at least in China (the world’s second largest economy) has changed. Above all else, what now matters most is the security of the supply and the price-to-quality ratio has slipped down the list of priorities.

This represents a paradigm shift as “Ricardian optimization” is no longer the be-all and end-all. A world that worries more about safety than low prices is one that will likely deliver lower productivity, and higher prices.

Taiwan as the new geostrategic fault line

Staying with the idea that semiconductors are the key battlefield in the unfolding US-China “cold war”, the past year saw two important events:

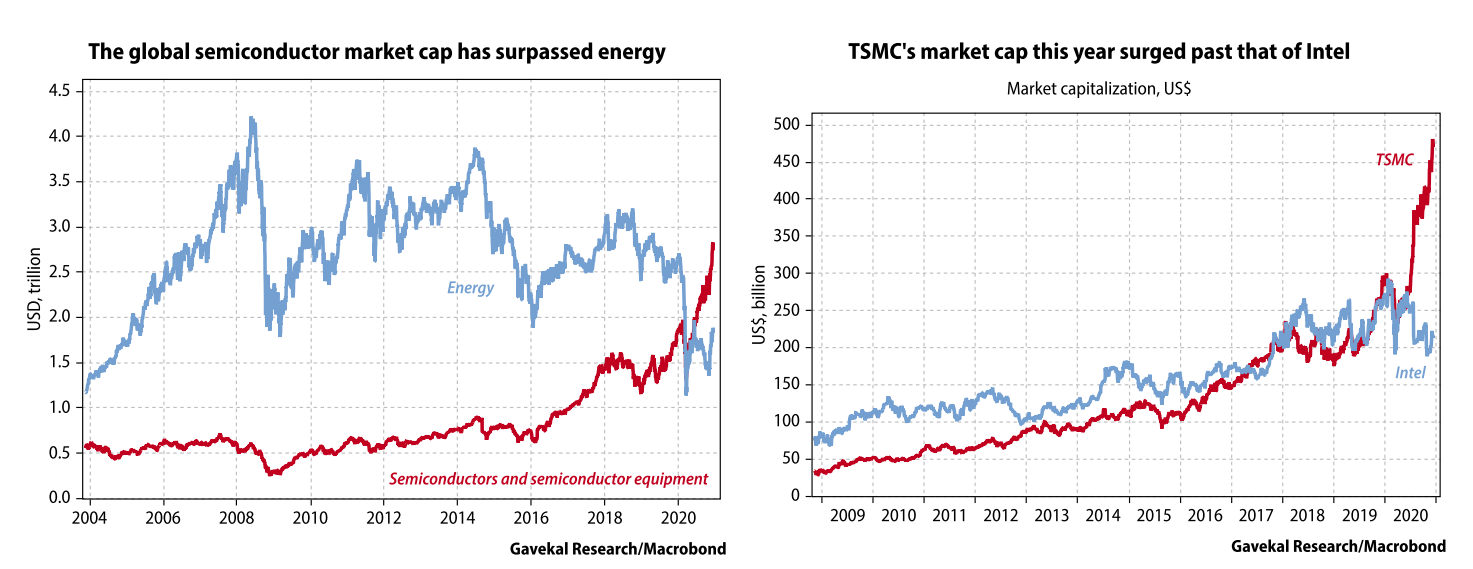

The global market capitalization of the semiconductor sector soared past that of the energy sector (see left-hand chart below). The market’s message was that chips are the commodity of the future while barrels of oil are the commodity of the past (whether the market is right on this is another debate).

A more important development came in July when Intel—the US firm that once ruled global semiconductor manufacturing—said it could not mass produce 7nm chips until 2023, some 18 months later than its guidance. Then just weeks later, Taiwan Semiconductor Manufacturing Corporation, which is already producing 7nm chips, confirmed that it will begin mass producing 3nm chips in 2022. In a nutshell, this means that the once-dominant Intel has lost its technological edge over TSMC, and is unlikely to regain it before 2025 at the earliest—if ever. Unsurprisingly, the market quickly adjusted to this new tech reality: the TSMC market cap more than doubled while the Intel market cap fell by more than a quarter (see right-hand chart below).

