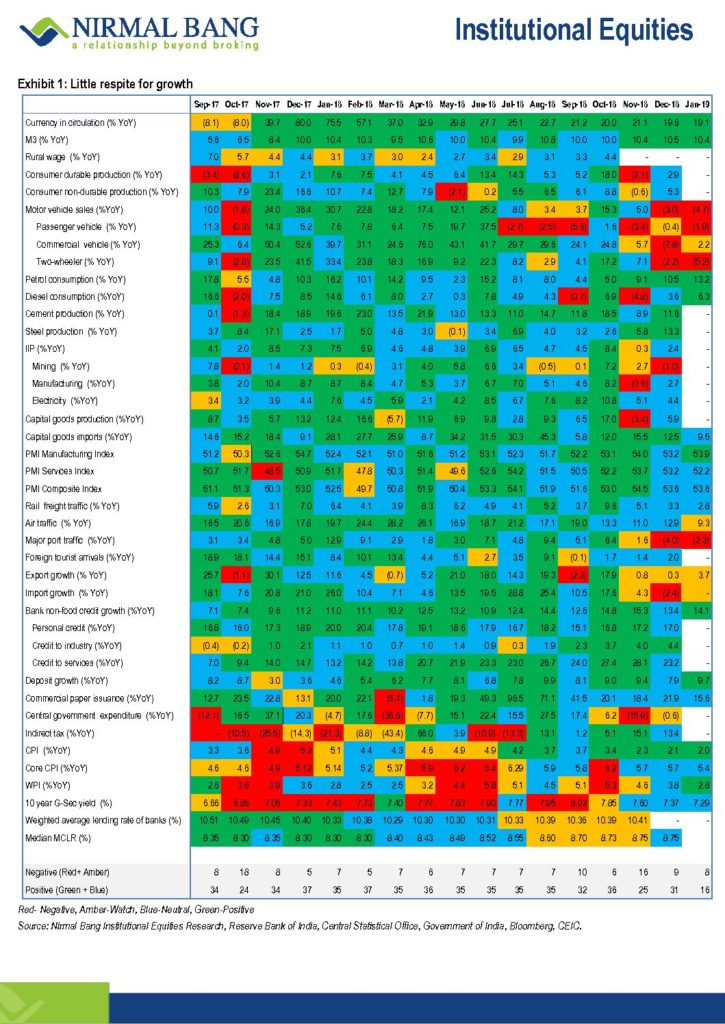

India Macro Economic Real indicators have been slowing down- as of Jan 19- Only 66.7% of indicators in positive territory in January down from 77% in December 2018.The govt is too indebted to do any meaning full capex. Corporate India is shying away from investing due to regulatory, political and technological uncertainity. Household were holding the forte till last year by going on a borrowing binge but that has also come to a halt.

Financial markets now believe that RBI will come out to rescue the economy by adding LIQUIDITY and cuting rates. I think they will try to experiment with easy money policies but the economy might not react so positively because India’s aggregate levels have been increasing faster than nominal GDP growth making it difficult for lower rates to provide meaning filip to the growth.

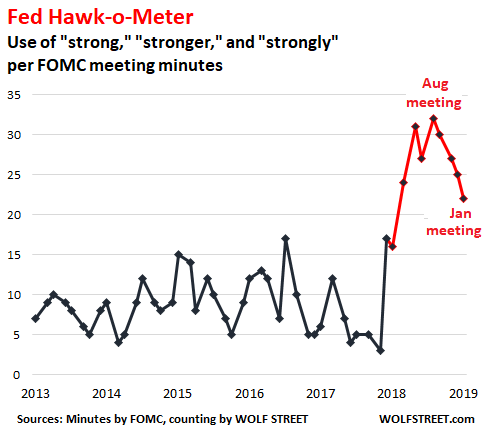

In the minutes of the January 29-30 meeting, released this afternoon, the mentions of “strong,” “strongly,” and “stronger” edged down for the fourth meeting in a row, this time by three points, to 22. The Hawk-o-Meter has now backed off quite a bit since the August 2018 high – when the Fed was rubbing it in that it would raise rates four times in the year – but it is still in outlier territory and redlining.

The G7 GDP volatility continues to trend lower.

A UBS tracker puts global growth at the weakest in a decade, with Germany & Japan seeing the biggest slumps in manufacturing

Nice chart showing the money companies spent during last 10 years on CapEx ($6.4T), buybacks ($4.9T) and dividends ($3.4T)

Recall the time

when David Einhorn came up with a devious idea of iPrefs to distribute the

massive cash that Apple was chewing among its shareholders in 2013. Instead of Apple

bowing to this idea, announced one of the biggest share buyback program and

planned to increase their dividend multifold to pacify investors demanding return

of their invested cash. Lesser known fact is that Apple had more than $130

billion in cash not in US but in Ireland and deploying a buyback would have required

them to bring that cash back in the States and pay huge taxes. Quick – witted Apple

did not disturb its cash sitting overseas but instead funded the buyback

through debt issuance and repaid the shareholders dividends through that loan.

