This chart highlights why the German govt is orchestrating a merger of Deutsche Bank and Commerzbank. Germany’s 5y default probability trades in tandem w/ Deutsche Bank’s default risk as Deutsche is too big too fail and so doom loop alive & kicking.

This is Inflation

UNDERSTAND THE DIFFERENCE BETWEEN REAL AND NOMINAL Are wages up 9x since 1964 or are they up 0.1x ?

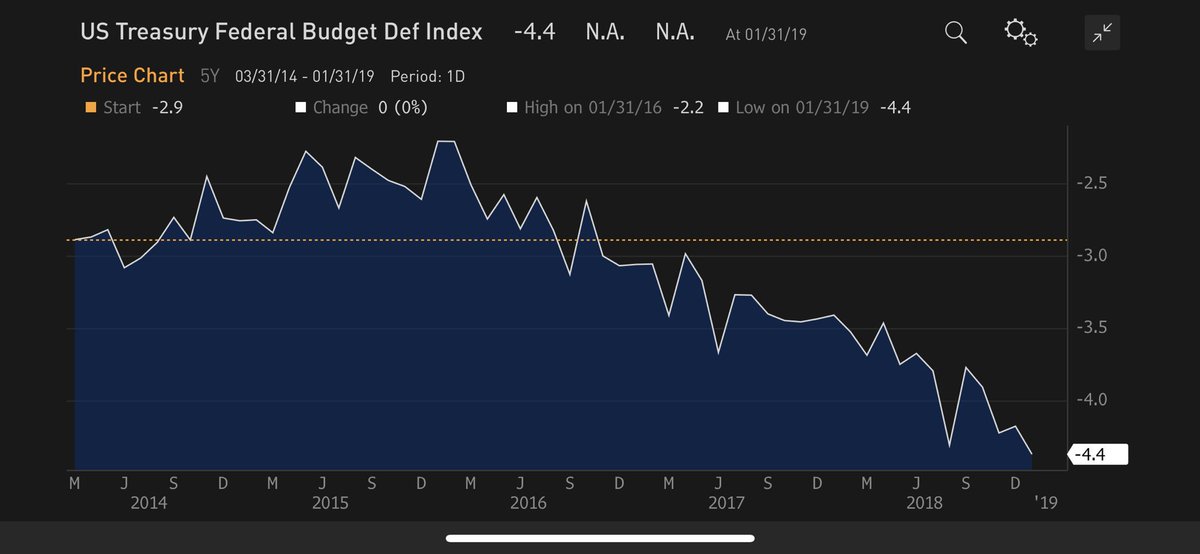

The US Budget deficit during the last 5 years!. Chinese stopped buying US debt in 2015 ,still US 10 year has barely budged in all these years

Tata had a

‘beginners luck’ when it acquired Jaguar and Land Rover in 2008 from Ford

Motors Co., named it Jaguar Land Rover Automotive PLC and launched Range Rover

Evoque which became huge success and a profit making machine for Tata’s. The

company’s market value soared above $29bn in 2015. Then came a speed bump.

China’s

government decided to phase out combustion engines joining UK and France to

eliminate gasoline and diesel engines by 2030. China and UK are the two largest

market in auto sector and JLR was heavily reliant on its sales in China and

production in UK.

First, sluggish

demand and collapsing shipments in China started a wave of realisation for JLR

that not all the reasons for its fall were global but also of ignored internal

quality control checks. Jaguar had 148 problems and Land Rover had 160 problems

per 100 vehicles. John Zeng, MD of LMC Automotive Shanghai said, “Quality issues have added to JLR’s troubles

in China where the company had multiple recalls. This has greatly jeopardized

Chinese consumers’ confidence in brand value. JLR’s quality control capability

and its after sales network are not good enough to support its volume expansion

or help it compete with rivals.” JLR is apparently restructuring its

network in China but is falling behind its German rivals such as Mercedes, Audi

and BMW.

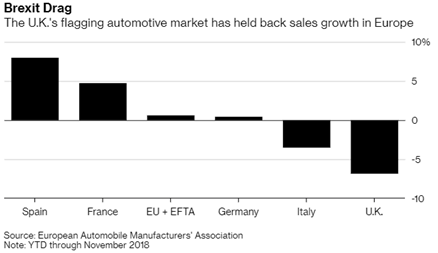

Second, it is exposed to risks of disorderly Brexit and it would be disastrous for JLR if Britain go for no – deal Brexit. They would be affected by disrupted trade flows between Britain and continent due to close links between assembly plants and suppliers on both sides of English Channel.