So to recap, the US has chosen to make semiconductors the battlefield in the unfolding Chinese Cold War at a moment when the US is losing its semiconductor manufacturing leadership, and to Taiwan, of all places!

This is a problem, as Taiwan has long been a source of potential instability in the US-China relationship. Even when the two countries sort of got along, and Taiwan produced plastic toys and bicycles, the disputed island state was a sore point in the relationship. Fast forward to today and the US and China no longer get along, while Taiwan is instrumental in producing the world’s most economically important commodity. The “passing of the baton” from Intel to TSMC could not have come at a worse time for the US!

In response the US is likely to sell Taiwan more weapons—which will infuriate Beijing and sour an already strained relationship. TSMC is being arm-twisted to move its wafer fabrication plants to the US and pressure is being applied to South Korea (the other key semiconductor producer) to pick a side between the US and China (interestingly, Seoul may decide that discretion is the better part of valor and move to become neutral—an Asian Switzerland of sorts).

Meanwhile, the first order of business for Beijing will be to continue investing in its domestic semiconductor industry in a bid to close the technology gap. Dan Wang and Matt Forney of Gavekal Fathom China have researched this in detail over the past year and published numerous papers on this topic. There are few reasons to think that the trend won’t accelerate since the ability to produce semiconductors domestically is no longer a business decision for China, but a national security one.

China’s second order of business will be to keep on investing in its military. There are solid historical correlations between strong military and a strong tech sector. The US has the world’s biggest defense budget and the largest tech sector. China has the second largest military and the second largest tech sector. Japan for years boasted the highest defense spending in Asia and is a credible tech player, as are Israel, South Korea and Taiwan, which are small countries that punch far above their weight in terms of military spending. In contrast, countries that used to spend on their military but no longer do, like France and the UK, have seen their tech sectors shrivel, with the eclipse of once proud national tech champions like Bull, Alcatel and Marconi.

The third order of business for China will be to ratchet up bellicose crossstraits rhetoric. The impact will be that both firms and individuals think twice about investing more in Taiwan, and may even reassess their dependence on components made in the island (i.e. the point above on supply chain security).

At the very least, these developments mean that a generation of geopolitical analysts who have spent their careers assessing every tiny shift in the greater Persian Gulf region will have to refocus on the Taiwan Strait instead. If only because each time the US cranks up the pressures on semiconductors, or its propping up of the Taiwanese military, China will likely respond by sending its ships through the Taiwan Straits and rattling its various sabers.

The financial front and the Hong Kong takeover

The other battlefront in the US-China Cold War is access to capital. In fact, the past year saw the following chain of events unfold: the US threatened China with an embargo of semiconductors that hold any US intellectual property (most semiconductors); China responded by launching naval maneuvers around Taiwan; the US reacted, saying that if China pushes too far, Chinese companies will be cut off from US capital markets or, worse, that Chinese banks will find themselves cut off from the US dollar system. This year also saw China respond by taking over Hong Kong.

The challenge for US policymakers is that kicking China off the dollar system would likely spur a global bust worse than the 2008 Lehman Brothers crisis. First, it would trigger a collapse in global trade (at a time when inventories are low). Second, many big US firms (Apple, Walmart, General Motors) rely on China for both production and final sales. And third because US corporates have invested over US$600bn in Chinese plants, property and equipment. Thus, kicking China off the US dollar system sounds like a hollow threat. It is one thing to kick off Iran, Venezuela or Sudan, all countries that, in the broader scheme of things, are roughly irrelevant to US corporations. To kick off China would be to invite an economic shock without precedent.

Still, because US policymakers have put such a course of action on the table, their Chinese counterparts must take it seriously. Hence the need to take control of the Hong Kong situation. After all, if Chinese firms are to lose access to US capital markets, Hong Kong can now present itself as the default choice to such orphans. Hence the need to internationalize the renminbi and present it as a credible alternative to the US dollar for trade settlement and reserve accumulation in Asia and across emerging economies more broadly.