It also committed itself to distribute over $100 billion to shareholders by the

end of 2015.

Since then,

Apple have being repurchasing shares frequently which has increased its share

price and ROE and kept their investors elated. The new normal for young

companies and big technological companies is to keep huge amount of cash in

their war chest and argue its necessity in future technological advancements

projects or acquisitions or a million other reasons. Yet, these companies have

kept their shareholders content by distributing dividends or repurchasing

shares and made their EPS look good.

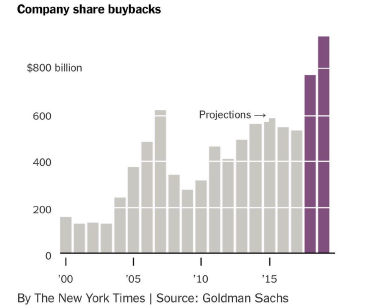

Flushed with

savings from lower tax rates and profits from a growing economy, big US

companies collectively spent a record amount of $1 trillion buying back their

own stock in 2018. Many argued that this led to further income inequality and

these companies should have invested the excess cash internally on projects or

by paying more wages to workers than distributing it to public. Some countered

by standing strong on theory that buybacks indicate a positive turn in a

company where these companies believe they are being undervalued by the market and

wish improve their valuation. Ed Yardeni of Yardeni Research points different

motivation for share repurchases and says, “S&P data suggest the aim of

buyback is to reduce dilution from stock compensation rather than to boost

EPS.”

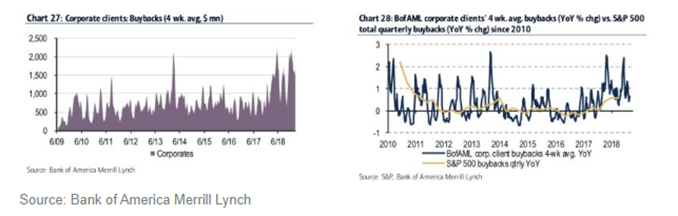

However, JPM estimates $400B of cash was repatriated between Q1 and Q3 while $190B was used for buybacks, $90B for corporate bond withdrawals and only $75B for Capex.

Buybacks funded

by debt issuance rose from 8% in 2010 to 32% in 2016 and the opulent brands

like Apple, Oracle, Microsoft, Cisco and many others announced big buyback

programs in 2018. Few argue that these

companies have exposed themselves to risk where if Fed goes in complete QT mode,

it would threaten these equity stocks.

Right now, major

shareholders like Mark Zuckerberg who owns stock in companies that use

repurchases exclusively can defer their own tax and their heirs can avoid taxes

altogether thanks to a loophole in tax code known as step – up in basis. Sen.

Marco Rubio proposed a fix for this as opposed to proposals by Sen. Bernie

Sanders and Sen. Chuck Schumer who suggested blocking the buybacks altogether.

When tax cuts

increased budget deficit, Republicans believed that tax cuts would boost

business investments. That didn’t happen and Rubio’s proposal tries to solve

this mystery.

Essentially, Rubio proposed that buybacks should be subject to same tax code as dividends i.e. would get taxed immediately instead of waiting for shareholders to sell the stock and also allowing these companies to immediately and fully deduct the cost of new investments, thereby making it more attractive.

The debate between two mind-sets in which one supports huge buybacks of 2018 emphasizing that it kept the money in circulation in the economy and boosted consumer confidence, other set effectively are of belief that excess buybacks could lead to stagnation of wages, increased inequality by enriching shareholders and executives. Corporations funded the buybacks from tax cuts instead of investing cash in internal growth. Rubio’s proposal implicitly aimed at making corporates think twice before repurchasing the shares and explore other value propositions rather than solely focusing on boosting EPS and be always in pursuit of higher ROE. Investing for long term and efficient use of cash could also keep fundamentals aligned as well.

WTO outlook collapsing faster than anytime since 2009.Something is not right but fear not Central Bankers will open another spigot of money.