Europe’s

struggles include a broader economic slowdown with Germany at risk for slipping

into a technical recession after dramatic plunge in industrial activity late

last year. The slump in region’s biggest economy was partly driven by carmakers

battling to adapt to new emissions testing procedures which caused production

bottlenecks and sales gyrations across the regions, noted Bloomberg.

Third, Tata, India’s biggest conglomerate was caught in a power struggle when Ratan Tata fired his successor, Cyrus Mistry. The company decided to eliminate 4,500 jobs or about 10 percent of global workforce. The cherry on this cake was on 7th February it told investors about its plan to write down its JLR’s investment by $3.9bn.

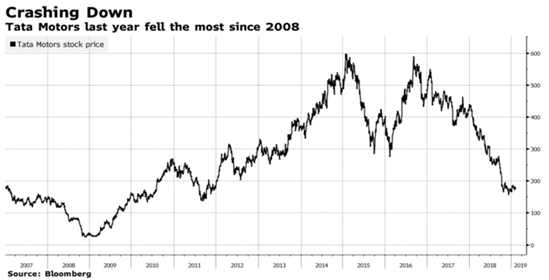

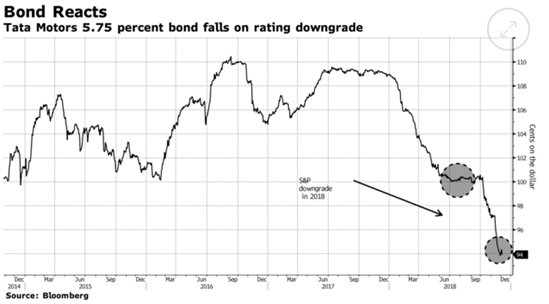

Tata Motors took a sharp fall and had their biggest drop in 26 years accompanied by being downgraded to BB- from BB by S&P Global Ratings for second time in five months. The icing around the cherry is that JLR also needs to raise $1bn in just over a year to replace maturing bonds, a tricky test for them given their debt in S&P’s junk category.

As per Tata,

this is all part of their plan. “As part of JLR’s plans to achieve 2.5 billion

pounds ($3.2bn) of investment, working capital and profits improvements by

March 2020, they would slash their global workforce by 4,500. This is expected

to result in a one-time exceptional redundancy cost of around 200 million

pounds for luxury unit of Tata Motors. The costs of voluntary scheme will be

recognised in quarter ending March 31.”

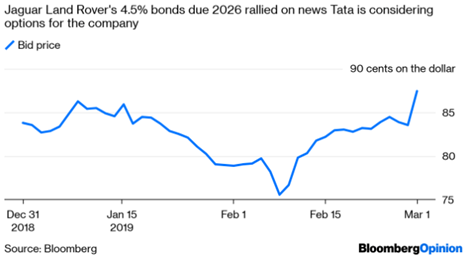

There are rumours of Tata exploring the possibility to sell its luxury car unit, Tata executives deny by implying a possibility of investing massively in UK though no formal statement has been announced. If this plan goes through it seems they could get some relief in tough weeks in the global economy.

JLR is also making efforts to step up in China and working a way around the Brexit uncertainty, without letting the corporate power struggle hindering them to make a mark again globally. Land Rover still ranks as most valuable major brands owned by Tata Group. The automotive marque was worth an estimated $6.2bn last year according to Interbrand. Tata’s like any other company are doing whatever is in their hand to revive the company

but what if as Bloomberg writes ….. on a macro level We have reached PEAK CAR SALES

US High Yield credit spreads at their tightest levels in over 3 months, 152 bps lower than Dec 27 levels. Credit always leads equities

The US consumer is a risk factor for the global economy. The US consumer accounts for 17% of global GDP and is more important than China. Deutsche Bank

Indiaspend writes “While the troubles of informal-sector workers and industry owners started after the Narendra Modi-government’s demonetisation programme–which invalidated 86% of India’s currency overnight–in November 2016, it was the implementation of the GST in June 2017 that led to unprecedented effects on small- and medium-scale industries, the primary employers of unskilled labour.