Now, convincing China’s trade partners to drop the US dollar and embrace the renminbi is a tall order. And perhaps the best way to explain why is to return to the old Gavekal analogy of reserve currencies being akin to computer operating systems.

At Gavekal, we use Microsoft for two main reasons. First, most of our clients use it—and naturally, we want to be able to swap files with them. Second, because everyone else uses Microsoft, any new team member will be proficient in Word, Excel, PowerPoint and other products in the Microsoft suite. Thus, any new Gavekal hire is able to hit the ground running without a need for IT training. Hence, for Gavekal to switch from Microsoft to another operating system, the new system would have to be much more than marginally better; it would need to be so good that all our clients, and all our potential employees, would be compelled to make the switch in short order as well.

The parallels with the US dollar are obvious, as it is the Microsoft of the trading and reserve currency world. Everyone uses the dollar because everyone else uses the dollar. For any currency to replace it, the new currency would need to be not just marginally better, but many miles better. Today, nothing comes close, including the renminbi. Consequently, the US dollar remains the cornerstone of the global financial architecture.

In recent decades, Apple (and to a lesser extent Google) eroded Microsoft’s dominance in operating systems. Apple did so initially by focusing on niche markets. If you visit an architect’s studio or a web design firm, all the computers are likely to be Apple. But as Apple focused on capturing niches, it pretty much abandoned the big corporate IT system spend to Microsoft, which is why, back in 2005-06 Apple traded at eight times earnings. But then Apple blindsided Microsoft by launching the iPhone and creating a parallel operating system (iOS and apps) that did not need corporate IT departments’ backing to thrive. Instead, with iOS, Apple went straight to the consumer.

Why revisit this territory? Because if the US dollar is the Microsoft of global currencies, there is little doubt that in recent years China has tried to position the renminbi as its Apple. First, China tried to capture “niche” markets that were at best peripheral to the incumbent currency behemoth: financing intra-Asian trade, funding commodity imports into China, and financing infrastructure projects in places like Myanmar, Sri Lanka and Pakistan where, historically, infrastructure projects have struggled to attract funding. But owning niche markets only gets you so far.

So, let’s accept that the US dollar has too many advantages, like dominance of the SWIFT system, for the renminbi to challenge the US currency at its own game. Yet if we further assume that Xi Jinping is serious about establishing the renminbi as Asia’s main trade and reserve currency, China doesn’t have much of a choice: it must follow Apple’s example and build a parallel operating system that doesn’t try to compete with the US dollar on its own turf.

Which brings me to the drive shown by the People’s Bank of China to launch a digital renminbi and the clear attempt by the Chinese Communist Party to place fintech behemoths firmly under its control. Coincidences? Like Apple before them, the Alipays and Wepays of this world want to establish a new, parallel operating system that helps Chinese consumers (and increasingly consumers in other emerging economies) with payments and cash transfers that bypass SWIFT (and so US control). A digital renminbi will only boost this attempt further.