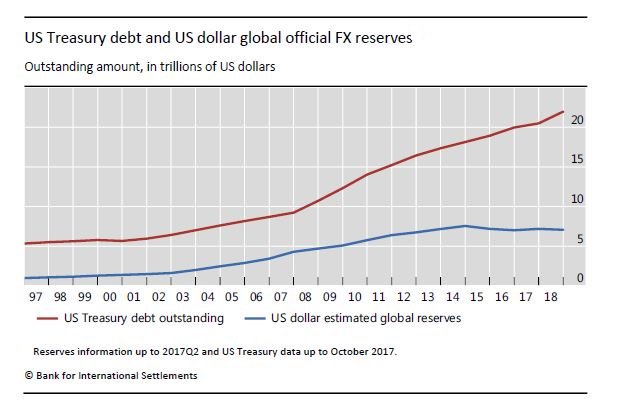

The supply of Risk free asset is rising faster than the demand from reserve managers. who will fund this?

The world monetary base is shrinking, only the sixth time since 1980 – each prior episode resulted in massive losses in Asian/EM equities (1982: -31%, 1990: -14%, 1998: -28%, 2000: -32%, 2008: -54% for EMs). In all five cases, Asia was in recession.

“The correlation of EM equities with the major central banks balance sheets is 0.94 in the past three years [and] world equities have a similar correlation of 0.94 since 2009”, BOFA writes before asserting that “central bank balance sheets are the most important driver of stock prices, in our view, by lowering risk premia, and cutting off deflation risk.”

The yield curve is almost on the verge of inversion. This is market way of saying that Fed has overshot on the rate hikes and who knows the next move is a rate cut?

At the time of this writing US markets are up 9 weeks in a row following the December lows making for risk free markets since Jay Powell famously caved on January 4th signaling flexibility on the balance sheet run off. Every tiny dip is bought and bears increasingly look the ones trapped, not bulls.

And the parade of central bank jawboning has been as spectacular as it has been global. Consider what signals have been sent to markets by central banks in just the past few weeks: The US Fed: No more rate hikes, flexible on balance sheet reduction, even open to stopping it altogether and discussing making bond purchases a regular tool, not just an emergency measure. I thought we were done with those? QE4 coming? The ECB: Discussing bringing LTRO (long term financing operation) back which would constitute another liquidity infusion. Didn’t they just end QE six weeks ago? BOJ: Ready to ease more. More? They never stopped and the BOJ famously owns more than 75% of the Japanese ETF market already. And China has added record liquidity infusions in 2019 desperate to provide liquidity to its lending market.

There is no doubt that this renewed global central bank capitulation has succeeded in levitating asset prices from the abyss in December. Greed is back, daily headlines hinting at a successful China trade deal to come and POTUS tweeting “up, up, up” all add up to a buying panic atmosphere.

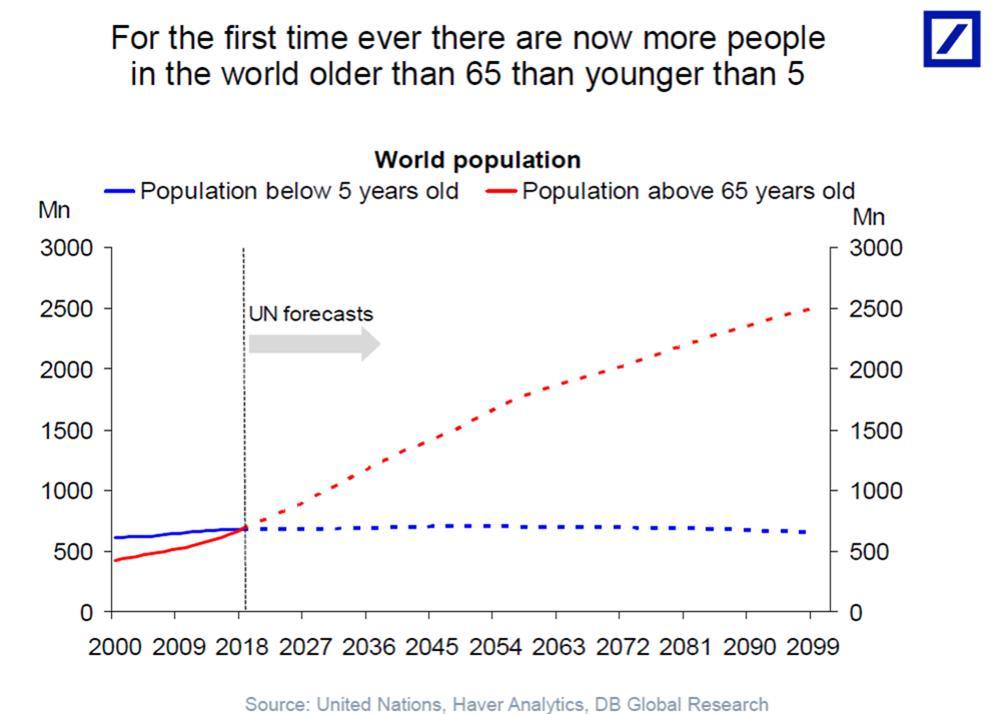

We’re running out of time, as a world, to fix our demographic problems. We’ve spent 20 yrs papering them over in debt + bubbles. It doesn’t get easier from here, and in fact it gets far worse, far faster. Many of these will be people who can sadly never retire.