The effects are made worse in an era of Chinese imports. “Earlier we had seasonal employment during festivals, but now everything we use in our festivals comes from China,” said Gautam Kothari, president of an industries’ association in Indore’s Pithampur industrial area, and a former chairperson of a labour education centre run by the labour ministry. “Local people used to get jobs by making toys, lamps, but those job opportunities are no longer available.” A 5% increase in imports and decrease in exports can cost “thousands of jobs”, he added.”

The other side of the story which patriotic Indians don’t want to hear. Nytimes writes “It was an inauspicious moment for a military the United States is banking on to help keep an expanding China in check. An Indian Air Force pilot found himself in a dogfight last week with a warplane from the Pakistani Air Force, and ended up a prisoner behind enemy lines for a brief time.The pilot made it home in one piece, however bruised and shaken, but the plane, an aging Soviet-era MiG-21, was less lucky.”

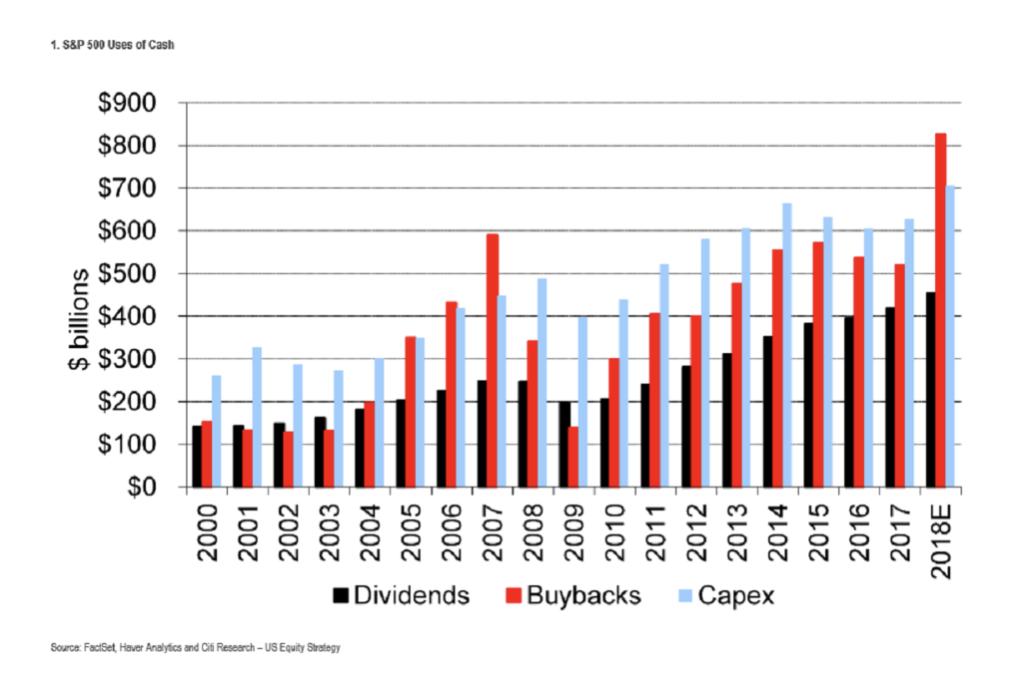

“Companies in the S&P 500 probably repurchased more than $800 billion of shares last year, an amount that surpassed the total they invested in new or upgraded plant and equipment. It’s the first time since 2008 that buybacks topped capital expenditures”Bloomberg

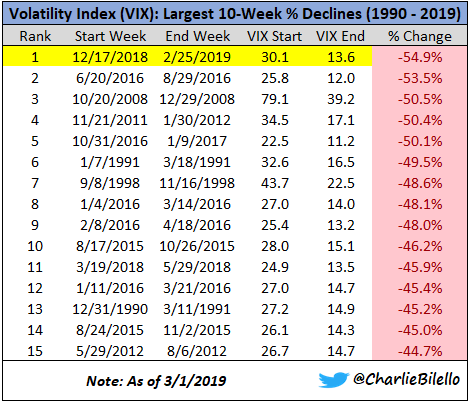

The Volatility Index has fallen 55% over the past 10 weeks, the largest 10-week decline in history. So much for Global Uncertainty