A rapidly shifting energy landscape

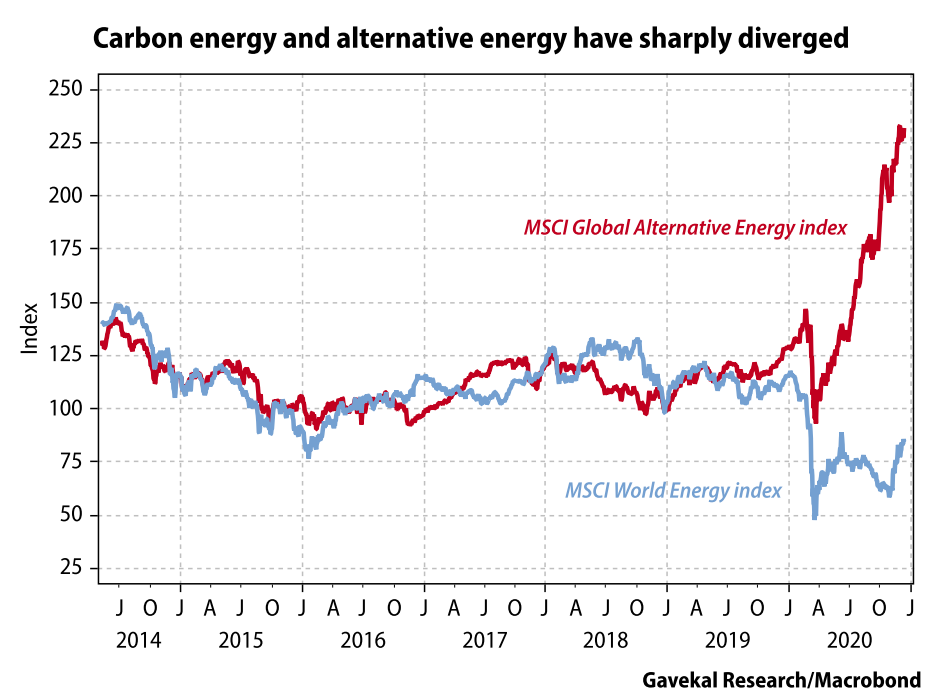

If a picture is worth a thousand words, few will be as space saving as the one below to describe energy investors’ year. Carbon energy companies and alternative energy companies produce the same thing: energy. The key difference is to be found in the way they do it. The former make it in dirty and reprehensible ways (or so the general consensus seems to go), while the latter produce it in the most virtuous manner (forget the needs for copper, lithium, cobalt, etc). This key difference is apparently enough to drive an unprecedented divergence in stock market performance between the two groups over the past nine months.

Another explanation for the performance divergence between green energy and carbon energy is linked to future government spending. As reviewed in Desperately Seeking Anti-Fragility (Part I), in a world in which government bonds are not the anti-fragile buffer of choice, investors face a bind. And the growth of green tech has appeared as a possible solution, with the following simple logic: the weaker economic growth is, the lower interest rates will be and the more Western governments will spend money to re-ignite activity. And spending billions on initiatives to stop climate change is an easy way to get money out the door, while also looking righteous. Better still, if green investments look like duds, governments can always increase regulation (no more carbon-driven cars) to ensure that money spent on green tech is not wasted, even if the result is a collapse in the broader economy’s productivity. After all, if growth ends up being weak because of new green regulations, interest rates will stay low, which then helps finance the next round of green investments. And if these investments underperform, governments can increase regulations to make sure that these investments appear wise, even at the cost of lower economic growth. Wash, rinse, repeat.

This impeccable logic has helped green tech become the new anti-fragile asset of choice, perhaps even replacing government bonds. But then, this likely means that green tech will, in the future, suffer a parallel fate to that of government bonds. For example, if interest rates across Western economies start to rise, will capital come out of the frothy green-tech space and return to the known shelter of bonds with yields (as opposed to the current shelter of bonds with no yields)? Or worse yet: what if governments find themselves in a situation where running multi-trillion deficits is no longer an option? Would green tech spending be the first sacrifice made?

For now, the rise of green-tech to anti-fragile status has helped contribute to the greatest ever underperformance by the energy sector of any broad S&P GSCI grouping. And following this underperformance, energy companies have little choice but to sharply reduce their footprint. Traditional energy firms are no longer rewarded by the market for delivering growth. The only thing they can do is return capital. To take a couple of examples:

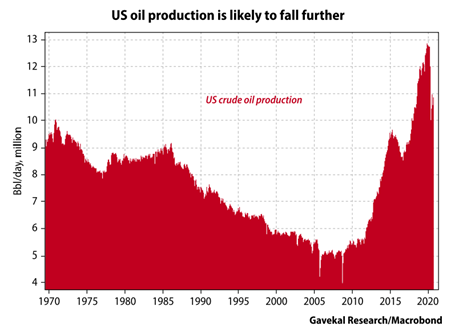

Chevron recently unveiled a capital spending budget of US$14bn-16bn a year through 2025. It represents a -27% cut from the midpoint of the company’s prior forecasts and is half what it spent in 2014.