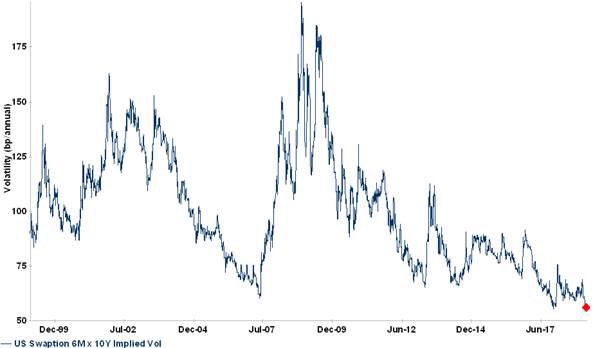

US rate vol at an all time low…..in fact the rates volatility has collapsed across the world

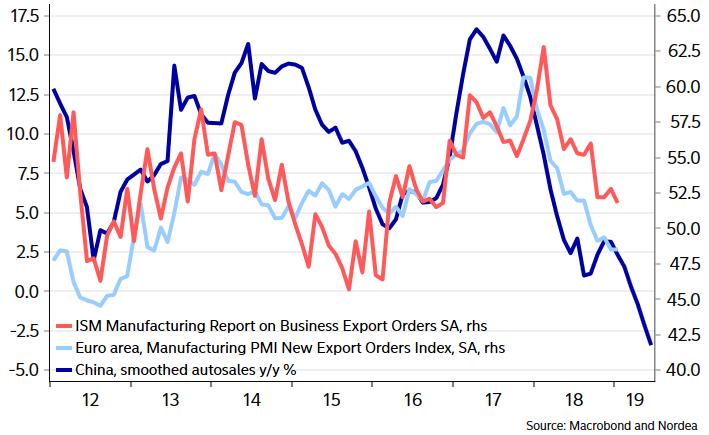

Chinese auto sales figures are plummeting ! Expect US and Euro area export orders to suffer more than already seen. China in itself is probably past the worst part, spill-over effects to US + Europe are still increasing. China currently awaits a meltdown in US manufacturing

Gold nearing the real test.

Extreme overbought and over bullish – Daily RSIs / DSIs:

Gold 73 = Highest since Sep 2017. DSI>85? Highest since Jan 2018.

US spends $8T more than trend to get 2% GDP growth it used to get organically. Businesses see the $8T + lever up; so do consumers. Asset bubble #3 fueled by that $8T. When bubble bursts, millions hurt again.

Teddy writes….The probabilities of US rates falling materially over the next six to eight months are the highest of the cycle. While global equities and commodities have begun to price in slowing growth, US rates are marginally off the highs – with the 10-year trading at 3.06%. The disconnect is likely due to supply and demand worries surrounding the Fed’s balance sheet run off, expanding US fiscal deficits, and the lack of demand from European and Japanese investors as hedged yields turn negative.

We see these concerns being largely priced into the market; however, the following line items seem they are not:

China will continue to pressure the global economy, with no real signs of stimulus coming through the system until the back half of 2019 under the assumption they will be able to expand credit at similar historical rates

The US economy will slow materially due to crude oil pulling down industrial production, as well as higher interest rates weighing on the consumer and US housing

US and Global Excess liquidity will drag equities lower, resulting in a bid for bonds

The Federal Reserve will likely get cold feet and backtrack as they recognize the economy is slowing

CTA and momentum players should continue to cover their shorts, in turn flipping momentum positive

Technically, US bonds are bottoming and have very favorable risk reward profiles over the following months

Given the above, we assign an 84% probability to 10 year rates falling to 2.3% from 3.06% over the next 6-8 months, before pausing and ultimately moving lower if our thesis is correct. Below we outline this thesis and seek to disprove the current bear argument.

Steven writes…..Credit markets often move before the equity markets, and this can offer helpful information about the near-term path of equity prices. In general, I like to see credit confirming what the equity markets seem to be saying. When credit stalls, like it is now, I take notice.

Investment grade spreads recovered about 30bps between January 3 and February 5, 2019. They have since widened out by about 2bps while the equity market is mostly flat.