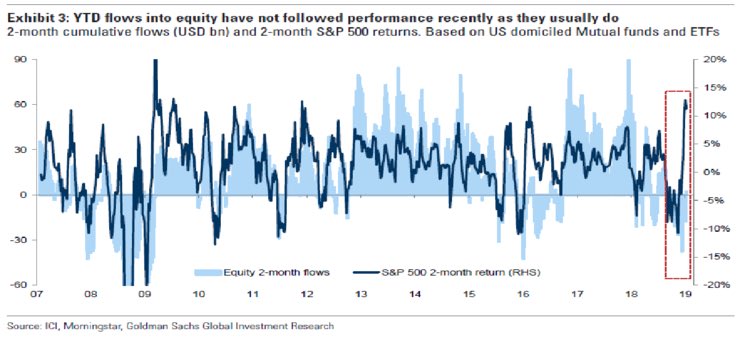

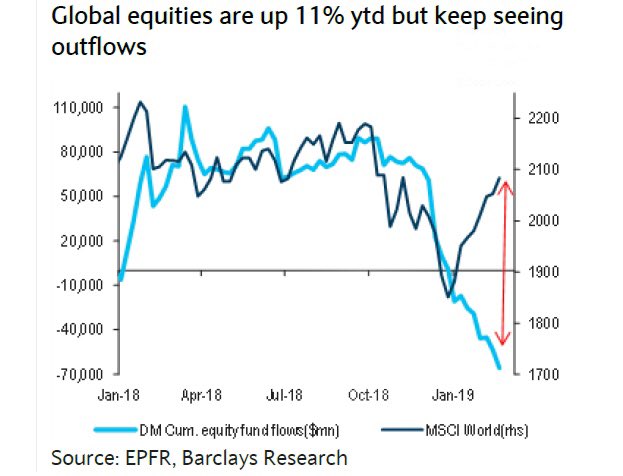

Looks like december finally put an end to the buy-the-dip mentality as equity fund outflows continue. Will they come back chasing? This is also happening in India where Fatigue and disillusionment is setting it.

The $22 Billion that is spooking the Indian Bond Market

The quantum of such semi-hidden public financing outside the Indian Govt books is around $22 billion, based on bond and loan-issuance data compiled by Bloomberg for the current fiscal year. With a month to go, this figure could surpass last year’s record of about $24 billion – and even that’s an understatement. The Food Corp. alone has borrowed $28 billion this year, according to an analysis by BloombergQuint, though more than four-fifths of that may have been from non-market sources such as the employees’ provident fund, postal savings and the Life Insurance Corp. of India. All this leads to crowding out where even lowering of interest rates also don’t help because the LIQUIDITY is getting sucked out.

Let’s embark on

a journey that began in the year 2000, one that was greeted with joy, now is

shunned by investors and called a ruin. A process called Fracking was

discovered in mid 2000s with which US created Shale wells and once a country

hugely dependent on crude oil imports plummeted to lowest level of crude imports

since 1967. Federal Reserve’s decision to keep interest rates about zero

percent in 2007 further bolstered the shale business and lured investors with

capital in exchange of promising lucrative returns and stable growth. How could

they have known that the energy with which shale boomed could also be doomed!

In 2014, oil

prices crashed, there was heavy crude sell – off, embedded options on oil

prices which were considered safe resort were no safer and they kept spiralling

down until February 2016! Shale producers revamped the production at the

expense of their longevity, depleted their long term reserves to maximise their

current production and now are under the gun by investors. Even though oil

prices rose considerably from its lowest in 2016, Capex remains 25 – 35% lower

than what it had in 2012 – 2014. According to Dealogic, companies raised about

$22bn from equity and debt financing in 2018, less than half the total in 2016

and almost one third of what they raised in 2012.

Shale industry

has had negative cash flows since its beginning and as Denning pointed out it

has not posted a return on capital above 10 percent any year since 2006 and IEA

estimated cumulative negative free cash flow of over $200bn between 2010 –

2014. Many however, overlooked the fact that McLean highlighted in the book ‘Saudi

America’ which said, “The ability of oil and gas exploration companies to tap

into underground formations is a result not only of technology but just as

important of cheap capital. The fracking boom has been fuelled mostly by

overheated investment capital, not by cash flow.” WSJ phrased this as, “A feature of shale, not

a bug.”