ExxonMobil said that its capital spending will fall to US$16-19bn next year, and US$20-25bn from 2022 to 2025. Those figures represent a -46% and -31% decline, respectively, from the previous capex guidance.

These are the capital spending plans of North America’s two largest oil companies. The picture gets darker as smaller companies are considered. The prevailing theme across the oil and gas sector is of sector consolidation, mergers and outright bankruptcies. Hence, it seems fairly clear that US oil production, which has already started to shrink, is set to fall further. This will have negative consequences for the US trade balance, and thus for the value of the US currency.

From a north-south European divide to a west-east divide

The Covid pandemic hit Italy early, and particularly hard. And as Austria and France, and then the rest of Europe closed their borders to Italy, it looked for a few weeks as if the Covid crisis might be the straw that broke the back of the eurozone camel (it is said that a camel is a horse designed by a committee and what is the euro if not a currency designed by a committee?). Still, snatching an apparent victory from the jaws of defeat, Europe seemed to embrace a common fiscal solution to match its common monetary policy. This promise of a fiscal backbone and the hope that Europe’s north-south economic divide might be seriously addressed helped push aside fears of the euro’s survival. In turn, this planted the seed for the common currency to mount an impressive rebound over the past six months.

Still, even as the north-south split appears to fade away into the background, a new division has emerged in Brussels. This time the split is more of a west-east cleavage and has less to do with economic divergences than different cultural outlooks. At the risk of over-simplifying, Hungary, Poland, the Czech Republic and Slovakia (known as the Visegrád group, but also the old Austro-Hungarian empire!) do not want to change their immigration policies to suit Brussels while also typically having different approaches to “family/personal matters” (the Visegrád countries are usually against homosexual marriage, sometimes against abortion and oppose notions of gender fluidity).

At first glance, such fights may appear rather unimportant for investors. After all, the Visegrád countries have kept their own currencies and so are not subject to direct euro break-up risk. Their financial markets are also fairly small (not many global investors are in Hungarian bonds or Slovakian equities) and finally, cultural issues seldom have clear investment impacts. Still, notwithstanding last week’s EU summit fudge over a Brussels threat to sanction countries deemed to have breached the “rule of law”, these eastern countries, if pushed, could still upend the great fiscal compromise on which so much of the euro’s rebound rests.

But perhaps most importantly, the growing tensions between west and east in Europe further remind us that Europe, with its bastard political structures, remains an uncertain place for foreign investors to deploy capital. For Europe remains just one bad electoral result away (perhaps France in 2022 or Italy in 2023) from the whole edifice coming down.

Japan’s quiet bull market

This year will mark the point when the patient foreign investor who got sucked in to the Japanese hype of the 1989 bull market finally broke even (in US dollar terms) and the Nikkei 225 got back to its all-time high (the left-hand chart below does not include dividends).

In fact, for all the Japan-bashing out there (in fairness, most foreign investors have stopped railing against Japan and now simply ignore the place), Japanese equity markets have had a very honorable past decade. This is especially true when one strips out financials.

The above charts may bring comfort to Western policymakers now set on a path (unprecedented budget deficits funded through massive expansions in central bank balance sheets) trailblazed by Japan after its epic real estate and stock market bubbles of the late 1980s burst. Time will tell whether Japan’s experiment gets replicated elsewhere, or remains an anomaly in the annals of economic experiments. Indeed, as Kenneth Rogoff and Carmen Reinhart reviewed in their book This Time It’s Different, when massive expansions in budget deficits led to increases in government debt beyond the 100% of GDP (arbitrary) mark, and were funded with big rises in monetary aggregates, then in almost every case that country experienced either a currency collapse and a surge in inflation, or a debt default. Every country, except for Japan.

One reason that Japan proved to be such an anomaly is that, when its crisis hit, oddly it was one of the world’s most efficient export producers (with world class companies like Toyota, Sony and Nintendo) and probably one of the world’s most inefficient developed economies in its domestic market. Anyone who traveled to Japan in the late 1980s, or even through the 1990s, will have memories of US$10 apples in grocery stores, US$300 cab rides, US$500 pairs of Nike shoes or US$1000 a head dinners at Tokyo restaurants. All this when dollars were worth a good bit more than they are today!

Fast forward to today and all these “excess prices” have, through a three decade long deflationary process, been squeezed out of a Japanese economy that now looks and feels far more “normal” than its predecessor. Going out for the evening in Tokyo no longer entails taking out a second mortgage. If anything crystallizes the fact that the cost structure in Japan has now normalized, it must be the tourism boom of recent years (until Covid obviously stopped foreign arrivals dead in their tracks, see left-hand chart below).

But while big rises in budget deficits, funded with central bank printing, ended up having little impact on domestic Japanese prices that were being compressed by the squeezing out of inefficiencies, will the same thing happen across Europe or the US? Suffice to say that no-one today is paying US$10 an apple in the supermarkets of Chicago, Los Angeles, Paris, or Berlin. Instead, the inefficiencies to be squeezed out are few and far between. And perhaps more worryingly, instead of being squeezed out, inefficiencies are set to increase if, as described above, the security of supply now trumps price, or quality, as the determining factor for capital allocation and procurement decisions.

Meanwhile, Japan may well continue to thrive, quietly and unbeknown to most investors, in such an environment.

A last one, for the road….

When 2019 started, 10-year treasury yields were falling (and trading below their 200-day moving average), oil prices were falling (and trading below their 200-day moving average) and the US dollar was rising (and trading above its 200-day moving average). Fast forward two years, and we have witnessed a reversal in all three of these key price trends.

I would argue that these key price reversals are linked to the above 10 developments. But whether this is right, or not, may be not be that relevant. What matters is that bond yields, energy prices and the US dollar are now moving in the opposite direction to the one investors grew used to in recent years. The times, they are a-changin’ but have portfolios?

Federal Reserve Assets surged $120 billion last week to a record $7.363 TN. Fed Assets inflated $3.593 TN, or 95%, over the past 66 weeks. M2 “money” supply surged $228 billion in this week’s report to a record $19.226 TN – with a 66-week gain of $4.255 TN (28%). Overheated markets have become wholly enchanted by this frightening monetary inflation.

In early rules-based versus discretionary central banking debates, it was long ago recognized that discretion came with the risk of one misstep leading invariably to a series of only greater policy mistakes. This is the story of the contemporary Federal Reserve – from Greenspan to Bernanke to Yellen and now Jerome Powell. Policy doctrine has become progressively in the clutches of a runaway financial Bubble.

The Fed was out digging a deeper hole this week – an error compounded by Chairman Powell’s press conference dovish overkill. We’re in the throes of a period of precarious Monetary Disorder. This is apparent in Credit data and the monetary aggregates, throughout the financial markets and, increasingly, in housing markets across the country.

Financial conditions are precariously loose. Yet virtually everyone is convinced extremely loose monetary policy is appropriate considering the economic hardship being suffered across the United States. This thinking – utter reverence for monetary and asset inflation – has become only more perilous during the pandemic.

Powell responded to a question on elevated equities prices: “Asset prices is one thing that we look at… We published a report a few weeks ago on that… And I think you will find a mixed bag there… With equities, it depends on whether you’re looking at PE’s or whether you’re looking at the premium over the risk-free return. If you look at PE’s, they’re historically high. But… in a world where the risk-free rate is going to be low for a sustained period, the equity premium, which is really the reward you get for taking equity risk, would be what you’d look at. And that’s not at incredibly low levels, which would mean that they’re not overpriced in that sense. Admittedly, PE’s are high, but that’s maybe not as relevant in a world where we think the 10-year Treasury is going to be lower than it’s been historically, from a return perspective.” ( this statement will come back to haunt him)

December 14 – Bloomberg (Rich Miller): “U.S. financial conditions are the easiest they’ve been in more than a quarter century as stock markets scale new heights on hopes of an end to the Covid-19 pandemic, according to an index compiled by Goldman Sachs… The index, which dates back to 1990 and also takes account of the value of the dollar and interest rates, reached its loosest level ever last week. That came as financial markets have boomed, thanks to unprecedented support for the economy from the Federal Reserve and Congress.” (this is the reason that asset market are perky because excess liquidity has to go somewhere)

Evidence of egregiously loose financial conditions is everywhere. The Fed’s ballooning balance sheet. Unprecedented system “money” and Credit growth, along with the largest quarterly Current Account Deficit ($179bn) since 2008. Dollar weakness and the rapidly inflating cryptocurrencies. Record stock prices – across market indices from the S&P500 to the small caps. Massive ETF inflows.