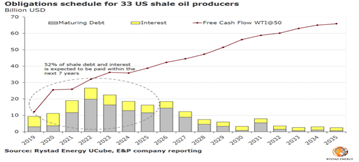

McLean further indicated that the very structure of shale business had fault lines. “For all the hoopla about the surge in US oil and gas production from fracking, most people overlook an important feature of the boom: The average shale well produces most of its oil or gas in first two years. That means oil companies must keep drilling new wells to keep production steady. To maintain production of 1 million barrels per day, shale requires up to 2,500 wells while production in Iraq can do it with fewer than 100.” Now, shale companies are under the radar and investors demand them to either be self – supporting or to return their invested cash. They find themselves straddled with depleting reserves and stalling gains from shale exploration productivity. Rystad Energy Senior Analyst Alisa Lukash said in her statements that, “E&P struggles to please equity investors and reduce leverage ratios simultaneously. Despite a significant deleverage last year, estimated 2019 free cash flow barely covers operator obligations, putting E&Ps on thin ice as future dividend payments in question.” Rystad finds that over half of the total debt pile for 33 companies it analysed is due within next seven years. Ultimately the industry will have to erase $4bn promised dividend payments.

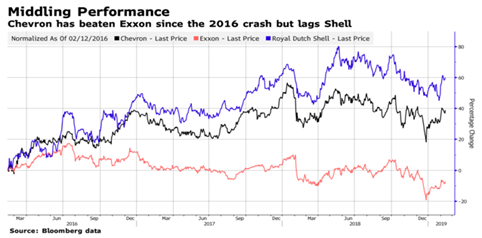

Amid dark clouds, the two big players ExxonMobil and Chevron remain optimistic. ExxonMobil recently said that its oil and gas reserves rose nearly 23 percent last year driven mainly by increases from holdings in US Shale (Permian basin), offshore Guyana and Brazil. US crude oil production has hit a milestone in August when it exceeded 11 million barrels for the first time according to Federal Energy Information Administration. When the survival of small shale companies is on the edge, many investors argue that M&A activity where the big multinationals absorb small shale companies could be profitable for everyone with big companies keeping more shale basins and small with continued operations.

West Texas

Intermediate (WTI) futures hit the highest level in February since November

with a barrel for March delivery at $55.93. The rally is driven by political

uncertainty, OPEC cuts and worries about slowdown in shale production is seeing

a rush out from short positions. Hedge funds abandoned their short selling bets

in January after oil had its best month in three years.

I would end this journey by quoting McLean, “Even today, it is unclear if we look back and see fracking as the beginning of a huge and lasting shift or if we wistfully realizing that what we thought was transformative was merely a moment in time.”

The automobile—once both a badge of success and the most convenient conveyance between points A and B—is falling out of favor in cities around the world as ride-hailing and other new transportation options proliferate and concerns over gridlock and pollution spark a reevaluation of privately owned wheels. Auto sales in the U.S., after four record or near-record years, are declining this year, and analysts say they may never again reach those heights. Worldwide, residents are migrating to megacities—expected to be home to two-thirds of the global population by midcentury—where an automobile can be an expensive inconvenience. Young people continue to turn away from cars, with only 26 percent of U.S. 16-year-olds earning a driver’s license in 2017, a rite of passage that almost half that cohort would have obtained just 36 years ago, according to Sivak Applied Research. Likewise, the annual number of 17-year-olds taking driving tests in the U.K. has fallen 28 percent in the past decade.

Meanwhile, mobility services are multiplying rapidly, with everything from electric scooters to robo-taxis trying to establish a foothold in the market. Increasingly, major urban centers such as London, Madrid, and Mexico City are restricting cars’ access. Such constraints, plus the expansion of the sharing economy and the advent of the autonomous age, have made automakers nervous. That’s also pushed global policymakers to consider the possibility that the world is approaching “peak car”—a tipping point when the killer transportation app of the 20th century finally begins a steady decline, transforming the way we move.

Rather than signaling the end of the road for the automobile, peak car is a reflection that reurbanization and the widespread adoption of mobile apps that can summon a vehicle on demand will lessen the need for many of the 1.3 billion vehicles now on the road. And with new cars increasingly expensive, but mostly used just a few hours a day, the financial case for alternatives is growing stronger. “When you put all these trends together, you’re going to see a cap on personal vehicle ownership start to emerge,” says Mike Ramsey, an automotive consultant with researcher Gartner Inc. “We are near peak car.”