There are myriad indications of conspicuous speculative excess: The Nasdaq100’s 47% y-t-d return, with a P/E of about 40. Individual company valuations with no basis in reality (i.e. Tesla’s $660bn mkt cap). A booming IPO marketplace. The SPAC phenomenon. Surging retail trading volumes (“Robinhood Effect”). The booming options-trading marketplace – retail and institutional – and, more specifically, the manic popularity of call option speculation. The blowup of hedge fund short-only and long/short strategies – with the Goldman Sachs Most Short Index surging 43% since the end of October and over 200% from March lows (up 53% y-t-d). Historically narrow corporate bond spreads (and low CDS prices) – in the face of major and mounting Credit impairment throughout the economy (households, corporations, state & local govt, etc.). Record investment-grade and high-yield corporate debt issuance. Booming private-equity and M&A.

In his press conference, Powell admitted the economy has proven more resilient to Covid spikes than the Fed would have anticipated. Clearly, economic activity has been bolstered by loose financial conditions, resulting booming equities and debt markets, and unmatched fiscal stimulus. But prolonging this addictive stimulant is fraught with risk. These risks do resonate with some Fed officials, with Robert Kaplan providing a voice of reason.

December 18 – Wall Street Journal (Patricia Zengerle and Eric Beech): “Reserve Bank of Dallas President Robert Kaplan said Friday that he believes it will be time for the central bank to start pulling back on its bond-buying stimulus efforts when it is clear the economy is recovering strongly. ‘I’m going to deliberately stay away from a timetable,’ Mr. Kaplan said… However, Mr. Kaplan said that as 2021 moves forward and vaccines to treat Covid-19 roll out, if the Fed is ‘making substantial progress on our dual mandate goals, I do think it would be healthy and very appropriate to begin the process of tapering our asset purchases.’ …Mr. Kaplan said he remains concerned extended periods of bond buying could bring problems. ‘These purchases, if they go on for longer than they need to, I worry that they have some distorting impact on price discovery, that they encourage excessive risk taking, and excessive risk taking can create excesses and imbalances that can be difficult to deal with in the future.’”

Abruptly redeploying QE in September 2019 – despite an increasingly speculative backdrop pushing stock prices to record highs (and with unemployment at multi-decade lows) – was a hefty blunder. QE should be recognized as a dangerous tool to be employed only in the event of systemic illiquidity precipitated by powerfully destabilizing de-risking and deleveraging (popping of a Bubble).

A measured QE response was appropriate in March. It is categorically inappropriate today – and arguably a dereliction of the Fed’s duty to safeguard system stability. Rather than supporting an unstable system’s adjustment to a changing financial and economic backdrop (as in 2008 and March), QE today directs powerful liquidity flows to already over-liquefied and highly speculative markets. Instead of accommodating deleveraging, $120 billion monthly QE at this late-cycle phase stokes speculative leveraging and only deeper structural maladjustment.

The Fed should at this juncture be preparing to “taper” – to commence a gradual process with the goal of policy normalization. It’s certainly no time to rationalize inflated securities (and housing) markets or to downplay what is obvious financial excess. And it is precisely the wrong time to further solidify the “Fed put” while emboldening an already manic Crowd of speculators. The Powell Fed has completely capitulated – and this is anything but lost on the markets. Our central bank has signaled to a frothy marketplace that massive (at least $120bn monthly) liquidity injections will continue indefinitely. It has become paramount to Fed policy to use its balance sheet to sustain market Bubbles for the purpose of spurring economic recovery. It is nothing short of our central bank abandoning its overarching monetary stability mandate.